Andrey Semenov

I initiated coverage of Super Micro Computer (NASDAQ:SMCI) in May of 2023 with a Strong Buy-rated article. In this article, I detailed their business strategy and the source of their competitive advantage. I followed this up with a more macro-focused article where I detailed a variety of industry-wide tailwinds and conducted a comparative analysis of Super Micro and the two largest server companies Dell (DELL) and HP (HPQ).

In this article, I’ll be reviewing the recent earnings report and will reiterate my Buy rating given strong demand tailwinds, easing supply constraints, and secular growth trends.

Let’s dive in.

Business Overview

Super Micro makes total IT solutions for data centers, cloud service providers (“CSPs”), universities, research labs, and any other entity that may require high-end computing solutions. Total IT solutions refers to hardware (server racks or nodes), software, and networking solutions to manage IT systems at scale. They are an engineering-led business with a majority of employees being engineers and an engineer-by-training CEO with numerous patents to his name.

Their competitive advantage is speed. They seek to always be first-to-market with leading-edge chips designed into a variety of different server configurations. Their Building Blocks architecture allows for custom rack scale solutions so customers can buy exactly what they need; nothing more and nothing less. They are enjoying a first-mover advantage with their liquid cooling solutions, a budding segment of the server market. Their servers are powerful and efficient, they seek to provide industry-leading PUE (power usage effectiveness) and energy efficiency to minimize customers’ TCO (total cost of ownership).

You can read more about their strategy in my “On The Leading Edge” article linked above.

I believe Super Micro is well-positioned to enjoy secular growth tailwinds for years to come. They are a “white-box” server provider, meaning they use industry-standard instead of proprietary components in their hardware. This gives customers more flexibility and less lock-in. While lock-in is typically a good thing, Super Micro’s status as a white-box provider didn’t harm them in the recent quarter as management noted that demand came from both new and existing customers. Existing customers see the value of Super Micro systems and want to continue leaning into the relationship. Using proprietary components to lock customers in isn’t as effective as simply providing industry-leading technology, and that’s exactly what SMCI does.

Nvidia CEO Jensen Huang was quoted last year as saying that AI will require one of the largest infrastructure buildouts in history. He believes this is akin to a new-age industrial revolution. Data centers now need to optimize spend between traditional CPU servers and AI-optimized GPU servers. Super Micro’s business model positions them perfectly to benefit from the increasing spending that is shifting toward GPU servers, and they are quickly becoming the leader in AI-optimized hardware. Super Micro will continuously benefit from CSPs and data centers expanding their AI computing capacity. The more embedded AI becomes in our everyday lives, the more units SMCI will sell.

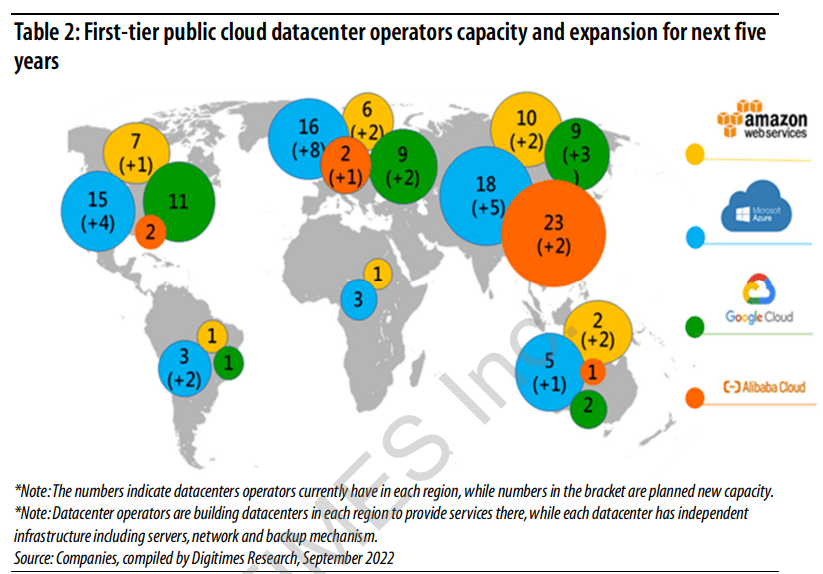

The four largest CSPs alone are contributing to this with massive data center buildouts. The AI hardware market is enjoying a long-run TAM expansion:

Digitimes Research

In short, if you believe we are witnessing an AI revolution (as I do), then in my view what you’ve found here is a company selling the picks and shovels to make that revolution possible.

