Mat Hayward

Executive Summary

I initiate coverage on Endeavor Group Holdings Inc. (NYSE:EDR) as a Buy with a target price of $28.50, as it presents a strong investment opportunity in the diversified sports and entertainment space. Endeavor’s business model is built on a foundation of owning and managing high-value sports properties, event management, and talent representation. This multi-faceted approach has positioned Endeavor with a diversified stream of high-growth cash flow streams, capitalizing on its strong portfolio that includes the Ultimate Fighting Championship (UFC), Professional Bull Riders (PBR), and significant events like the Miami Open and New York Fashion Week.

My analysis highlights Endeavor’s impressive financial performance, as evidenced in its latest earnings report. The company’s strategic focus on expanding its asset portfolio and integrating new technologies has yielded a notable 10.1% increase in consolidated revenue. This growth trajectory, supported by significant agreements and expansion into new markets, reflects Endeavor’s resilience and adaptability in a dynamic industry.

The industry outlook remains promising, with the entertainment and sports sectors experiencing a digital and experiential transformation. Endeavor’s strategic investments in content creation and event management position it well to leverage these industry trends. However, the analysis also underscores potential risks, including the high revenue and EPS expectations, sensitivity to consumer spending fluctuations, and regulatory challenges that could impact future performance.

Company Overview

Endeavor Group Holdings Inc., headquartered in the United States, is a multifaceted organization in the realm of intellectual property, content, events, and experiences. Established in 1995, Endeavor has evolved into a significant entity in the entertainment and sports sectors, distinguished by its innovative approach to content and event management.

At the helm of Endeavor’s operations is its diverse portfolio of businesses, segmented into three primary categories:

-

Owned Sports Properties: This segment is made up of unique and scarce sports properties, including the Ultimate Fighting Championship (UFC), Professional Bull Riders (PBR), and Euroleague Basketball.

-

Events, Experiences & Rights: Endeavor’s prowess in this segment is evident through its ownership and operation of marquee events like the Miami Open, HSBC Champions, Frieze Art Fair, New York Fashion Week, and Hyde Park Winter Wonderland. These events underscore the company’s capability to create and manage large-scale, high-profile experiences that attract global audiences.

-

Representation: Complementing its event-centric businesses, the Representation segment delivers services to talent and corporate clients, integrating the endeavors of Endeavor Content. This division underlines the company’s expertise in content creation and management, catering to a broad spectrum of client needs in the entertainment industry.

Endeavor’s business model is reflective of its strategic focus on leveraging intellectual properties and relationships across various platforms and formats. This approach not only diversifies revenue streams but also solidifies Endeavor’s position in the competitive landscape of content and event management. The company’s ability to adapt and innovate in the dynamic sectors of sports and entertainment is pivotal to its ongoing success and future growth prospects.

Recent Financial Performance

EDR reported its third quarter 2023 earnings on November 8th, 2023. CEO Ari Emanuel highlighted several key developments during the quarter, including the launch of TKO, which achieved substantial media rights increases, record-breaking global marketing partnerships, and new international events. Endeavor also announced a significant agreement with the NFL to manage its media rights across various markets in Asia and Europe.

Financially, Endeavor generated $1.344 billion in consolidated revenue, marking a 10.1% increase, with a net loss of $116 million for the quarter. This loss was primarily attributed to transaction-related expenses associated with the TKO transaction. The Owned Sports Properties segment, including TKO, saw a revenue increase of 19.3% to $479.7 million, driven by UFC’s higher media rights and content fees, as well as additional Fight Night events compared to the previous year. Endeavor’s Events, Experiences & Rights segment faced a 7% decrease in revenue, partially offset by new contracts and increased media production revenue.

Endeavor’s Representation segment experienced a slight revenue decrease, impacted by strikes and offset by growth in sports and music divisions. The Sports Data & Technology segment saw a substantial increase in revenue, attributed to the acquisition of OpenBet and growth in betting data and streaming at IMG ARENA.

On the operational front, Endeavor’s recent earnings call highlighted the company’s continued focus on strategic investments and acquisitions to strengthen its market position. These strategic moves are designed to not only expand its portfolio but also to integrate new technologies and platforms, enhancing the overall value proposition to clients and stakeholders. The management team’s emphasis on long-term, sustainable growth, as opposed to short-term gains, was evident in their discussion of these initiatives. The company’s ability to navigate the complexities of the global entertainment and sports sectors while maintaining financial discipline has been a key factor in its positive performance trajectory.

