Jitalia17

There are a lot of dividend paying stocks out there, but few look as attractive as Prudential (NYSE:PRU) does right now. The company’s operations are poised to pay the firm’s enticing ~4.7% dividend well into the future, and shares appear reasonably valued, trading at only a very slight premium to historical measures.

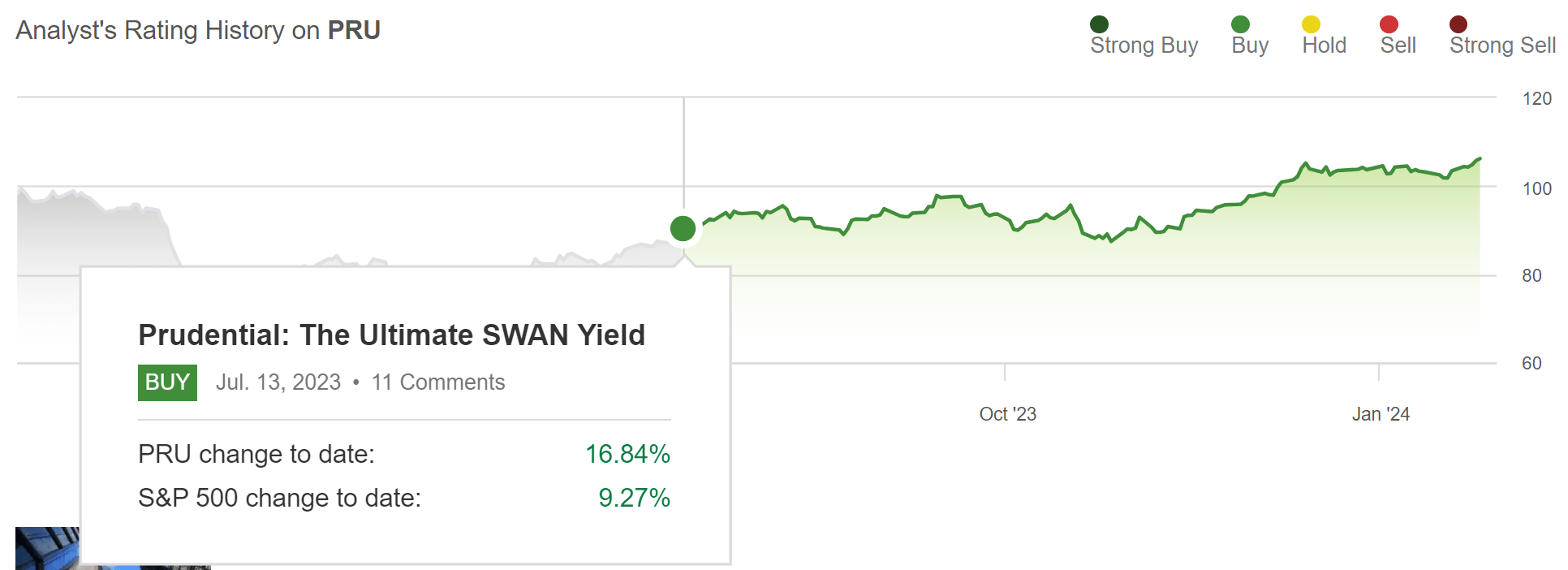

When we wrote about the company in July of last year in an article titled “Prudential: The Ultimate SWAN Yield“, we made the case that the company had a number of strong tailwinds powering the yield, and that investors in the name could rest easy. Since then, the stock has outperformed the S&P 500 handily:

Seeking Alpha

Today, we thought it would be good to catch up with this thesis and see whether or not PRU is still poised to perform well looking into 2024 and 2025.

Is PRU an attractive looking buy in the market today? We certainly think so, and here are 3 key reasons why you should consider adding PRU to your portfolio, if you don’t already own some shares.

Let’s dive in.

1.) Business Strength

If there’s one thing to know about Prudential, it’s that the company is exceedingly well diversified across businesses and geographies.

A breakdown from our first article explains this rather simply:

In case you’re unfamiliar with Prudential, it’s a multi-pronged financial services company based in Newark, New Jersey. The company has three main lines of business:

- PGIM

- ‘U.S. Businesses’, which contains:

- Retirement Strategies

- Group Insurance

- Individual Life

- and ‘International Businesses’

PGIM is the company’s investment management arm, U.S. Businesses covers the company’s insurance and pension operations, and International Businesses account for investment management and insurance businesses internationally, like Prudential Japan, Prudential Africa, etc.

Essentially, the company is a hybrid between an asset manager and an insurance company operating in lots of global markets.

