Spencer Platt/Getty Images News

Still Assembling The Puzzle

About a year ago, a friend of mine brought CAVA Group, Inc. (NYSE:CAVA) to my attention, as I feverishly delineated my Chipotle (CMG) thesis for my community while it traded around $1250/share. He noted that CAVA was essentially the Mediterranean version of Chipotle and that he preferred CAVA to Chipotle. This, of course, piqued my interest.

At the time, CAVA was still a private company, though it was already capturing the attention and penchants of folks in the eastern portion of the United States, one of whom happened to be my friend.

While I’d never eaten there, I always take the product affinities of my network of friends and family seriously, as I believe these affinities are where we can find some of the best investments.

By mid-2023, CAVA forced open the IPO window (financial idiom) that’d been shut for almost 18 months and went public, raising about $340M in the process (resulting in the company having a giant cash hoard alongside no debt as of today).

As CAVA IPO’d, I immediately began assessing the merits of the business via an analysis of its S-1 (first gov’t mandated filing for companies IPO’ing), alongside a couple visits to the restaurant itself. Luckily, there were a few only about 45 minutes from where I live (with only 300 total locations, it was indeed lucky).

I found that, very interestingly, not only was CAVA’s margin profile virtually identical to that of the margin profile of Chipotle, but also, the format of the restaurant was entirely identical to that of Chipotle, and I reported all of this in my original work on CAVA. You may read that introductory analysis via the link below:

From a margin perspective, specifically, both companies report restaurant level margins of about 25%, meaning that, for instance, 25% of CAVA’s $2.6M in total sales per restaurant is profit.

Cava’s Restaurant Margins, Average Unit Volume, And Same Store Sales Are Virtually Identical To What Chipotle Reported Earlier In Its Lifecycle

CAVA Q3 2023 Earnings Presentation

Among Chipotle’s and CAVA’s peers, such as Sweetgreen (SG), this margin is truly exceptional (about 80% better than SG’s margin!).

But while it was easy to understand CAVA’s unit economics and while they were clearly exceptional, demonstrating that CAVA had Chipotle-like business potential, I was still a bit uneasy about CAVA’s revenue growth cadence.

There were quarters of missing sales data; furthermore, I did not know how the company would perform on its quarterly calls. To this end, we received the first set of missing puzzle pieces via CAVA’s Q2 2023 report, which I analyzed for you a few months ago:

With CAVA’s first quarterly report in mind, I felt that, with my Chipotle expertise, I had sufficient understanding of the CAVA business to begin purchasing shares, and I did so at $30.80/share (and made it a new Top Idea as well within my community) in October.

This decision to buy at $30.80/share was precisely in line with what I told you I would do in Craving CAVA linked just above.

We will discuss exactly what this purchase price meant from a valuation perspective later today. But, before we do that, let’s review CAVA’s most recent quarter whereby we will further lay the foundation for valuing CAVA.

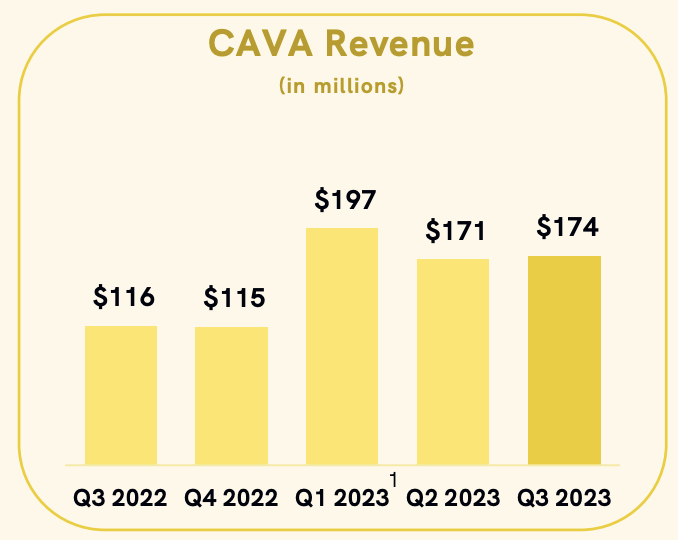

Adding Another Puzzle Piece: Q3 2023 Results

On CAVA’s most recent earnings call, it announced that it had completed all of its Zoes Kitchen conversions, so the sales growth depicted below is entirely CAVA-generated. We’re now buying pure-play CAVA henceforth.

