Chinnapong/iStock via Getty Images

Intro

Hims & Hers Health (NYSE:HIMS) is a pioneering player in the telehealth sector that has been making waves in the healthcare industry. Operating in the vast and rapidly expanding telehealth market, we believe HIMS is well-positioned as an early-stage disruptor with a unique approach to providing accessible healthcare solutions. The company generates revenue through its innovative platform, offering a range of telehealth services, including consultations, prescriptions, and personalized wellness products. The stock is currently trading 29% off its 52-week high, and over the past year, it has posted a 16% gain, slightly trailing the S&P 500’s 20% surge during the same period. With a market cap of ~$1.8 billion, we believe HIMS has the potential to be a multi-bagger in the long run, anchored in the company’s robust financial performance and its well-established positioning within its market. We assign HIMS a Buy rating and price target of $14, suggesting 50%+ upside from current share price levels, with room for further expansion over the long run.

Attractive TAM

Given the heightened competition within the already crowded telehealth market, some investors might express reservations about committing to a relatively early-stage business like HIMS. In many ways, we view this hesitancy as understandable, especially with larger and more established players vying for share in the industry. However, though the competitive landscape may be intensifying, we argue that the sheer size and diversity of the TAM suggest that heightened competition doesn’t necessarily pose a significant threat for HIMS. As consumers increasingly prioritize digital health platforms, there appears to be more and more opportunities within the market. HIMS, along with its competitors, can coexist and flourish by tapping into various segments and addressing specific needs within the broader healthcare and wellness space. We firmly believe that there’s ample room for each player to secure their share of the pie, fostering a landscape where competition encourages innovation rather than hindering overall growth.

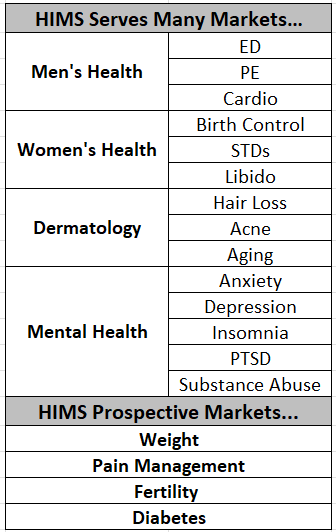

In Figure 1 below, we illustrate the current markets HIMS operates in, spanning men’s health, women’s health, dermatology, and mental health. These sectors alone offer a substantial growth runway; yet, as HIMS consistently broadens its product portfolio, we anticipate even more substantial growth opportunities in the future. As of now, HIMS has noted its strategic intent to venture into the weight management, pain management, fertility, and diabetes markets going forward, further adding to its growth story.

Figure 1 (Loft Capital Mgmt., HIMS 3Q23 Investor Presentation)

