urbazon

Investment thesis

Our current investment thesis is:

- DLTH is likely on a slow decline to zero. The company, while providing good quality products that certainly have their place in the market, is unable to gain upward traction. Marketing efforts have fallen flat, innovative responses to industry developments have been non-existent, and competition has grown substantially. We believe it is likely too late for a resurgence.

- We expect the company to stabilize in H2’24, although will likely continue to underperform the market. For its brands to succeed, we believe a strategic takeover is required.

Company description

Duluth Holdings (NASDAQ:DLTH) is a retail company specializing in rugged, outdoor-inspired clothing, gear, and accessories. Known for its innovative products, Duluth focuses on providing solutions for tradespeople and outdoor enthusiasts, combining durability with comfort.

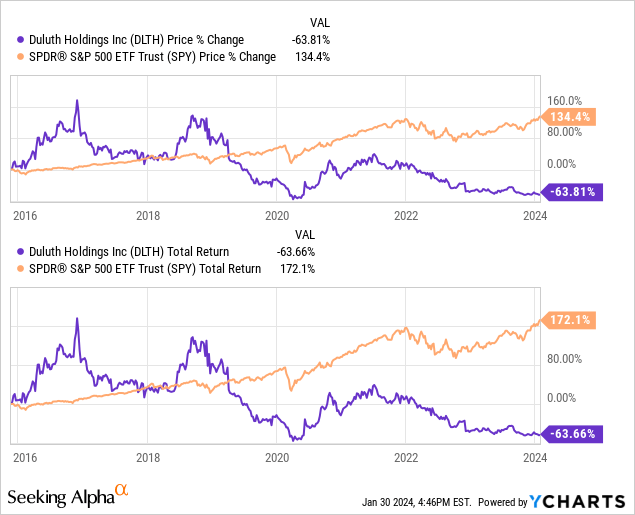

Share price

DLTH’s share price performance has been disastrous, with the company losing over 50% of its value during the last decade. This has been a volatile period for the retail industry and DLTH has struggled to adapt, contributing to a decline on many fronts.

