Aajan

It’s been a while since I last visited COPT Defense Properties (NYSE:CDP) with a ‘Buy’ rating here back in October, highlighting its defensive property profile, discounted valuation, and long-term growth potential.

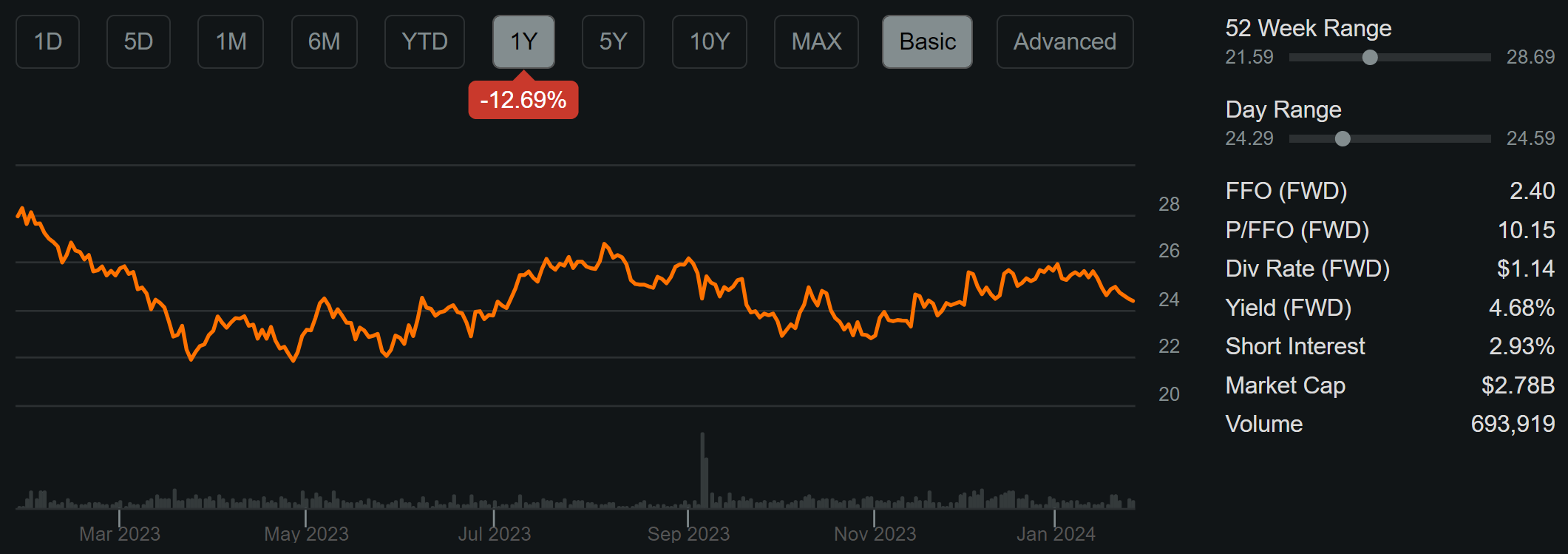

While the stock has seen its ups and downs since then, mostly driven by market speculation around the direction of interest rates, the stock is down from its recent peak in January to land at 1.3% below where I covered it last. Over the past year CDP is down by 13%, as shown below, despite healthy operating fundamentals.

CDP 1-Yr Price Return (Seeking Alpha)

In this article, I provide an update and discuss why CDP continues to offer good value and income opportunity for patient investors focused on the long-run, so let’s get started!

Why CDP?

