SDI Productions/E+ via Getty Images

Northrim BanCorp (NASDAQ:NRIM) is a small bank that capitalizes only $300 million and operates in Alaska. Although not well known among retail investors, I find this bank very interesting and apparently the market thinks the same: its price per share is near an all-time high.

This bank has fully recovered from the crisis that resulted from the failure of SVB and has a major competitive advantage dictated by its geographic location. In fact, the top 4 banks in Alaska (including Northrim) have 90% deposit market share. Linking to my previous article on NRIM, the strengths of this bank remain unchanged as do its future prospects. It is a growing market and has the potential to capitalize on this trend.

Despite missing EPS estimates in Q4 2023 by $0.05, I view this quarterly as positive overall.

Loan portfolio and NPLs

Investor Presentation Fourth Quarter 2023 Nasdaq: NRIM

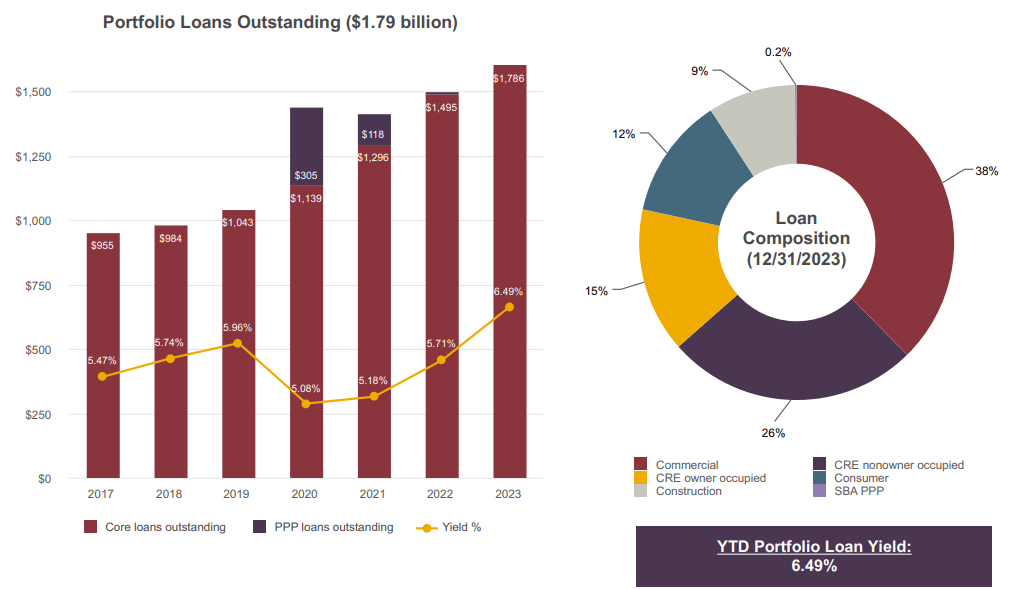

The loan portfolio reached $1.79 billion, up a whopping 19.50% from the previous year. This is a great result and is supported by a still low LTD: only 72%. So, management still has a good margin to lend at current market rates. The YTD portfolio loan yield was 6.49%, a good figure but one that could change a lot in the coming months given the maturity structure.

- 31% of loans mature or reprice in the next three months, 15% of loans mature or reprice in three to twelve months, and 16% of loans mature or reprice in one to two years.

- 18% of earning assets reprice immediately when prime or other rate indices change.

Basically, only 38% of total loans will be repriced after the two years, all others will be repriced earlier. This exposes the bank to considerable rate risk should the Fed cut rates more than expected. In addition, most of the loans belong to the commercial category, which could make this bank’s profits rather cyclical.

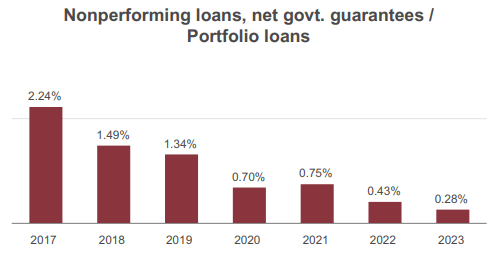

In any case, the strength of deposits and low NPLs reassure shareholders at the moment.

Investor Presentation Fourth Quarter 2023 Nasdaq: NRIM

Typically, NPLs rise when rates are high, as it coincides with the time when borrowers begin to struggle to pay their installments. However, this is not the case for NRIM, whose NPLs are at an all-time low since 2017, only 0.28%. This is a sign that the loan portfolio is high-quality.