Furthermore, the earnings report underscored Endeavor’s robust cash flow position, which is critical for future investments and debt management. In my view, the company’s effective cost management strategies, coupled with a strong cash flow, have positioned it well to pursue growth opportunities while managing its leverage.

Industry Overview

The movie and entertainment industry is poised for significant changes and evolution within the next few years. It’s transitioning from traditional formats and channels towards a more diverse, digital, and, personalized landscape. The rise of streaming platforms, led by giants like Netflix, Amazon Prime, and Disney+, is fundamentally altering how content is distributed and consumed. These platforms have not only expanded access to a vast array of content but have also intensified competition for viewers’ attention. As streaming becomes more prevalent, traditional cable and satellite providers are adapting, often by launching their own digital platforms.

This digital shift is complemented by a significant investment in original content creation. Companies are focusing on developing unique, high-quality content to differentiate themselves in a crowded market, a trend exemplified by Netflix’s and Amazon Prime’s increased budget allocations for original productions. Another notable trend is the increasing importance of international markets. As the industry becomes more global, there’s a growing emphasis on content that resonates across diverse cultural landscapes, especially in high-growth regions like Asia-Pacific.

Furthermore, technological advancements are reshaping the industry’s future. The integration of technologies like virtual reality (VR) and augmented reality (AR) is beginning to offer immersive experiences, potentially opening new revenue streams and ways of storytelling. The industry is also witnessing a surge in e-sports and gaming content, driven by a younger demographic. This shift not only diversifies the industry’s portfolio but also aligns with changing consumer preferences, particularly among millennials and Gen Z.

However, these transformations bring challenges. The battle for market share is leading to increased content production costs, and the saturation of streaming services may lead to consumer subscription fatigue. Moreover, the industry must navigate regulatory landscapes that vary significantly across regions, affecting content distribution and profitability. The ongoing global economic uncertainties, including the impact of COVID-19, also continue to affect consumer spending patterns and advertising revenues, critical income sources for the industry.

Specifically for in-person sporting events the growth of in-person sporting events is dynamic and multifaceted. This transformation is driven by various factors, including technological advancements, changing consumer preferences, and the global economic environment.

First and foremost, the sports industry continues to invest heavily in enhancing the entertainment experience for fans. This investment focuses on turning venues into comprehensive entertainment zones that engage fans before, during, and after games. For instance, major football clubs like Manchester City and Spanish giants Real Madrid and FC Barcelona are transforming their stadiums into year-round entertainment and leisure destinations. This shift indicates a broader trend where the physical experience of attending sports events is being augmented with diverse entertainment offerings to maintain fan engagement and expand revenue streams.

Within the context of sports broadcasting, 2024 marks a significant leap in how sports are viewed and experienced. Innovations in content delivery and the use of cutting-edge technology are reshaping sports broadcasting. For example, in cricket, the evolution involves the integration of esports tournaments and enhanced streaming services, reflecting a broader trend across the sports broadcasting industry.

Regarding the economic impact, the sports event ticket market has been experiencing steady growth. Grand View Research estimated that the global sports event ticket market, valued at $6.45 billion in 2021, is projected to reach $18.7 billion by 2028. This growth trajectory is further supported by the increasing average revenue per user (ARPU) in sports events. For instance, Statista estimates that the ARPU for sports events, which was $67.24 in 2017, will rise to $101.6 by 2027. This increase represents a 51% growth in revenue per user over ten years. Additionally, the number of users attending sports events is anticipated to grow from 300.8 million in 2022 to 317.5 million in 2027.

However, it’s important to note that the sports industry, like many others, is not immune to macroeconomic trends such as inflation. For instance, while the cost of concessions at sports events has seen relatively flat movements, ticket prices have traditionally mirrored inflation rates. The average annual inflation rate for attending sports events between 2000 and 2022 was 2.88%, indicating a more significant increase than the national inflation rate. Despite this, the demand for sports event tickets has continued to grow, albeit moderated by aggressive price hikes and the broader economic context.