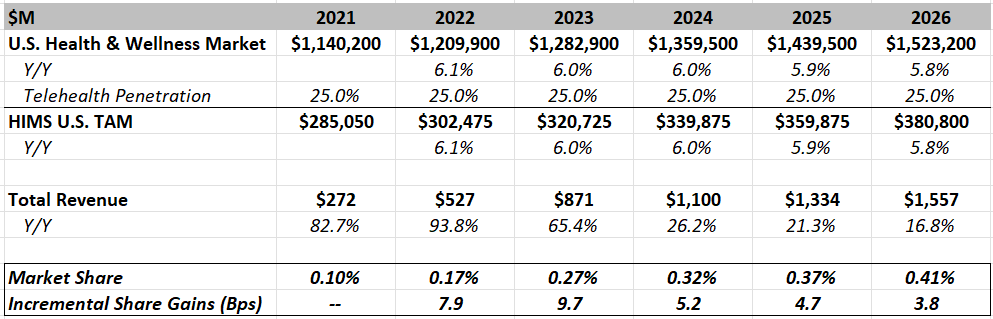

According to Precedence Research, the U.S. Health & Wellness market – the broad sector in which HIMS operates – achieved a valuation of $1.2 trillion in 2022 and is anticipated to exhibit a compound annual growth rate (“CAGR”) of ~6% through 2026, reaching $1.5 trillion. Notably, data from the Centers for Disease Control and Prevention indicates that 37% of U.S. adults used telemedicine services in 2021. To exercise prudence in our analysis, we conservatively employed a 25% telehealth penetration rate for that year, maintaining it as a constant factor through 2026 to accommodate for the heightened demand for telehealth services in 2020 and 2021 due to the pandemic. Consequently, our calculations place HIMS’ TAM at $285 billion in 2021, which we estimate to grow to $381 billion by 2026. Figure 2 below provides a concise overview of our TAM estimates. It is worth noting that in 2021, HIMS’ revenue of $272 million accounted for a mere 0.1% share of the U.S. market, and even with consensus revenue projections reaching $1.6 billion by 2026, the company is anticipated to hold only a 0.4% market share. This reinforces our assertion that while HIMS is strategically positioned to gain market share in the coming years, the sheer size of the telehealth market for health and wellness is expansive enough to accommodate the success and growth of multiple businesses simultaneously.

Figure 2 (Loft Capital Mgmt., Precedence Research, CDC, Seeking Alpha)

Financial Performance

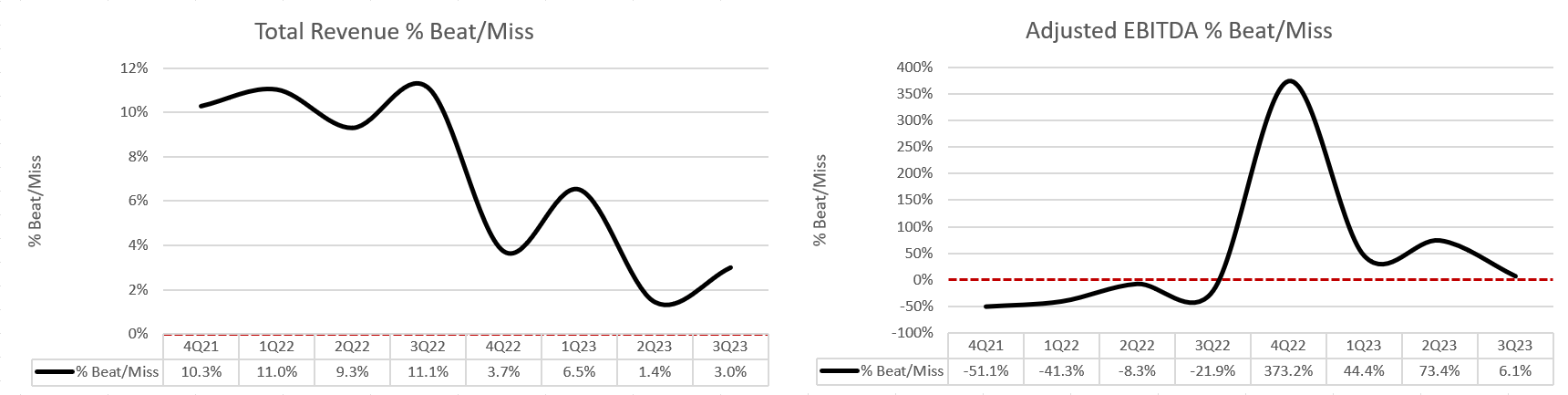

HIMS has exhibited robust financial performance in recent quarters despite the macro headwinds we experienced throughout 2023. In 3Q23 announced in November, the company’s top-line grew 57% y/y, to $227 million, and HIMS generated $12 million in adjusted EBITDA, achieving an adjusted EBITDA margin of ~5%. In Figure 3, we highlight HIMS’ consistent outperformance, surpassing consensus revenue estimates in each of the past eight quarters and beating adjusted EBITDA estimates in each of the past four quarters. This trend underscores management’s strong visibility into the business and adeptness in managing investor expectations, which we view as very important given the early-stage nature of the business. Further, this gives us confidence in HIMS’ ability to consistently meet its financial targets, continuing its trajectory of top-line growth and margin expansion in the coming quarters.

Figure 3 (Loft Capital Mgmt., Seeking Alpha)