Commercial analysis

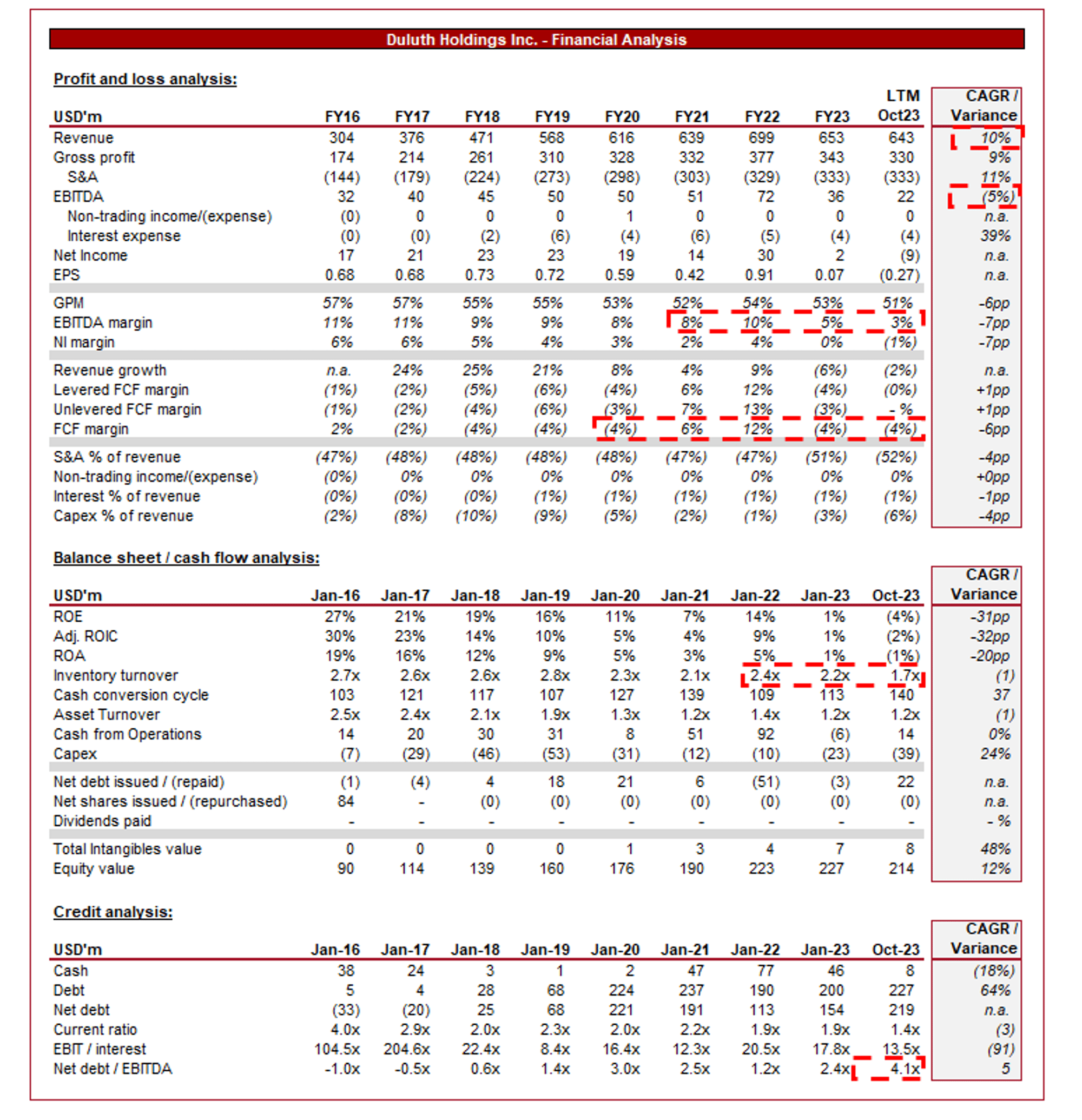

Financials (Capital IQ)

Presented above are DLTH’s financial results.

DLTH’s revenue has grown respectably, with a CAGR of +10% since FY16. The issue, however, is that profitability has persistently declined as its EBITDA CAGR is (5)%.

Business Model

DLTH operates as a multichannel retailer, selling workwear, outdoor apparel, and accessories. The company utilizes a combination of retail stores, an e-commerce platform, and catalogs to reach its customer base. The company is primarily based in the Midwest and South of the US.

The company broadly caters to a niche market, primarily targeting customers who value durable and functional clothing for outdoor and work activities, a detachment from the current fast-fashion trend. This niche focus has allowed the company to develop a loyal customer base, in spite of fluctuating trends as well as a reputation in the industry.

Unlike many in the retail industry, DLTH has a strong direct-to-consumer model. This approach allows the company to have more control over its brand image and customer experience, while also enhancing unit economics by cutting out retailers.

DLTH has invested well in its e-commerce platform, and integrates technology to enhance the online shopping experience. The company sells an impressive ~63% through this channel, again enhancing its unit economics and ensuring it remains connected to its customers as the e-commerce trend continues.

Competitive Positioning

The company’s approach to quality has created a distinctive brand identity. The brand’s humorous marketing approach (an example linked), often featuring unconventional advertising, has underpinned its brand recognition and customer engagement.

This said, we are unsure whether its approach, which was previously “edgy” and ahead of its time, has now fallen stale.

As the following illustrates, the brand has essentially experienced minimal development since c.2015, currently trending down despite the retail bump experienced during the pandemic.

Google

We attribute this to the changing retail environment. Consumers are increasingly fashion-orientated (and less utility-driven), influenced more heavily by short-term trends and social media. This has given rise to fast fashion and the current “faster fashion” trend, such as with the likes of Shein.

DLTH’s less aggressive/fast approach, across the whole business from marketing to the number of products released, leaves it susceptible to competitive pressures. Realistically, as the current trend continues, we struggle to see this changing.

Apparel Industry

With the fast-moving nature of the apparel industry, we see the following as key factors in order to succeed.

- Innovation in Product Design – Quantity is now king in the fashion industry and so the pressure to continually innovate and create new, trendy products is critical. DLTH has attempted this, such as with its Women’s “Performance Pants”, leaning into both the fitness and athleisure trend together.

- E-commerce Growth – Not only is a robust e-commerce sales base critical to overall growth but growing an online presence and visibility on social media.

- Responsive to Market Trends – Beyond just design, the importance of responding to trends and developments is critical. This is an industry that was historically slower-moving and now requires greater agility.

We struggle to see material development from DLTH in this regard. The company is inherently a niche player and has been further crowded out by the mass production of clothing. Carhartt, a similarly positioned niche player (albeit significantly larger), has played the trend game far better, gaining popularity (again) in the streetwear segment.