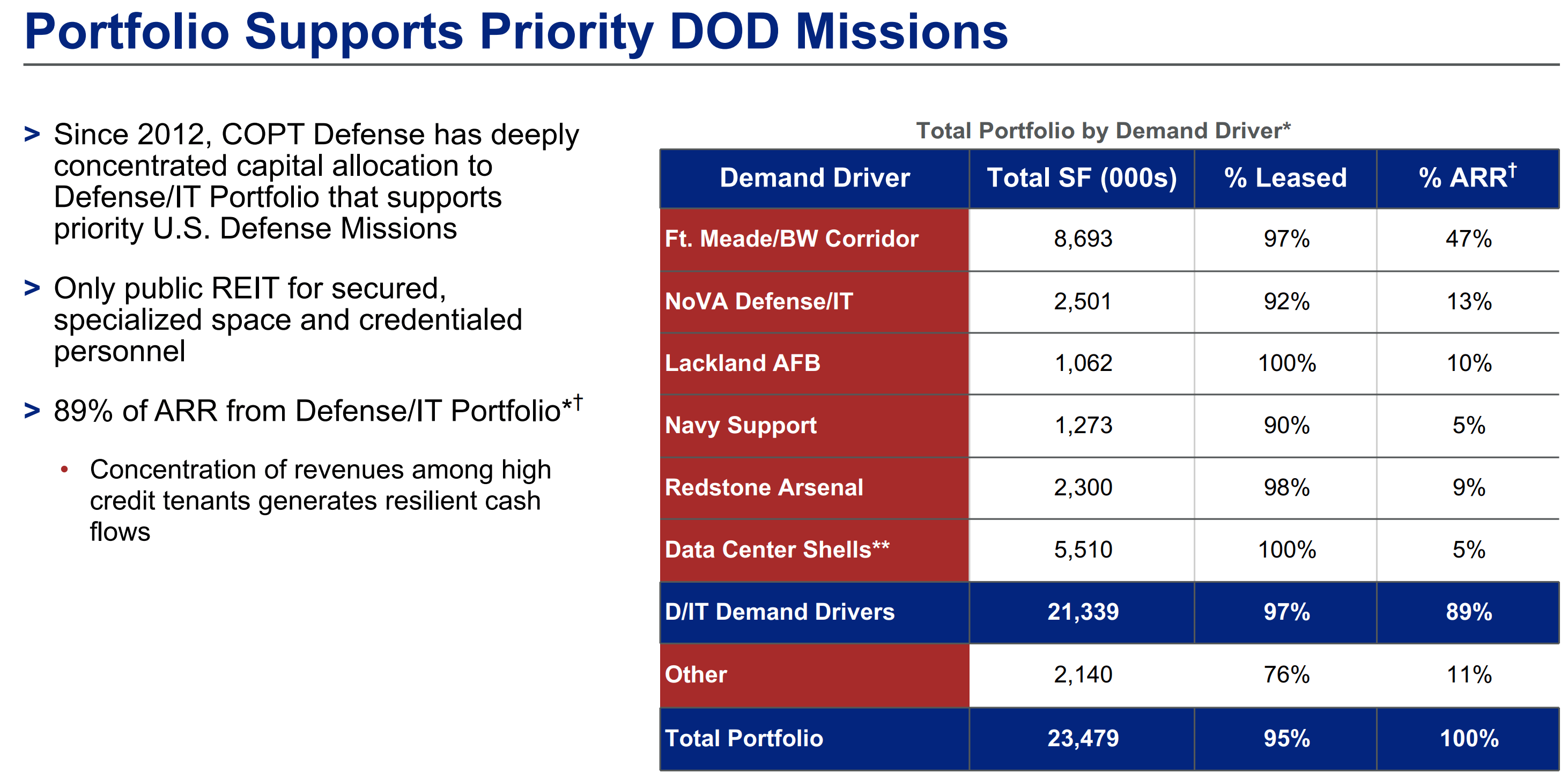

COPT Defense Properties is a member of the S&P MidCap 400 Index, and is a self-managed REIT that’s focused on owning and leasing properties associated with the mission-critical Defense/IT segment. This includes properties related to the U.S. government and its defense contractors, from which CDP derives 89% of its annual recurring rents. At present, COPT’s portfolio consists of 188 properties covering 21.3 million square feet, of which nearly half (47%) of annual rents come from Ft. Meade/Baltimore-Washington Corridor, as shown below.

