JHVEPhoto

After a stellar last year, which saw online travel bookings provider Booking Holdings’s (NASDAQ:BKNG) price rise by 76%, January 2024 has been underwhelming for it with the stock remaining essentially flat. But in comparison, the S&P 500 Consumer Discretionary index has declined by 2.85% during this time even as the S&P 500 (SP500) index has seen a small uptick of 2.5%.

This appears small, but it can be a sign of things to come in a year when the US economy in particular is expected to experience a slowdown, after deftly skirting one last year with 2.5% growth. This is more likely to impact consumer cyclical companies, including Booking Holdings. But the macros aren’t entirely stacked against it, as inflation still has some room to come off and interest rates are expected to soften this year too.

Impact of US travel demand slowdown

First, let’s look at the slowdown’s potential impact on sales. The fate of the US economy is particularly important this year considering that the contribution of travel and tourism to GDP is the biggest across all countries, and is 3.5x the next biggest, China.

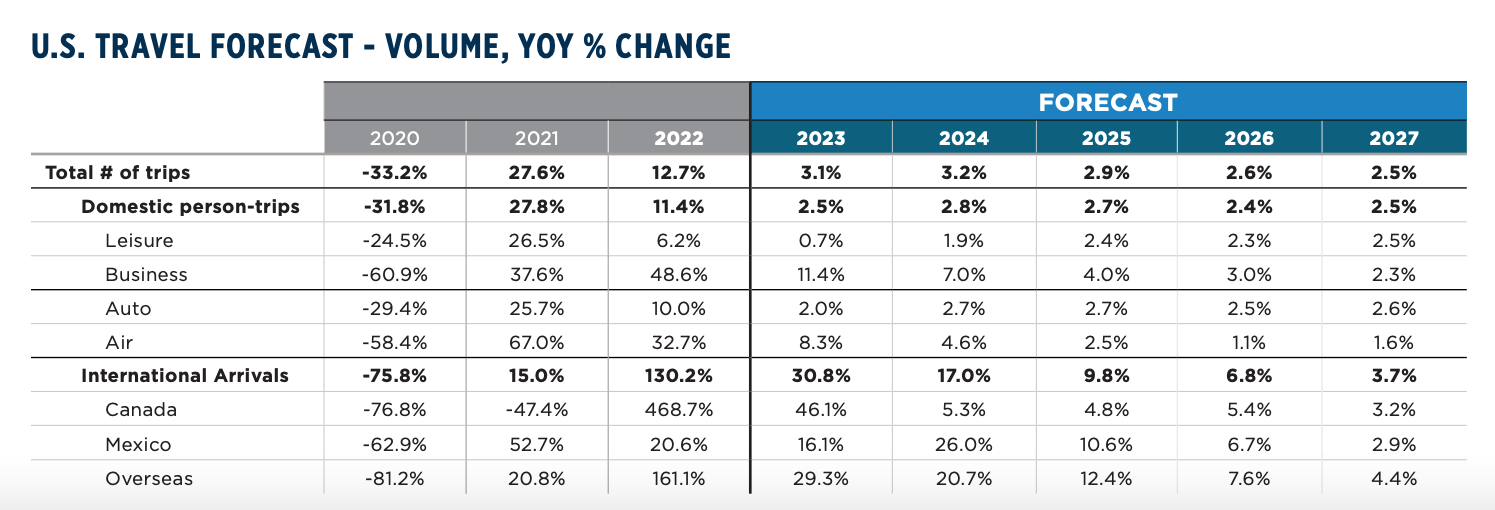

So far the US Travel Association’s US travel demand forecasts aren’t too bad with growth in trip volumes in 2024 expected to stay the same as last year (see table below), but it does show the continued normalization after an upsurge in post-pandemic travel demand.

Source: US Travel Association

The normalization is already visible in Booking Holdings’s revenue growth. The numbers for the first nine months of 2023 (9m 2023) are up by 27.1% compared to the 63.5% seen for 9m 2022. While growth in 2022 was higher due to a low base effect as the pandemic was very much around in the first half of 2021, it was also due to a genuine spurt in travel demand during the year which is now cooling off.