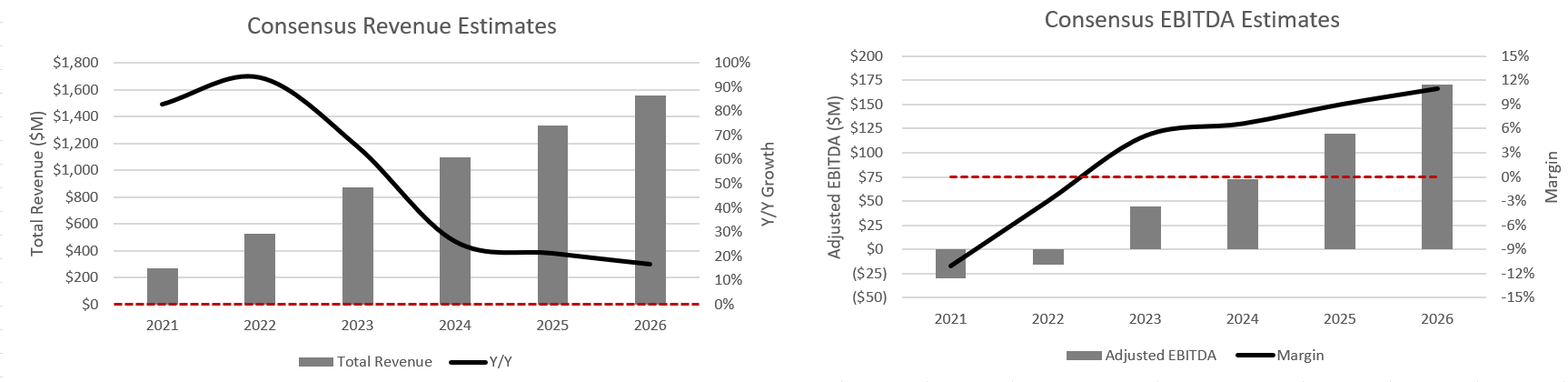

On a broader scale, HIMS has done a great job continuing to grow its top-line at an impressive clip while simultaneously prioritizing profitability. From 2020-2022, the company grew total revenue at a CAGR of 88%. Though analysts are forecasting growth to decelerate going forward, they still expect HIMS to increase its top-line at a CAGR of 36% from 2022-2026, reaching $1.3 billion in revenue, which indicates must faster growth than the broader health & wellness telehealth market. On the profitability front, HIMS finished 2022 with -$16 million in adjusted EBITDA; however, analysts estimate adjusted EBITDA to grow 800%+ from 2022 levels, reaching $119 million by 2025, or a ~9% margin.

From our perspective, HIMS presents investors with an excellent blend of growth and profitability prospects, coupled with an appealing valuation. Moreover, the company operates in a market boasting a massive TAM, which creates a combination that positions HIMS as an attractive investment opportunity going forward.

Figure 4 (Loft Capital Mgmt., Seeking Alpha)

Key KPIs

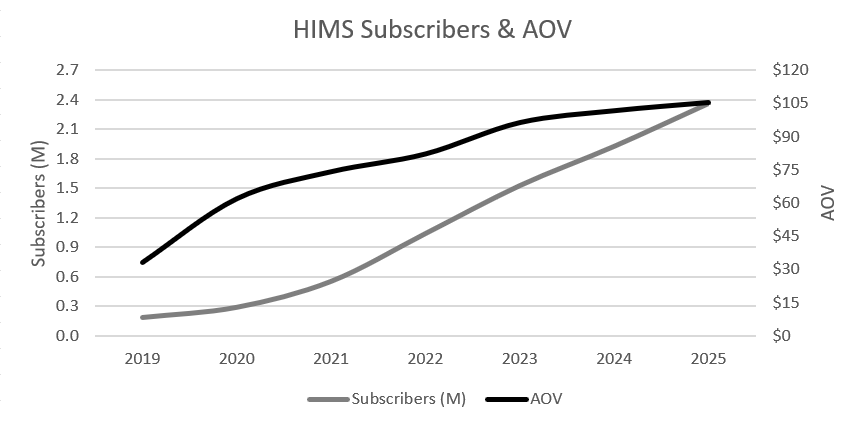

In our opinion, it is important to closely monitor several KPIs for HIMS, most notably the company’s subscriber count and average order value (AOV), which serve as pivotal indicators of the company’s operational health and financial performance. HIMS exited 3Q23 with 1.43 million subscribers, beating consensus estimates of 1.39 million, and representing 37% growth from HIMS’ subscriber count at the end of 2022. From 2022-2025, analysts are forecasting HIMS to grow its subscriber count at a CAGR of ~32%, reaching 2.36 million, which we view as extremely strong growth, particularly given the competitive landscape. Further, HIMS finished 3Q23 with an AOV of $99, 21% above its ending value in 2022, which indicates that customers continue to recognize the value offered by the platform, as reflected in their increased spending on the platform. From 2022-2025, analysts estimate AOV to expand at a CAGR of ~9%, serving as additional validation of our argument that consumers are unmistakably recognizing the value inherent in the HIMS platform and deriving satisfaction from their overall experience.