Investor Presentation

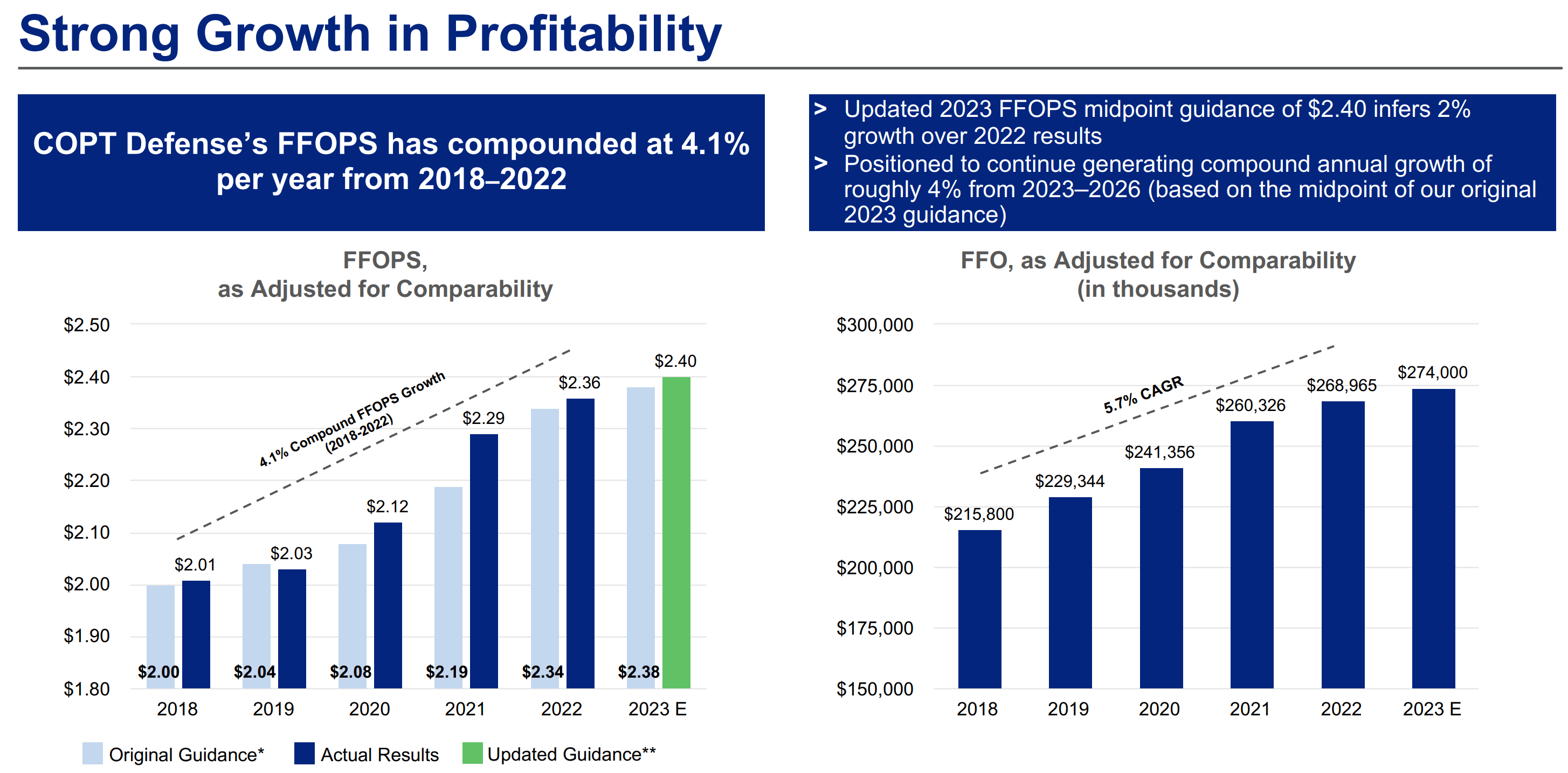

What sets CDP apart from its Office REIT peers is that remote work does not really factor into the equation. That’s because the critical nature of the work performed at its sites makes it simply unrealistic or unsecure for the work to be performed remotely. This has resulted in steady FFO per share growth since 2018 for CDP, at a time when commercial office real estate has seen plenty of upheaval. As shown below, CDP’s FFO/share has risen at a respectable 4.1% CAGR since 2018.