Deposits and NIM

Investor Presentation Fourth Quarter 2023 Nasdaq: NRIM

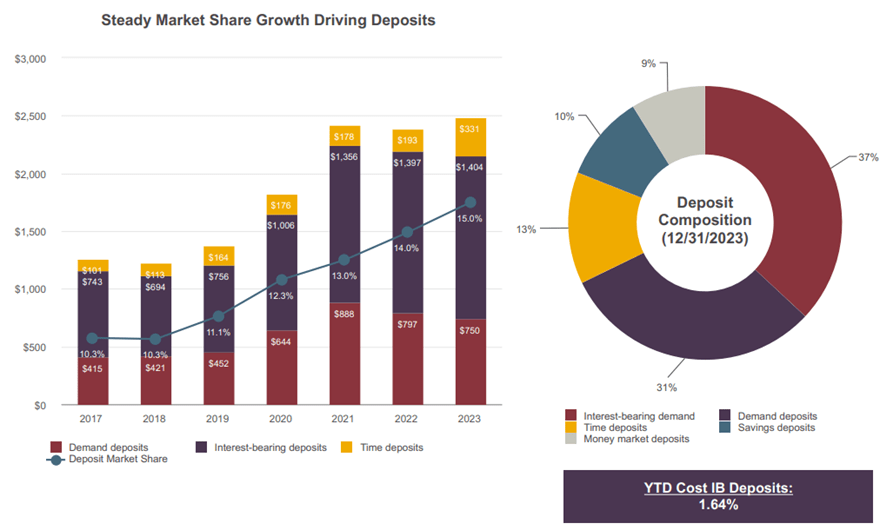

Total deposits reached $2.48 billion, an increase of 4.20% over last year. The composition of deposits remained about the same, with non-interest bearing deposits accounting for about one-third of total deposits. Interest-bearing deposits and time deposits have taken on greater weight but the YTD cost IB deposits still remains very low: 1.64%.

This is the main advantage of NRIM, namely being able to obtain resources at a relatively low price compared to current market rates. After all, there are very few competitors in Alaska and it is not surprising: suffice it to say that 6 branches can only be reached by boat or plane. Operating in this territory means accepting higher operating costs than the average regional bank, but just as there are disadvantages there are also advantages, in this case low competition.

By the way, NRIM is getting a larger and larger share of the deposit market in Alaska: in 2018 it was 10.30%, in 2023 it reached 15%. So, this bank does not have a hard time finding low-cost liquid resources, which is why the LTD ratio is so low. At the same time, it is difficult for new competitors to enter this niche market so full of pitfalls: the last one was Wells Fargo in 2000 buying National Bank of Alaska.

Investor Presentation Fourth Quarter 2023 Nasdaq: NRIM

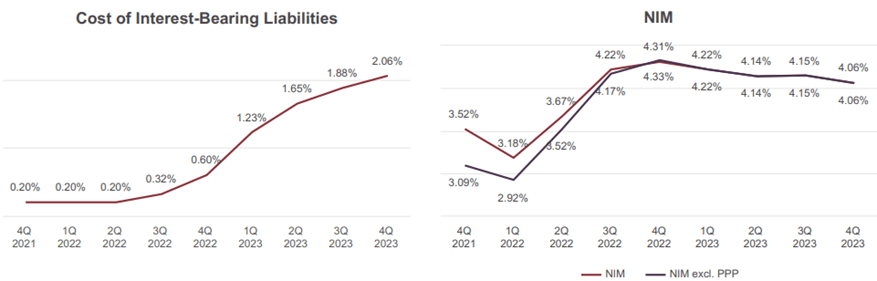

Given the low cost of interest-bearing liabilities, the NIM as a result is quite high, namely 4.06%. It has been steadily declining since Q4 2022, but still remains a strong performance.

Shareholder remuneration

In addition to deposits, the other striking aspect of NRIM is shareholder remuneration. From this point of view, this bank almost looks like a non-financial company. Dividends and buybacks are the priorities and the results achieved in recent years have been impressive.

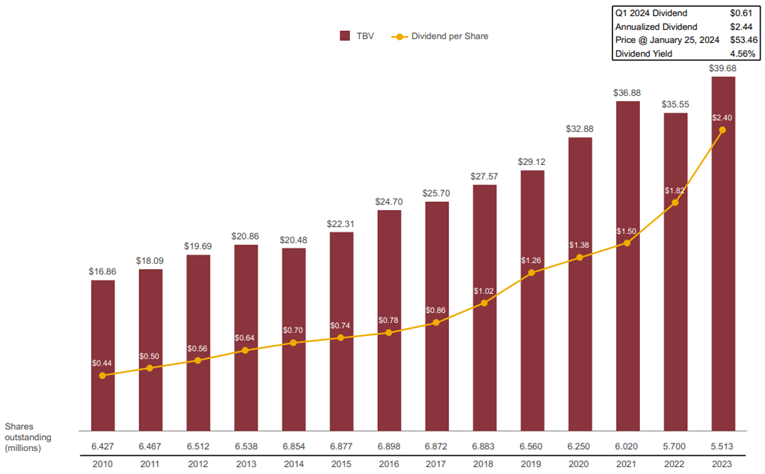

First of all, about 20% of the outstanding shares have been bought back in the last 5 years, and the buyback has not ended there. A few days ago the Board authorized the repurchase of 110,000 additional shares. In addition, this huge buyback has not adversely affected the growth of TBV per share, the main factor on which the price per share is based.