The most straightforward way to see this is by comparing the absolute annual revenue increase. If revenues for the full year 2023 continue to grow at the same rate as seen in 9m 2023, the absolute increase would be USD 4.6 billion, far lower than the USD 6.1 billion rise seen last year. The numbers are expected to slow down even further this year, in both absolute and growth terms to USD 2.3 billion and 10.6% respectively. The key point here is that the demand growth slowdown is real, and I believe it will become more visible in 2024.

Slowing inflation bumps up margins

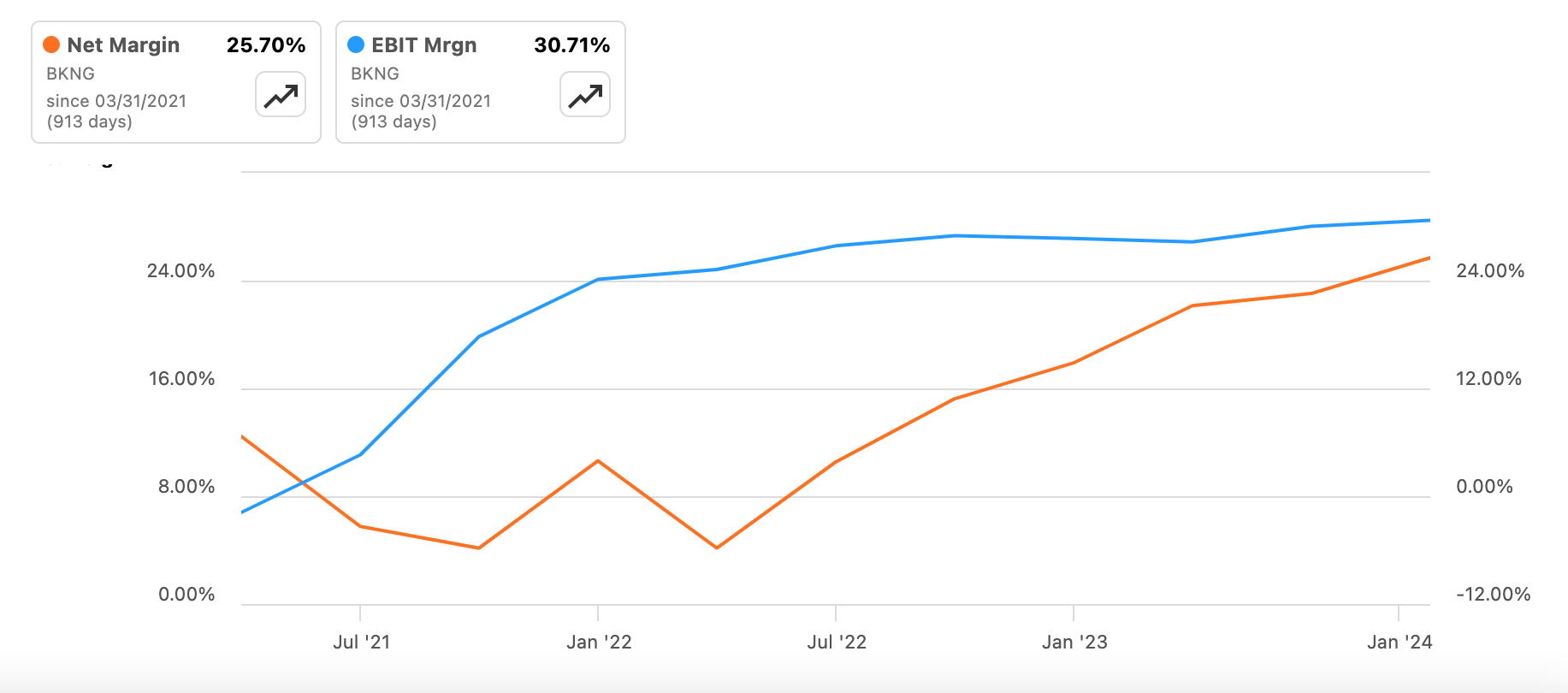

However, the macroeconomy isn’t entirely at odds with the company’s financial prospects. While growth might be set to soften, the cooling off in inflation is good for margins. The ratio of operating expenses to revenues has already declined to 68.5% for 9m 2023 (9m 2022: 71.2%). Conversely, this shows up in the increase in operating income margin to 31.5% for 9m 2023 (9m 2022: 28.8%).