Investor Presentation

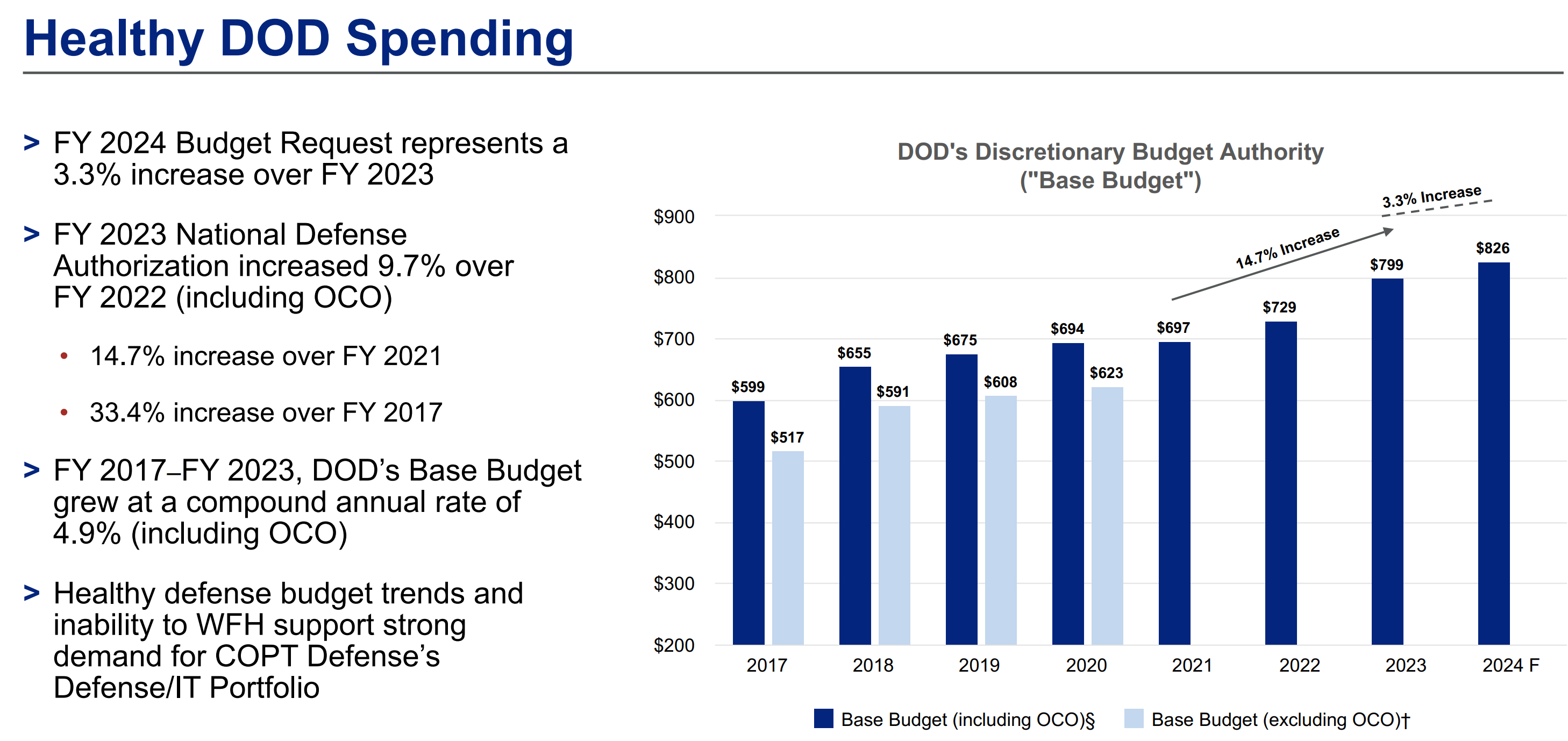

In addition, the steady nature of government contracts and funding for the Department of Defense makes CDP’s tenants less susceptible to economic downturns and corporate downsizing. This is supported by the following chart, which shows that the National Defense budget has risen every year since 2017, and that the FY23 budget rose by 9.7% over FY22. Notably, this timeframe includes executive leadership from both U.S. political branches.

Investor Presentation

While CDP’s share price has largely stagnated since the last time I visited it in October, its operating fundamentals have only strengthened over this timeframe. This is reflected by CDP’s Occupancy improving by 230 basis points from 93.6% in Q2 to 95.9% in Q3, and by the leased rate improving by 200 bps from 95.0% to 97.0% between the two quarters. This includes a 97% leased rate for the Defense/IT portfolio, which is a record high for the company since it began disclosing this segment in 2015, and represents a 70 bps YoY increase.

Also encouraging, CDP continues to see same property cash NOI growth of 4.5% during the third quarter (down from 5.8% growth in Q2) driven by strong leasing volume and high tenant retention. This is reflected by tenant retention of 83% in the first nine months of 2023 (82% in Q3), putting CDP on track to achieve its annual goal of 80% to 85%.

Looking ahead to Q4 results sand beyond, CDP has avenues for external growth, as it has 1 million of active developments underway. This could be a material growth driver for CDP, as it represents 4.7% of CDP’s current portfolio base. This includes six projects located in Maryland, Northern