Earnings Review

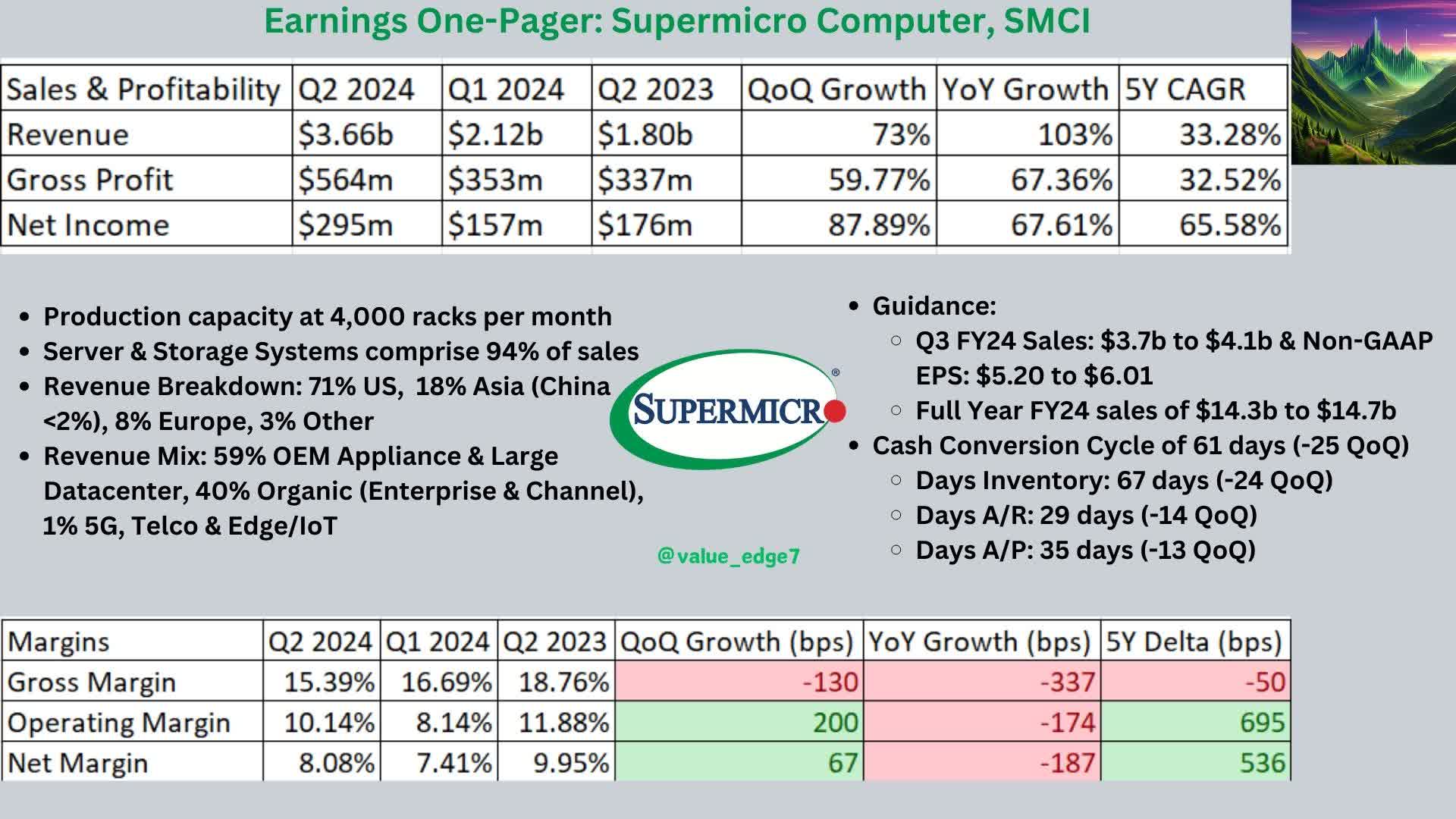

For a quick visual overview, I prepared this earnings snapshot:

Authors Creation

The $3.66b revenue figure was up 103% YoY and 73% QoQ. The company is well on its way to the $5b quarterly run rate necessary to achieve the old $20b annual revenue goal. Meanwhile, Q3 FY24 and full-year guidance were quite promising. Management guided for $3.7b to $4.1b in Q3 FY24 which would represent 188% to 219% YoY growth and 1% to 12% QoQ growth. The FY24 revenue guidance is $14.3b to $14.7b, or 101% to 106% YoY growth.

SMCI was a darling stock of the AI wave that sent many tech names into orbit in 2023. While many companies look overvalued because of AI hype, Super Micro is executing at scale and overdelivering on ambitious goals. This is not a company that investors should ignore.

In short, this report was stellar. Absolutely incredible. Management guided for close to $3b in revenue this quarter and blew that guidance out of the water. This was mostly because of strong secular demand growth and the easing of the supply constraints that sent the stock tanking after the Q4 FY2023 earnings.

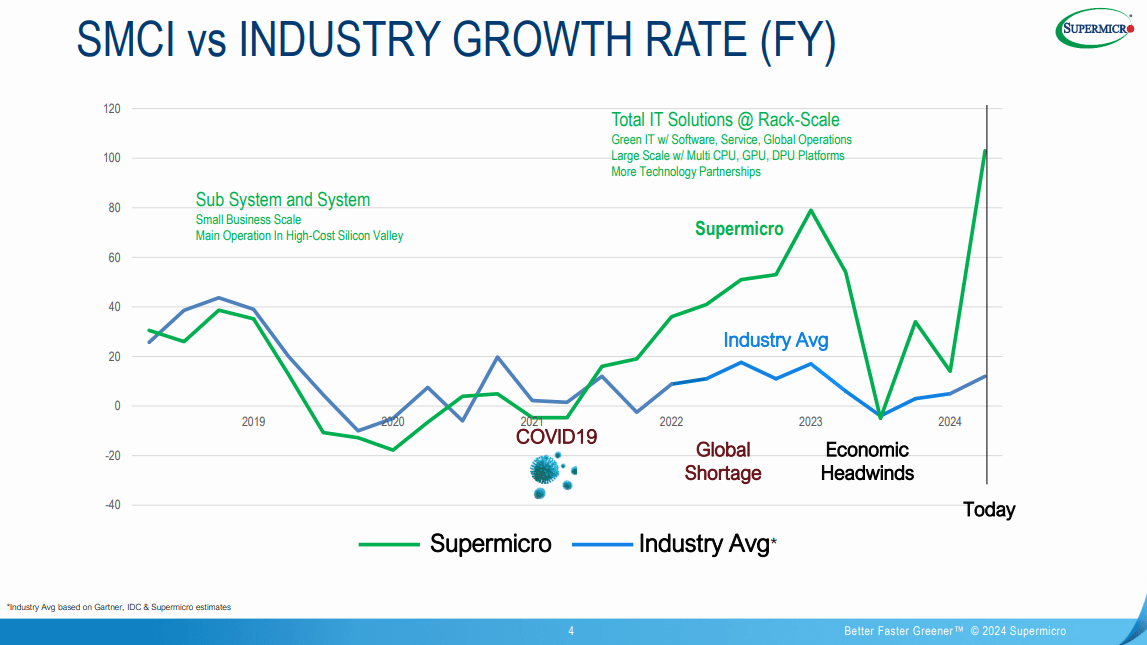

The phenomenal 103% YoY growth has rocketed SMCI far above the industry average growth rates:

SMCI Q2 FY2024 Investor Presentation

This was the company’s first ever $3b quarter and this quarter’s revenue exceeded full year 2021 sales. One important note is that two existing CSPs/large data center customers represented 26% and 11% of total Q2 revenue. AI/GPU and rack-scale total IT solutions now comprise greater than 50% of sales.

