LumiNola

Over the past year, or close to it, I have been doing my utmost to become more focused on writing about financial companies, particularly regional banks. One of the firms that I ended up writing about in a bullish article that I published in July 2023 was Webster Financial Corporation (NYSE:WBS), a bank holding company and financial holding company that engaged in many traditional banking and financial services products. At that time, I mentioned how far shares had fallen because of the banking crisis that began in March of that year. Even though shares had recovered nicely from the bottom, I believed that they offered tremendous upside potential. This was based on the idea that deposits were continuing to grow and that the overall revenue and profit side of the business was doing quite well.

As a result of this, as well as how shares were priced, I ended up rating Webster Financial a “buy.” That reflected my belief that the stock would be likely to outperform the broader market for the foreseeable future. And so far, that is precisely what has transpired. Shares are up a whopping 41% if we include the distribution. That’s significantly higher than the 10.8% rise seen by the S&P 500 (SP500) over the same window of time.

After such a meteoric rise, however, I am afraid to say that I think the stock has had its run, or at least most of its run. Given how shares are currently priced, and in spite of continued growth from a deposit and loan perspective, I believe that downgrading Webster Financial Corporation shares to a “hold” only makes sense.

Continued progress

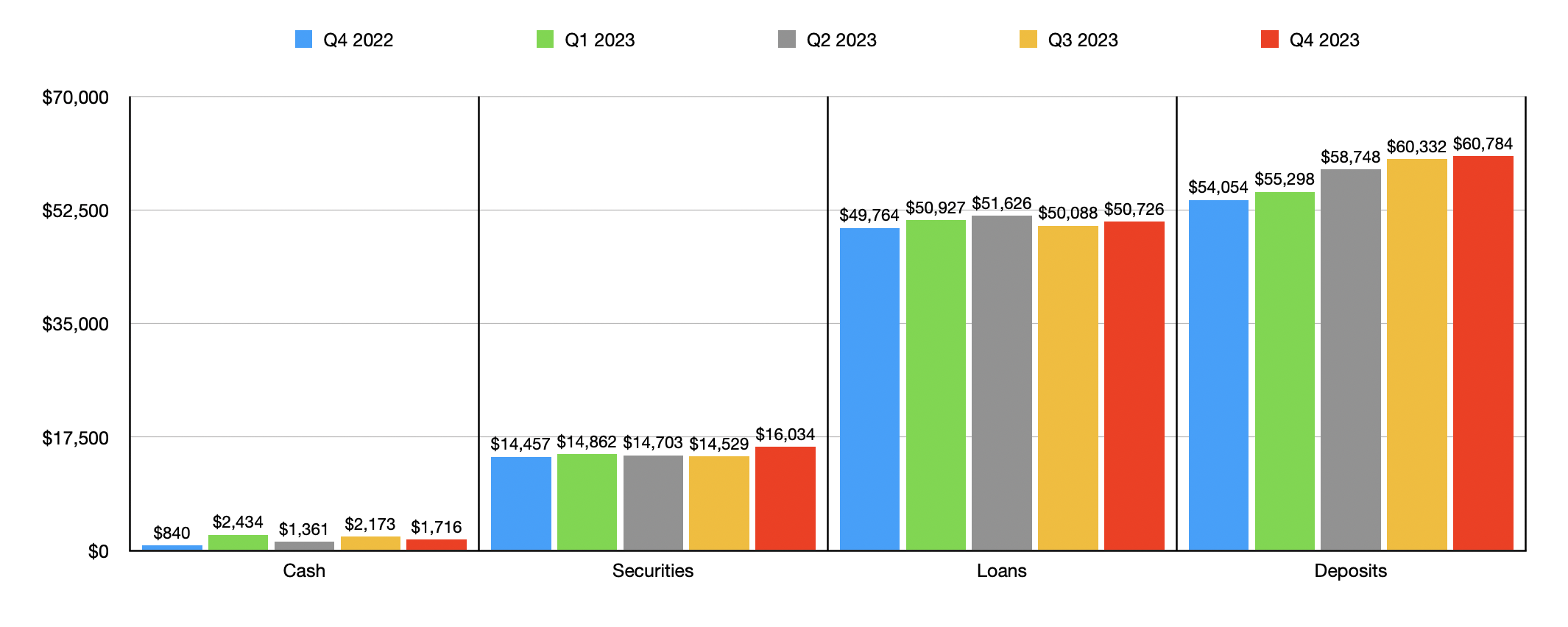

Back when I wrote about Webster Financial, we only had financial data covering the first quarter of its 2023 fiscal year. Today, that data now covers all of the 2023 fiscal year. And what that data shows is that the institution as a whole is quite healthy. Consider, for instance, the value of deposits. Back in 2022, deposits totaled $54.05 billion. Deposits continued to grow even in spite of the bank crisis that began in March of last year. By the second quarter of the year, deposits had expanded to $58.75 billion. And by the end of 2023, they increased further to $60.78 billion.

Author – SEC EDGAR Data

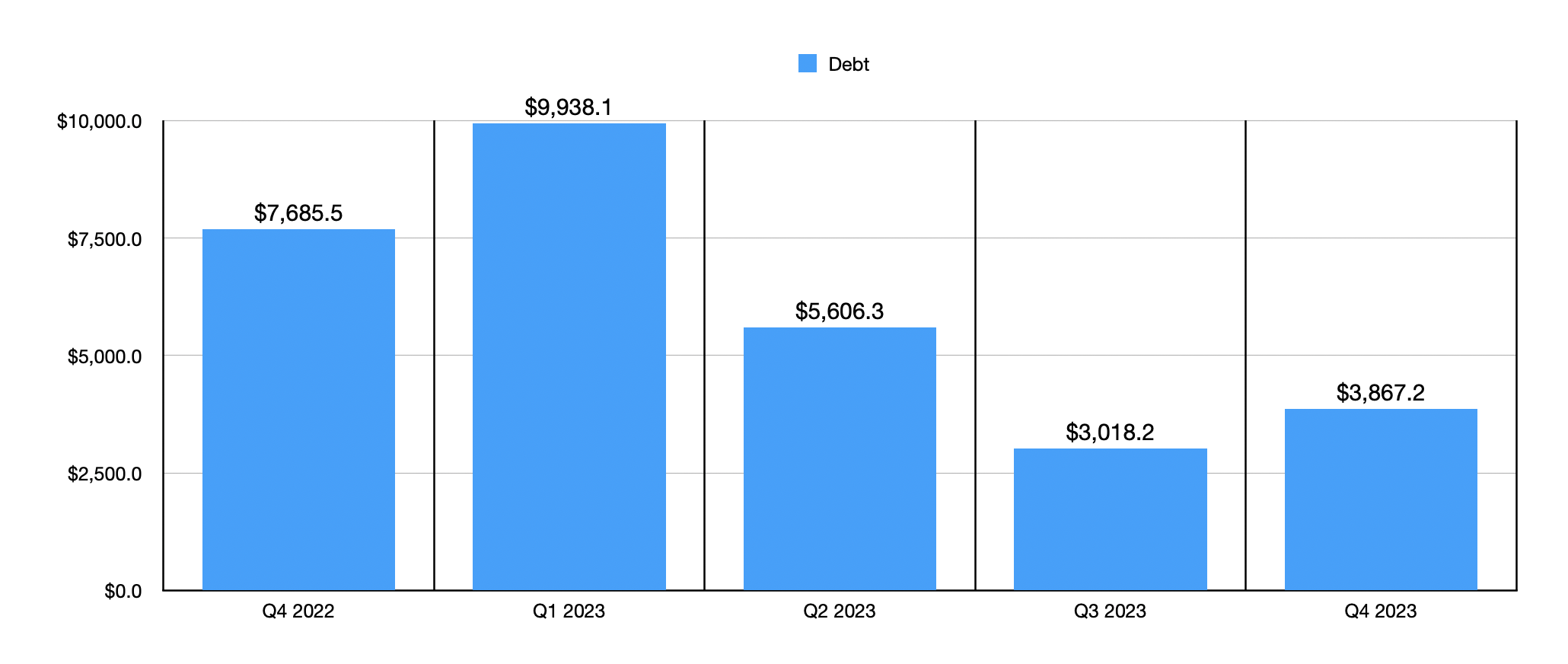

There have been other bright spots for the company. And there have been some that have been mixed. As an example, we need only look at the value of loans. Year over year, loan values grew from $49.76 billion to $50.73 billion. But the reading at the end of 2023 was actually a bit lower than the $51.63 billion the company had on its books at the end of the second quarter of last year. It is worth noting, however, that while loans decreased, the value of investment securities grew. At the end of last year, investments totaled $16.03 billion. That’s a nice increase over the $14.46 billion seen at the end of 2022. Cash and cash equivalents approximately doubled from $839.9 million to $1.72 billion, all, while debt managed to drop from $7.69 billion to $3.87 billion.