CAVA Q3 2023 Earnings Presentation

As we saw in the graphic in the introduction, CAVA grew at 49.5% year-over-year in Q3 2023 to $174M in total sales, and the above chart reflects as much.

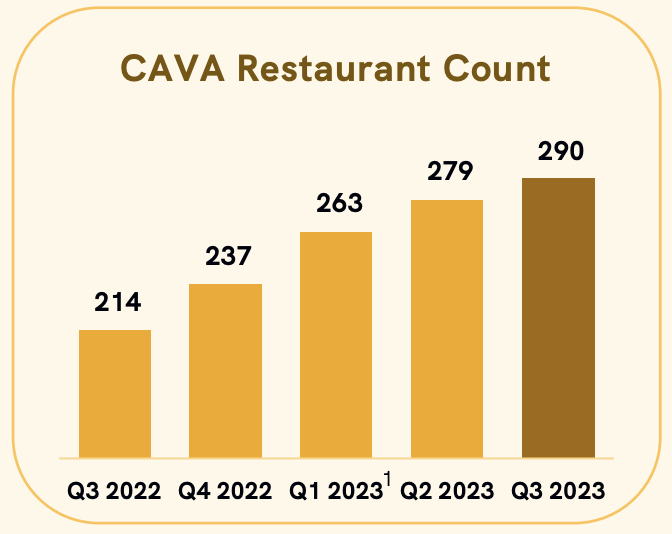

Cava’s growth was driven by a combination of growing locations, depicted below, and revenue growth of existing locations (communicated via a metric called Same Store Sales growth, a Net Retention Rate, so to speak, of the restaurant world).

CAVA Grew Restaurant Count To 290 In Q3 2023

CAVA Q3 2023 Earnings Presentation

We opened 11 net new CAVA restaurants during the quarter with continued expansion across Alabama, Arizona, California, Florida, Georgia, the Carolinas and Texas.

In the fourth quarter so far, we’ve opened 12 additional restaurants, putting us on track for 70 to 73 net new CAVA restaurant openings in 2023. With our last Zoes restaurant conversion completed, we are now operating under a single powerful CAVA brand.

Brett Schulman, CEO, Q3 2023 CAVA Earnings Call (emphasis added).

While CAVA’s openings in Q3 2023 were somewhat slow, its Q4 openings appear to be more than on track as the above quote indicated. Interestingly, the market sold the stock off despite this news of accelerating sequential openings. We will discuss CAVA’s somewhat tepid same store sales guide, which caused the sell off (which has since reversed course) in my eyes, in just a moment.

So CAVA will end 2023 with over 300 locations throughout the U.S.