The company also increased its annual revenue goal from $20b to $25b and announced two more production facilities are in the works.

Revenue growth far outpaced OpEx growth, contributing to a higher operating margin this quarter despite a decline in gross margin. The majority of the OpEx increase is attributed to higher compensation and headcount, which is the cost of this pace of growth. The company had materially negative FCF this quarter mostly because they grew inventory by $1b in the 2nd half of 2023.

Business Update

Management noted that the Nvidia (NVDA) HGX-H100 system is currently the most popular AI solution. Nvidia has strong pricing power with these systems so this contributed to SMCI’s gross margin decline. Demand for inference systems is also increasing, something I expect will be a secular tailwind over time. Inference demand will continue increasing as AI becomes more pervasive in our everyday lives.

True to their strategy, they announced systems incorporating the next-gen Nvidia B100 are in the design phase while Advanced Micro Devices (AMD) MI300X systems are in sampling. A system based on the Intel Gaudi 3 AI chip is coming soon.

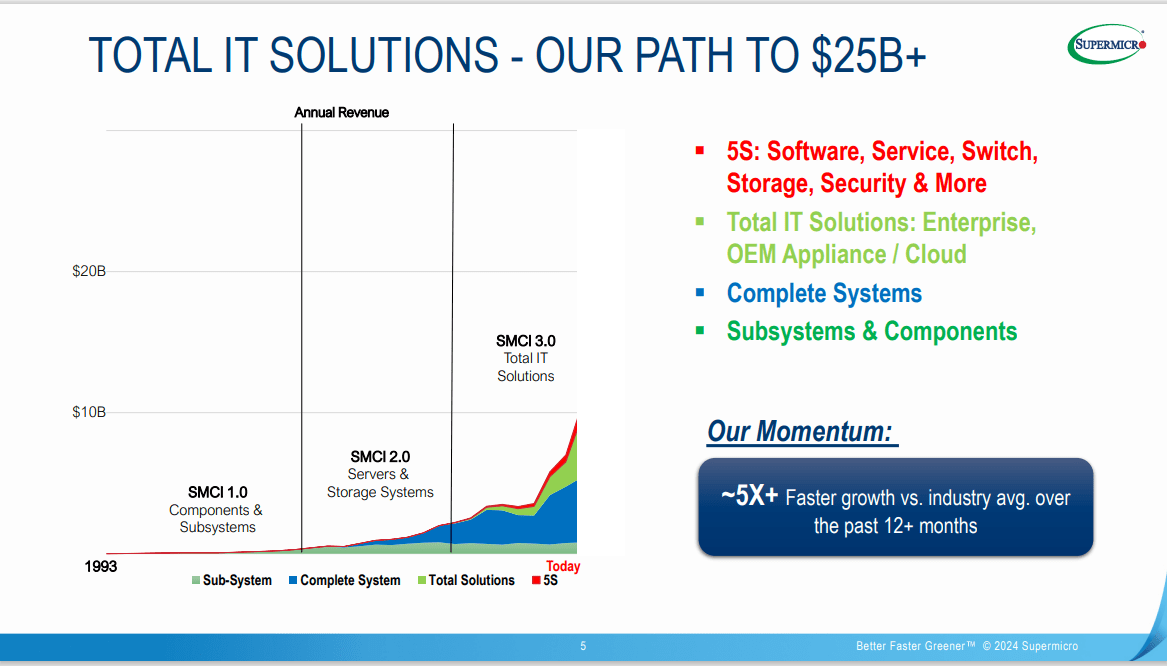

CEO Charles Liang also mentioned that Super Micro 3.0 is in “overdrive”. Super Micro 3.0 denotes the strategy shift to becoming a supplier of full IT Solutions. They are planning their next phase of growth with Super Micro 4.0 but didn’t give any detail about what this is.

