Wolterk

Ameriprise Financial (NYSE:AMP) is a leading financial services company that just reported impressive results for the fourth fiscal quarter, despite missing EPS estimates. The company reported low-single digit growth in its operating income in Q4’23, but Ameriprise Financial is a deeply profitable financial services franchise that achieves mid-double digit returns on equity. The firm also benefits from growth in its wealth management business and continued to attract a healthy amount of new client assets. I believe Ameriprise Financial has an attractive risk profile given that the firm is operating at high returns on equity. The wealth management business is also facing attractive long term growth prospects. With shares trading at a 9.3% earnings yield, I believe shares are a buy!

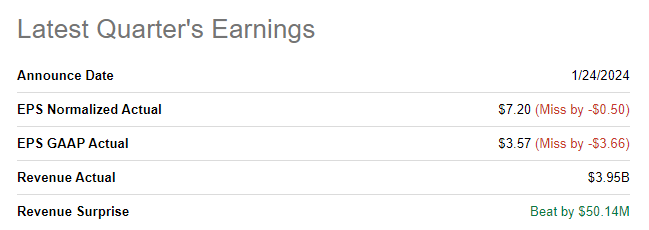

Ameriprise Financial missed Q4’23 EPS expectations

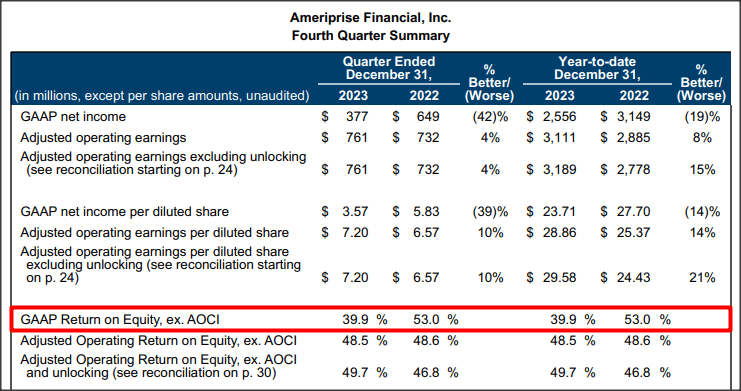

The financial services firm failed to meet expectations for its fourth quarter in terms of earnings, but exceeded top line expectations. Ameriprise Financial delivered adjusted EPS of $7.20 which missed the consensus EPS estimate by $0.50 per-share.

Seeking Alpha

2 reasons to buy Ameriprise Financial in 2024

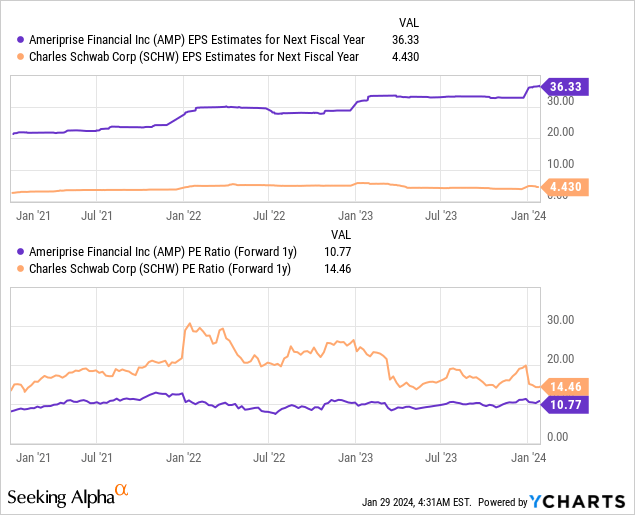

Ameriprise Financial is a well-known diversified financial services company with a market cap of $40B. At its core, Ameriprise Financial offers investors wealth and asset management services as well as financial planning advice. Ameriprise Financial competes with other banks and other financial services firms like Charles Schwab. I have covered Charles Schwab’s recent Q4’23 earnings as well: A Solid Value Play.

