MichaelWarrenPix

On Thursday, Valley National Bancorp (NASDAQ:VLY) saw its shares decline by about 4% after reporting fourth quarter earnings. Shares are lower than a year ago, as is the case with many regional banks, far underperforming the market, though recent performance has been better. Since recommending shares as a buy in October, they have returned nearly 30%, eclipsing my $10 price target. With new financial results and its strong price performance, now is an opportune time to revisit VLY. I remain bullish.

Seeking Alpha

In the company’s fourth quarter, Valley earned $0.22, which missed estimates by $0.03 as revenue fell by 13% to $450 million. For the full year, Valley earned $1.06. The company has been very successful in diversifying away from its legacy tri-state area (NJ/NY/CT) and into the Southeast, which now accounts for about half of its deposit base. I have viewed shares favorably because the company has done a remarkable job of retaining deposits, despite its small size; additionally, credit quality has been quite strong.

Moreover, with its relatively small securities portfolio, VLY has not been plagued with unrealized losses on fixed-income investments; indeed, it has a modest $146 million loss sitting in accumulated other comprehensive income (AOCI). Because of its small AOCI loss, I view VLY as more defensive against a surprise further increase in interest rates, though this appears to be less of a risk than it was a few months ago.

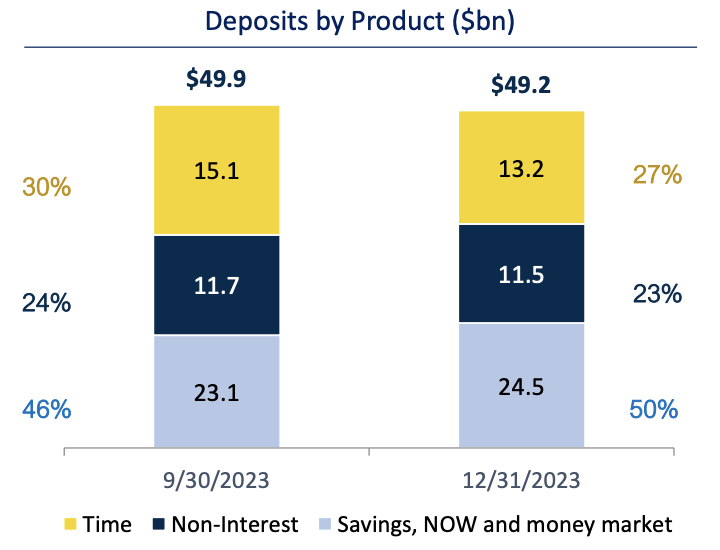

In this quarter, its performance was a bit more mixed. First, deposits fell by $640 million to $49.2 billion sequentially. They are still up from $47.6 billion a year ago. As you can see below, this decline in deposits was driven by time deposits while noninterest-bearing deposits were close to flat and core deposits grew.

Valley National Bank

Last quarter, VLY had significant maturities in its online and indirect deposit platforms, which can be more expensive, as VLY is competing solely on interest rates. For deposits earned by customers at branches, ancillary services (i.e. treasury services for corporate customers) allow banks to compete on non-rate factors. I do not view deposit declines as good things, but this mix shift is relatively favorable.

Management also feels confident in the stability of its franchise because, on January 16th, it reduced online deposit rates by 20bp. Since December, it has cut 1-year CD rates by 75bp. These measures should reduce some funding cost pressure. In Q1, $5.6 billion of deposits roll off at 4.96%. In total, deposit rates increased by 19bp to 3.19%, so these maturities are fairly expensive funding. VLY will need to roll the vast majority of these over, which will test its decision to lower rates. I will closely be monitoring deposit flows in Q1; if we see deposits broadly stable despite this level of maturities and lower rates, investors will feel much more comfortable with VLY’s pricing power.

