vofpalabra/iStock via Getty Images

My first job was delivering newspapers when I was around 14 years old.

My mom had bought me a moped, and I was excited to start working. So what that if I had to be up at 4:00 in the morning?

I needed money to put gas in my new toy!

I would drive over to pick up the newspapers well before the sun was up, then spend about an hour rolling up each one and packing them in my quiver.

By 5:00 a.m., I’d be rolling.

My route included around 50 houses, which meant 50 households relying on me to have their news to them every day.

Rain, sleet, or snow, those papers had to show up. No excuses allowed.

If I was sick, I still had to work.

If my moped broke, I would have to use my bike.

If I’d stayed up late the night before or “just needed a personal day,” I was out of luck. There was no such thing.

There were simply no excuses.

There were, however, plenty of rewards to this strict schedule. And not just in the equally steady paycheck…

You Gotta Give the Customers What They Want

That first job of mine was actually two-fold. I delivered “the goods” every day to my customers and collected their payments once a month.

For that second responsibility, I had to knock on their doors and interact with them face-to-face. These were particularly good days for me since I’d usually get tipped along the way.

Why?

I recognized that, if I delivered 100% customer satisfaction, they would make it even more worth my while. So I determined very early on to do precisely that.

As it turned out, that led to even more moneymaking opportunities. I remember one customer asked me to cut the grass – allowing me to rack up another $100 per month.

Another asked me to take care of her pets, giving me another $50 per month.

It didn’t take me long to save up $1,000 that way. And believe me, that was a lot of money back in those days.

In fact, I quickly accumulated over $3,000… all from committing to give my customers what they wanted: a paper on their doorstep every morning.

That’s how my friends started calling me the “Piedmont Paper Punk,” a title I had no problem accepting. They were jealous because I was racking up that cash.

Who could blame them?

So now you know why I’ve written over 5,000 articles in 14 years, publishing an article every single day – seven days a week – for so many years.

Rain, sleet, or snow. No interruptions or exceptions are allowed.

That’s all important if you want a successful, exemplary career. You always need to:

- Understand your customer

- Deliver on your commitments

- Go the extra mile when appropriate.

And, of course, you need to know how to rack up the cash flow, which is the main point I’m driving at today.

Let’s Talk About Dividends

It’s been a while since I applied for that paper boy route. But I’m pretty sure I knew from the get-go that tips could be part of it.

In which case, there’s one more very important lesson I learned from it…

Always look for dividend-paying opportunities. Because dividends have positive consequences.

For starters, they suggest the company’s earnings power is strong. They also provide investors with valuable signals about management’s willingness to reward shareholders instead of overpaying themselves.

Dividends impose discipline on managers, who know that once a dividend is paid just once… investors expect it to be paid again and again without fail.

Just like my newspapers.

Also similarly, a sustainable dividend policy tends to create the “clientele effect.” This means that their stockholders are happy and therefore less likely to dump shares.

In fact, they’re likely to even reinvest those dividends, helping the company to grow even more… and offer even better dividends down the road!

Last but not least – and this is a proven fact – stocks that pay sustainable dividends fluctuate less than stocks that don’t.

In the 1980s, Michael Jensen of Harvard University proposed the free cash flow theory. It states that free cash flow acts as an effective monitor of corporate managers.

(Yup, we’re back to management again.)

The basic premise is that good managers with proper checks and balances will deploy free cash flow efficiently by investing in new projects, increasing dividends, or repurchasing shares. Their stocks are less prone to bad news as a result.

As a reminder, real estate investment trusts (REITs) MUST pay out at least 90% of their taxable income. And most payout is close to 100%.

This means their dividends are even more frequent and sustainable. So let’s get to my list of four extremely predictable REITs…

Come rain, sleet, or snow.

Realty Income Corporation (O) – 5.6% Yield

When it comes to reliable income and steady growth, Realty Income is the place to be.

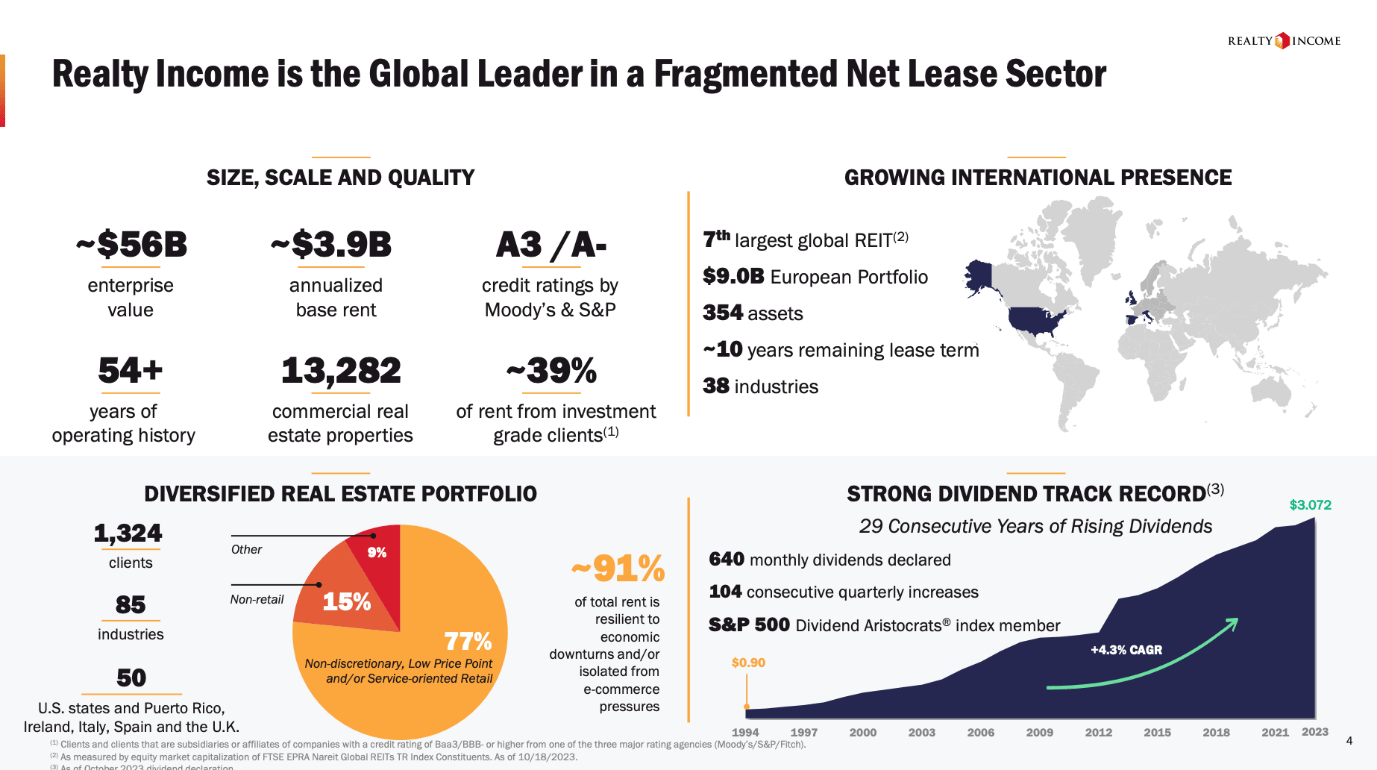

One of our favorites isn’t just America’s largest triple-net lease retail REIT but also a company with a track record that most cannot compete with.

The company, which calls itself “the monthly dividend company,” has an enterprise value close to $60 billion.

It has a history of more than 50 years and a track record of 29 consecutive years of dividend growth, making it one of the few dividend aristocrats in its sector and a member of the S&P 500 Dividend Aristocrats Index.

Since 1994, the dividend has been hiked by 4.3% per year, which is a lot for a high-yield stock. Over the past five years, that number has dropped to 3.7%, which is still decent.

Realty Income

Its portfolio includes ownership in over 13,000 commercial properties located across all 50 states, the United Kingdom, Spain, Italy, and Ireland.

The predominant focus of Realty Income’s portfolio is on single-tenant, free-standing commercial retail properties.

Additionally, there are holdings in industrial and gaming properties, although they constitute a smaller percentage.

Breaking down the portfolio, approximately 83% of annual rent comes from close to 13,000 retail properties, 13.1% from 364 industrial properties, and 2.6% from 1 gaming property (Encore Resort and Casino). That’s the Encore Resort and Casino in Boston, not the one in Las Vegas.