Economic & External Consideration

Current economic conditions represent headwinds for DLTH. With elevated rates and inflation, consumers have allocated spending to core costs, contributing to softening spending on discretionary purchases.

Slightly surprisingly, retail expenditure has remained robust, albeit lacking growth and appears precariously positioned. Nevertheless, DLTH’s revenue declined in FY23 (-6%) and continues to fall in the LTM (-2%).

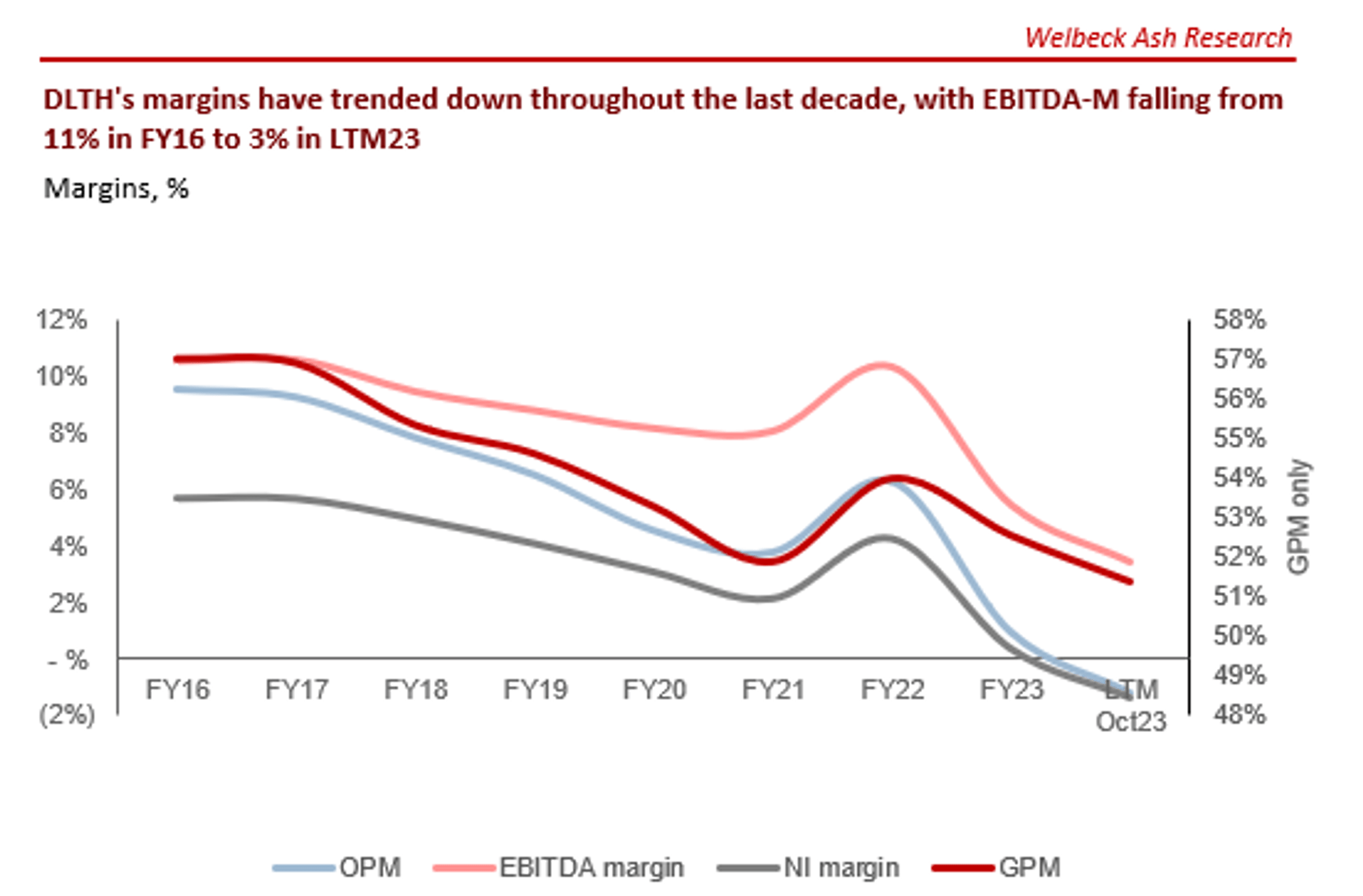

Margins

Capital IQ

Whilst DLTH’s top-line trajectory appears strong, it must be contextualized by its margins. The company has materially foregone its GM% in order to maintain growth, contributing to a net-negative situation for the company.

