Justin Sullivan

Investment action

Based on my current outlook and analysis of Levi Strauss & Co. (NYSE:LEVI), I recommend a buy rating. While I agree that the macro conditions are not perfect for LEVI, I really like how the business has executed the DTC transition so far, which has driven margin in the right direction. The management decision to implement a restructuring program today is also something I am in favor of because now is the best time to better position the business for growth since growth opportunities are scarce. The valuation certainly isn’t in demand either, as LEVI is trading below its historical average. That said, I think investors should remain cautious when building their positions in LEVI, as near-term results could be volatile due to the macro environment.

Basic Information

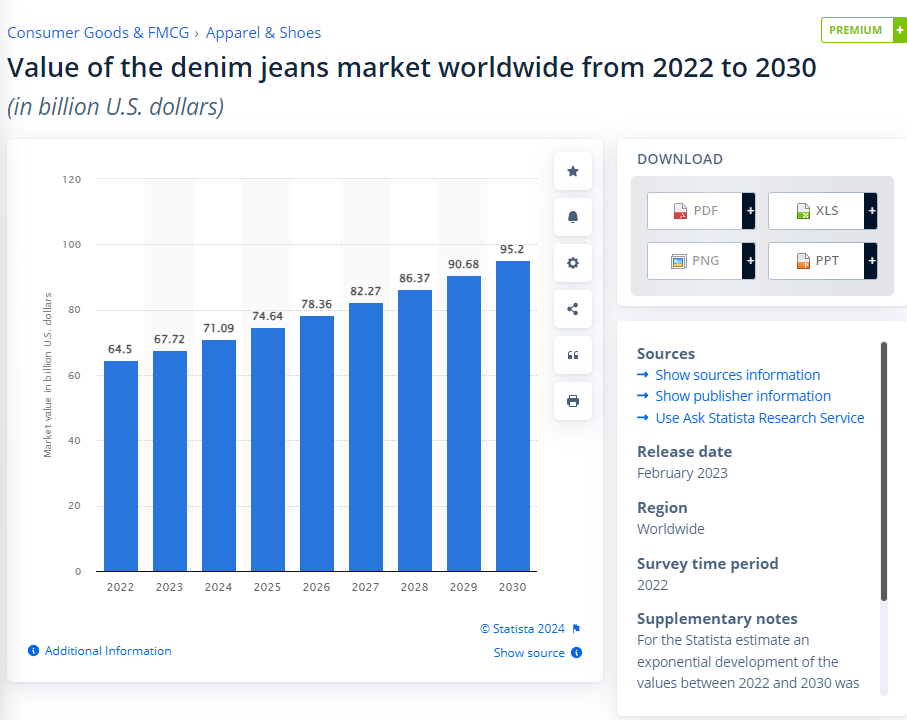

LEVI is a global jeans wholesaler and retailer. The business has a presence in the Americas, Europe, and Asia. While the company operates under several different brands, Levi’s brand accounts for the largest share of the pie. It is hard to find the actual size of the LEVI addressable market given that it sells a wide range of products made of various materials. To get a sense of the market size, I used the global denim jeans market as a benchmark to figure out the LEVI market position and the industry outlook. Based on Statista market size estimates and LEVI FY23 revenue, it seems that LEVI has a market share of maximum high single-digits. Given that LEVI’s total revenue includes other products outside of jeans and the market size shown below is just denim jeans, I would put LEVI’s market share to be around mid-single-digits. The industry is also expected to grow, which should be a tailwind for LEVI in the future.

Statista

Macro pressure weighing on growth in the near term

Although the industry is expected to grow over the long term, I believe the LEVI near-term growth outlook is going to be heavily dampened by the weak macroeconomic conditions. The nature of LEVI’s products is discretionary, and in bad times, consumers tend to cut back on discretionary spending because their disposable income shrinks. While US (50% of FY23 sales) inflation has tapered since the 6% level, inflation has proven to be sticky, and I believe it is likely to persist in the near term. This also undermines the probability of a rate cut by the Fed in the near term (yes, they did announce their intention to cut rates, but if inflation and unemployment stay strong, it will be hard to justify a cut). The fact that US holiday season sales were weaker than expected is a sign that the higher cost of living is eating into consumers’ disposable income. Aside from the US, an uncertain economic outlook is expected for Europe (26% of FY23 sales) as well.

The pressure from the macroclimate can be seen in LEVI’s 4Q23 performance and guidance. For the US, management is guiding for low-single-digit FY24 growth despite FY23 being an easy comp year (FY23 US growth down -3.2%). Regarding Europe, the wholesale market was still facing challenges in 4Q23 due to the fact that wholesale partners are being prompted by a more dynamic macro environment to be cautious when planning their orderbooks. Peer comments on Europe were not positive as well.