Realty Income

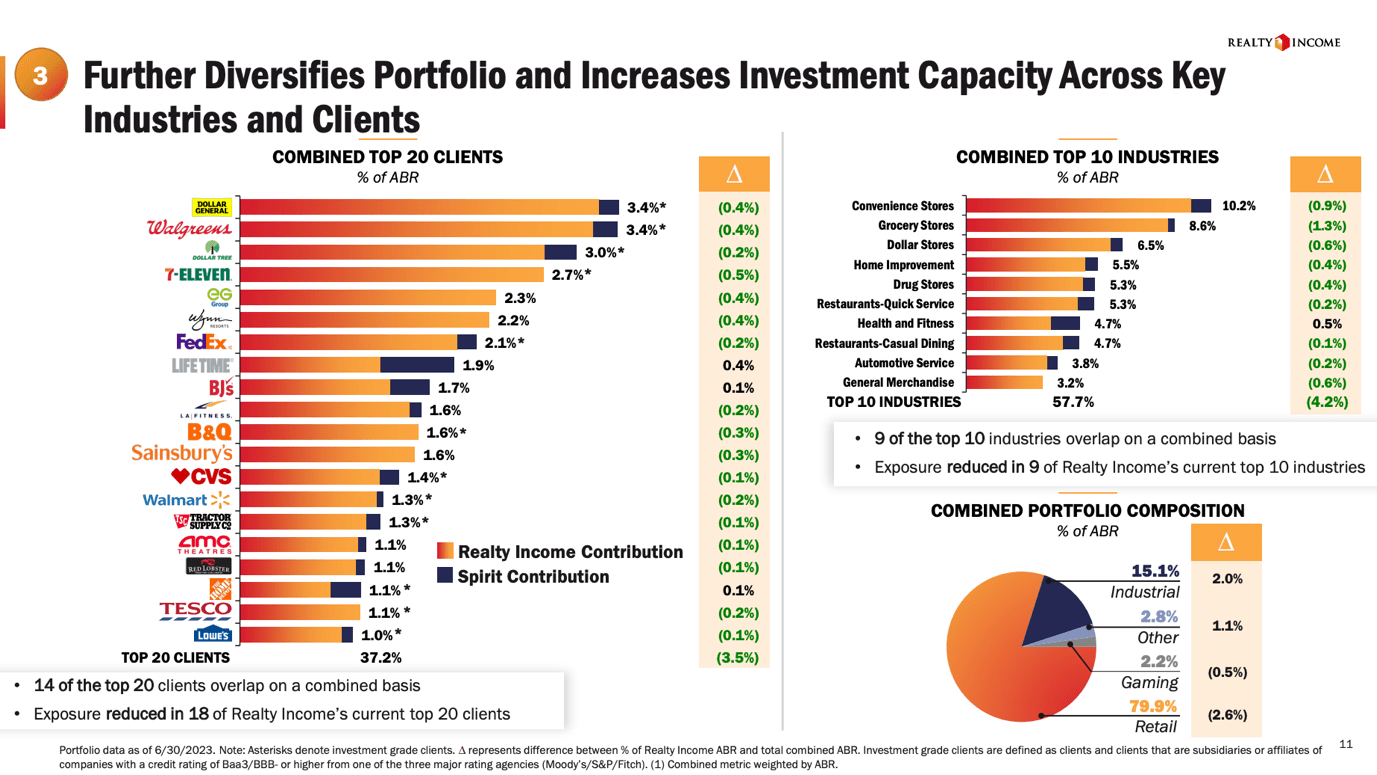

Speaking of Las Vegas, recent developments include a joint venture with Blackstone Real Estate Income Trust (“BREIT”) to acquire an interest in the Bellagio Las Vegas and a merger agreement with Spirit Realty, further diversifying O’s portfolio and increasing exposure to gaming and industrial properties.

The combined Realty Income/Spirit company would have an even bigger footprint in assets rented by the nation’s largest corporate tenants.

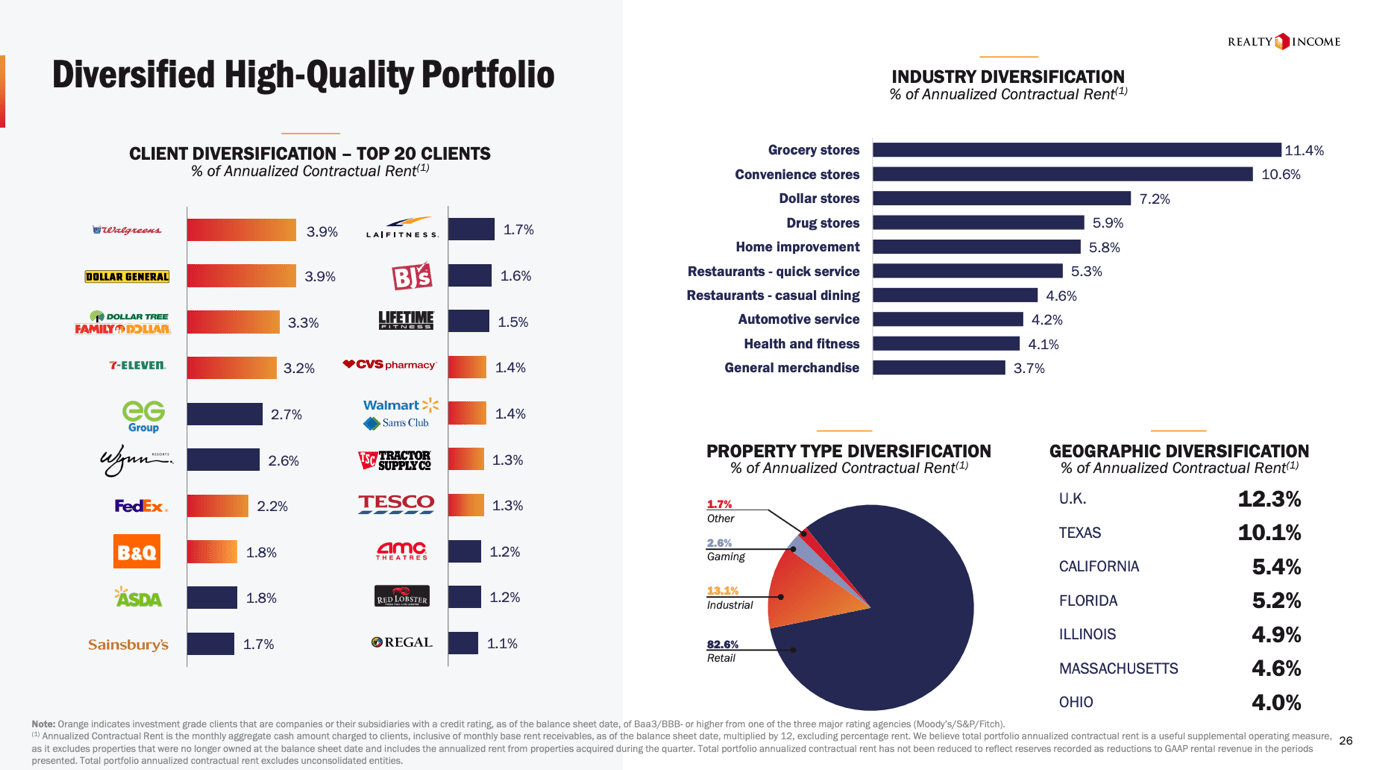

Looking at the chart below, we see that the combined portfolio would see high exposure to safe tenants like Dollar General (DG), Walgreens (WBA), Dollar Tree (DLTR), and 7-Eleven.

More than a quarter of the company’s rent would be generated in anti-cyclical segments like convenience stores, grocery stores, and dollar stores!

Realty Income

Especially in this tricky environment of poor consumer confidence and elevated rates, Realty Income has proven its stability.

As of the end of the third quarter of 2023, Realty Income reported an impressive portfolio occupancy of 98.8% and a weighted average lease term (“WALT”) of 9.7 years, which contributes to the “sleep well at night” aspect of this investment.