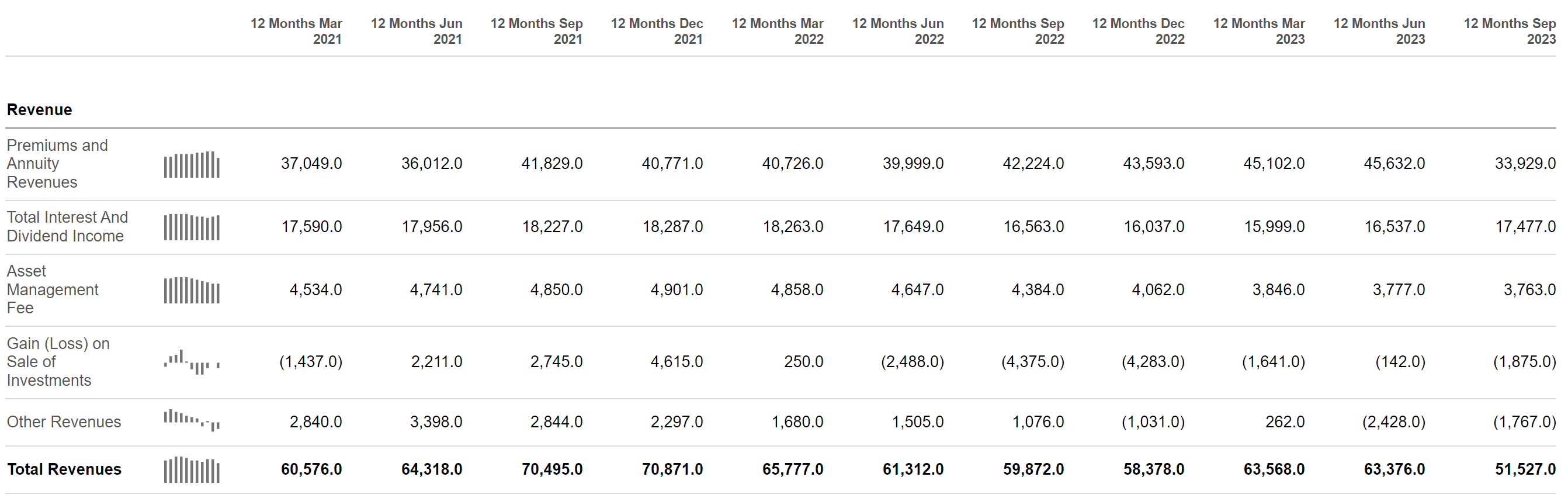

However, despite the broad lines of business, PRU is still primarily an insurance company, with the lion’s share of company revenue derived from premiums and annuities:

Seeking Alpha

This hasn’t changed since our last article on the company, and we expect that the company’s insurance business will continue to make up the bulk of PRU revenues for the foreseeable future.