Given the level of competition in the industry, it is incredibly difficult to win back margins, as consumers are price-sensitive. This means Management must achieve quite considerable efficiency gains. Investment is being made in its production facilities but we struggle to see this generating the improvements required to revert back to its pre-pandemic levels.

Quarterly results

DLTH’s recent performance has been disappointing, with top-line growth of (10.7%), +0.7%, (1.7)%, and (6.1)% in the last four quarters. In conjunction with this, margins have continued to trend down.

The company has experienced lower customer traffic in both direct and retail channels, alongside market share loss following strong unit sell-throughs during Q2. Management has continued to liquidate stock, which is positive, but the unit economics of this is disappointing.

Due to this continued decline, Management has had to raise debt to fund its short-term commitments, further compounding its poor performance by creating unnecessary inefficiencies.

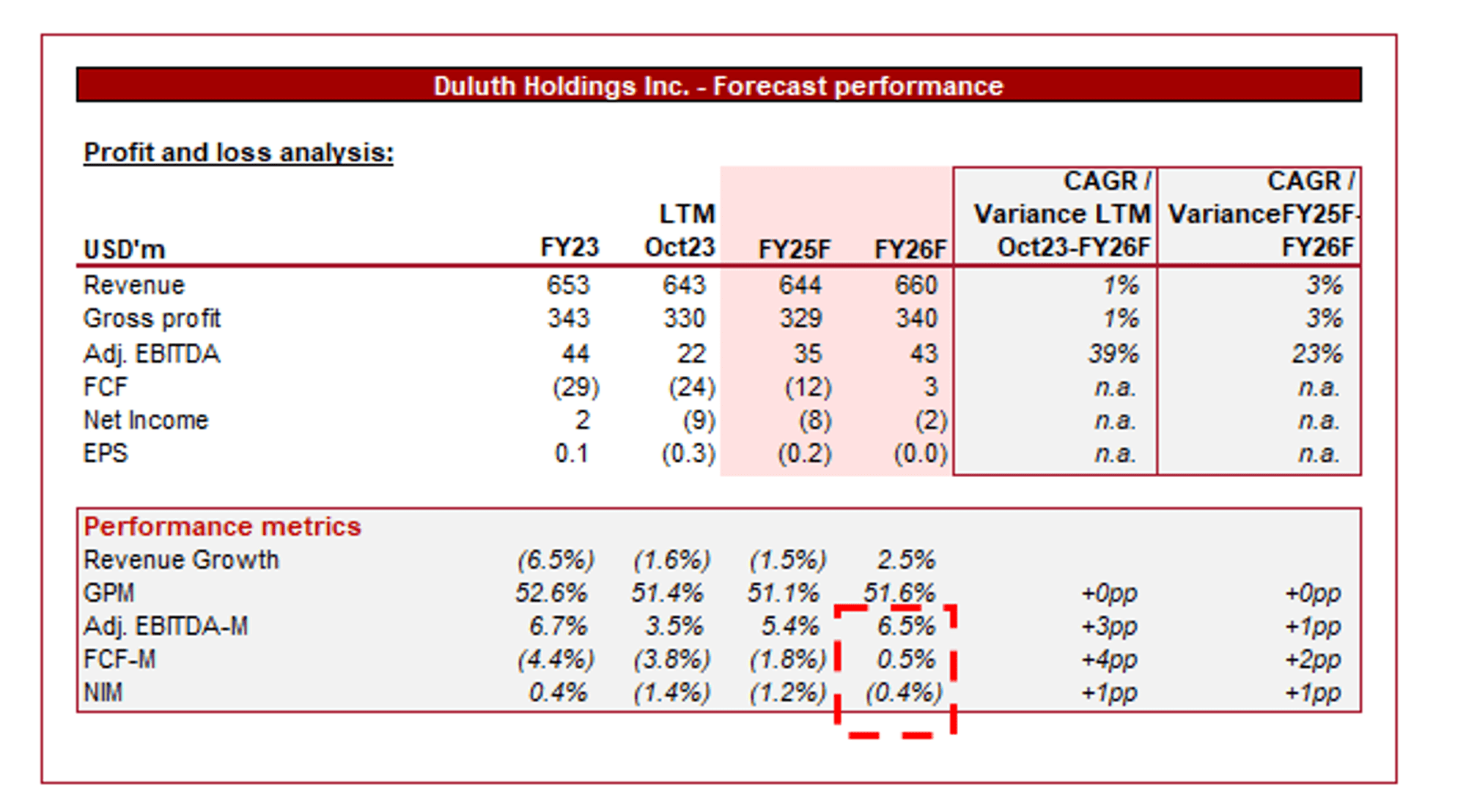

Outlook

Capital IQ

Presented above is Wall Street’s consensus view on the coming years.