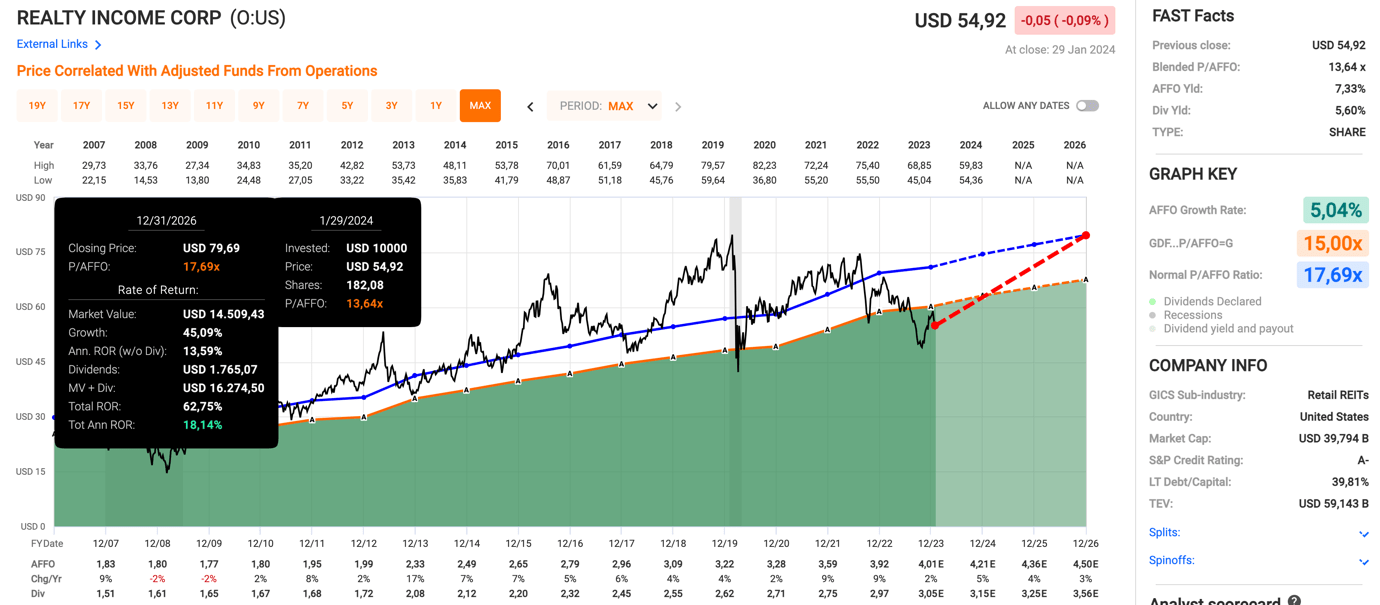

With regard to its performance, since 1994, the stock has returned 13.4% per year with a beta of 0.5 versus the S&P 500. In other words, investors outperformed the market with subdued risk!

Speaking of outperformance, because of elevated rates and sticky inflation, Realty Income trades at a discount.

Using the data in the chart below:

- Realty Income trades at a blended P/AFFO (adjusted funds from operations) of just 13.6x. The company’s normalized valuation is 17.7x.

- This year, AFFO is expected to grow by 5%, potentially followed by 4% growth in 2025 and 3% growth in 2026.

- While the discount is currently warranted due to the threat of prolonged elevated funding rates and inflation, the company remains strong due to its strong balance sheet with an A- credit rating, sale-leaseback benefits, safe tenant portfolio, and elevated occupancy rates.

- If the company gradually works its way back to 17.7x AFFO over the next few years, it could return between 15% and 18% per year, including its dividend.

FAST Graphs

Sure, it may take a while until the market gives strong REITs the valuation they deserve. However, for investors looking for great value, that’s great news, as nothing beats buying great companies below “fair” value.

Hence, Realty Income has an iREIT® Buy rating.

NNN REIT, Inc. (NNN) – 5.5% Yield

If you like Realty Income, you’ll like NNN REIT as well, which is formerly known as National Retail Properties.

One thing I like about NNN is that it is much smaller than Realty Income. With a $7.6 billion market cap, it is much easier to grow without having to engage in multi-billion dollar deals like Realty Income.

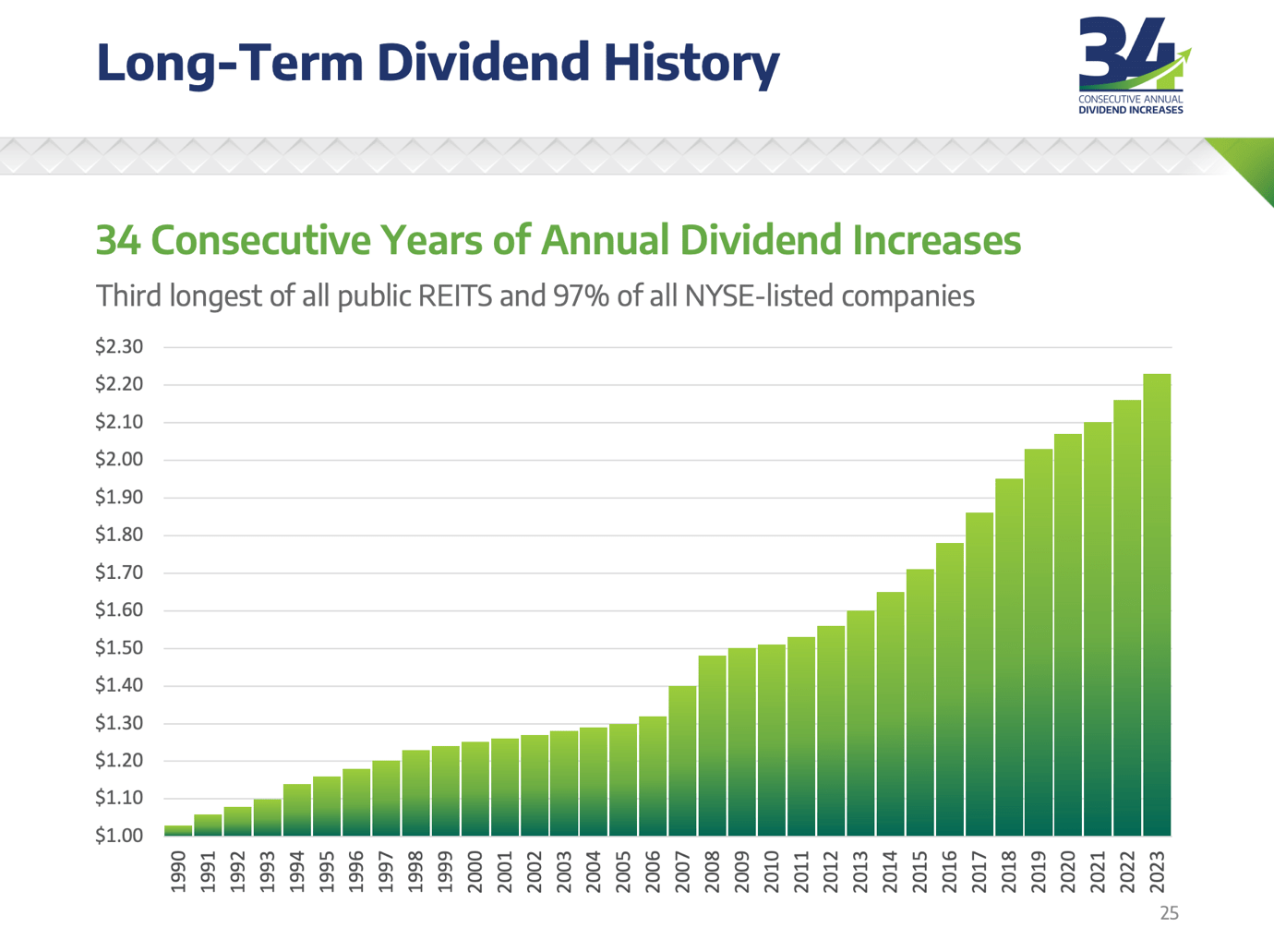

The company, which is a triple-net lease REIT like Realty Income (it’s also literally in its name), specializes in single-tenant net lease retail properties and boasts an impressive track record of 34 consecutive annual dividend increases, making it a dividend aristocrat as well.

NNN REIT

Last year, the company raised its dividend by 2.7%, aligning with the five-year dividend CAGR of 2.7%. NNN pays a quarterly dividend.

While the dividend growth may not be groundbreaking, it is consistent, embodying the essence of high-quality income investments.