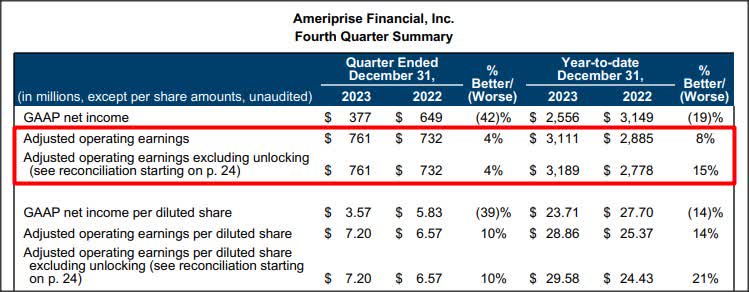

Ameriprise Financial generated a total of $761M in adjusted operating earnings in Q4’23, showing 4% year over year growth. On a full-year basis, adjusted operating income was up 8% to $3.1B. The earnings report was better than I thought, especially because the financial adviser had great success in growing its client assets in the fourth quarter.

Ameriprise

I see two reasons why Ameriprise Financial could be an interesting buy for long term investors in the financial services industry:

1. Ameriprise Financial has a rapidly growing wealth management segment that benefits from increasing client assets and 2. Ameriprise Financial is a very profitable financial adviser with 40-50% returns on equity.

As to the first point, the wealth management segment.

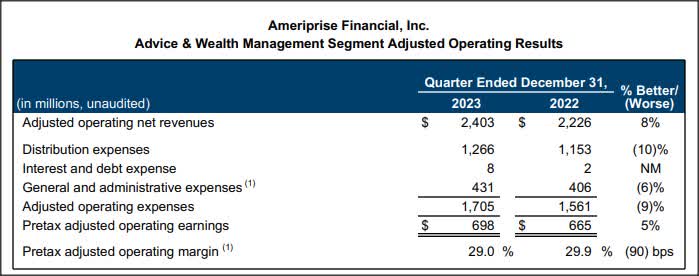

This segment was once again key to Ameriprise Financial’s solid quarterly earnings in Q4’23. The financial services company saw a 19% increase in client assets under management in Q4’23 and Ameriprise Financial ended the year with $901M of client assets on its balance sheet. In the fourth-quarter alone, $23B in new client assets flowed to the company, showing an 83% increase. The result of these underlying trends has been an 8% jump in revenues in Q4’23, year over year, and a massive adjusted operating margin of 29%.

Ameriprise

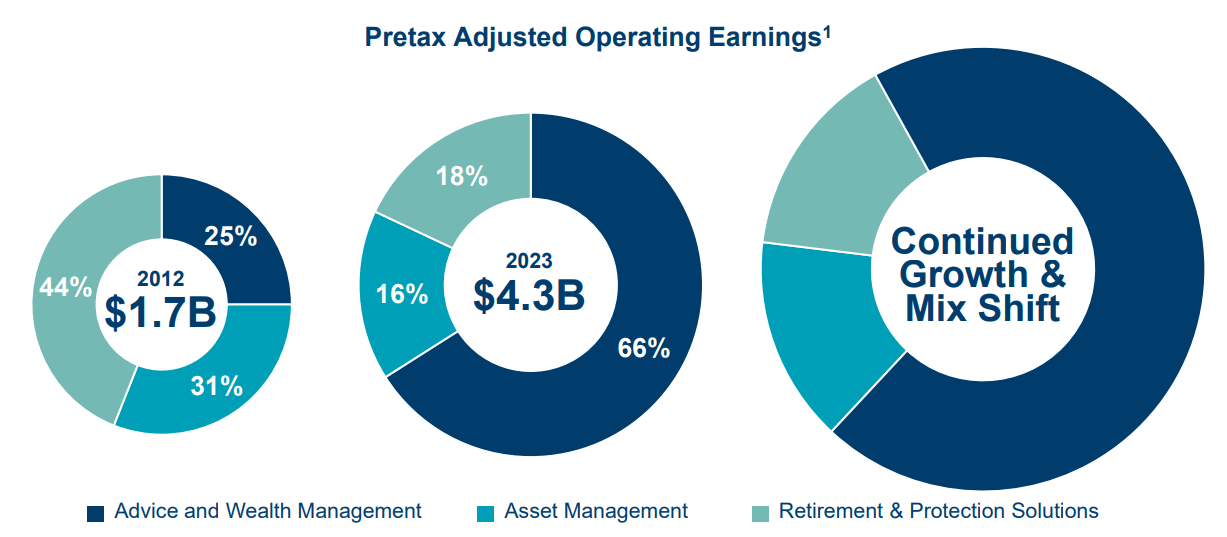

Ameriprise Financial is aggressively growing its advice and wealth management business and the segment now accounts for the majority of adjusted operating earnings.