Analysts are forecasting limited growth in the coming years, with a CAGR of +1% into FY26F. In conjunction with this, margins are expected to recover from the LTM level but only reach FY23.

We concur with these estimates. Section-by-section, this analysis has compounded the issues with DLTH, with macro headwinds to commercial concerns.

We struggle to see how the company can achieve consistent growth above inflation at a margin-neutral level, let alone driven margin improvement.

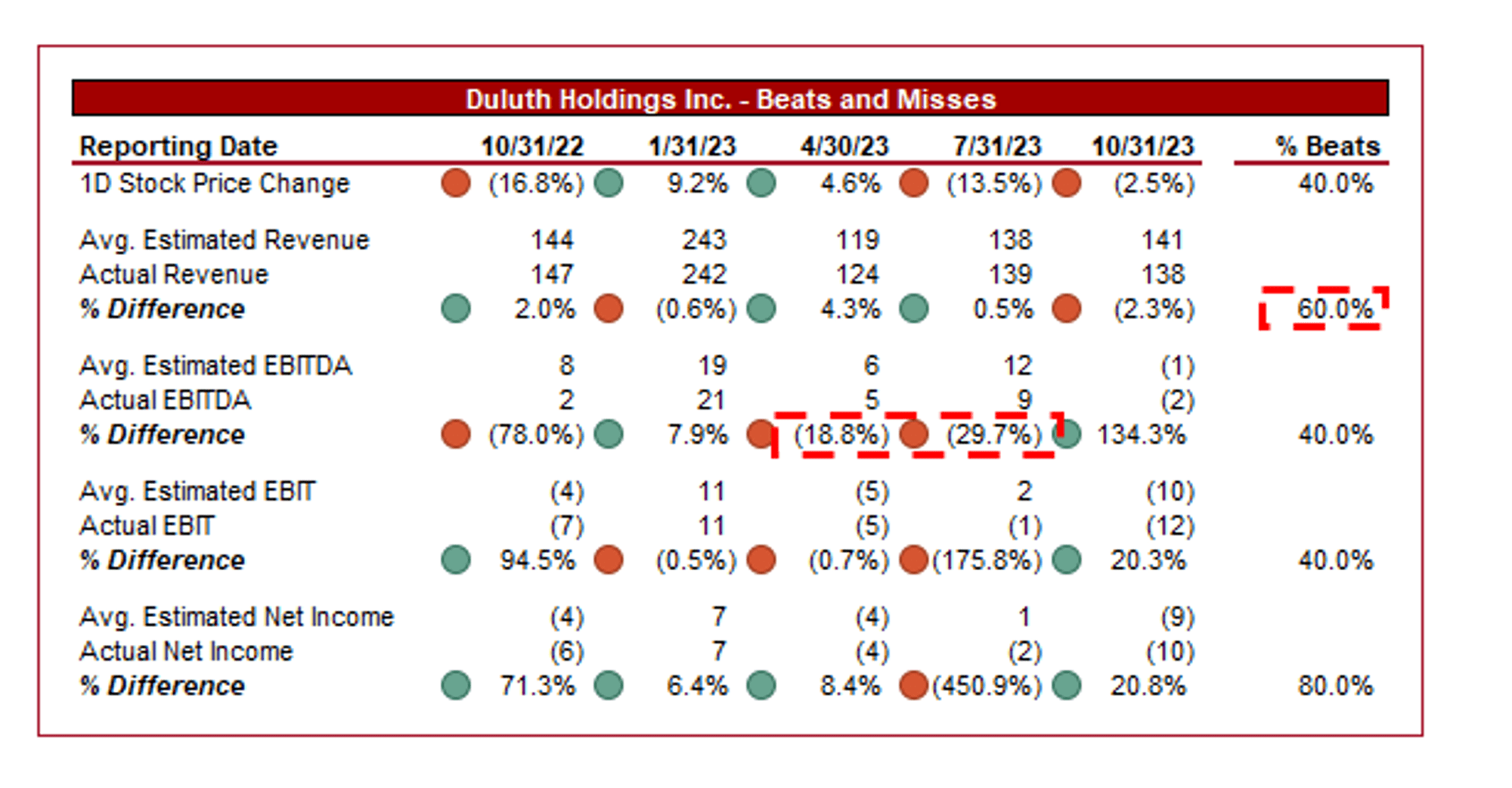

Beats and Misses

Capital IQ

It is worth highlighting that DLTH’S recent trajectory relative to estimates has been poor, primarily due to considerably