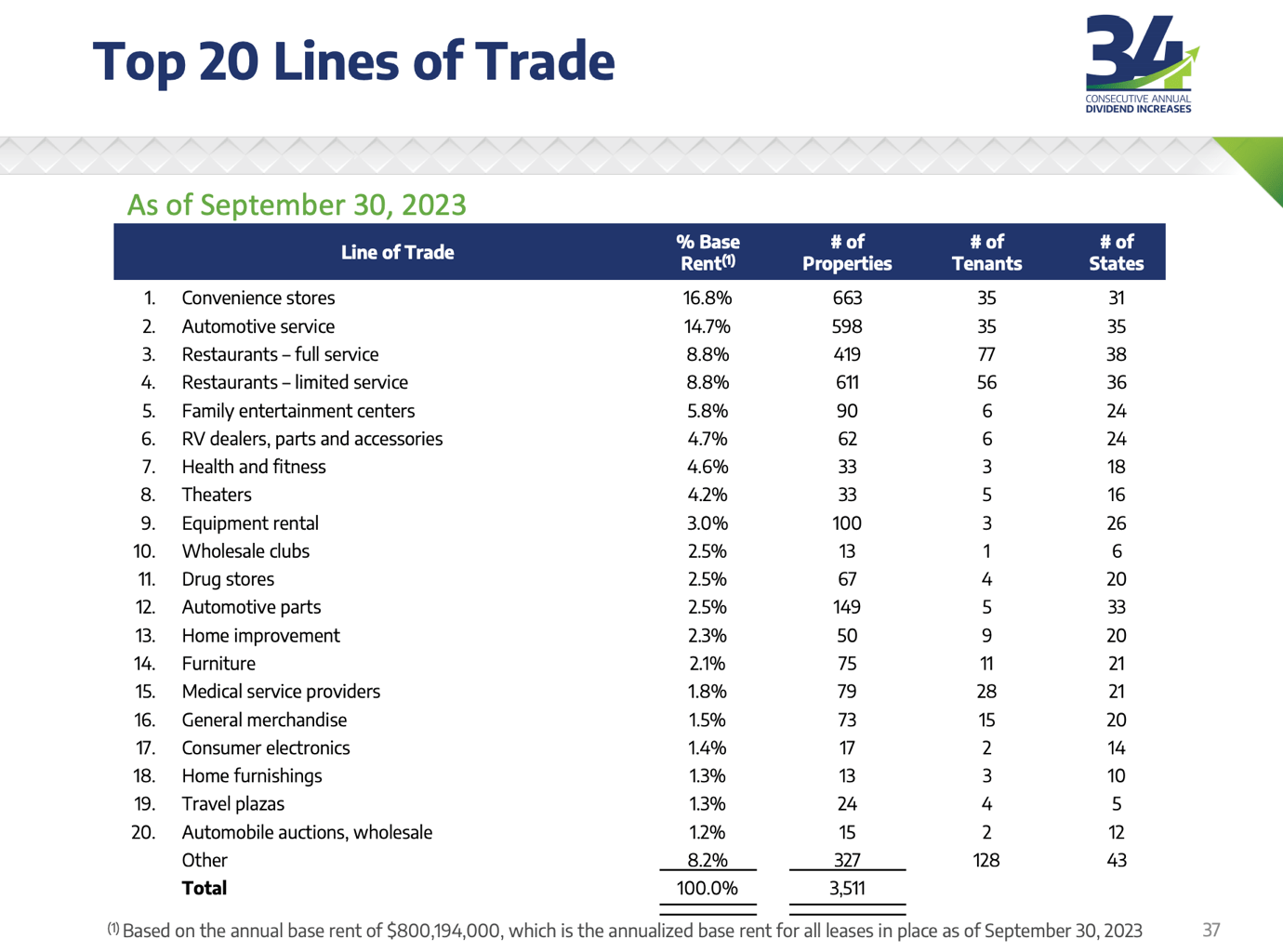

Going back to its tenants, with a diverse tenant base, including convenience stores, automotive services, restaurants, entertainment, car dealers, health and fitness, NNN stands on solid ground.

NNN REIT

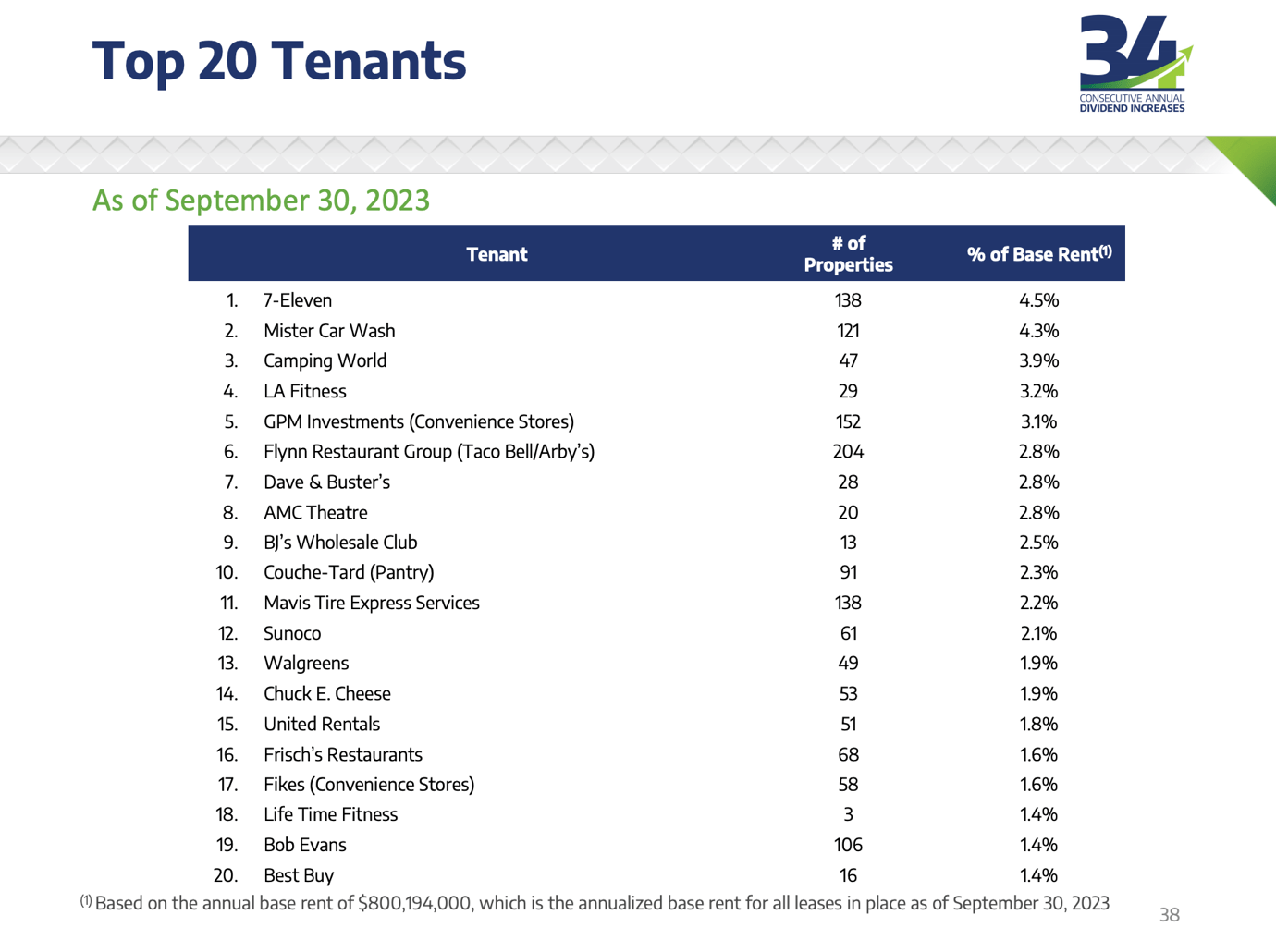

The largest tenant, 7-Eleven, contributes 4.5% of the annual base rent, and a mere 2% of leases expire through 2024, with a weighted average remaining lease term of 10.1 years.

NNN REIT

Moreover, NNN boasts a BBB+ credit rating, just one step below the A-range.

Its debt features an average weighted effective interest rate of 3.9%, an average weighted maturity of 12.6 years, and less than 8% of its debt due before 2026. The interest coverage ratio is a robust 4.6x, making it one of the strongest REITs on the market.