Author – SEC EDGAR Data

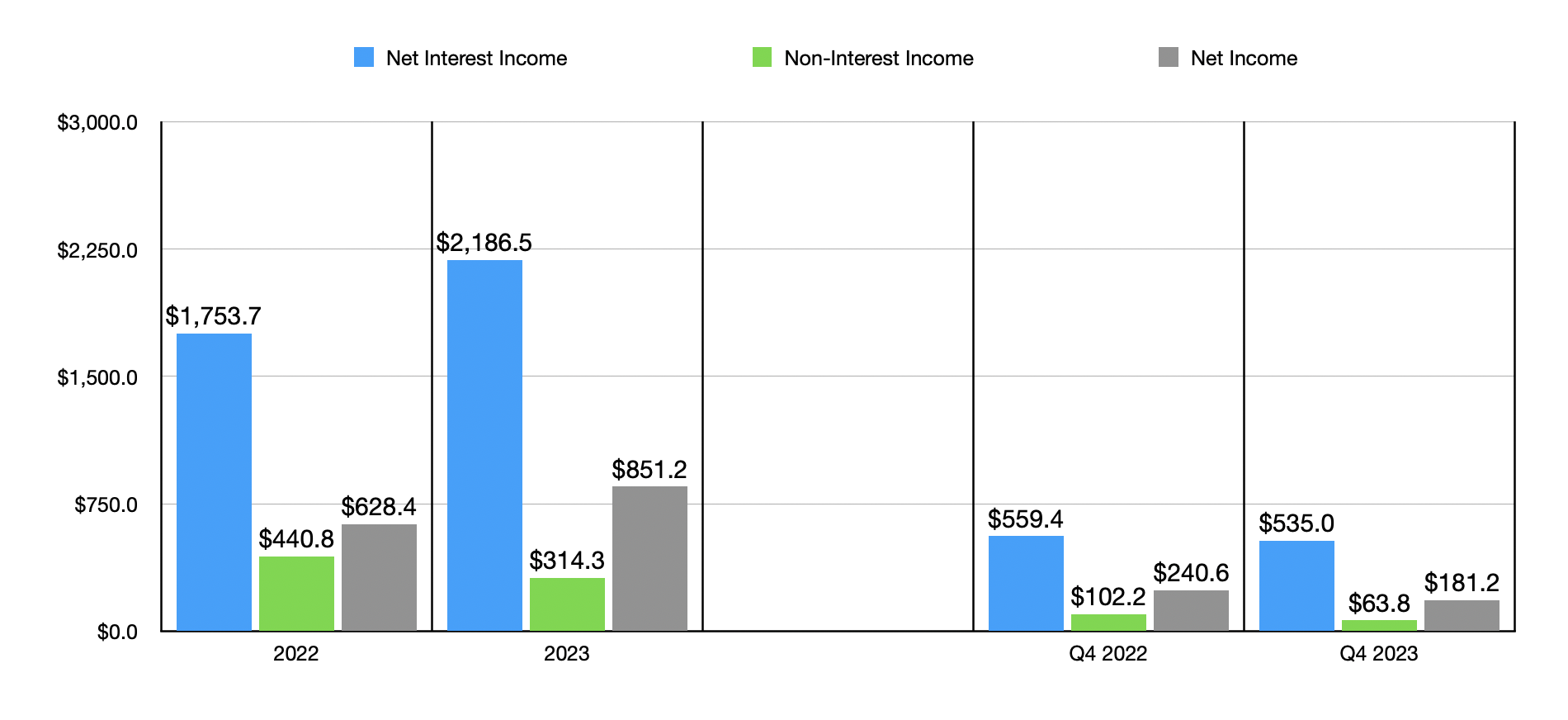

The overall growth of the company’s balance sheet, not to mention higher interest rates that pushed its net interest margin from 3.49% to 3.52%, aided it in growing revenue and profits. As an example, for 2023 in its entirety, the business generated net interest income of $2.19 billion. That’s up from the $1.75 billion generated in 2022. It is true that non-interest income managed to drop from $440.8 million down to $314.3 million. There were multiple contributors to that, such as a decline in wealth and investment services revenue, a drop in loan and lease-related fees revenue, a reduction in deposit service fees, and even a larger loss, year-over-year, on the sale of investment securities. Fortunately, this did not stop net profits from climbing from $628.4 million to $851.2 million.