Ameriprise

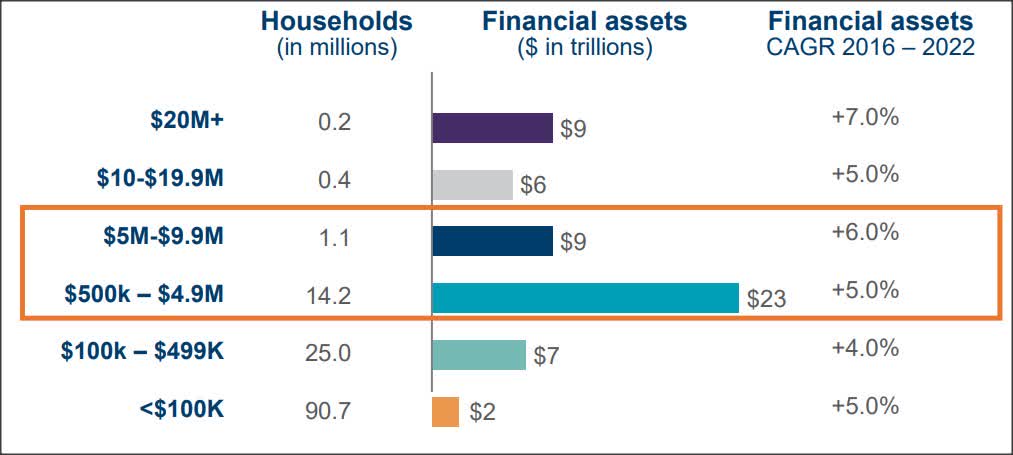

The longer term outlook for the financial services industry is also positive as U.S. households are expected to continue to see growth in their financial assets. Ameriprise Financial’s core market, those households with financial assets between $500k and $9.9M, grew in the mid-single digits in the past and is projected, according to Ameriprise Financial (Source), to grow at 3-5% going forward.

Ameriprise

The second reason relates to Ameriprise Financial’s high returns on equity. The financial services industry is very profitable and it showed in the company’s fourth-quarter earnings release. Ameriprise Financial generated a return on equity of 39.9% in FY 2023 compared to a 53.0% return in FY 2022. The company’s super profitable wealth management and advisory business is a key driver of these equity returns.

Ameriprise

Ameriprise Financial trades at an earnings yield of 9%+

The financial services company obviously benefits when the stock market is doing well and clients feel wealthy. The U.S. economy advanced 3.3% in the fourth-quarter, according to the first reading of the GDP report, and the Dow Jones hit a new all-time high just days ago.

Ameriprise Financial is expected to generate earnings growth of 17% in FY 2024 and 8% next year which calculates to FY 2025 P/E ratio of 10.8X. Charles Schwab, for comparison, trades at a price-to-earnings ratio of 14.5X and is projected to see 27% EPS growth next year. The faster growth, as well as the bigger size of Charles Schwab, are likely reasons why the financial adviser is more expensive than Ameriprise Financial.

Ameriprise Financial is currently valued at a P/E ratio of 11X which implies an earnings yield of 9.3%. Given the strength of Ameriprise Financial’s earnings release for Q4’23, high margins and ROE, favorable market backdrop and a positive wealth management outlook, shares could trade at a 12X P/E ratio and the earnings potential would not be overvalued, in my opinion. This implies a fair value of $436 and 11% upside potential.

Risks with Ameriprise Financial

Ameriprise Financial’s earnings and returns on equity are reliant on the state of the capital markets. This implies that financial services companies are subject to intense earnings volatility in the short term which could make Ameriprise Financial an unattractive investment for some investors that don’t have a high risk acceptance. What would change my mind about AMP is if its operating margins or ROE (measures that I monitor closely) were to fall significantly.

Final thoughts

Ameriprise Financial last week submitted a strong earnings sheet that indicated that the financial advisor’s core earnings grew 4% in the fourth-quarter and 8% on a full-year basis. More importantly, Ameriprise Financial is very successful in pulling new client assets to its wealth management platform. The segment itself is super profitable with operating margins near 30% and the firm’s overall equity returns are impressive as well. Considering that Ameriprise Financial is valued at only an 11X P/E ratio, I believe the risk profile is still very much favorable for long term investors!

Q2 2024 Earnings Call Transcript")