Virginia, and Alabama, that are already 90% leased, signaling positive demand drivers that are solidly in place. Three of these projects have been placed into service in the fourth quarter, with all 3 being 100% leased. Beyond that, CDP has the potential for another 1.2 million square feet of development potential, giving it a good line of sight into the near to medium term.

Risks to CDP include potential for higher than expected inflation, which could outpace its average annual rent escalations of 2.7% on recently renewed leases. Other risks come from the fact that CDP’s tenant health is highly dependent upon government funding for defense spending. However, that risk may be muted in the near term, as the FY 2024 budget request represents a 3.3% increase from 2023 levels, which seem reasonable considering global conflicts in the Middle East and Ukraine.

Meanwhile, CDP carries a strong balance sheet with no variable debt exposure and $200 million of cash on hand along with 85% available capacity on its revolving credit lines. It also has a reasonable net debt to EBITDA ratio of 6.0x, which is at the level at which ratings agencies consider to be safe for REITs, thereby supporting its BBB- investment grade credit rating. As shown below, CDP has no significant debt maturities until 2026, thereby making it less susceptible to the current higher interest rate environment.

Importantly for income investors, CDP currently yields 4.7% and the dividend is well-covered by a 47% payout ratio. It’s worth noting that CDP has demonstrated its ability to raise dividend last year with a 3.6% increase after keeping the dividend flat since 2012 as it deleveraged the balance sheet.