Like others, we have seen a more challenging macroeconomic backdrop in Europe, and that is impacting consumer confidence and the wholesale channel. PVH 3Q23 call

DTC transition

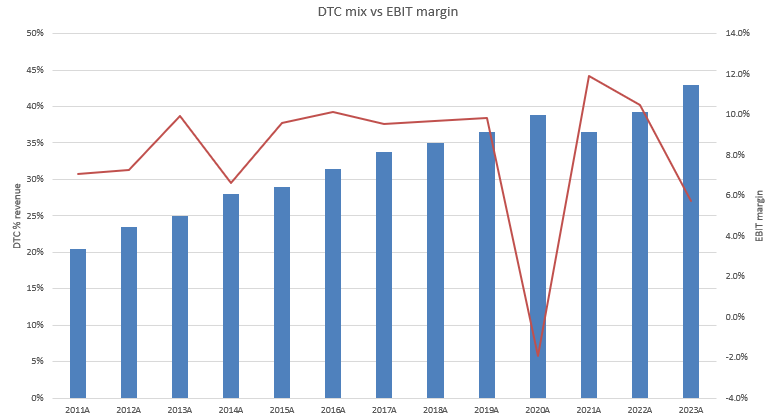

What I do like about LEVI that makes me feel positive about it when the economic cycle turns is that it is executing really well on its DTC (direct to consumer) strategy. LEVI has spent the last several years focused on increasing penetration of the structurally higher DTC channel, with the goal of hitting ~60% penetration.

Along with the key contributors to the structural drivers of our gross margin, including DTC, international and women’s, we expect continued improvement in 2024 as we progress on our path to 60% as discussed during our 2022 Investor Day.

In my opinion, as a retailer (particularly for fashion) that has a recognizable brand, having a DTC model makes the most strategic sense. Firstly, you get to control the brand much better in terms of pricing, distribution, and market presence. Imagine Chanel running a wholesale model; the entire brand value deteriorates as the product is no longer scarce, and as it becomes more common, the urge to purchase it becomes less. While LEVI is not a luxury brand, I think the principles are the same, in that LEVI will have better control over where and how its products will be displayed (on a mannequin vs. lying around with a dozen other cheaper brands) and pricing (especially when determining discounts and promotions). Secondly, it has a better margin profile given that LEVI does not need to give a cut to the middlemen.

Author’s work

The result of this transition is evident in LEVI EBIT margin expansion from FY11 until pre-covid, where margins expanded by around 800 bps and by nearly 45% post-covid. While EBIT margin has been pressured in FY22/FY23 due to the macro situation, I believe it is fair to say that, on a like-for-like basis, LEVI now has a structurally higher margin profile once the cycle turns.

Another great thing about a DTC strategy that can drive top-line growth is that LEVI has more data about its targeted consumers. This enables LEVI to have better insights on what product to launch, especially those with high gross margins like women’s and tops. LEVI’s acquisition of Beyond Yoga was a telling sign that management is executing well on this front as well.

International, definitely helping, and there we are really focused on is growing women’s which is accretive to gross margin growing Beyond Yoga, which is accretive to gross margin. So those are the things that are structurally helping. 4Q22 call

Global productivity initiatives

Together with the ongoing DTC transition, I also feel positive about management implementing a restructuring program during this period (this is the best time to restructure as growth opportunities are scarce). The two-year plan that the management has laid out to optimize the operating model, redesign the company, and find places to cut costs is anticipated to produce a net savings of $100 million in FY24. Prioritizing resources to accelerate direct-to-consumer growth with a smaller wholesale business is the first objective. Secondly, it is to boost procurement skills to help LEVI better manage inventory, free up working capital for cash, improve COGS, and lastly, improve productivity in stores. The financial implication is that top line and gross margin should see a direct impact, and because of operating leverage, EBIT and earnings should see elevated growth.

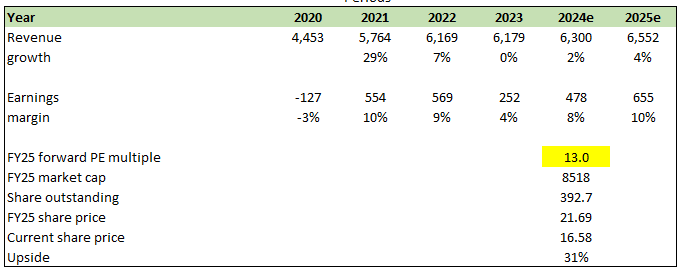

Valuation

Author’s work

I believe LEVI can grow at 2% in FY24 (management guidance) as the business continues to execute well on the DTC front, although the macro pressure will continue to put pressure on growth (2% growth is below industry-expected growth). In FY25, I expect the macro conditions to be much better, which should improve the discretionary spending environment. That said, I am being conservative in assuming any major growth acceleration as LEVI. I assumed 4% growth in FY25 (the midpoint between 2% in FY24 and 7% in FY22). However, I am more bullish on margin expansion as the two key drivers – the DTC transition and restructuring program – are independent of the macro environment. Given how LEVI has executed so far, I think margin expansion is achievable. That said, I think the market will continue to stay wary of the growth outlook; hence, any re-rating in multiples will only happen when there are obvious signs that the cycle has turned (it could be in FY25, but I am not speculating on this).

Risk and final thoughts

Historical success in the DTC transition could be due to the low-hanging fruits (ending wholesale relationships with weak wholesalers, for example), and future transitions could be a lot harder as LEVI may hurt wholesale relationships from here on. As such, DTC penetration could slow from here, making the margin expansion outlook weaker. Weaker macro conditions will also hurt both revenue and margin outlooks as consumers spend even less.

I recommend a buy rating for LEVI based on positive factors such as the execution of the DTC transition and the implementation of a strategic restructuring program. The ongoing restructuring program, emphasizing cost savings and enhancing operational efficiency, further supports future margin expansion and growth. While near-term growth may face headwinds, I believe LEVI will be in a better position to grow and expand its margin in the next upcycle. That said, investors should remain cautious due to macroeconomic pressures affecting both revenue and margin outlooks.

Q2 2024 Earnings Call Transcript")