Figure 5 (Loft Capital Mgmt., Company Filings, Seeking Alpha)

Liquidity Position

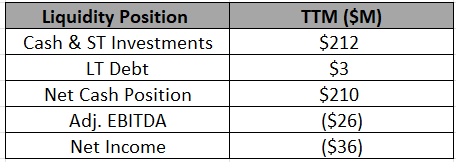

With cash and short-term investments totaling ~$212 million and an essentially debt-free balance sheet, HIMS maintains a net cash position of ~$210 million. This financial fortitude not only exemplifies the company’s prudent fiscal management, but also positions it favorably to weather any potential economic downturns. For investors cautious about the inherent risks associated with investing in a non-profitable early-stage company, a solid balance sheet becomes a key reassurance. HIMS’ robust liquidity not only provides a safety net but also serves as a strategic asset, affording the company the financial flexibility to continue its growth trajectory and navigate market dynamics effectively.

In 2021 and 2022, HIMS reported negative free cash flows of -$38 million and -$33 million, respectively; however, in 3Q23, the company generated $19 million in free cash flow. Further, analysts estimate HIMS to generate $39 million in positive free cash flow for the full year in 2023, marking a significant improvement y/y. Looking ahead, given the company’s trajectory and robust performance in recent quarters, we anticipate sustained growth in free cash flow in outer years, driven by continued top-line expansion and the realization of operating leverage in its business model. Given its lack of debt, robust net cash position, and ongoing growth, HIMS has ample capital resources as it progresses towards profitability, and we do not anticipate any need for the company to raise additional capital in the near to medium term.

Figure 6 (Loft Capital Mgmt., Company Filings)

Analyst Estimates

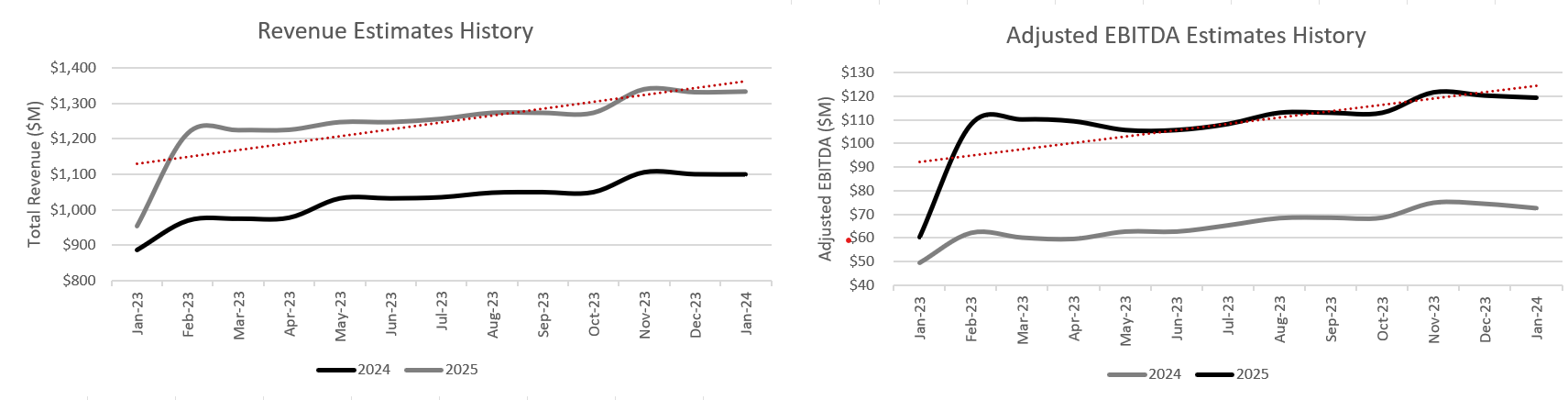

Analyst estimates for HIMS present a compelling narrative, with top-line projections for both fiscal year 2024 and fiscal year 2025 witnessing significant increases of 24% and 40%, respectively, over the past year. Equally impressive are the adjusted EBITDA estimates, which have increased by 46% for 2024 and 98% for 2025 in the same period. These upward revisions signify not only robust financial performance, but also underscore management’s adeptness in navigating the dynamic telehealth landscape. Further, we view increasing estimates as an indication that management has a strong visibility into the business and an effective strategy in managing investor expectations, which we view as a positive both in the next 12-24 months and over the long haul. Although we consider analyst estimates for 2024 and 2025 to be generally reasonable and indicative of HIMS’ recent financial performance, we do see further upside to numbers going forward, rooted in HIMS’ ongoing ability to attract new customers to its platform and broaden its product portfolio, as previously highlighted above.