Looking ahead, the future of in-person sporting events seems to be marked by a combination of innovative fan experiences, both physical and digital, and a keen sensitivity to the broader economic environment that could shape consumer behavior and spending patterns. The sports industry’s ability to adapt to these changes will be crucial in maintaining and expanding its fan base and revenue streams in the coming years.

Valuation Overview

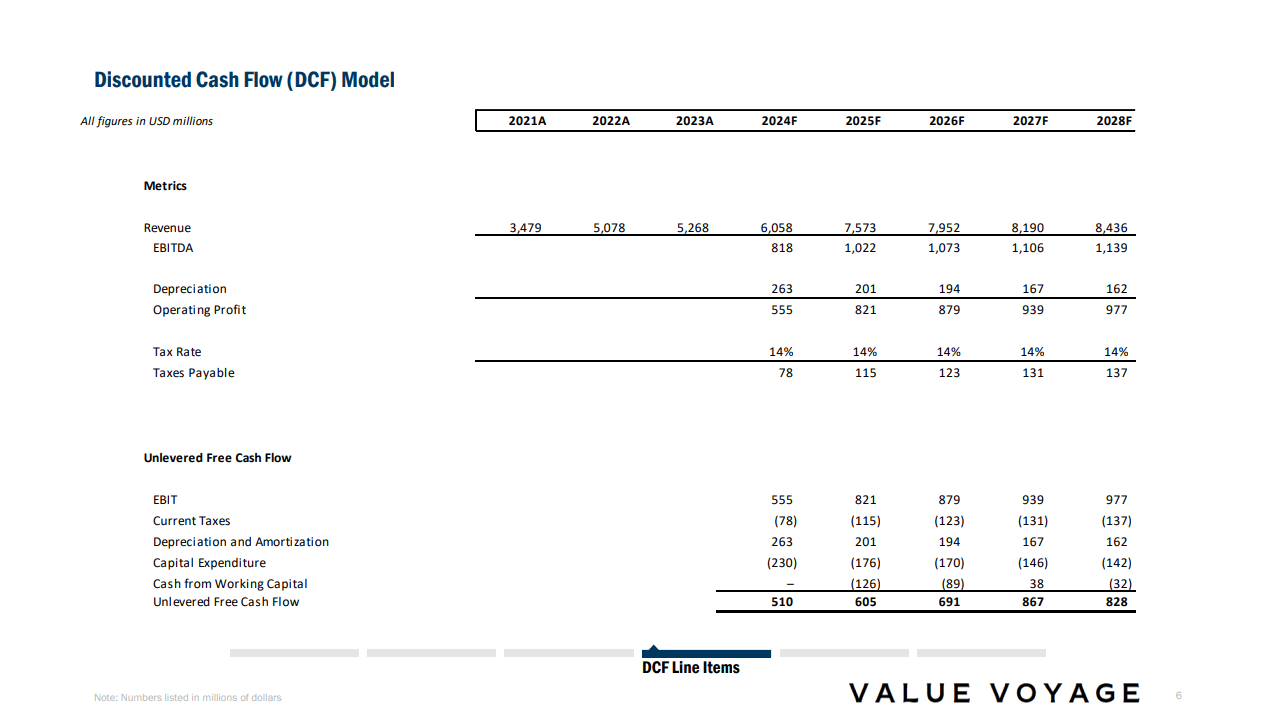

In my analysis, I’ve conducted an intrinsic valuation of EDR using the Discounted Cash Flow (DCF) method. This assessment is based on financial forecasts from 2024 to 2028, underpinned by a blend of current industry trends and future expectations. I’ve applied a Weighted Average Cost of Capital (WACC) of 7% (pulled via FactSet) and a terminal multiple of 10x EBITDA, informed by historical data and comparative company analysis.