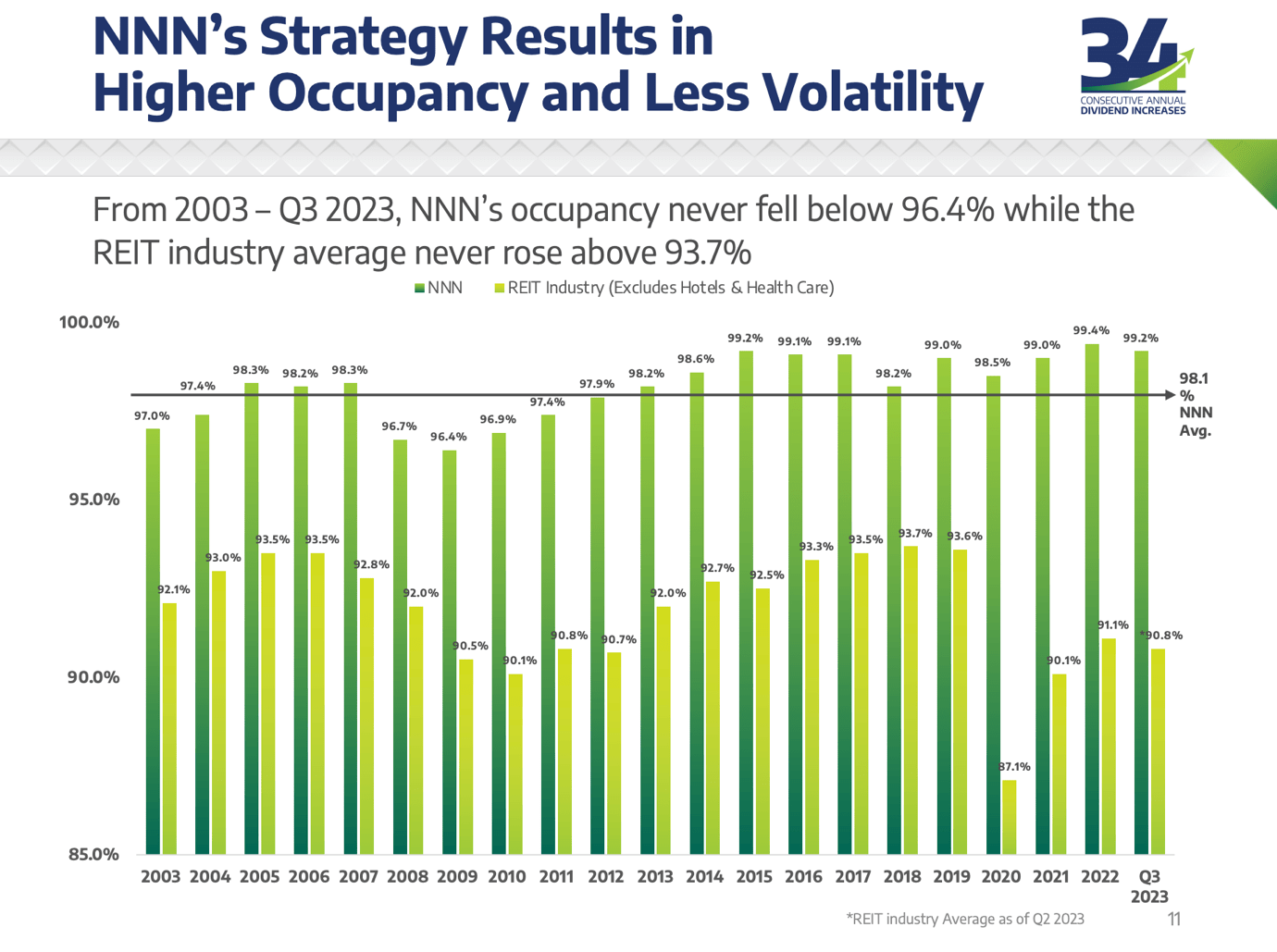

When it comes to occupancy, despite a minor dip to 99.2% occupancy at the end of the third quarter, well within the longer-term range, NNN has historically outperformed its peers.

NNN REIT

It also helps that NNN is attractively valued.

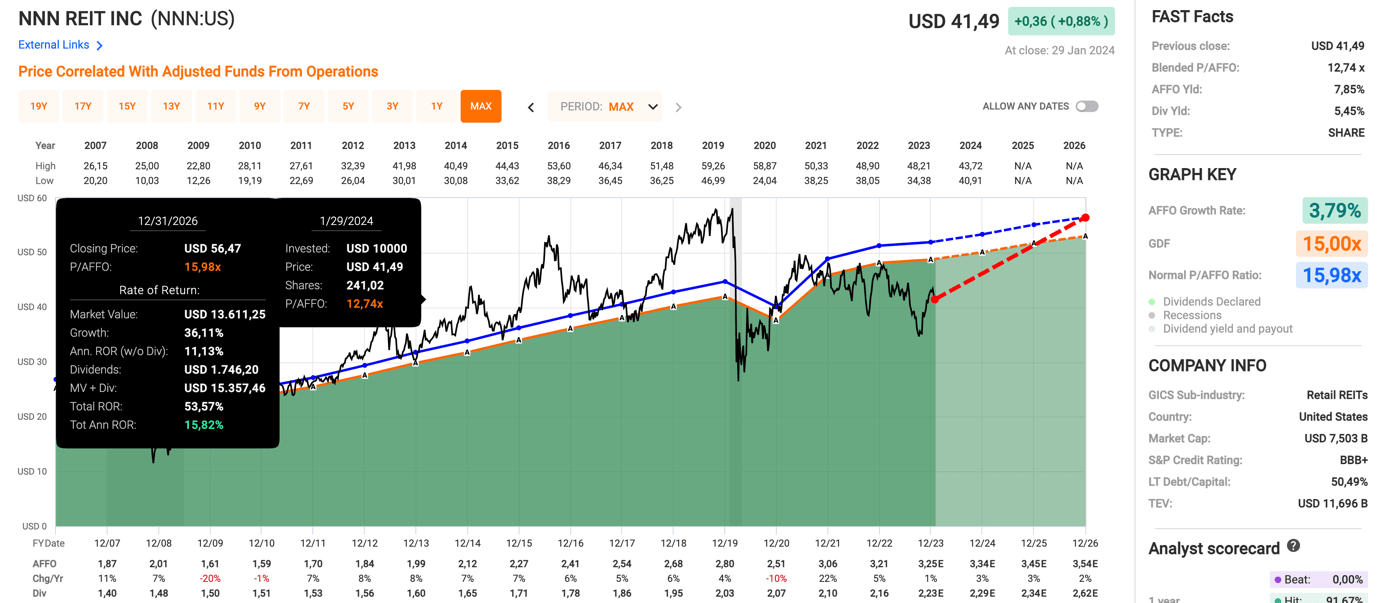

Using the data in the chart below:

- NNN trades at a blended P/AFFO ratio of 12.7x, below its long-term normalized multiple of 16.0x.

- In the 2024-2026 period, annual AFFO growth is expected to average roughly 3%, which is similar to Realty Income.

- A gradual return to its normalized valuation by incorporation of its dividend and expected AFFO growth indicates a potential annual return exceeding 15%.

FAST Graphs

While the return is highly influenced by central bank rate changes, NNN is attractively valued with a Buy rating from iREIT®.

Agree Realty Corporation (ADC) – 4.9% Yield

REIT number three is also a triple-net lease REIT.

Why?

Because an article about high-quality income has to include ADC – regardless of whether it is correlated to the other two picks in this article.

As most readers may know, Agree Realty CEO Joey Agree often spends time answering questions on Seeking Alpha, which is just one of many ways the company proves that it cares about all of its stakeholders, including shareholders.

Here’s a picture of Joey and I when I met him in December:

Brad Thomas

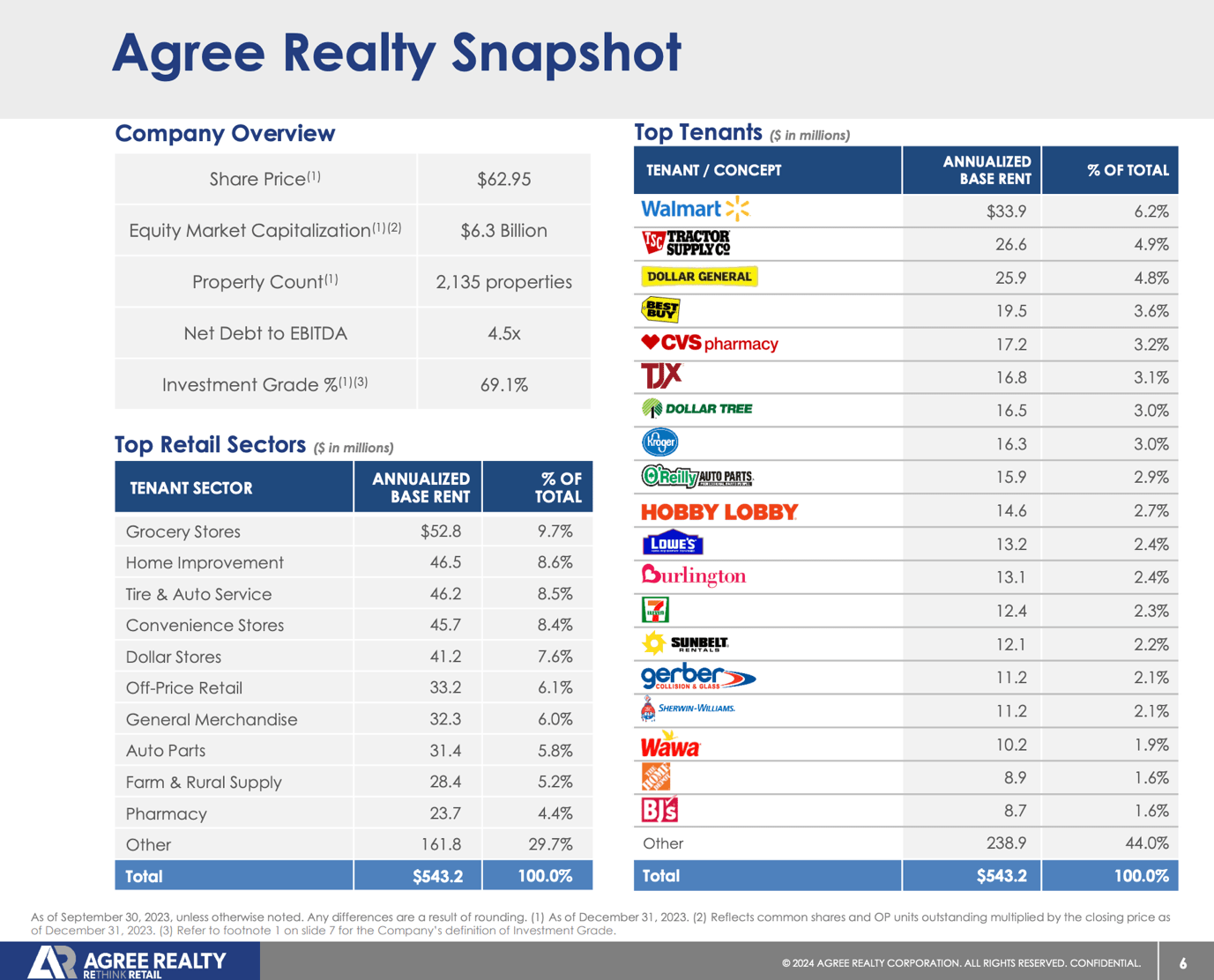

Founded in 1971, Agree Realty has grown into a giant, owning more than 2,130 properties totaling over 44 million square feet in 49 states.

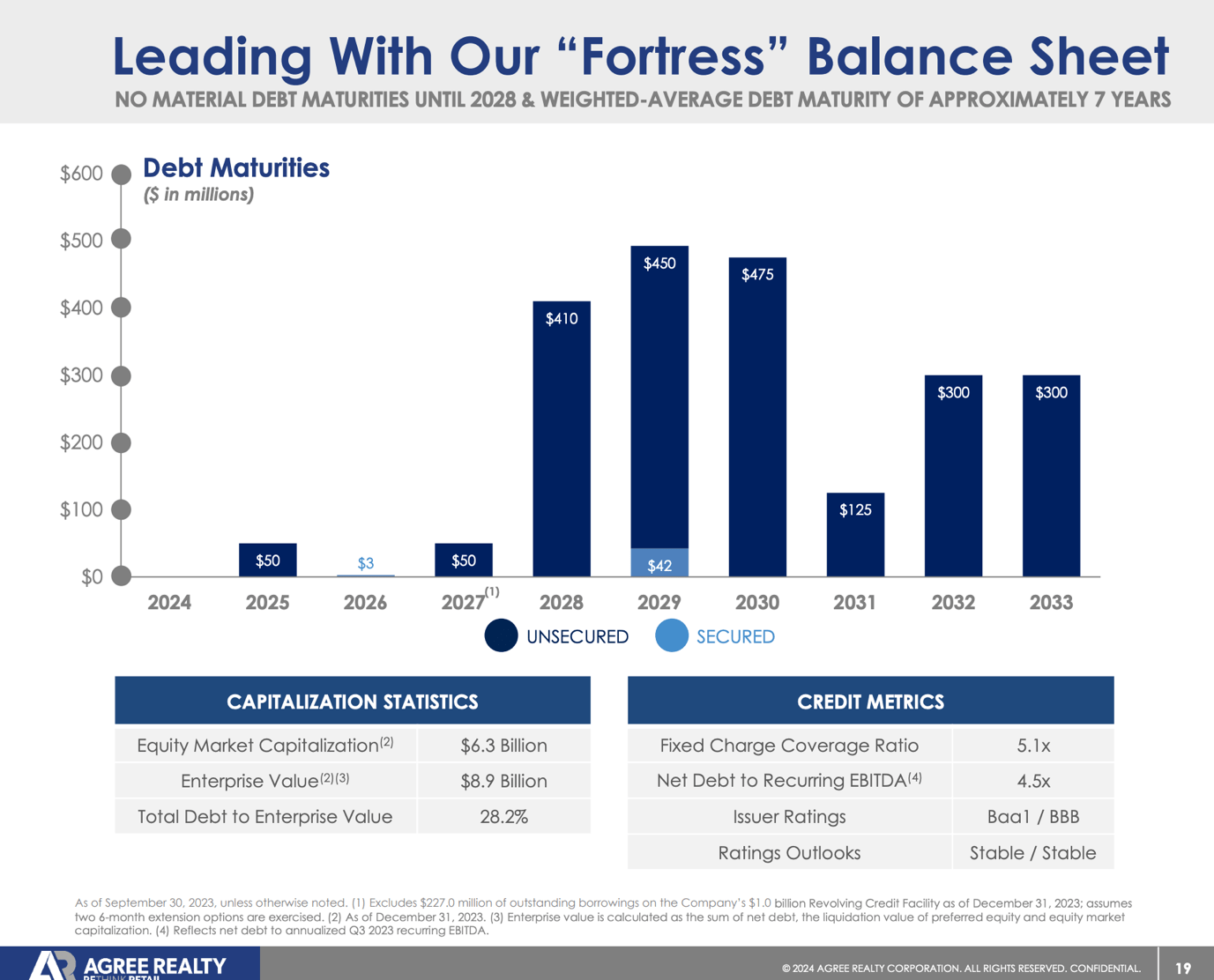

Headquartered in Royal Oak, Michigan, the company has an investment-grade credit rating of BBB from S&P. This credit rating is backed by a net debt ratio of 4.5x (EBITDA) and no meaningful debt maturities until 2028.

In other words, while some REITs are currently stressing about refinancing debt at much higher rates, Agree Realty has more time and way more financial flexibility.

Agree Realty

Furthermore, like Realty Income, the company has some of the best tenants in the entire REIT universe.

Its top tenants include some of the market’s favorite dividend stocks, including Walmart (WMT), Tractor Supply Company (TSCO), Dollar General, Lowe’s (LOW), and Home Depot (HD).

Its largest tenant is Walmart, accounting for slightly more than 6% of its annual base rent.