Operating and Net Income Margins, 3y (Source: Seeking Alpha)

But the highlight of the numbers is the continued three-digit growth of 123% in net income (2022: 233.3%), resulting in a margin of 24.5% (2022: 14%). If revenues grow at the same rate as in 9m 2023 for the full year and the net margin remains constant too, net income growth would however slow down to 74.3% during the year, even though the number remains quite strong.

Interestingly, the increase in net income seen so far and expected is despite a huge 180% increase in interest expenses for 9m 2023. The interest coverage ratio while still strong at 7.6x, halved from the 15.3x it was at for 9m 2022. In other words, there’s a possibility of margins gaining further ground as interest rates subside. To me, this suggests that as the year rolls on, the EPS growth forecast for 2024 of 17.6% may well be revised upwards.

What the market multiples say

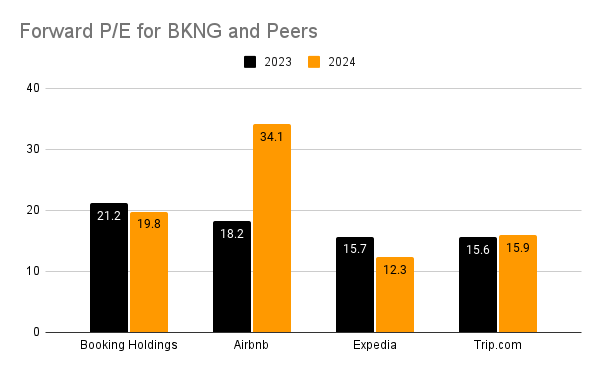

BKNG’s market multiples also work more in its favor than not. My estimates for 2023 show that the stock’s forward GAAP price-to-earnings (P/E) ratio is at 21.2x. This is actually lower than the 24.8x for the TTM GAAP ratio.

Next, I compared the stock with its peers that have a market capitalization of over USD 1 billion, leaving out India’s MakeMyTrip (MMYT) whose figures are outliers compared to the rest of the set. In this case, the stock does appear to be slightly overvalued (see chart below) when considering the 2023 figures. Even for 2024, it trades slightly higher than peers except Airbnb (ABNB).

There’s a reason for the premium, though. Over the past three years, its CAGR for revenues at 32.4% is second only to Airbnb at 38.4%. And it’s the only one to consistently post profits over this time. Of course, the numbers are muddled over this period because of the pandemic, but even then, there’s something to say if Booking Holdings still came out ahead. In any case, the average of peers’ forward P/E for 2024 is at 20.8x, which is slightly higher than that for BKNG at 19.8x.

Source: Seeking Alpha, Author’s Estimates

What next?

In light of the company’s performance over time, I’d compare its market multiples with its own past levels. And as far as those go, the stock looks good, indicating around 25% upside to the stock. Moreover, its financial performance over the past few years imparts confidence in the stock at a time when the US is forecast to see a slowdown, which can impact its demand. Revenue growth has already cooled off for Booking Holdings and is expected only to decelerate further this year.

But where the macros are unfavorable to the top line, they are working in the favor of margins. The ratio of operating expenses to revenues has already softened, bumping up the operating profit margin. Further, with interest rates expected to start coming off this year, the net margins stand to benefit further as well. I wouldn’t be surprised if the company’s profits turned out better than expected right now. This in turn would make its forward P/E more attractive, which isn’t out of line with the sector average anyway. I’m going with a Buy rating on Booking Holdings.

Q2 2024 Earnings Call Transcript")