lower-than-expected margins. This is illustrative of its struggles with demand, contributing to greater discounting to maintain growth.

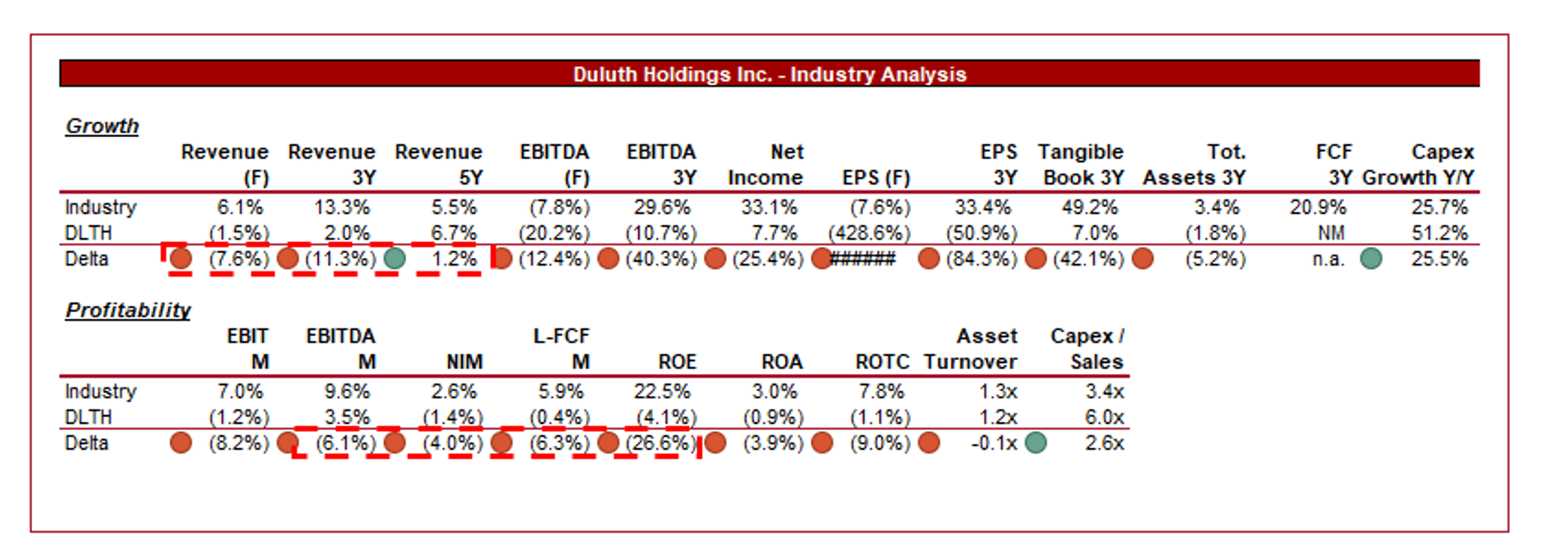

Industry analysis

Seeking Alpha

Presented above is a comparison of DLTH’s growth and profitability to the average of its industry, as defined by Seeking Alpha (28 companies).

We will not loiter in this section for too long, DLTH is a major underperformer. The company is significantly below its peers in margins, and its recent growth is also lagging behind (and is forecast to continue).

Realistically, when layering in its commercial concerns, also, DLTH is one of the weaker constituents of this cohort.