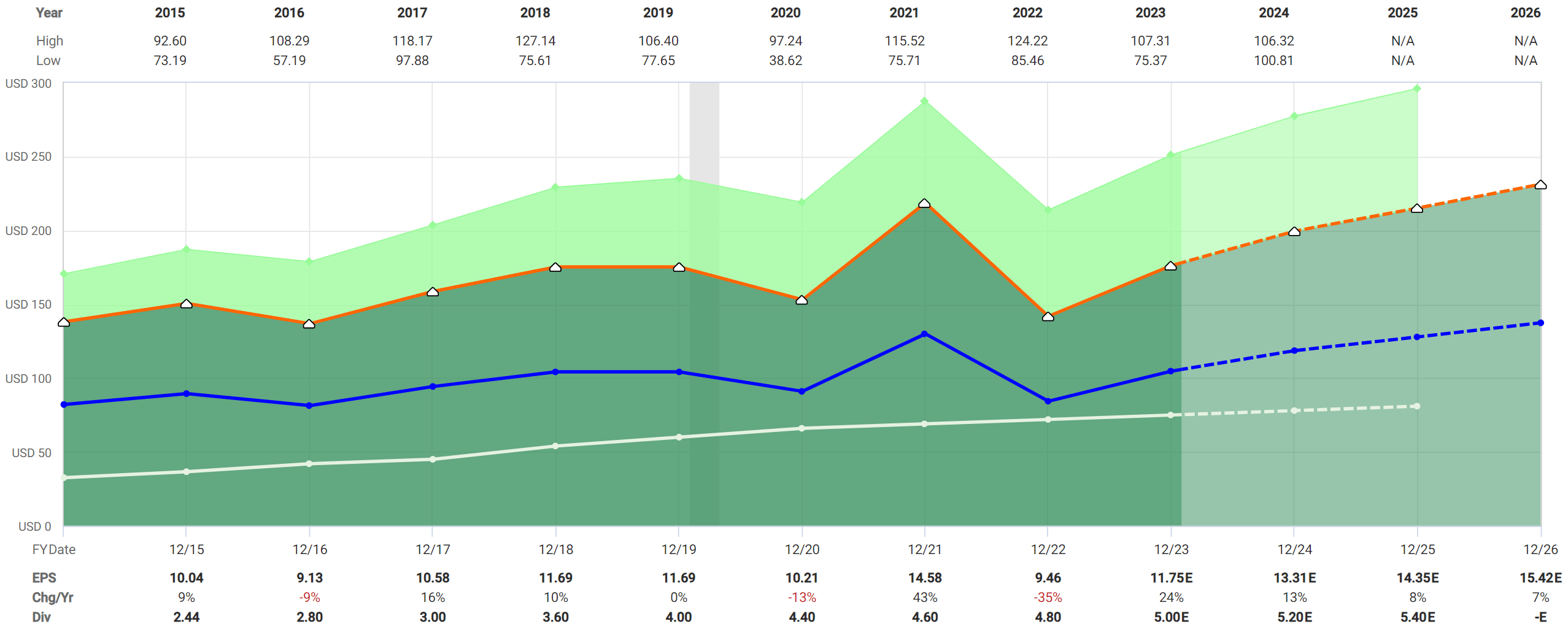

Looking forward, analysts see EPS growing throughout 2024 & 2025, and into 2026, on the back of a lower expected rates environment, a strategic relationship with LPL Financial (LPLA), and continued momentum in places like Brazil:

FAST Graphs

The company’s new business unit, Prismic, is also of interest, as an in-house annuity reinsurance company is highly synergistic with PGIM’s asset management business. This appears doubly true, especially considering that Prismic may also end up taking outside business for other companies that need annuity reinsurance. Here’s what Charles Lowery, Chairman & CEO had to say about it:

It is one of our most exciting opportunities to drive sustainable long-term growth across our investment management, insurance and retirement businesses. Through Prismic, we can ensure portions of our life and annuity in-force and new business to reduce market sensitivity, free up capital and invest in growth opportunities. Prismic can also offer its services to other insurance companies in need of reinsurance support, tapping into additional sources of third-party capital to drive further growth.

In addition, Prismic expands PGIM’s assets under management. Prismic is a great example of how Prudential can unlock value for customers, shareholders and other stakeholders with our mutually reinforcing business system, which combines the power of our brand, global asset and liability origination capabilities and multichannel distribution.

This last bit is the key here – management is showing the ability to utilize PRU’s brand, scale, and balance sheet to attract new business to the firm.

For us, this means that we’re optimistic about PRU’s coming earnings release, which is slated to report next Tuesday. Analysts are expecting $2.72 in earnings, but given the positive catalysts we mentioned, we’re expecting numbers a bit higher than that.

We’ll be looking at the following numbers to get a better sense of how things will continue to progress over time:

- Prismic committed capital growth

- PGIM investment outflow stabilization

- Operating income improvement

These are all important keys to continued business velocity on both the top and bottom lines, so increases should bode well for us as investors.

Finally, when combined with PRU’s strong balance sheet, it’s tough to argue that PRU is anything but a genuinely strong SWAN play.