Figure 7 (Loft Capital Mgmt., Seeking Alpha)

HIMS Long-term Targets

HIMS has set ambitious targets for both the long-term and specifically by 2025. The company is dedicated to achieving adjusted EBITDA margins within the 20%-30% range in the long run, reflecting a substantial opportunity for margin expansion from current levels. By 2025, HIMS anticipates generating a minimum of $1.2 billion in revenue and at least $100 million in adjusted EBITDA, implying an adjusted EBITDA margin of 8.3%. Although current analyst estimates slightly surpass these targets, with expectations of $1.3 billion in revenue and $119 million in adjusted EBITDA for 2025, the consensus underscores a collective confidence in HIMS’ growth narrative and its ability to meet or exceed these ambitious goals. It’s important to note that HIMS is perceived as a “show me” story, requiring concrete evidence of its potential. Despite this, our confidence remains strong, as we believe in the company’s ability to consistently expand its top-line and expand margins in outer years. While there are many puts and takes that go into achieving these long-term targets, generally speaking, we are optimistic about HIMS’ ability to achieve these lofty goals.

Figure 8 (Loft Capital Mgmt., HIMS 3Q23 Investor Presentation, Seeking Alpha)

Valuation

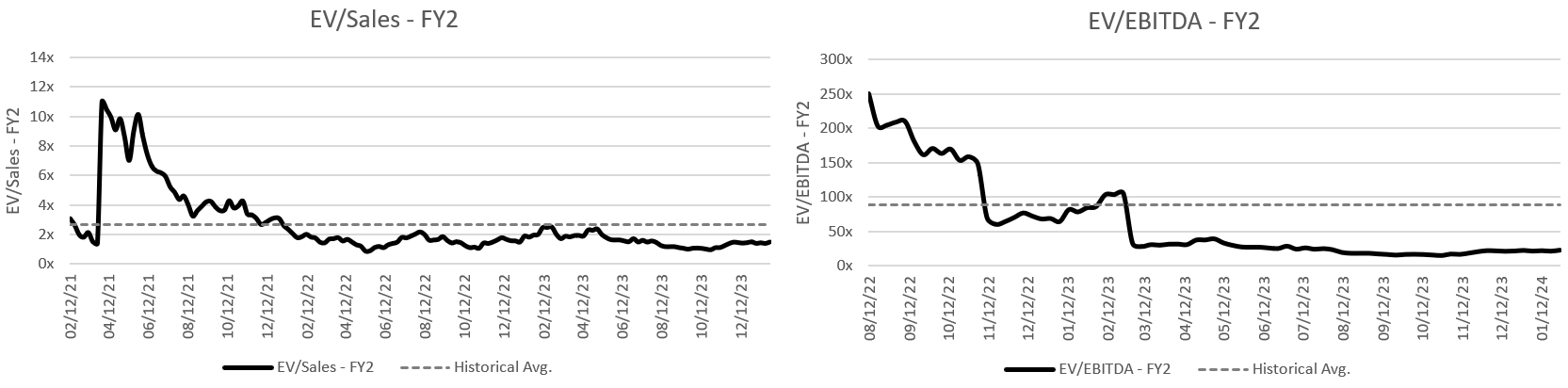

Trading at 1.5x EV/revenue, the stock is currently 43% below its historical multiple, and on an EV/EBITDA basis, it stands at 22.9x, marking a 74% discount from its historical average. We note that HIMS lacks an extensive trading history, having gone public in 2019 and experiencing a pandemic-related surge like many other businesses. As a result, interpreting its recent discounts compared to historical trading levels requires some caution.