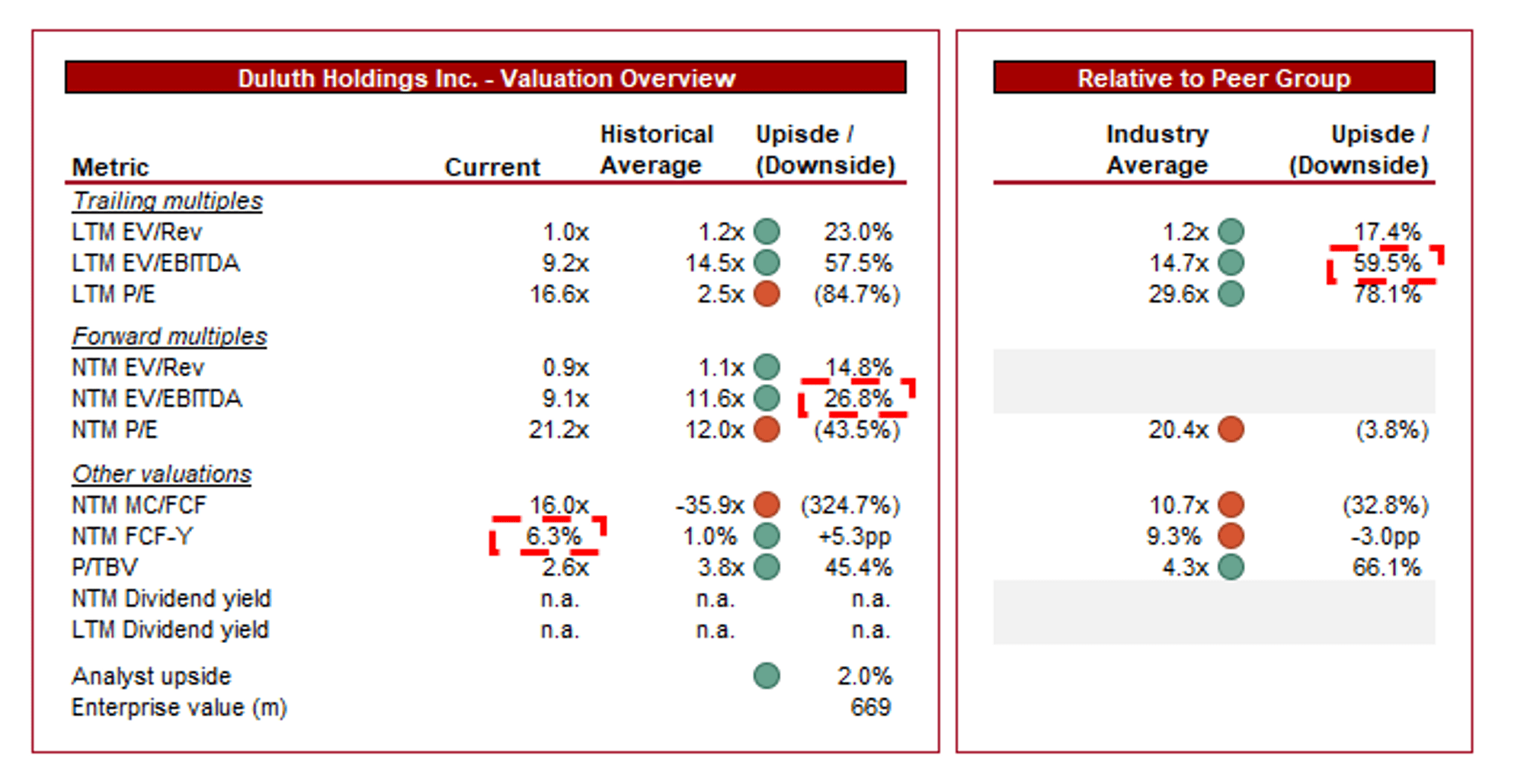

Valuation

Capital IQ

DLTH is currently trading at 9x LTM EBITDA and 9x NTM EBITDA. This is a discount to its historical average.

A discount to its historical average is undoubtedly warranted, owing to its declining commercial position and weakening financial performance. Further, the company is trading at a discount to its peers, although this turns to a premium on a NTM basis, likely due to DLTH’s severe underperformance expected contributing to multiple expansion.

DLTH’s valuation is directionally correct, although we do not see any clear evidence to suggest it is highly undervalued. With a business as weak as DLTH is currently, this would be the only reason to entertain a buy.