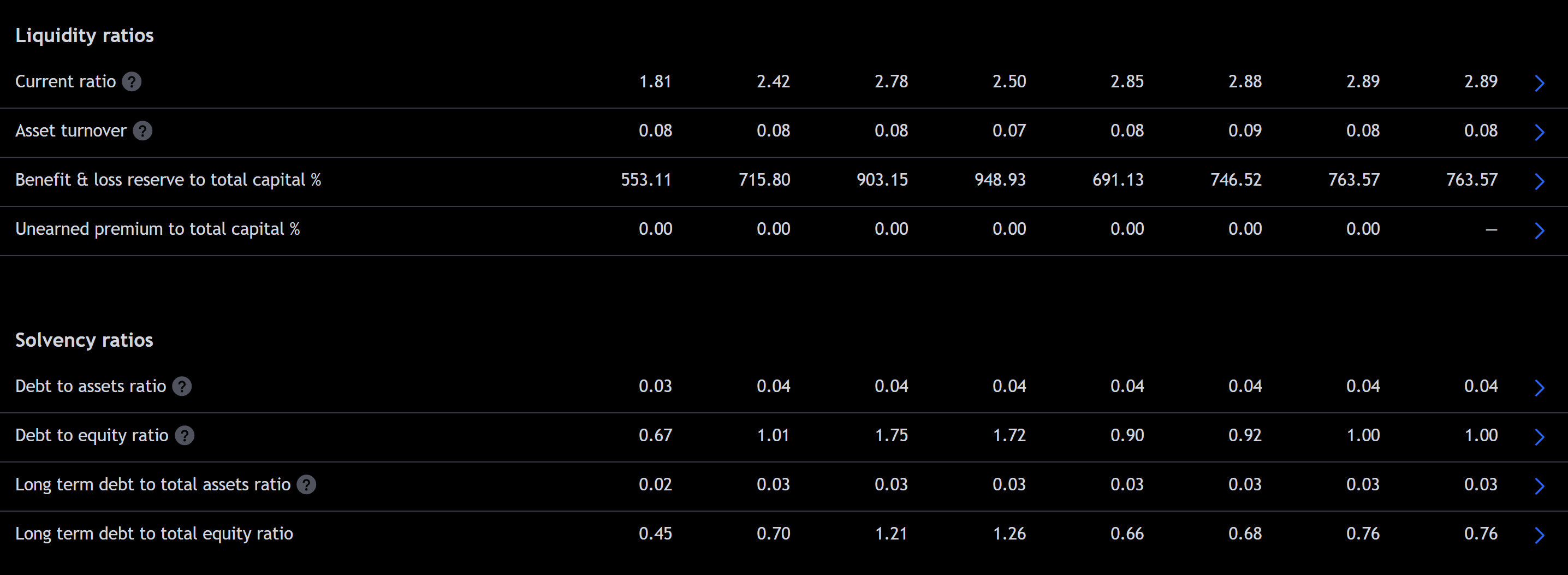

With $681 billion in total assets, only $25 billion in debt, and more than $25 billion in tangible book value, PRU appears to be highly insulated from market volatility, business cycle shocks, and other solvency/liquidity issues:

TradingView

All in all, PRU appears to be a well-capitalized, growing global insurance and financial services firm, with solid synergies throughout the company’s lines of business and significant future EPS growth potential.

2.) Dividend Strength

This strength across the business translates to a high level of dividend safety and yield, which makes shares in PRU appear highly attractive at this point in time.