Author – SEC EDGAR Data

As for the latest quarterly results, which cover the final quarter of 2023, net interest income did pull back slightly, falling from $559.4 million to $535 million. This seems to have been attributed, for the most part, to a decline in the company’s net interest margin from 3.74% in the final quarter of 2022 to 3.42% the same time of 2023. Non-interest income followed suit, dropping from $102.2 million to $63.8 million for the same aforementioned reasons. The drop caused by both of these metrics caused net profits to drop from $240.6 million to $181.2 million.

Author – SEC EDGAR Data

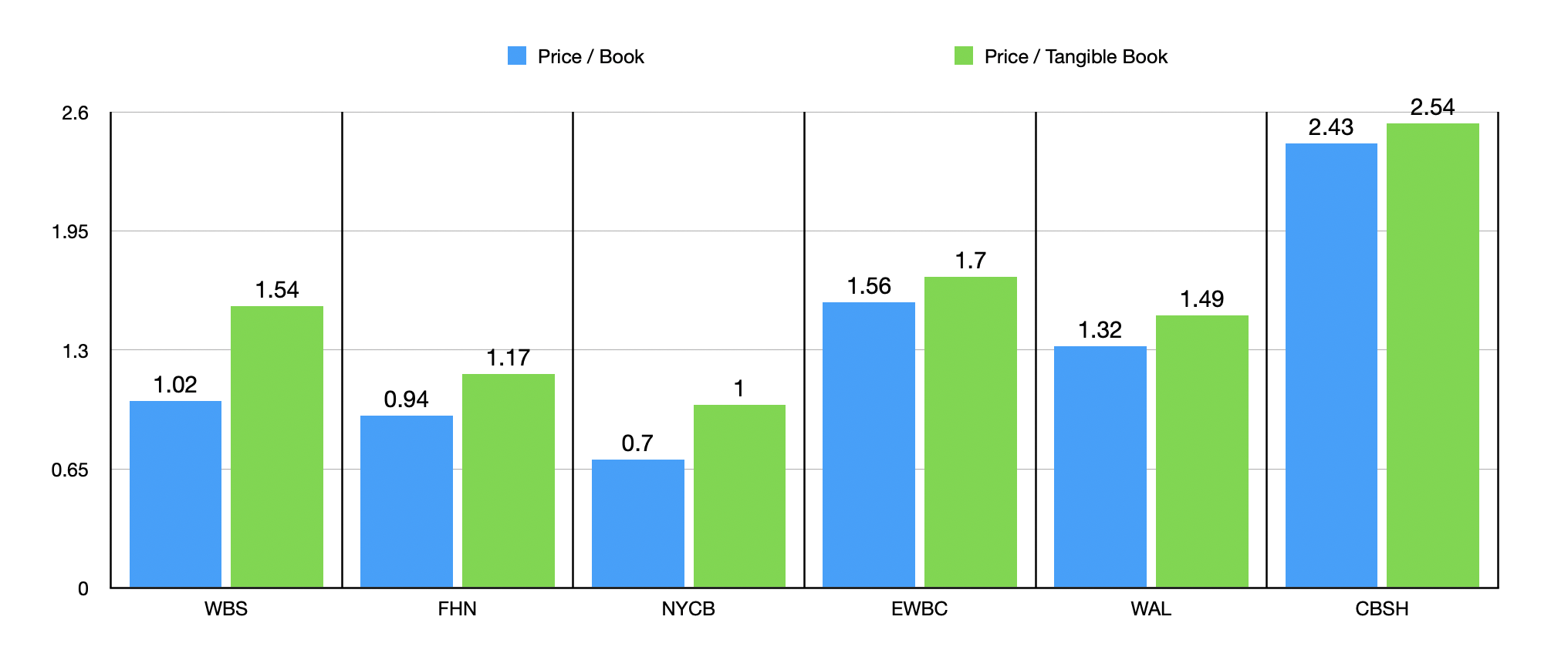

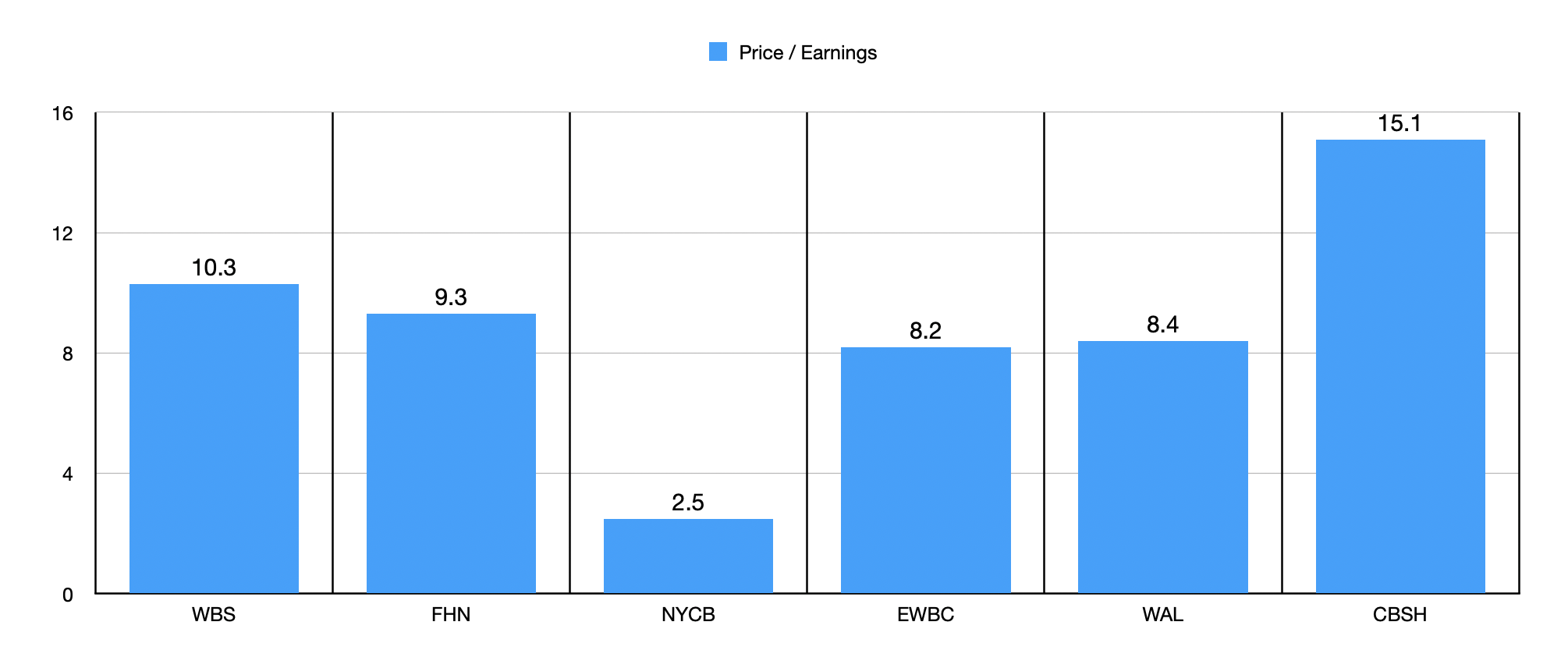

The company’s book value and tangible book value both managed to grow for 2023 as well. At the end of 2022, book value per share was $44.67. By the end of 2023, it had risen to $48.87. Over the same window of time, tangible book value per share grew from $29.07 to $32.39. Speaking of book value, the book value as of the end of 2023 translates to a price to book multiple of 1.02, while the price to tangible book value is 1.54. In the chart above, you can see how the enterprise stacks up on this front against five similar firms. Only two of the five businesses shown are cheaper than on a price to book basis. That number increases to three out of the five when it comes to the price to tangible book value approach. There are, of course, other ways to value the business. On a price to earnings basis, shares are trading at a multiple of 10.3. As the chart below illustrates, that makes it the second most expensive of its group.