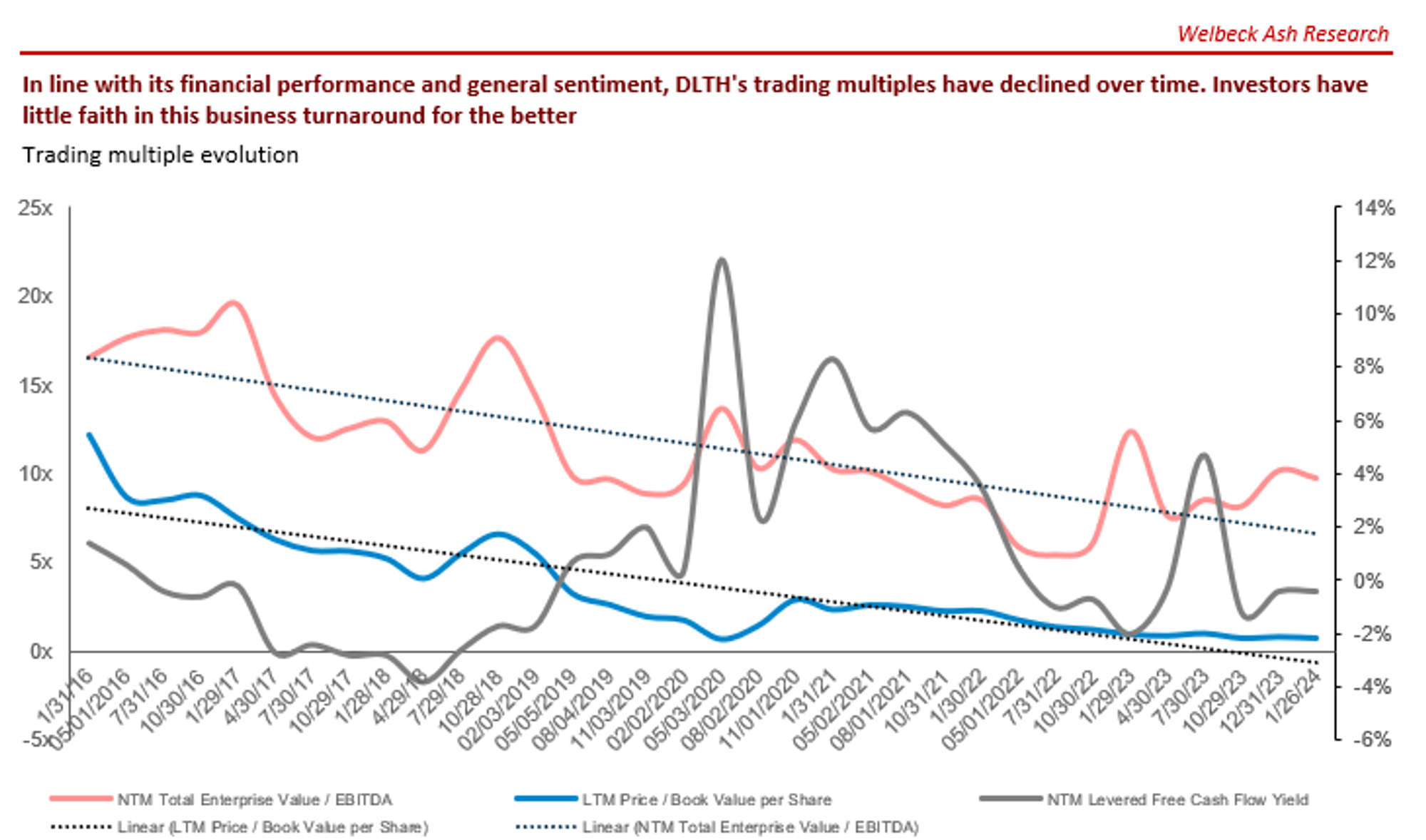

Capital IQ

Key risks with our thesis

The risk to our current thesis is an ability to generate hype significantly, which can come as simply as a TikTok trend, or as engineered as a limited collaboration with popular brands. This could have the same impact on DLTH as what occurred with Champion and Carhartt, among others.

Secondly, if its share price continues to trend down, we could see a strategic takeover by a brand consolidator who would look to strip away the stores and invest in marketing, while taking production in-house.

Final thoughts

We are not convinced by DLTH at all. The company is performing poorly in a highly competitive industry, and lacks any clear route to a resurgence. DLTH’s financial weakness is almost secondary to this, but does not make for appealing reading.

We see no reason for investors to consider this stock and if things do not change, the share price will continue to fall.

Q2 2024 Earnings Call Transcript")