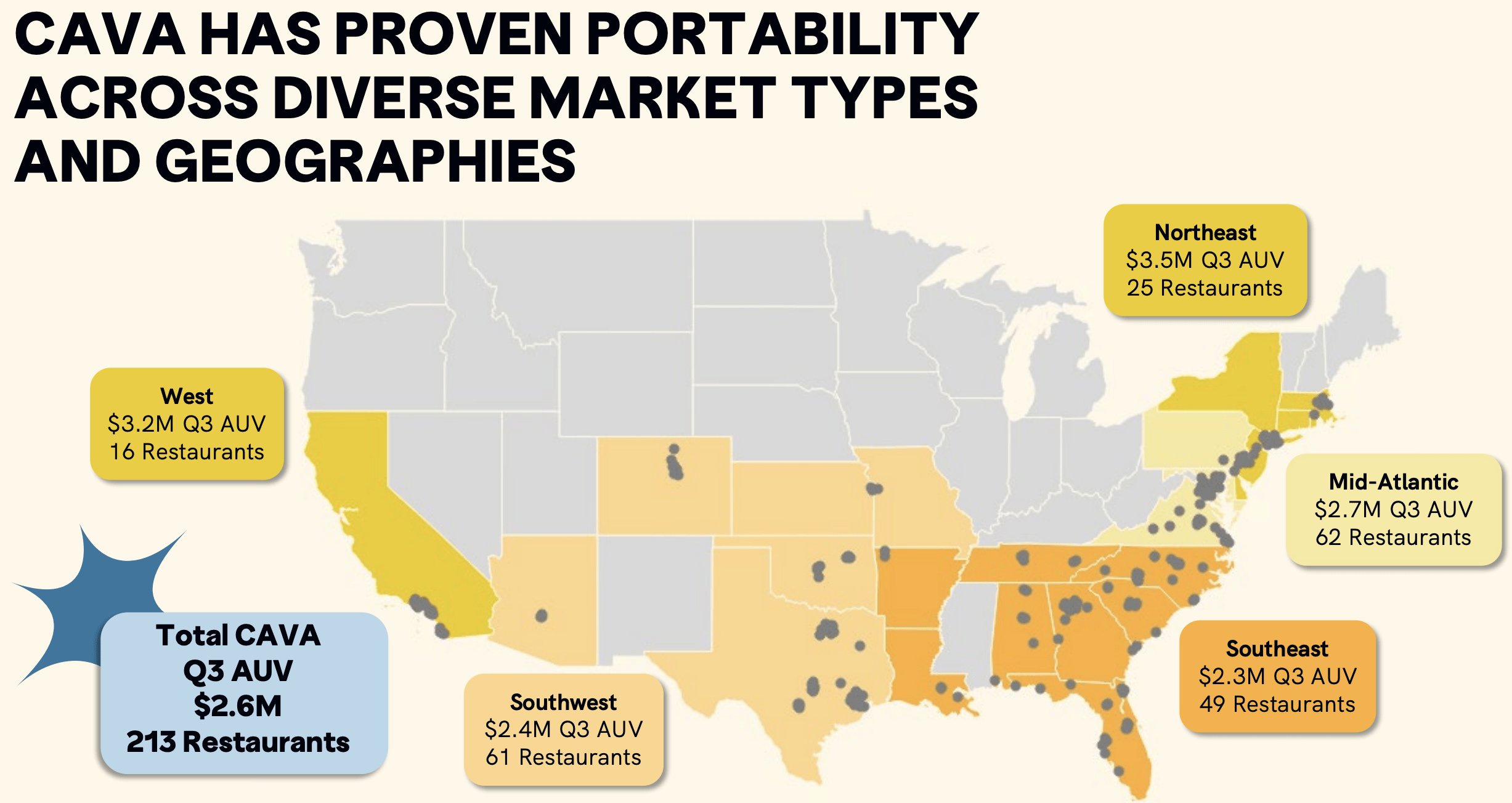

CAVA’s Locations In The U.S.

CAVA Q3 2023 Earnings Presentation

In CAVA’s original public filings with the SEC, the company projected that it would experience 15% 10 year annualized restaurant location growth starting in 2022, bringing it to “over 1,000” locations by 2032.

Based on our internal analysis and third-party research, we believe there is potential to have more than 1,000 CAVA restaurants in the United States by 2032.

CAVA S-1 (emphasis added).

As we share our craveable food and Mediterranean hospitality across the country, we continue to expect annual unit count growth of at least 15%. We’re excited to enter Chicago in 2024 with at least 3 new restaurant openings expected in that market. Like others in the sector, we are seeing changes in real estate market.

Brett Schulman, CEO, Q3 2023 CAVA Earnings Call (emphasis added).

Notably, we’re now in 2024, which means that our modeling, based on 10 years out, has shifted fairly substantially. Instead of projecting a base case of 1k locations by year 10, we will be projecting something more like 1,000 locations * 1.10^2, or about 1,200, as a base case.

I believe 1,300 by 2034 is more than achievable, and I also believe AUVs will reach $3.5M by that time via same store sales growth + natural rate of inflation for CAVA’s offering (which they state is 2.5% to 3% per year).

While expansion can be difficult, CAVA would have to work very hard, in my eyes, to not achieve that level of scale by 2032, as the concept is so incredibly desirable and unique (and, as such, will have an easy time siphoning market share from legacy fast food, among other food concepts).