Figure 9 (Loft Capital Mgmt., YCharts)

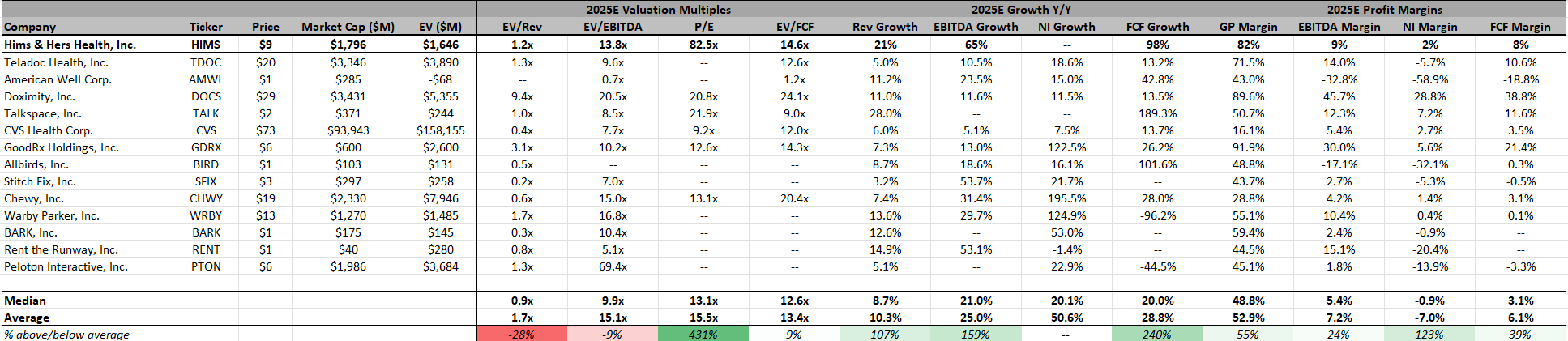

In a comparative analysis of HIMS valuation against its peers, both within the telehealth sector and other direct-to-consumer (D2C) companies, intriguing disparities emerge. HIMS is currently trading at a 28% discount to the peer average on an EV/revenue basis and a 9% discount on an EV/EBITDA basis. Notably, despite these discounts, HIMS boasts superior top-line and EBITDA growth, coupled with a more favorable margin profile compared to the peer group average. This, in conjunction with the fact that over 90% of its revenue is recurring, resembling a SaaS model, positions HIMS as notably undervalued. The recurring revenue model provides a level of predictability and consistency that is akin to SaaS businesses, warranting a premium valuation. The combination of these factors suggests that HIMS may be trading at a discount relative to its peers, in our opinion, presenting a compelling investment opportunity for those seeking growth potential and a robust business model in the telehealth and D2C space. Note, we chose to incorporate various other direct-to-consumer businesses into our comparative analysis for several reasons, including: (1) we believe that there are limited direct competitors in the current market landscape for HIMS, and (2) despite the potential divergence in verticals among the additional D2C companies considered, we find their business models closely resembling that of HIMS, which serves as a good proxy for evaluating HIMS’ current valuation.

Figure 10 (Loft Capital Mgmt., Seeking Alpha)

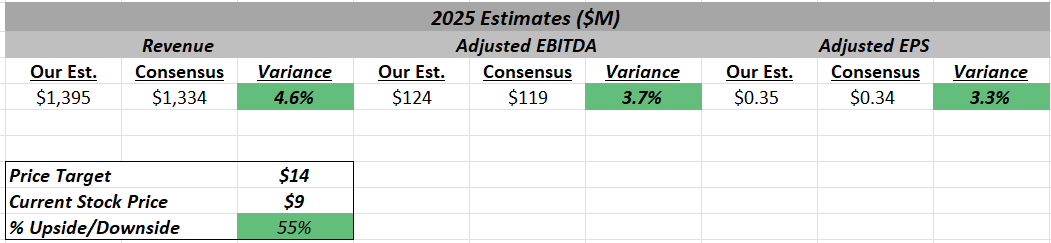

We estimate HIMS’ 2025 revenue to reach $1.395 billion, slightly above consensus, and, by applying an EV/revenue multiple of ~2.0x, below HIMS’ historical multiple but 17% above its peer group average, we arrive at a price target of $14, suggesting ~55% upside from current share price levels. Our premium multiple compared to the peer group reflects HIMS’ stronger top-line and EBITDA growth, a more favorable margin profile, and the recurring nature of its revenue, resembling a SaaS model. Further, our revenue estimate, which is slightly higher than consensus, reflects our belief that there is potential upside to numbers in 2024 and 2025, particularly as HIMS continues to add new customers to its extremely sticky customer base, as well as venture into new verticals, thereby expanding its product portfolio.