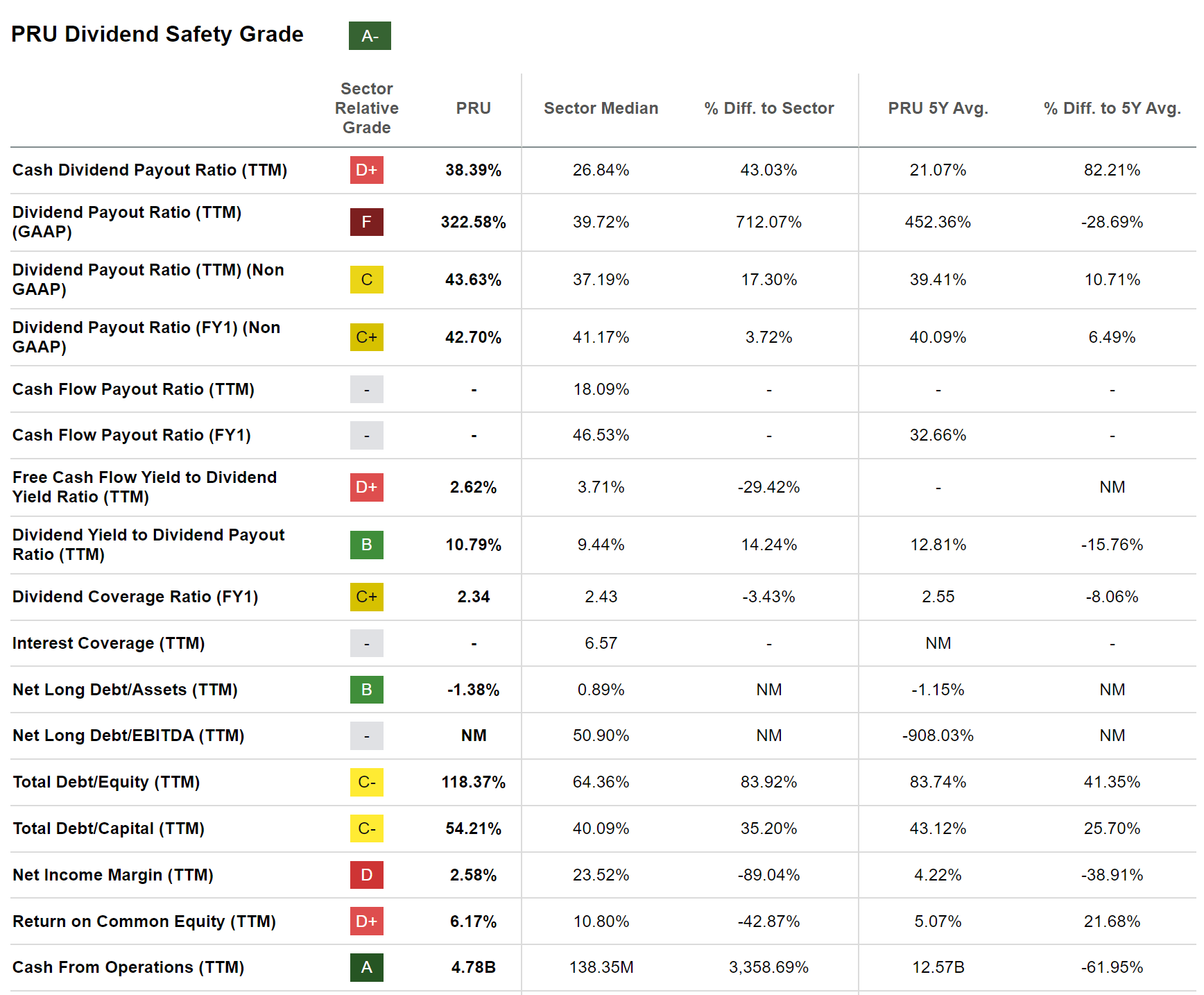

Right now, PRU pays a 4.7% dividend yield, which is well covered. Seeking Alpha’s Quant rating system gives the Dividend a Safety rating of “A-“, which is something we agree with:

Seeking Alpha

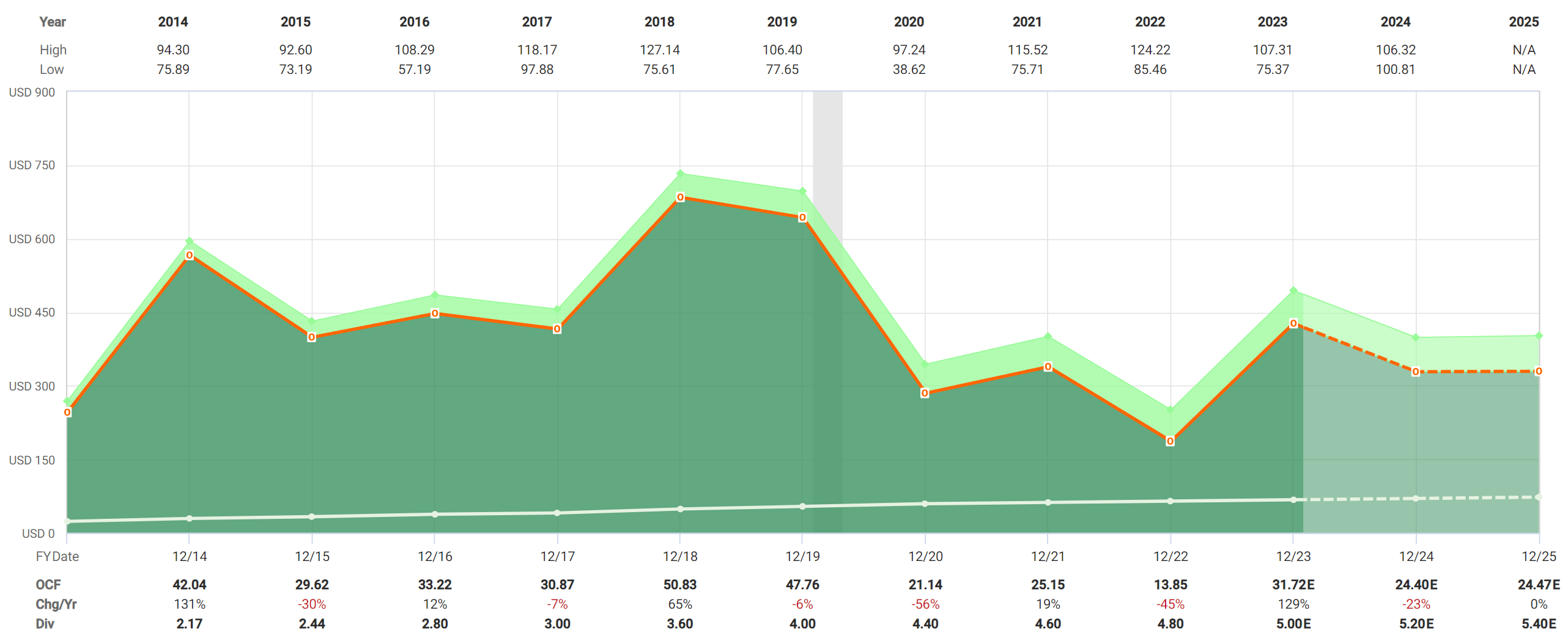

Some of the metrics here may appear unattractive, but this is largely due to some earnings lumpiness that PRU has experienced over the past few quarters. In reality, the dividend is more than covered by the company’s operating cash flow, which has been steady at more than $20 per share over the last decade plus, save 2022 and the associated interest rate situation:

FAST Graphs

Above, the white line at the bottom of the graph is the dividend payout. As you can see, there’s a tremendous amount of room for the payout to be sustained, or even raised, over time – especially considering that the current payout is only expected to be $5 per share over the coming twelve months.