Author – SEC EDGAR Data

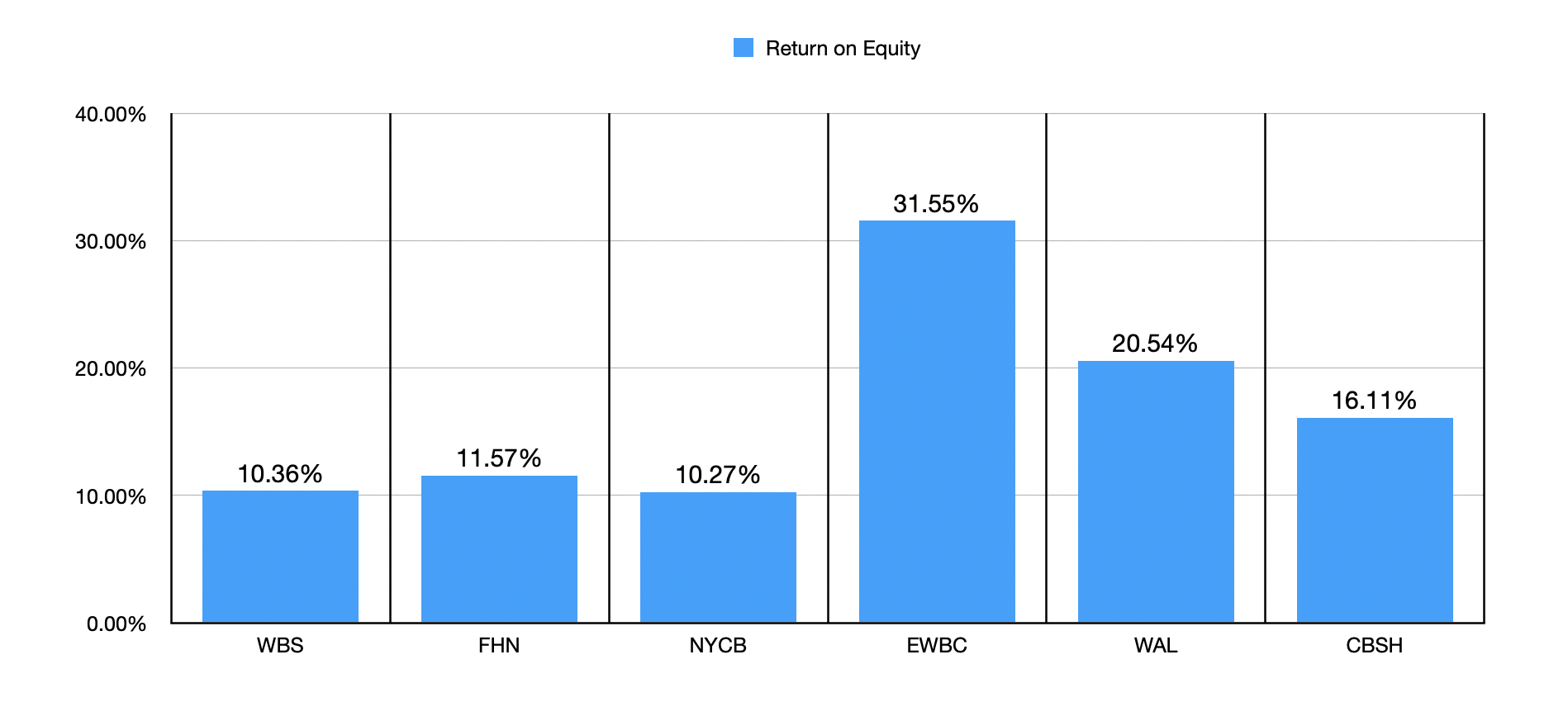

So what we have here is an institution that maintains high quality and that looks to be more or less fairly valued compared to similar firms on a price to book basis, but is expensive relative to earnings. We also need to pay attention, however, to other metrics that help us determine the value of the enterprise. The first of these shown below is the return on equity. The current return on equity of Webster Financial is 10.36%. Only one of the five companies that I compared it to have a reading lower than that.