Super Micro Q2 FY24 Investor Presentation

Production Capacity

By June 2024, management expects to have a production capacity of 1,500 DLC (Direct Liquid Cooling) racks per month and a total rack capacity of 5,000 rpm.

The San Jose, Netherlands, and Taiwan facilities are operating at a 65% production utilization rate. They are also adding two new production facilities and warehouses in Silicon Valley. They are using the new Malaysia facility to expand their Building Blocks capacity, presumably by designing different systems with leading-edge chips that fit a variety of different server node configurations. More and more customers will be able to order fully customizable AI-optimized racks from SMCI.

This increased production capacity will support their new $25b annual revenue target. Given the $20b revenue target aligns with 5,000 rpm or 60,000 racks per year, it follows that we can expect annual production capacity to increase to roughly 75,000 to make the $25b revenue goal achievable in the coming years.

Super Micro is scaling globally and, with it, its manufacturing operations.

Valuation

For the past year, Super Micro was trading at a stunningly low valuation. Recent price performance has brought it closer to a fair value, but I believe the stock still presents an attractive growth opportunity.

Seeking Alpha Quant rates Super Micro a ‘D’ mostly because it looks quite overvalued using backward-looking metrics. On the FWD basis, SMCI trades at a 26 Non-GAAP P/E and 30 GAAP P/E. For a company guiding for growth well into the double digits, this is a very modest multiple. Its PEG ratio is significantly below that of the industry average at 1.06, earning an A- Seeking Alpha grade.

The company guided for full-year revenue on the low end at $14.3b, so the $27.68b market cap still represents less than a 2 FWD P/S ratio. However I don’t believe P/S is a good metric for such a low gross margin business, so this should be taken with a grain of salt. SMCI is opting for gross margin compression for the sake of growth, which I believe will be a net positive for shareholders over time.

The company has rapidly growing sales and profit, immaterial debt levels, and exposure to, in my view, one of the most promising end markets in the modern world. Despite its parabolic 2023 performance, SMCI still looks to be trading at a fair value today.

Risks

The key risk here is volatility. The stock traded mostly sideways for the last three months of 2023 and regularly has 5-10% daily swings. Volatility is not something many investors can stomach and can lead to panic selling and major losses. Especially with such a strong YTD return, I expect this volatility to increase in severity in 2024. Any SMCI investor has to be willing to take a long-term view and ride out short-term volatility because there will be plenty.

Further, SMCI performance will be acutely linked to Nvidia and other leading chipmakers’ results. Any negative news as such will materially impact SMCI’s stock, even if the news doesn’t particularly impact SMCI’s core business. While SMCI has been one of the best trades of 2024 so far, such a rapid rise can lead to similarly rapid descents. Wall Street operates on a percentage basis, so the higher highs will lead to more drastic nominal moves on an ongoing basis. A year ago, a 10% drop represented a nominal decline of $7.23. Today, a 10% drop would be $51.30.

For this reason, I wouldn’t recommend SMCI to investors with a short-term time horizon, as the beta is quite hard to stomach. For example, I added to my existing position in early August 2023 at $351, which now looks like a great trade. However, from mid-August 2023 to early January 2024 it was a wholly unprofitable decision. The stock didn’t improve from that price point until the recent earnings pre-release.

An investment in SMCI carries with it the expectation of severe volatility. Investors who aren’t able to stomach that volatility will likely take big losses. Despite this risk, I firmly believe SMCI will be worth significantly more five years from now than it is today, so long-term investors still have an opportunity to participate in the growth story presented.

Conclusion

Super Micro has had one of the most incredible calendar years of any stock I’ve ever researched. They are growing at a mouth-watering pace and executing bold business goals. Many investors will be scared by the yearly price graph, so I suggest a strategy of dollar-cost averaging or taking a small starter position before diving deeper into SMCI. Regardless, I believe this is a business that you will benefit from investing in over the long term.

Q2 2024 Earnings Call Transcript")