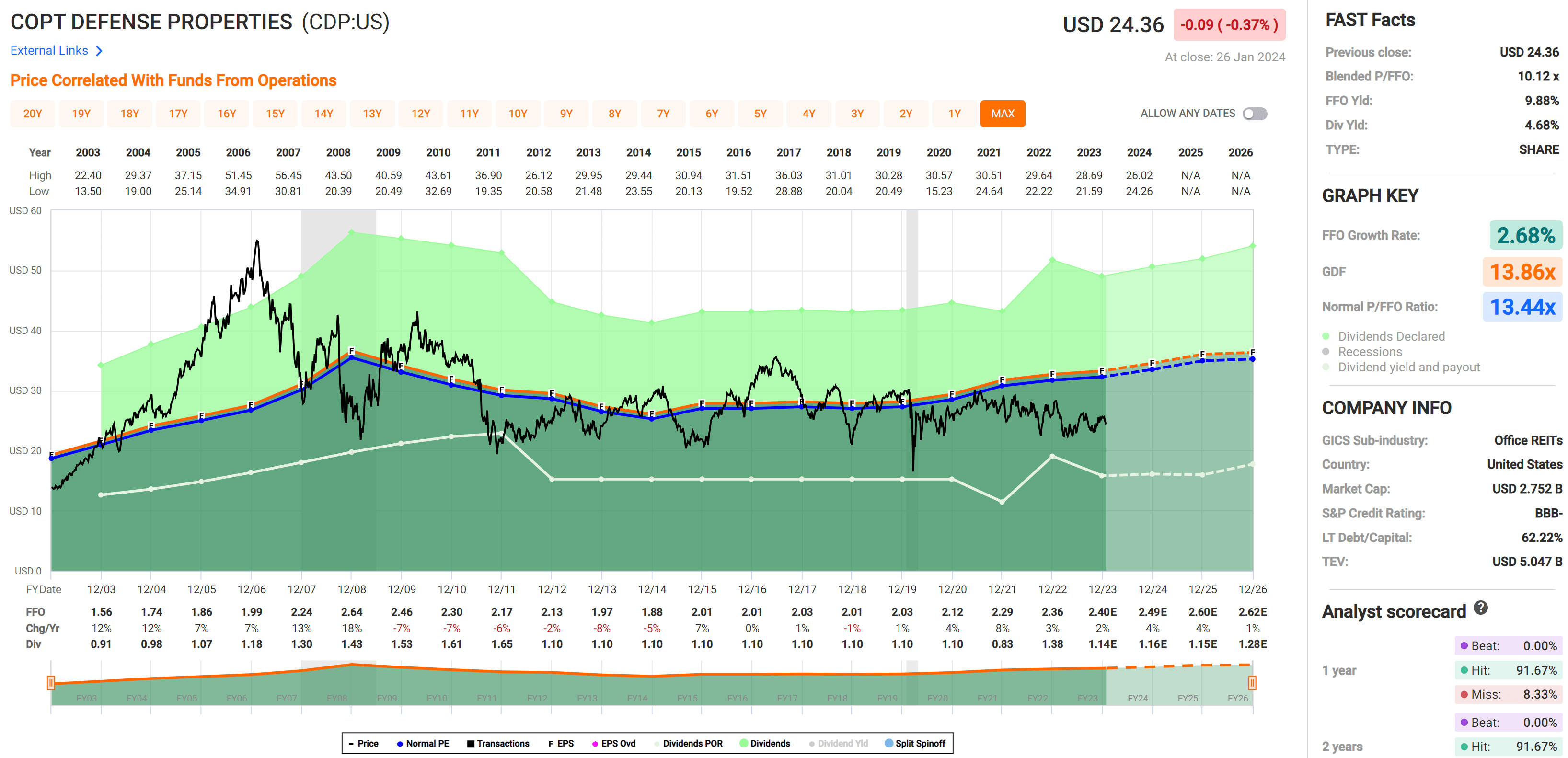

Lastly, I see value in CDP at the current price of $24.36 with a forward P/FFO of just 10.2, sitting below its normal P/FFO of 13.4. At the current valuation, the market is pricing in plenty of uncertainty, which I don’t believe is reasonable for CDP’s certainty around its durable government-related tenants. Analysts project 4% annual FFO/share growth over the next 2 years, which I believe is reasonable estimate considering the 2.7% annual rent escalators and development pipeline that should add value. As such, CDP could produce market-beating returns with a 4.7% yield, a 4% annual FFO/share growth rate, and a conservative 2% per year reversion to mean valuation.