That is, I believe CAVA has something extremely special in its premium Mediterranean offering, and the specialness of this offering has afforded it fantastic restaurant level margins which will, over the long run, ultimately flow to the bottom line (in the case of Chipotle, to the tune of ~15% free cash flow margins, if not higher in the years ahead).

Below, we can see the profits that CAVA generates from each of its locations on average.

CAVA’s Restaurant Level Profit Margins

CAVA Q3 2023 Earnings Presentation

CAVA restaurant-level profit in the third quarter was $43.6 million or 25.1% of revenue versus $25.2 million or 21.7% of revenue in the prior year, representing a 72.8% increase. The margin expansion was largely a result of improved food, beverage and packaging costs and sales leverage on labor and occupancy.

Tricia Tolivar, CFO, Q3 2023 CAVA Earnings Call.

As I’ve mentioned, this metric is what separates CAVA from other food concepts out there, such as Sweetgreen and what puts it in Chipotle’s league.

When Chipotle was of similar maturity to CAVA today, Chipotle generated low 20% restaurant level margins, just as CAVA does today roughly. As it has matured, it has come to generate 27%+ restaurant level margins, and, based on CAVA’s ability to generate 25%+ margins today, I believe CAVA could certainly achieve Chipotle’s restaurant level margins over the long run as well.

Q3 results continue to demonstrate the power of our model and the value we are capable of delivering over the long term. Having said that, and as reflected in our guidance, the restaurant-level margins delivered in Q3 should not be considered CAVA’s new normal given the continued wage investments in Q3 and Q4.

Tricia Tolivar, CFO, Q3 2023 CAVA Earnings Call (emphasis added).

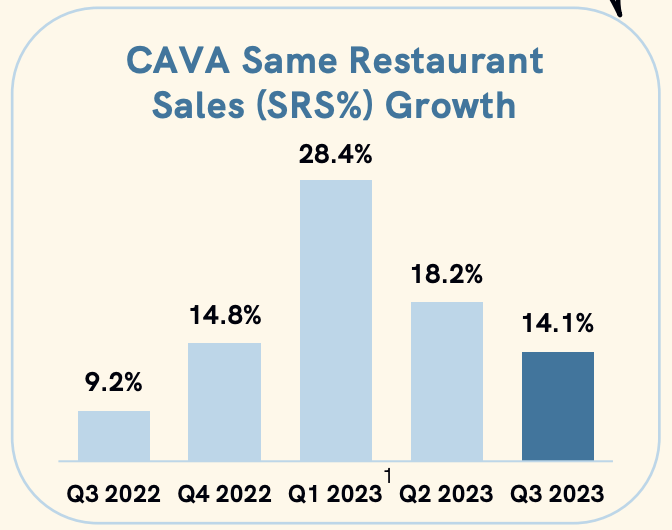

In addition to Chipotle-like restaurant level margins, which poise CAVA to create substantial shareholder value over time, CAVA also has differentiated same store sales growth relative to its fast food peers.

CAVA’s Same Restaurant Sales Growth

CAVA Q3 2023 Earnings Presentation

Again, these are Chipotle-like growth metrics. They are truly exceptional!

But while they’ve been exceptional, curiously management has talked down the rate at which they will grow in the quarters ahead consistently since IPO’ing.

Andrew Barish: Yes. Hey, guys, great results. Just wanted to clarify, I’m doing the math, right, on what you’ve reported year-to-date. It implies the fourth quarter same-store sales are kind of flattish to slightly positive. Am I missing something there? Or can you clarify a little bit on sort of how that rolls up to the 15% to 16% for the year?

Tricia Tolivar: Yes. Hey, Andy, it’s Tricia. Good to hear from you. So the implied guidance is a little positive, up to about 4.7% or so. And what that reflects is the strong comp in the fourth quarter of the prior year at 15% and taking, to a lesser extent, into play the macroeconomic environment and the impact that it may have on the consumer.

Q3 2023 CAVA Earnings Call (emphasis added).

Considering how much I love the concept myself and considering how busy all of the locations are that I’ve visited (I’ve been to three different locations at this point), I find low to mid single digits same store sales growth to be vastly too conservative.