Agree Realty

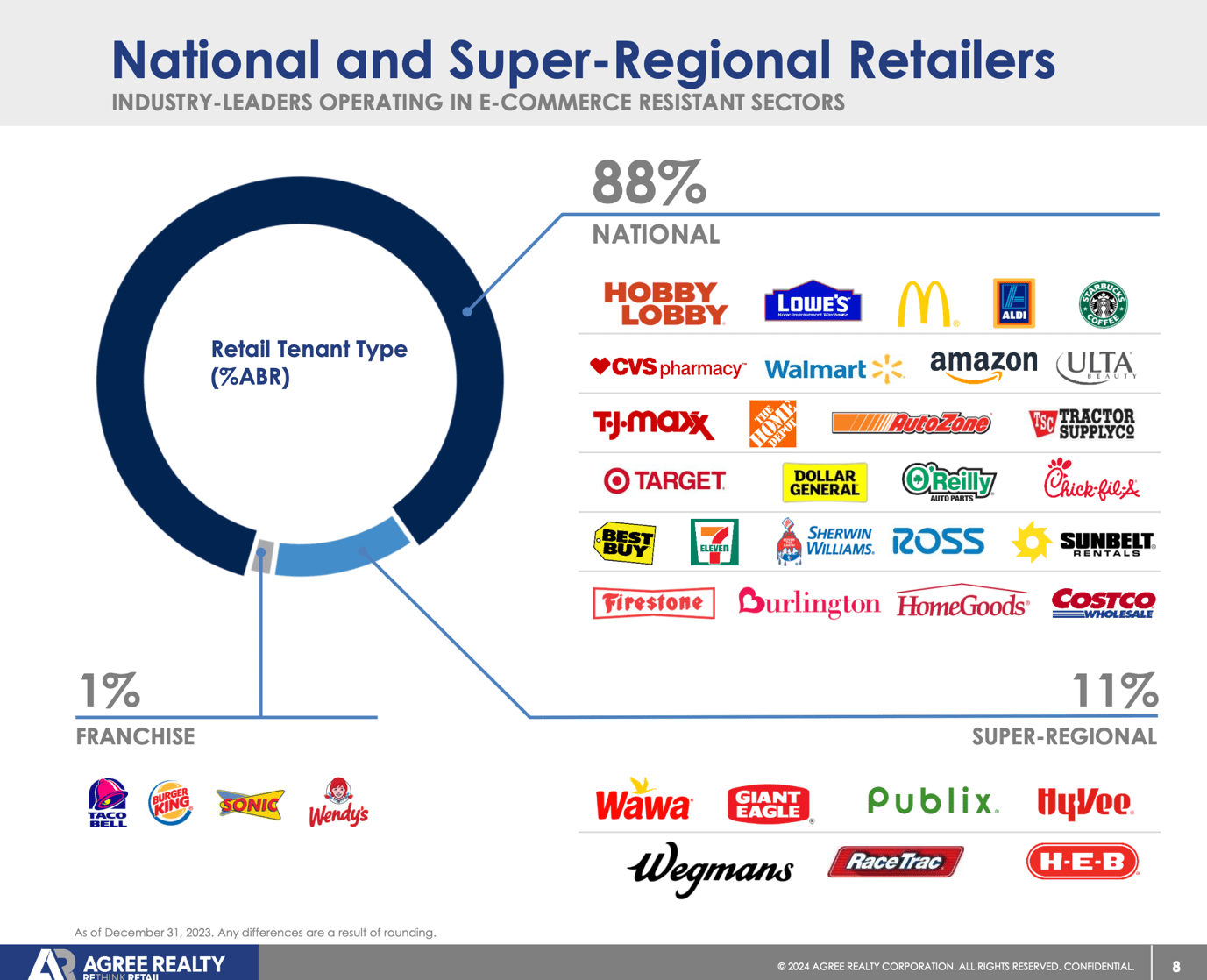

Furthermore, what sets this portfolio apart is that 69% of its tenants have investment-grade balance sheets. This is almost unheard of in the REIT space.

While renting to the “big guys” may come with some potential disadvantages, like lower pricing power (everyone wants to have a company like Walmart as a tenant), the company’s portfolio screams stability, which adds to the stock’s appeal.

It also helps that a big chunk of its income comes from defensive industries like grocery stores (9.7% of annualized base rent), convenience stores (8.4%), and dollar stores (7.6%).

Agree Realty

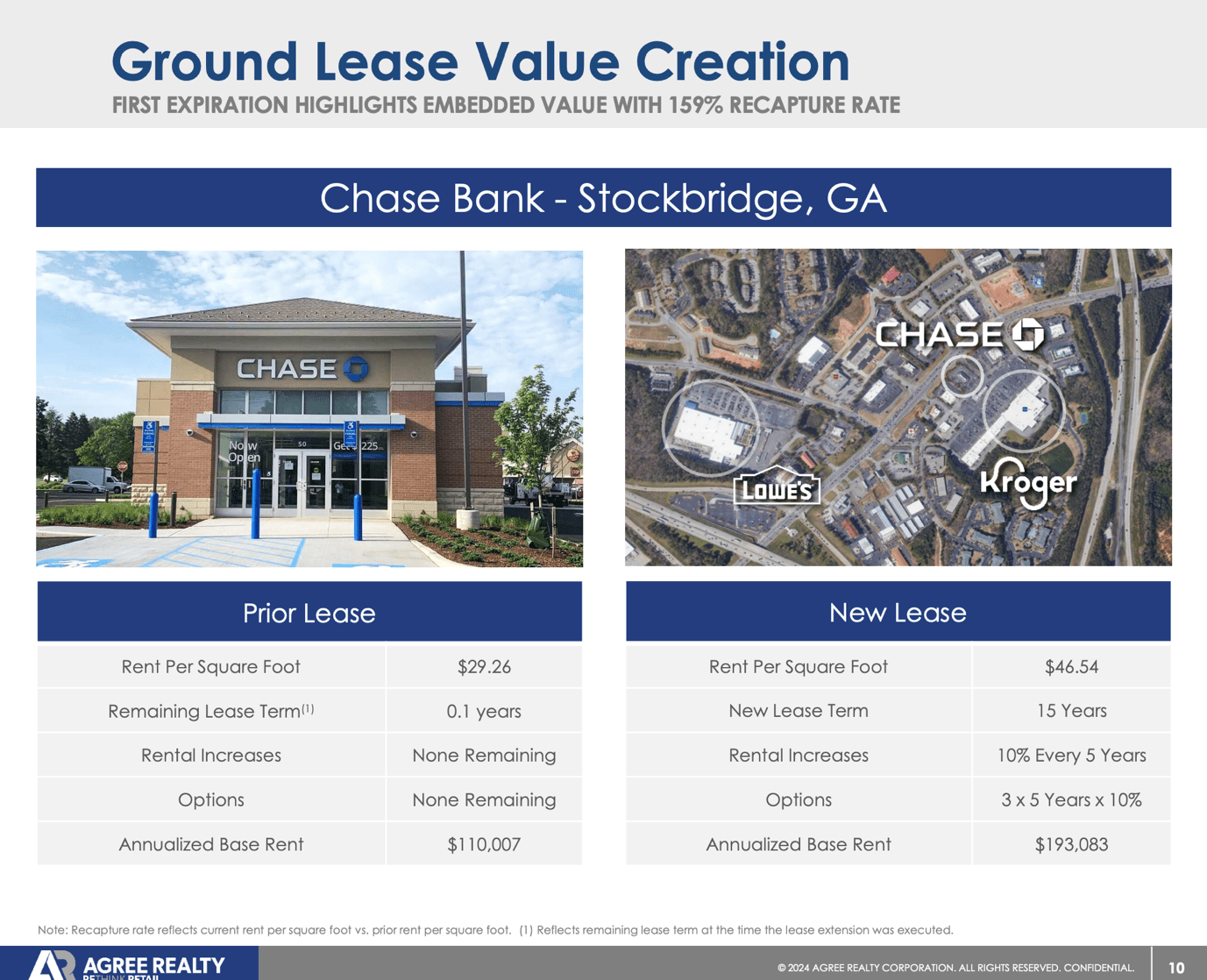

The triple-net lease giant also benefits from ground leases and sale-leaseback deals.

Looking at the example below, we see that the company has turned a ground lease into a highly profitable new deal, raising the annualized base rent by more than $80,000 and including a highly favorable rent escalator that should protect the company against (average) inflation rates.