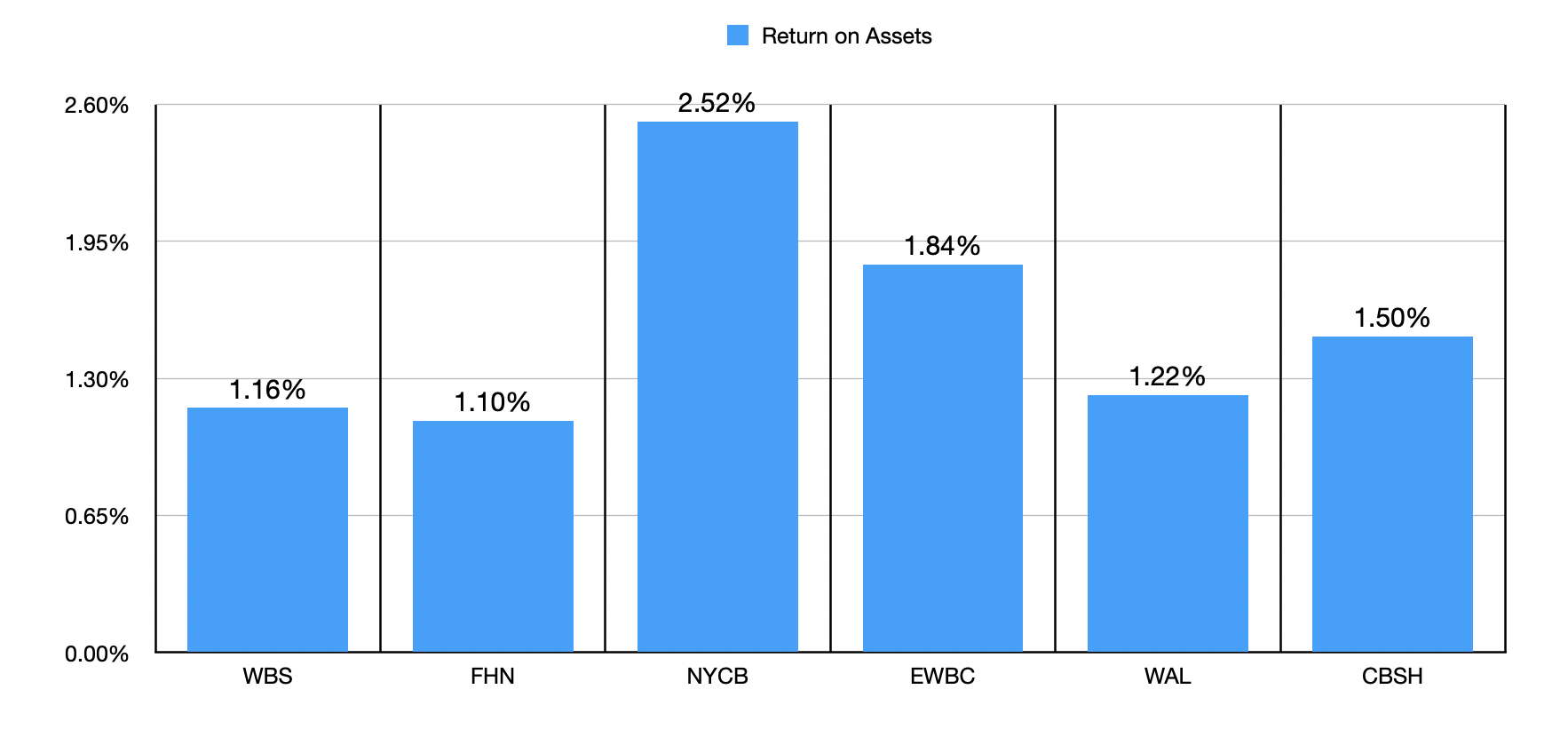

The same exact thing applies when it comes to the return on assets reading of 1.16%. Only one of the five institutions has a lower reading there too. As you can imagine, this is disappointing. The numbers calculated are not bad by any means. But they certainly don’t point to a scenario where the stock should be trading at a premium to its peers. If anything, a slight discount might be justified.

Author – SEC EDGAR Data Author – SEC EDGAR Data

Takeaway

From all that I can see, Webster Financial remains a decent institution. Shares experienced tremendous upside over the past several months. Long term, I suspect that the company will continue to improve. But that doesn’t mean it will always be a great investment.

Given the upside achieved, I would argue that there probably are other opportunities that make more sense right now than Webster Financial Corporation shares. This is especially true when you consider how Webster Financial fares compared to similar firms. Because of that, I’ve decided to downgrade the stock from a “buy” to a “hold.”

Q2 2024 Earnings Call Transcript")