I think Ms. Tolivar is trying to develop a track record of under-promising and over-delivering, which is great, but I just see this guidance as vastly too conservative.

If I, Mr. “Visionary Investing,” am just now becoming acquainted with the concept, which has been around for a 17 years now, then it’s likely that there’s still decades of more and more folks becoming acquainted with it, which will drive elevated same store sales.

Folks are still discovering Chipotle even today. They are still trying it for the first time, 30 years after its founding. The same will be the case for CAVA in the decades ahead.

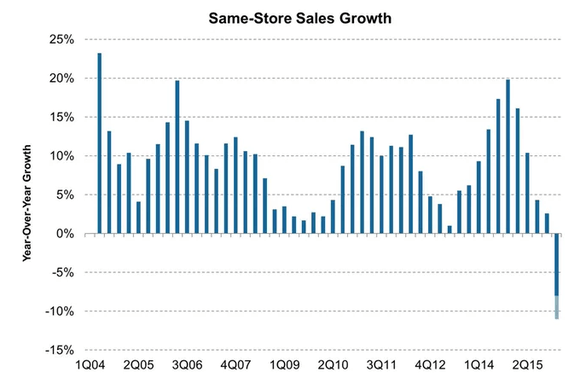

As evidenced for this, we can see below that Chipotle experienced, consistently, 5%-20% same store sales growth consistently during the first decade it was public (the big decline at the far right is the ecolapocalypse, which allowed me/my community to generate such huge returns in Chipotle over the last half decade or so).

Chipotle’s Same Store Sales Growth 2004 to 2015

Fox Business

That said, I mean… the macro is brutal, and, unlike Chipotle, which arguably offers the best value on a $/calorie basis in the fast food market (~$9-$10 can feed a person for 24 hours in most of its markets), CAVA is a bit more of a premium offering, so perhaps they’re seeing headwinds associated with inflation and higher rates, which is creating a near term dip in same store sales growth, though we can’t be sure.

In short, however, I believe CAVA will generate not just Chipotle-like restaurant level margins, but also Chipotle-like same store sales growth, outstripping the arguably too conservative guidance which Ms. Tolivar has laid out, and which is being baked into analysts’ consensus estimates, likely causing the selloff in late 2023.

So we tend to look at things on a 2-year stack. And so when we had a 28% comp in the first quarter of last year, there was a benefit of about 10 points related to weather and Omicron, and that is going to make Q1 of 2024 a bit challenging for us. So I wouldn’t expect significant positive comps as we go into Q1. But certainly, our long-term approach and thinking about low to mid-single digits on a same-restaurant sales basis annually seems to make sense to us.

Tricia Tolivar, CFO, Q3 2023 CAVA Earnings Call (emphasis added).

It frankly makes no sense to me. There’s just so much more room for the company’s brand awareness to expand via which same store sales will grow rapidly.

Her guidance is akin to what a very mature 20th century fast food restaurant experiences.

But, again, it’s probably for the best that CAVA develops a track record of under-promising and over-delivering.

For comparison, here was Chipotle’s guidance for same store sales growth, and note that Chipotle is a vastly more mature company (13 years older), with 10x CAVA’s location count (3k+ vs 300).

Restaurant level margin was 26.3%, an increase of 100 basis points year-over-year. Adjusted diluted EPS was $11.36, representing 19% growth over last year and we opened 62 new restaurants, including 54 Chipotlanes. Trends remain strong in October and we anticipate comps in the mid to high single digit range for the fourth quarter, which includes our recent pricing action.

Chipotle Q3 2023 Earnings Call (emphasis added).

For those who’d like more management commentary on this controversial subject, here’s an exchange that I found insightful apropos of same store sales (a.k.a., “comps”).

Jon Tower: Just a couple of clarifications and then a question. First, on the comments about the fourth quarter guidance, the implied comp. Are you seeing a slowdown of that magnitude quarter-to-date?

[Even Jon is scratching his head here!]