Investor Presentation Fourth Quarter 2023 Nasdaq: NRIM

Almost every year TBV per share has increased, which explains why this bank is near an all-time high. Also, the dividend has been increased substantially, and few banks can keep up with such a growth rate.

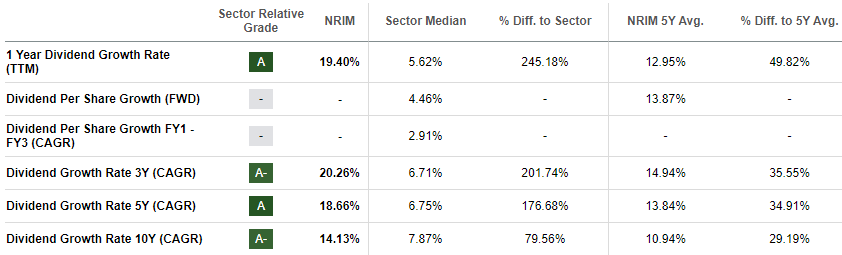

Seeking Alpha

As you can see from this image, over 3-5-10 years NRIM’s dividend growth is far above the industry median. Moreover, at least for the time being, its sustainability is out of the question.

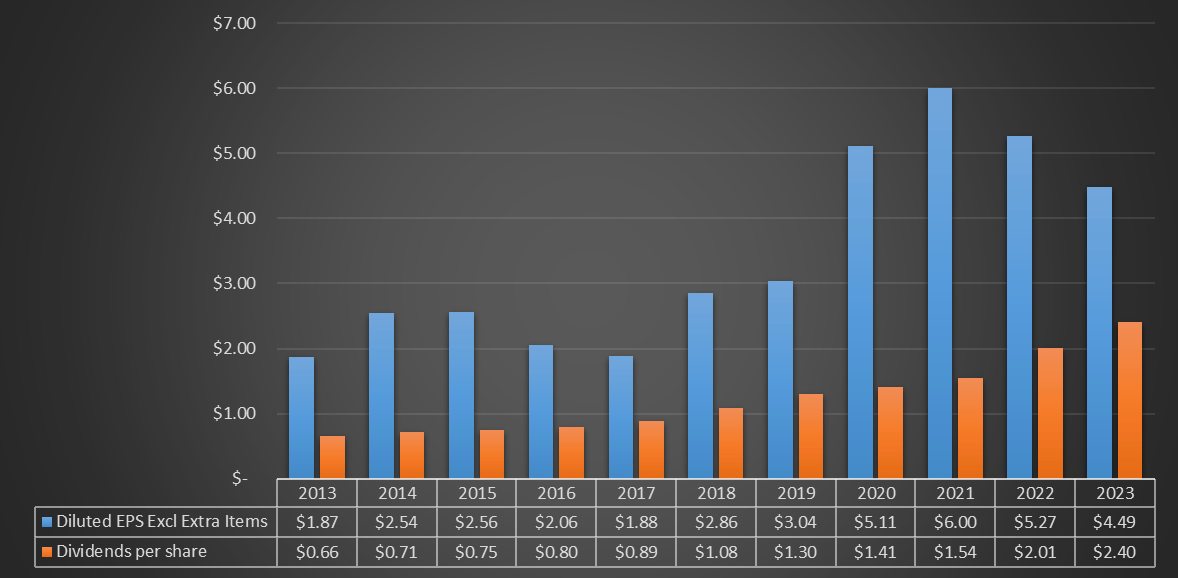

Chart based on Seeking Alpha data

EPS largely covers the dividends issued, albeit not as much as in the past. The reduction in EPS compared to 2021 may be a concern, but in my view this is a temporary difficulty. After all, the macroeconomic environment has deteriorated a lot and NRIM has still shown resilience by keeping NIM high without growing NPLs. In other words, once there is clarity on the future of monetary policy, I expect that NRIM can continue to grow as in the past. Nevertheless, the long-term trend remains bullish on EPS, as well as TBV per share and deposit market share.

Conclusion

Northrim BanCorp is a bank operating in Alaska and its competitors can be counted on the fingers of one hand. While this is good as it almost leads to an oligopoly regime, higher operating costs dictated by adverse weather conditions should be highlighted. Regardless, the end result is an NIM above 4% with extremely low NPLs. EPS is struggling to grow, but the long-term trend remains bullish as does TBV per share.

Finally, shareholders have been well compensated over the past 5 years, both through buybacks and double-digit dividend growth. The latter’s growth will probably slow somewhat in the coming years, at least until EPS returns to growth. Although NRIM is close to an all-time high, the dividend yield remains quite high at 4.40%.

Q2 2024 Earnings Call Transcript")