I project EDR’s revenues to show a consistent upward trend, starting from $6.058 billion in 2024, and gradually increasing to $8.436 billion by 2028. This anticipated growth reflects EDR’s strategic business initiatives and its solid market positioning:

EDR Discounted Cash Flow Projections (Author’s Calculations)

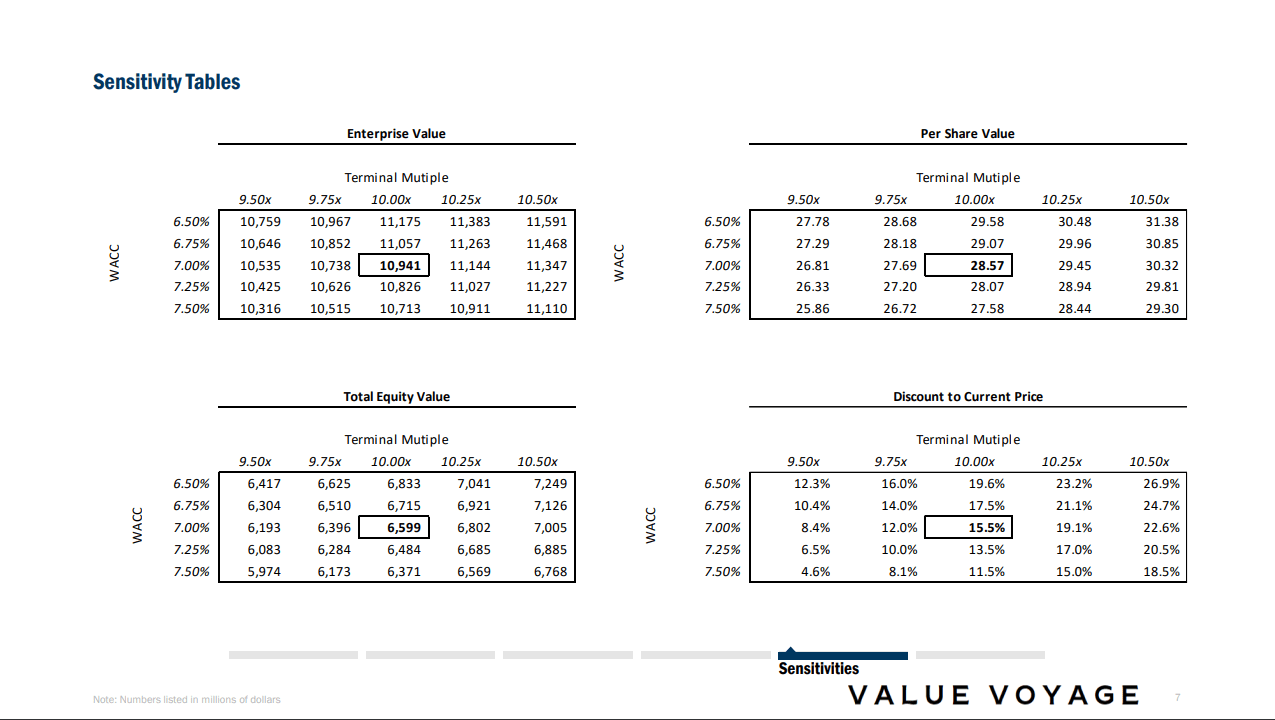

My financial analysis culminates in a per-share valuation of $28.50 for EDR:

EDR Per Share Value Sensitivity Tables (Author’s Calculations)