Agree Realty

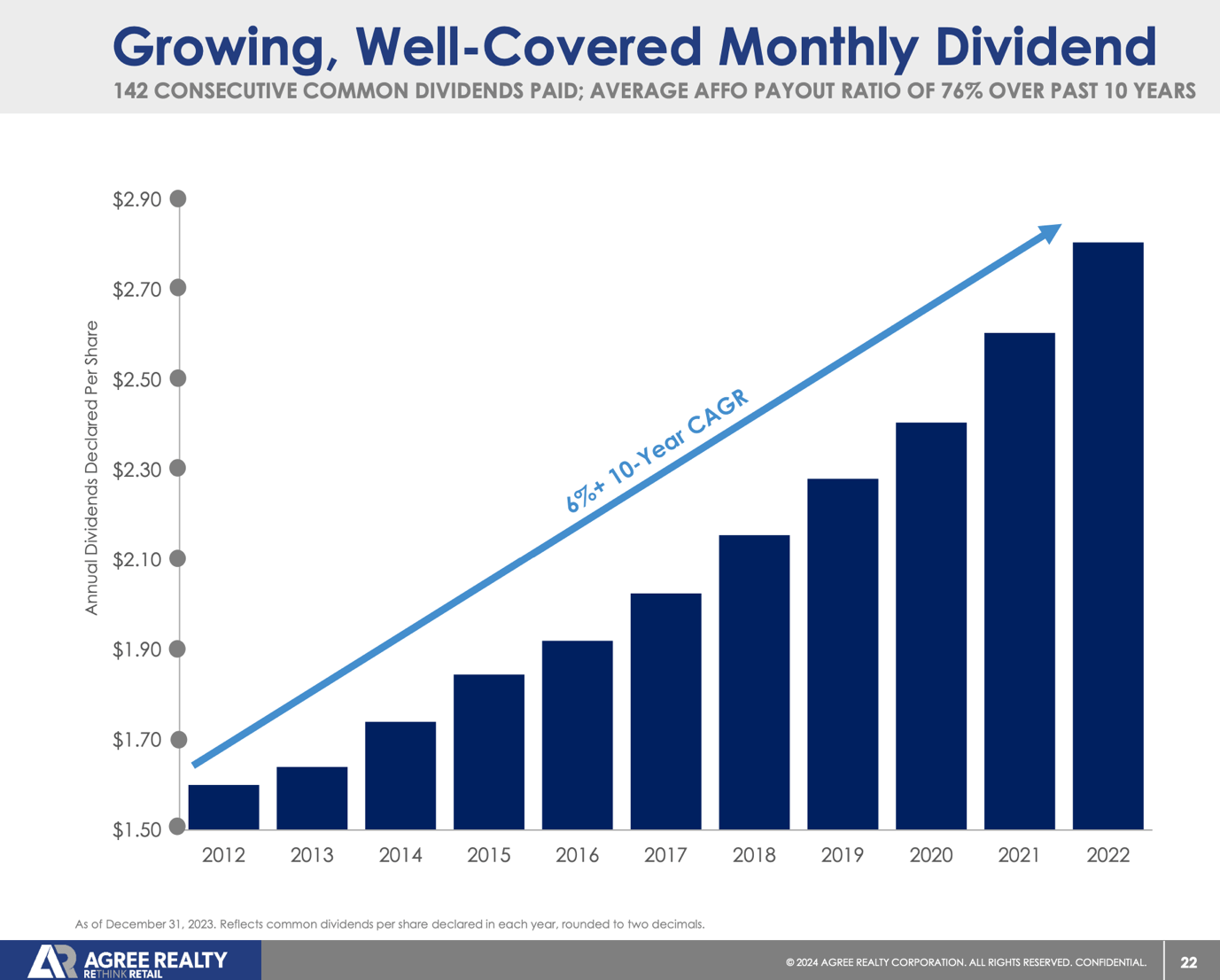

With regard to its dividend, the company yields less than Realty Income and NNN. However, it has higher dividend growth.

Agree Realty is also a monthly payer. After hiking its dividend by 2.9% on October 12, 2023, it currently pays $0.247 per share per month in dividends. This translates to a yield of 4.9%.

The five-year dividend CAGR is 6.3%, which is roughly equal to the annual dividend growth rate since 2012, as seen in the chart below.

Agree Realty

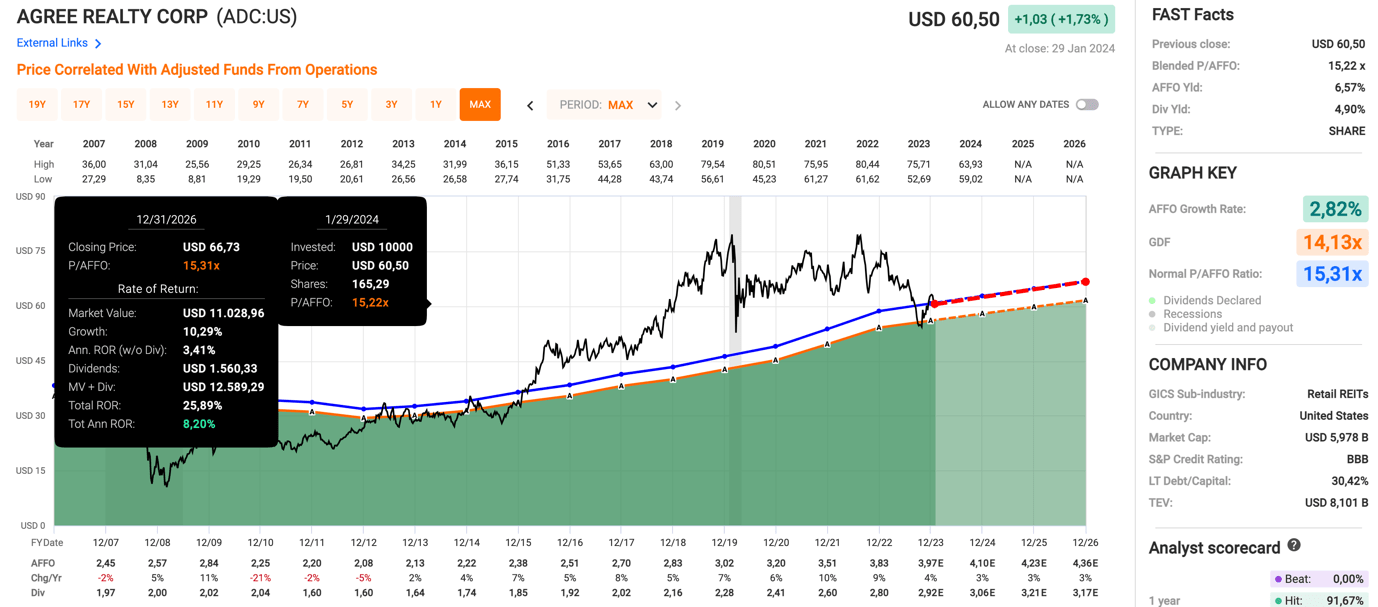

This year, the company is expected to generate $4.10 in AFFO, which implies a healthy dividend payout ratio of 72%.

Speaking of expected AFFO growth, as we can see in the chart below, the company is forecasted to grow AFFO by 3% per year in the 2024-2026 period, similar to O and NNN.

- ADC currently trades at a blended P/AFFO ratio of 15.2x, which means it trades a bit higher than the two peers covered in this article.

- Its normalized valuation is 15.3x, which fits its growth outlook.

- When combining its projected AFFO trajectory, 15.3x AFFO multiple, and its dividend, the stock has an annual total return outlook of 8% per year.

FAST Graphs

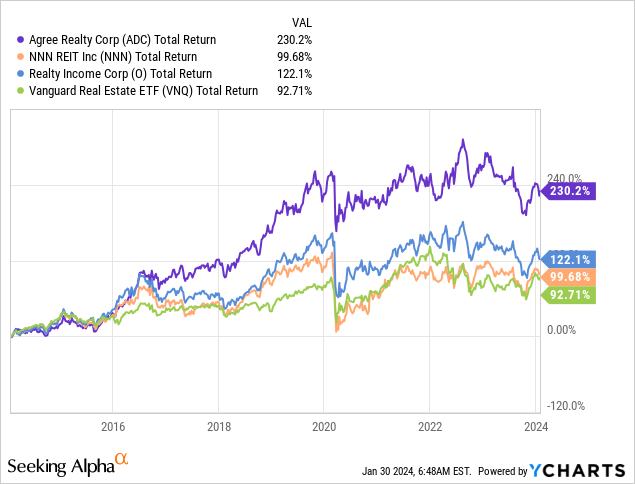

The only reason why ADC has a lower total return outlook than O and NNN is the fact that it has performed better during the recent REIT downturn.

On a prolonged basis, it is likely that ADC will continue to deliver a higher total return than NNN and O.

Over the past ten years, ADC has returned 230%, beating O and NNN by a significant margin, while all REITs covered in this article have outperformed the Vanguard Real Estate ETF (VNQ).

Seeking Alpha

Given its valuation, the stock has a Buy rating from iREIT®.

Takeaway

Reflecting on my early days as a newspaper delivery boy, the key lessons resonate in my investment approach today. Just as I prioritized delivering newspapers come rain, sleet, or snow, successful investing requires a commitment to reliable income. Three exceptional REITs align with this ethos:

- Realty Income: A stalwart in triple-net lease retail REITs, offering a 5.6% yield and stability in a diversified portfolio.

- NNN REIT: A smaller yet robust triple-net lease REIT, boasting a 5.5% yield, consistent dividend growth, and attractive valuation.

- Agree Realty: With a monthly payout, this triple-net lease giant yields 4.9%, demonstrating impressive stability with investment-grade tenants and a noteworthy long-term total return.

Much like my newspaper days, these REITs exemplify the importance of understanding your “customers” (tenants), delivering on commitments (consistent dividends), and going the extra mile for success.

In the ever-changing market, these investments promise steady returns, rain or shine.

Happy SWAN Investing!

Q2 2024 Earnings Call Transcript")