FAST Graphs

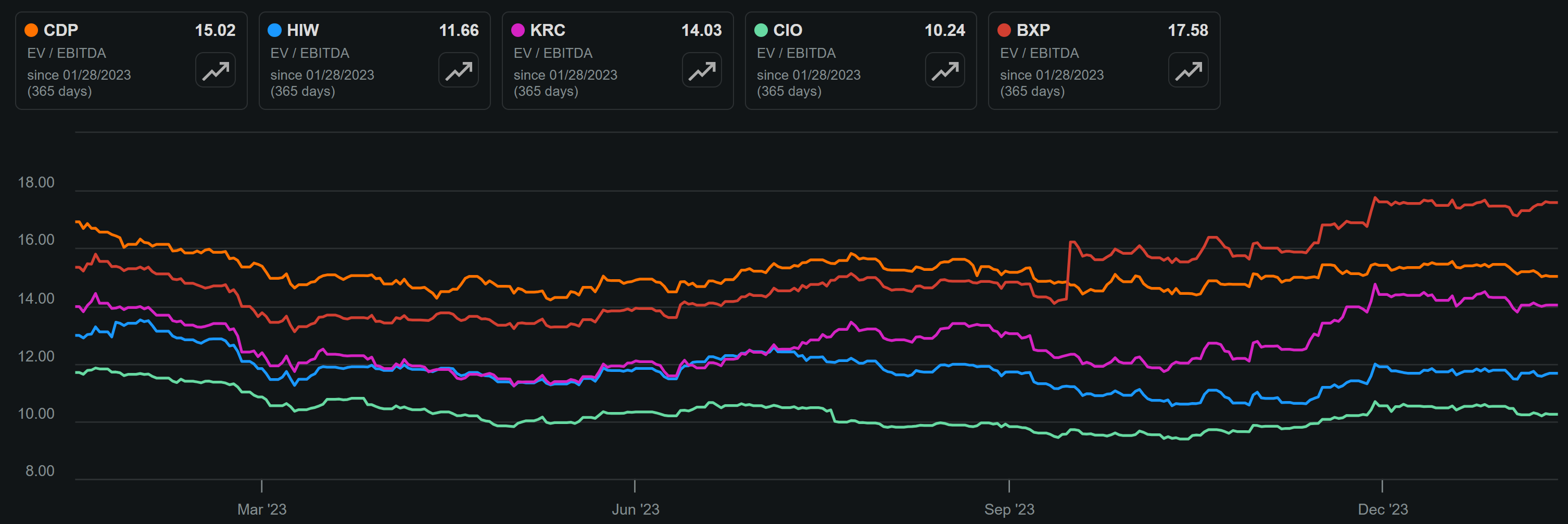

Compared to Office REIT peers, CDP has a ‘middle of the road’ valuation. For this exercise, I use EV/EBITDA, since Enterprise Value includes both the value of equity and debt, resulting in a normalized and fair comparison compared to using P/FFO, which measures only equity value.

As shown below, CDP carries an EV/EBITDA, which is cheaper than that of Boston Properties (BXP), but more expensive compared to Kilroy Realty (KRC), Highwoods Properties (HIW) and City Office REIT (CIO). While I do see value in CDP’s cheaper Office REIT peers, I believe CDP remains a solid choice for those seeking a comparatively safer property profile along with better dividend growth potential in the near term.

CDP vs. Peers EV/EBITDA (Seeking Alpha)

Investor Takeaway

CDP has a strong portfolio of government-leased office properties with stable cash flow, a reasonably leveraged balance sheet, and solid dividend growth potential. Its focus on the defense sector provides stability in its tenant base, while its development pipeline could drive future growth. Plus, CDP offers an attractive current yield and potential for above-market returns due in part to its undervaluation. As such, CDP may be a worthy addition to a diversified income portfolio for its quality attributes. For the above reasons, my thesis around CDP remains unchanged since the last time and I maintain a ‘Buy’ rating.

Q2 2024 Earnings Call Transcript")