Figure 11 (Loft Capital Mgmt.)

Analyst Ratings

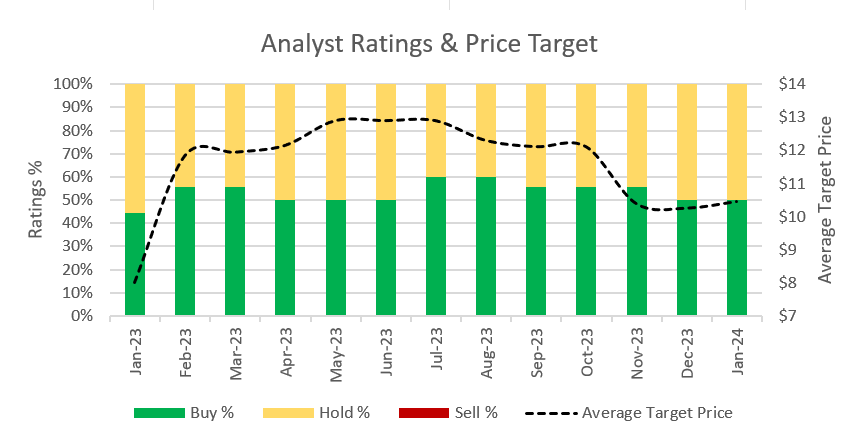

Over the past year, analyst ratings for HIMS have been rather evenly split between Buy and Hold recommendations. Currently, ~50% of analysts have a Buy rating on the stock, accompanied by an average price target of $10, indicating a potential upside of just under 20%. We note that this falls below our price target of $14, which reflects our belief that the market is currently overlooking HIMS, particularly given its robust competitive positioning within its market, which is bolstered by the company’s strong balance sheet and attractive valuation. As we look beyond the immediate horizon, we maintain confidence in HIMS’ ability to capitalize on its competitive strengths, potentially leading to greater returns for investors than the current analyst consensus suggests.

Figure 12 (Loft Capital Mgmt., Seeking Alpha)

What Else We Like

There are several other aspects about HIMS that contribute to our optimistic outlook of the business, including: (1) its impressive 85% long-term retention rate underscores the quality of its products and services, emphasizing the platform’s ability to cultivate a loyal and sticky customer base, (2) with a pay-back period of less than one year, HIMS has solid unit economics, and we believe there is ample room for further improvement looking ahead, (3) 90% of the company’s revenue is recurring, imparting a SaaS-like feel that we believe merits a premium valuation, (4) HIMS boasts a noteworthy 33% insider ownership, aligning the interests of key individuals with the success of the company, which we view as extremely positive for investors, and (5) the fact that HIMS is already adjusted EBITDA profitable signifies a clear and successful trajectory towards sustained profitability, solidifying its position as a compelling investment opportunity in the evolving telehealth landscape.

Risks to Thesis

Investing in HIMS comes with inherent risks that investors should carefully consider, including: (1) further market deterioration could exert pressure on consumers, potentially leading to a reduction in the adoption of non-essential services, including certain telehealth offerings provided by the company, (2) the telehealth sector is experiencing growing competition, especially from major players within the healthcare market. While we reiterate that the TAM for telehealth is substantial, increased competition could impact HIMS’ ability to win market share long-term, (3) HIMS is currently not profitable, and though a clear path to long-term profitability exists, in our opinion, there remains a risk that HIMS may not reach its long-term targets or sustain profitability, (4) the slow adoption of telehealth services by the majority of Americans, who still prefer in-person healthcare visits, presents a challenge that could impede HIMS’ growth over time, and (5) investors should also be aware of potential regulatory changes, technological risks, and the need for continued innovation to stay competitive in this dynamic industry.

Final Thoughts

We believe HIMS has emerged as a compelling investment opportunity, poised for substantial growth both in the short and long term. The company’s robust positioning within its operating market, which is complemented by a massive TAM, forms a solid foundation for future success. Factor in HIMS’ strong financial performance, SaaS-like recurring revenue model, and its attractive valuation, and it becomes evident that the stock offers investors an enticing blend of growth potential and stability. Accordingly, we believe that HIMS represents a great buy today, presenting not only significant upside in the next 12-24 months, but also promising long-term prospects. We rate HIMS a Buy with a price target of $14, suggesting 55% upside from today’s share price.

Q2 2024 Earnings Call Transcript")