Tricia Tolivar: Well, as we’ve stated prior, we are not going to give inter-quarter or intra-quarter guidance as it relates to same-restaurant sales. And I’ll just reinforce what we said earlier, we had a very strong Q4 of 2022 at a 15% comp. And so factoring that in, as well as the uncertainty in the macroeconomic environment, we feel comfortable with the guidance that we’ve outlined today.

Q3 2023 CAVA Earnings Call (emphasis added).

Expanding Its Presence

With my Field Research channel, I’ve shared instances of social media brand distribution for various companies I own, namely Chipotle.

For instance, on Instagram of Meta Platforms (META) and YouTube Shorts of Google (GOOGL), I often see organic references to Chipotle, such as “how to get the most from your Chipotle bowl” or “check out this interesting Chipotle meal design I created” or “Have you tried Chipotle’s new quesadilla?” Talking about it makes me want to go to Chipotle for the 4th time this week!

CAVA has a likewise “social media-oriented” brand, and I expect the company to become a viral sensation, akin to Chipotle, over time.

- If you’re an owner of the company, I’d encourage you to give their X profile a follow.

- They also have 189k followers on Instagram, and they have presences on other platforms as well.

Example of CAVA’s Social Media Presence Which Creates Free/Viral Marketing For The Company Which Creates Brand Awareness

X

As CAVA expands its footprint, its social media followings and the “earned media” therefrom will expand as well.

CAVA Q3 2023 Earnings Presentation

I eagerly await the day that CAVA opens locations in St. Augustine, FL!

We also need a couple more Chipotles, as an aside.

With all of these ideas as our platform, we can now value the business with confidence.