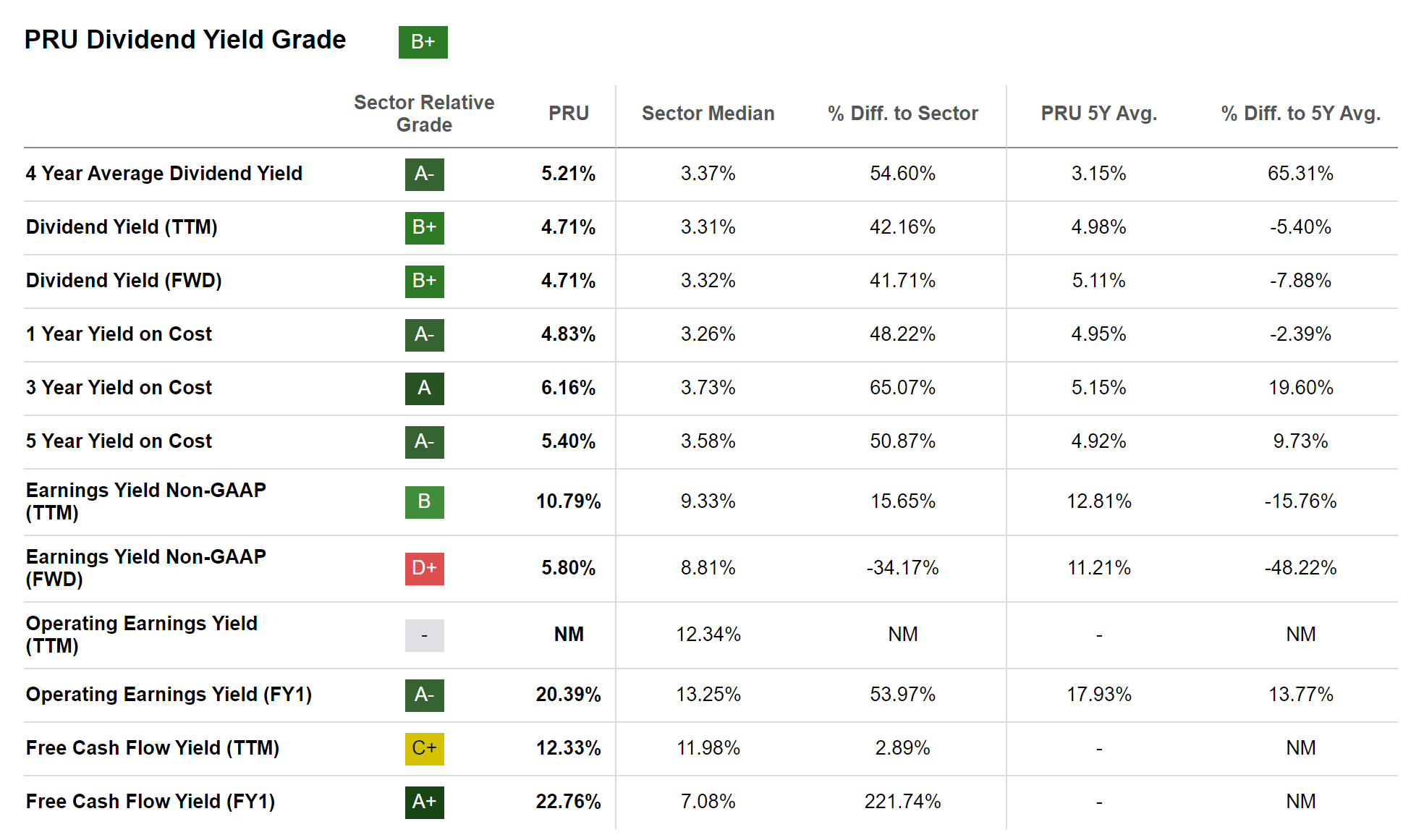

While the dividend appears safe, the yield is also quite high, coming in at a rate of 4.71% (“FWD”) as of writing:

Seeking Alpha

This is significantly higher than the financial sector’s (XLF) average yield of 3.32%.

Additionally, PRU has sustained a higher payout over time, with a 4 year average dividend yield of 5.21%, which is more than 50% higher than the sector. This indicates a high level of certainty on the part of management that the dividend can and will be sustained well into the future.

As we wrote in our first article – between the defensively positioned business and the high payout, PRU still appears to be a SWAN-type yield at nearly 5%.