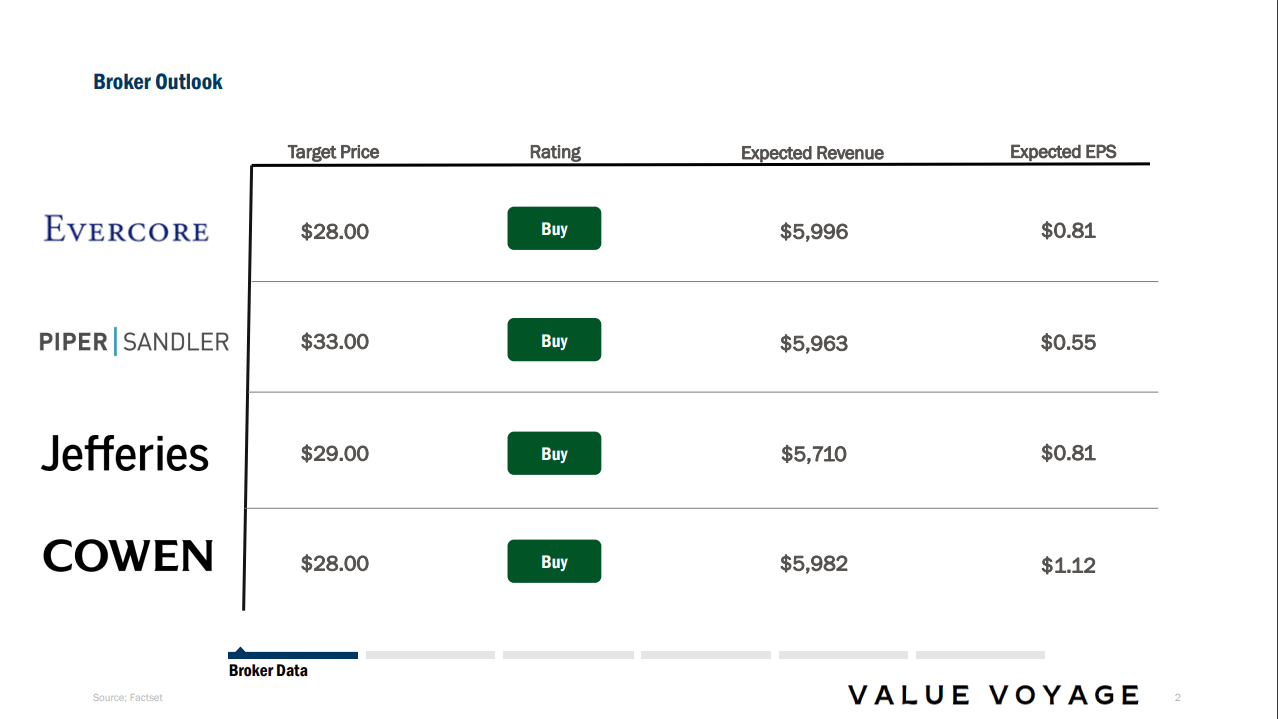

This falls on the lower end of selected broker estimates for EDR:

EDR Broker Estimates (FactSet)

Risk to Thesis

My thesis has three main risks.

First, EDR’s ambitious revenue and EPS expectations set a high bar for performance. The company’s growth strategy hinges on expanding its diverse portfolio of assets, which includes talent management, sports, entertainment, and media properties. While this diversification offers multiple revenue streams, it also necessitates continuous innovation and market leadership to meet aggressive financial targets. The entertainment industry, in particular, is highly competitive and rapidly evolving, with consumer preferences and technological advancements shaping the landscape. Consequently, any failure to adapt to these changes or to successfully manage its diverse holdings could result in revenue and EPS falling short of expectations. This risk is compounded by the company’s reliance on high-profile events and talent, where unforeseen issues such as cancellations, talent disputes, or underperformance can have a significant financial impact.

Second, EDR’s performance is closely tied to consumer spending trends. The company’s portfolio, particularly in live events and entertainment, is susceptible to economic cycles. In periods of economic downturn or reduced consumer confidence, discretionary spending on entertainment and sports events may decline, impacting EDR’s revenue streams. This sensitivity is heightened by the post-pandemic economic landscape, where consumer spending patterns remain uncertain. While there has been a surge in demand for live experiences post-lockdowns, the long-term sustainability of this trend is unclear, especially in the face of potential economic headwinds.

Finally, a third key risk for EDR lies in the realm of regulatory and legal challenges. The company operates in various jurisdictions worldwide, each with its regulatory environment. Changes in regulations, whether related to talent management, media rights, or event hosting, can pose operational and financial challenges. Moreover, the legal landscape governing intellectual property rights, contract negotiations, and talent representation is complex and subject to change. As Endeavor expands its global footprint, compliance with these diverse regulatory and legal frameworks becomes more challenging, potentially leading to increased legal costs and operational complexities.

Conclusion

Initiating coverage with a Buy rating, I believe that Endeavor’s diverse portfolio, strong market position, and strategic focus on growth through innovation and expansion present a compelling investment case. The company’s unique assets and market positioning are the driving factors behind the large expectations moving forward. While acknowledging the risks associated with high-performance expectations, consumer spending trends, and regulatory dynamics, I am confident in Endeavor’s potential to deliver value to shareholders. The company’s strategic maneuvers, including acquisitions and partnerships, fortify its competitive advantage, making EDR an attractive investment within the sports and entertainment space.

Q2 2024 Earnings Call Transcript")