Valuation

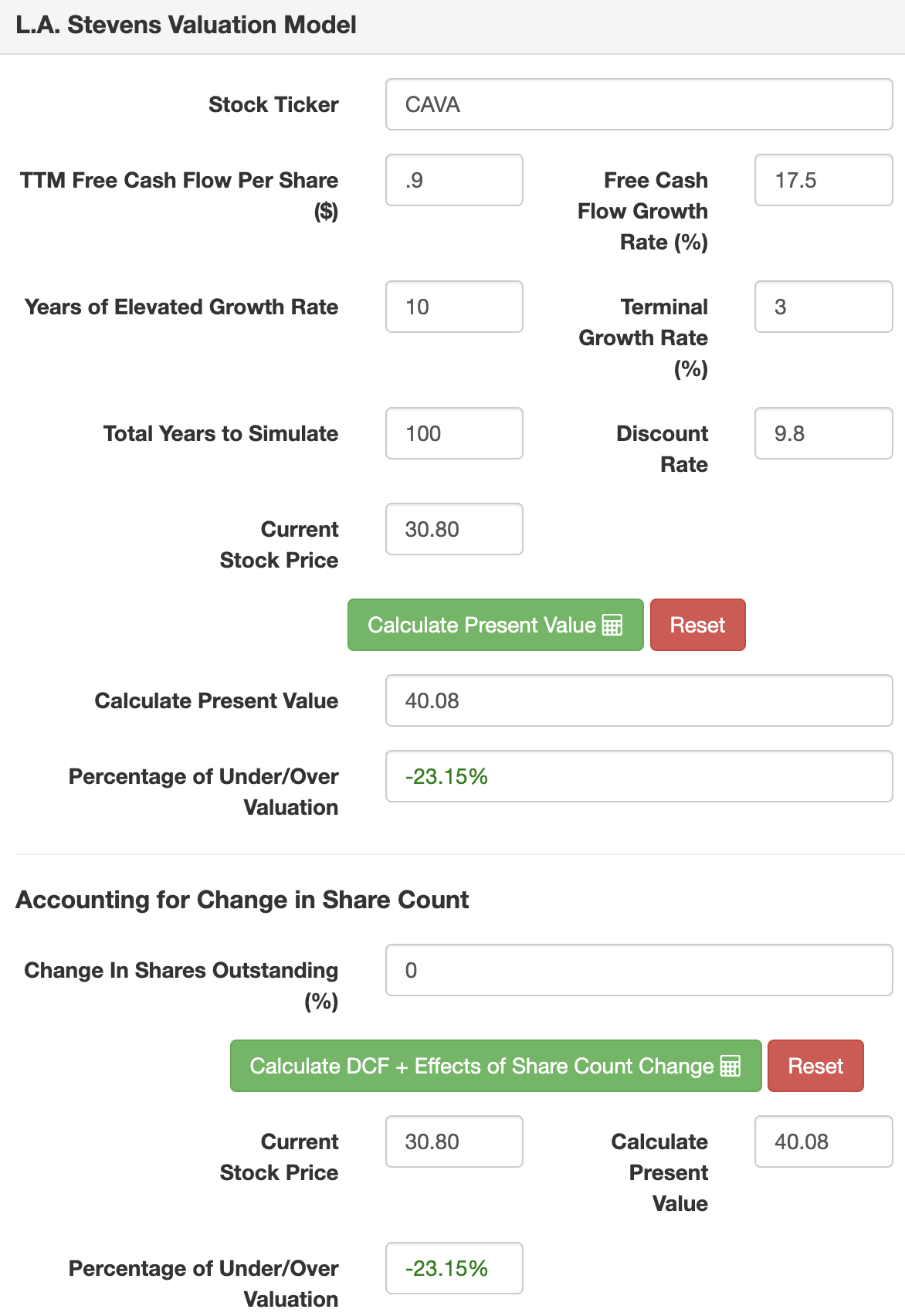

Based on the data shared today, here are my valuation assumptions:

Assumptions:

|

TTM Sales [A] |

$720 million |

|

Potential Free Cash Flow Margin [B] |

15% |

|

Total diluted shares outstanding [C] |

120 million |

|

Free cash flow per share [ D = (A * B) / C ] |

$.9 |

|

Free cash flow per share growth rate (conservative) |

17.5% |

|

Terminal growth rate |

3% |

|

Years of elevated growth |

10 |

|

Total years to stimulate |

100 |

|

Discount Rate (Our “Next Best Alternative”) |

9.8% |

Notably, my 15% free cash flow margin is influenced by the economic performance and margins of Chipotle, i.e., its 27%+ restaurant level margins, ~20% operating margins, and recently achieved ~15% free cash flow margins.

And here are the results (note that I inserted CAVA’s share price at $30.80/share, where I plan to continue buying at some point in the future):

L.A. Stevens Valuation Model L.A. Stevens Valuation Model

Considering CAVA will still have ample runway for growth both domestically and internationally by 2034, I do not think that 30x price to free cash flow is expensive at all. It represents a 3.33% free cash flow (“FCF”) yield, for a company that could be growing ~15% even by 2034.

With share buy backs, free cash flow per share growth could be even higher.

I will say that CAVA is not the most asymmetric bet in our coverage universe presently. I think I used conservative to accurate assumptions, as opposed to very conservative assumptions.

Further, CAVA is young.

There are people building it who are imperfect, so things could go wrong.

I think CAVA would become extremely asymmetric at $20/share, such that I would increase the weighting well above 1-2%, where I’ve been recommending it recently.

Concluding Thoughts

Shifting to liquidity. At the end of the quarter, we had 0 debt outstanding, $340.4 million in cash on hand and access to a $75 million undrawn revolver, with an option to increase our liquidity if needed. We delivered cash flow from operations of $73.1 million for the current year-to-date period compared with $5.2 million in the prior year period. The increase was primarily driven by our improved operations, driving increased profitability across the fleet.

Tricia Tolivar, CFO, Q3 2023 CAVA earnings call.

While things could go wrong at various points in the years ahead for CAVA, it is more than prepared financially.

Its $340M in cash, alongside no debt, is a true war chest with which the company could withstand anything the macroeconomic environment threw at it.

Like all of our companies, the macro may try to derail us, but it simply cannot break us. We have way, way, way too much cash on our balance sheets. “Gargantuan cash hoards,” as it were.

And CAVA is no different.

In short, especially for the CAVA fanatics out there, I believe accumulating shares routinely in the low $30s/share and in the years ahead makes a lot of sense. I see buying CAVA as something akin to buying Tesla (TSLA) or Apple (AAPL): it offers a “rave-worthy” product, and I want to be a part of the growth thereof.

Thank you for reading, and have a great day.

Q2 2024 Earnings Call Transcript")