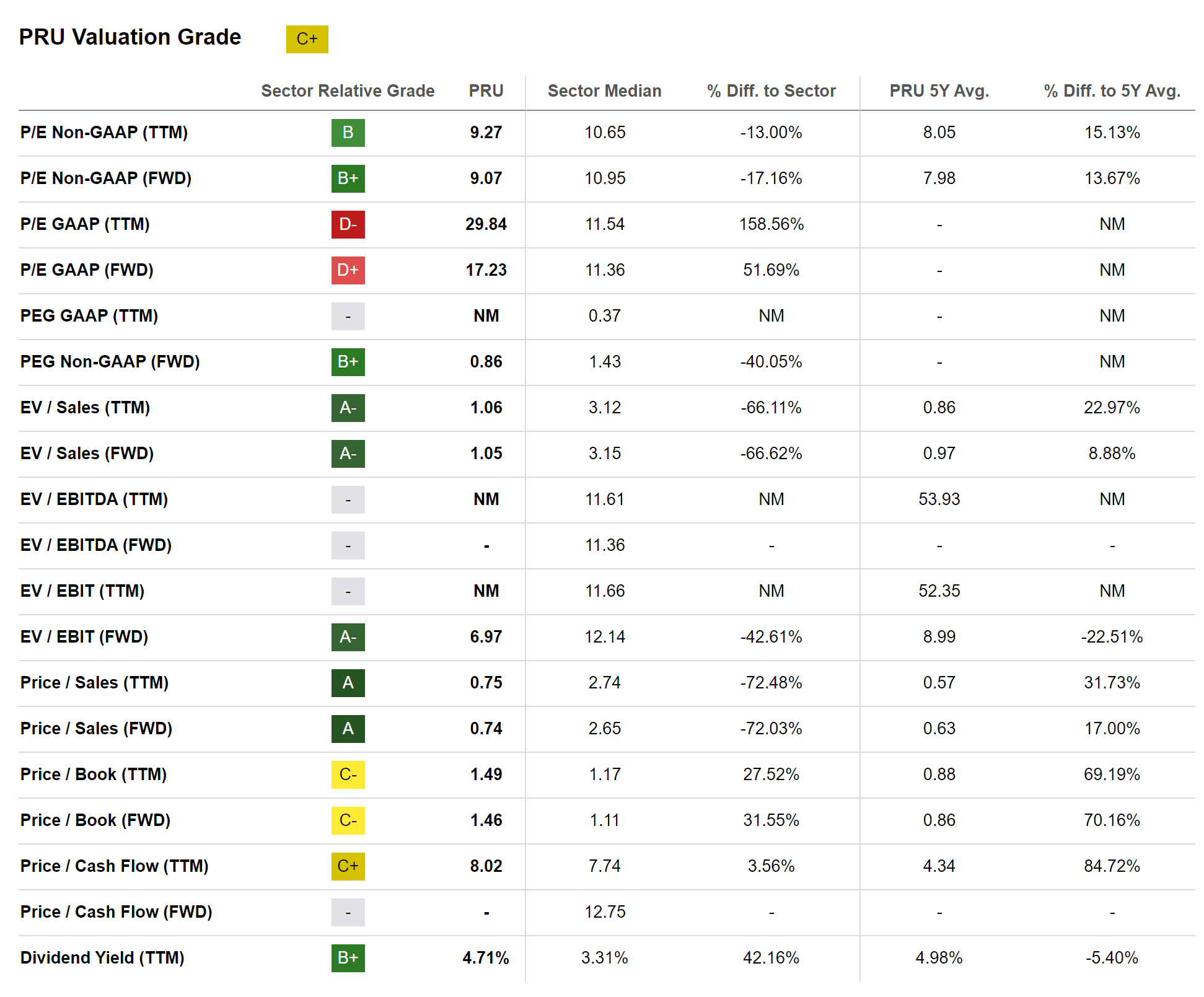

3.) The Valuation

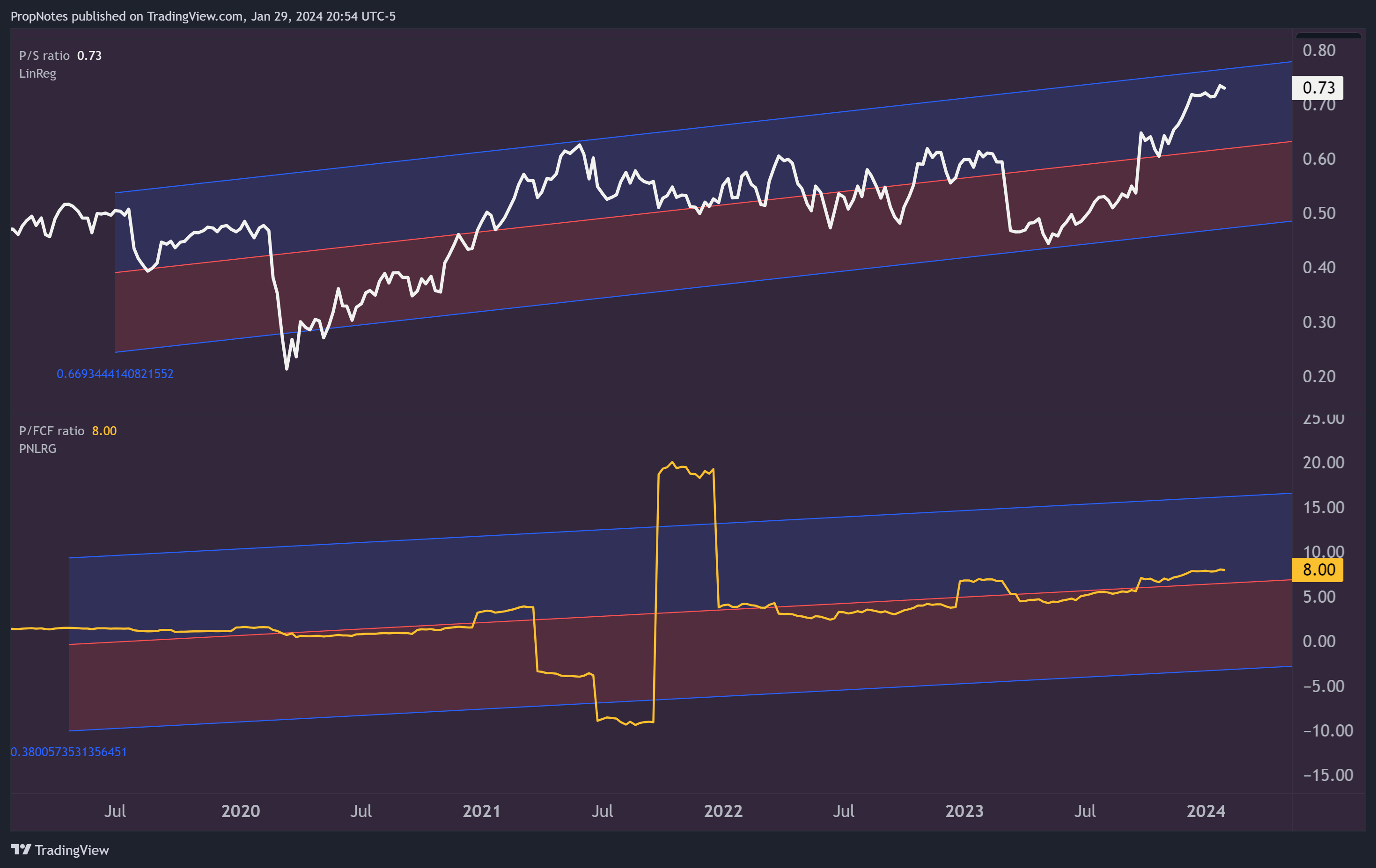

However, despite the value that this status has to investors, the company appears reasonably valued at only 9x forward Non-GAAP earnings. The sales multiple is looking a bit historically extended at 0.7x, but this is largely due to recent revenue slowdown which should ameliorate over time.

The FCF ratio is also extended somewhat, but it remains within the linear regression range below, indicating an average, if not completely unreasonable historical price for PRU shares:

TradingView

Seeking Alpha’s Quant Rating System also puts PRU in this ‘middle of the road’ range, at a ‘C+’:

Seeking Alpha

Price / Book and GAAP valuations appear stretched somewhat vs. historical multiples, but adjusted numbers appear far more palatable, and given the lumpy nature of some of PRU’s recent quarterly results, we’re happy going by these ratios.

In our eyes, fair value for PRU shares is somewhere between $110 – $135. We arrived at this by taking the 9y normal P/E of 9x and adjusting 10% in either direction for fair value purposes, which results in a multiple between 8.1x and 9.9x. Combined with projected ~10% EPS growth over the coming year, the FV range represents material upside towards $125 per share over the next year.

While the price we recommended the stock at last year was certainly ‘better’, there’s enough upside moving forward to re-iterate our view.

As long as you don’t need to pay through the nose for this yield, we’re happy to remain bullish on the stock.

Risks

We’ve laid out the positives to PRU; the huge capital moat, the diversified operations, the well covered dividend, and the reasonable entry point multiple.

However, there are some risks to consider here as well.

The key risk to watch here is with interest rates. Long duration exposure caused a significant hiccup for PRU in 2022’s EPS numbers, and further volatility on this front could cause more earnings swings going forward.

In addition to rates exposure, PRU is also exposed to the global economy to a greater degree than other, more U.S. focused insurance companies. This comes with its own set of risks and rewards, including regional instability, FX risk, and significant operational complexity to consider.

However, PRU has appeared to weather these risks in the past with a high degree of competency, and thus we believe that these exposures and risks remain muted for now.

Summary

All in all, PRU appears to be a highly attractive income investment opportunity, with diversified business operations and a safe, robust yield. Plus, it trades at a historically reasonable multiple.

There are some risks to consider around interest rates, FX exposure, and regional cyclicality, but they hardly detract from what remains an otherwise pristine income thesis.

What more could you ask for?

We re-iterate our “Buy” rating for PRU.

Stay safe out there!

Q2 2024 Earnings Call Transcript")