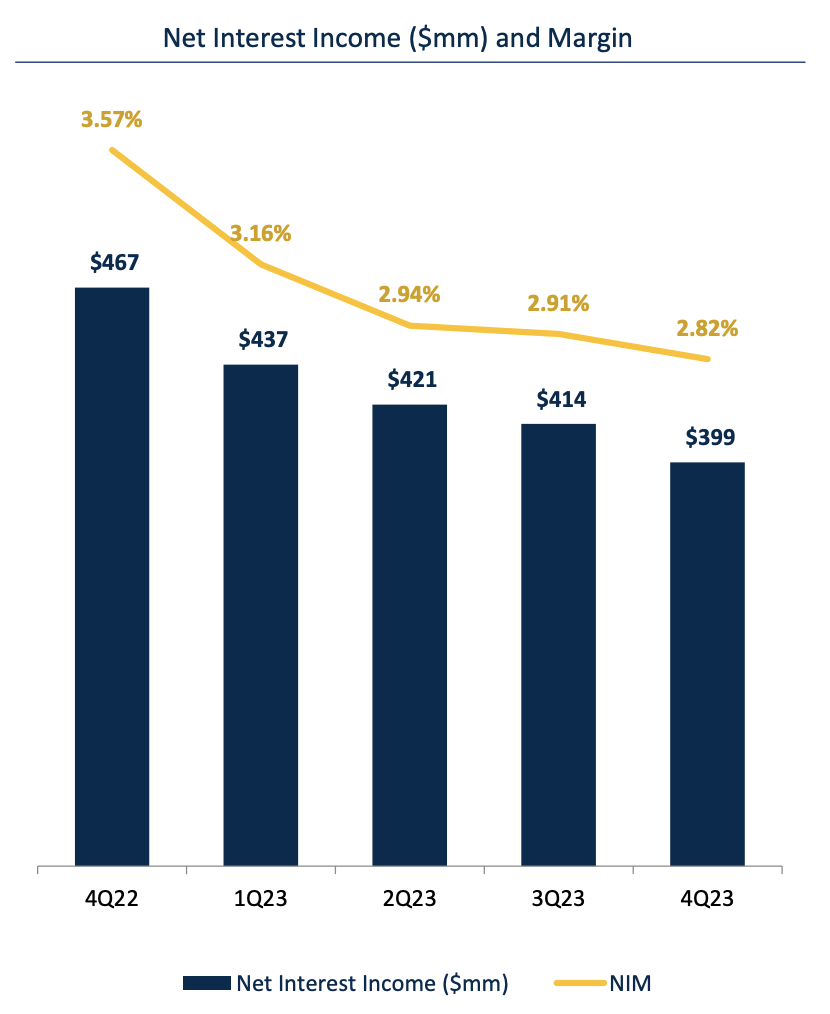

Because deposit costs rose by 19bp, VLY saw its net interest margin (NIM) decline by 9bp. This was a disappointing performance considering NIM had narrowed just 3bp in the prior quarter and was primarily due to deposit costs rising more than loan yields. Importantly, management expects net interest income to rise from here, suggesting we are also likely at or near a trough in NIM.

Valley National Bank

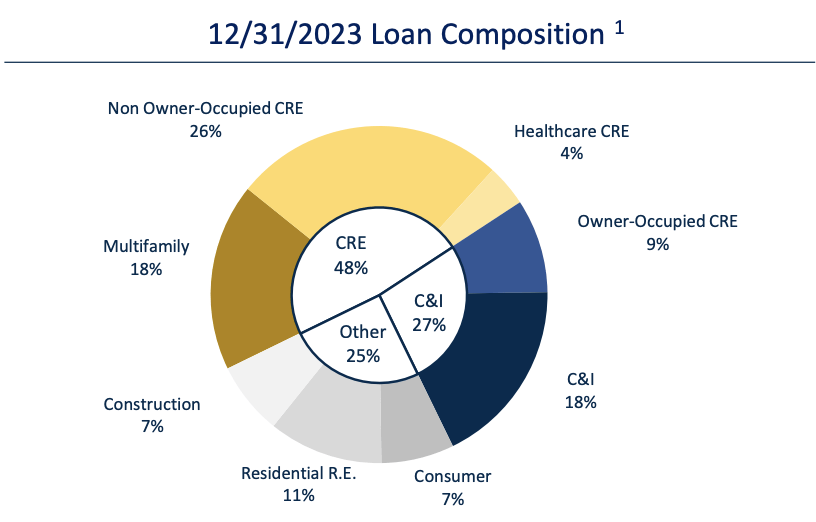

Despite lower deposits, loans rose by $0.1 billion to $50.2 billion. Valley has a fairly granular loan book with about half of its exposure in commercial real estate (CRE). It has a $28 billion CRE portfolio with 25% in Florida, 21% in New Jersey, and 24.9% in New York City. This is an exposure I continue to follow closely given the pressures in the sector. Importantly, the average loan-to-value is just 57%, meaning valuations could fall significantly before VLY would face losses on its loans.

Valley National Bank

Now, not all commercial real-estate exposure is equal, and much of its exposure is to multi-family, where I feel comfortable given the buoyant US housing market and structural under-supply. Much of its exposure is also in Florida, which continues to be a high-growth market, given migratory trends. It does have $3.3 billion in office, which faces more sustained pressures, in my view. Importantly, the average loan is just $3 million with a 53% loan-to-value. The granularity and asset coverage in this portfolio make me comfortable that losses will be manageable.

While credit quality is good, there was some deterioration, and in Q4, it provisioned $21 million for loan losses from $9 million previously as net charge-offs rose to $17 million. This is still below 0.2%, a very strong level. Allowances for credit losses are 0.93% of loans while non-accrual loans rose from 0.52% to 0.58%. This coverage is less than 2x, which I would often view as light. However, the vast majority of its portfolio is secured by assets with low LTVs, where losses given default tend to be much lower than on unsecured debt. This is a reason net charge-offs are so low. Credit metrics should be closely monitored but they are not concerning.

Valley’s own credit quality is also strong. Its common equity tier 1 (CET1) ratio of 9.3% rose from 9.2% last quarter, and unlike banks with large AOCI losses, VLY does not have a need to raise capital from here. I would expect it to maintain its ~4% dividend and use retained capital to continue to grow the business and further diversify into the Southeast. As of Q4, it has a $8.79 tangible book value.

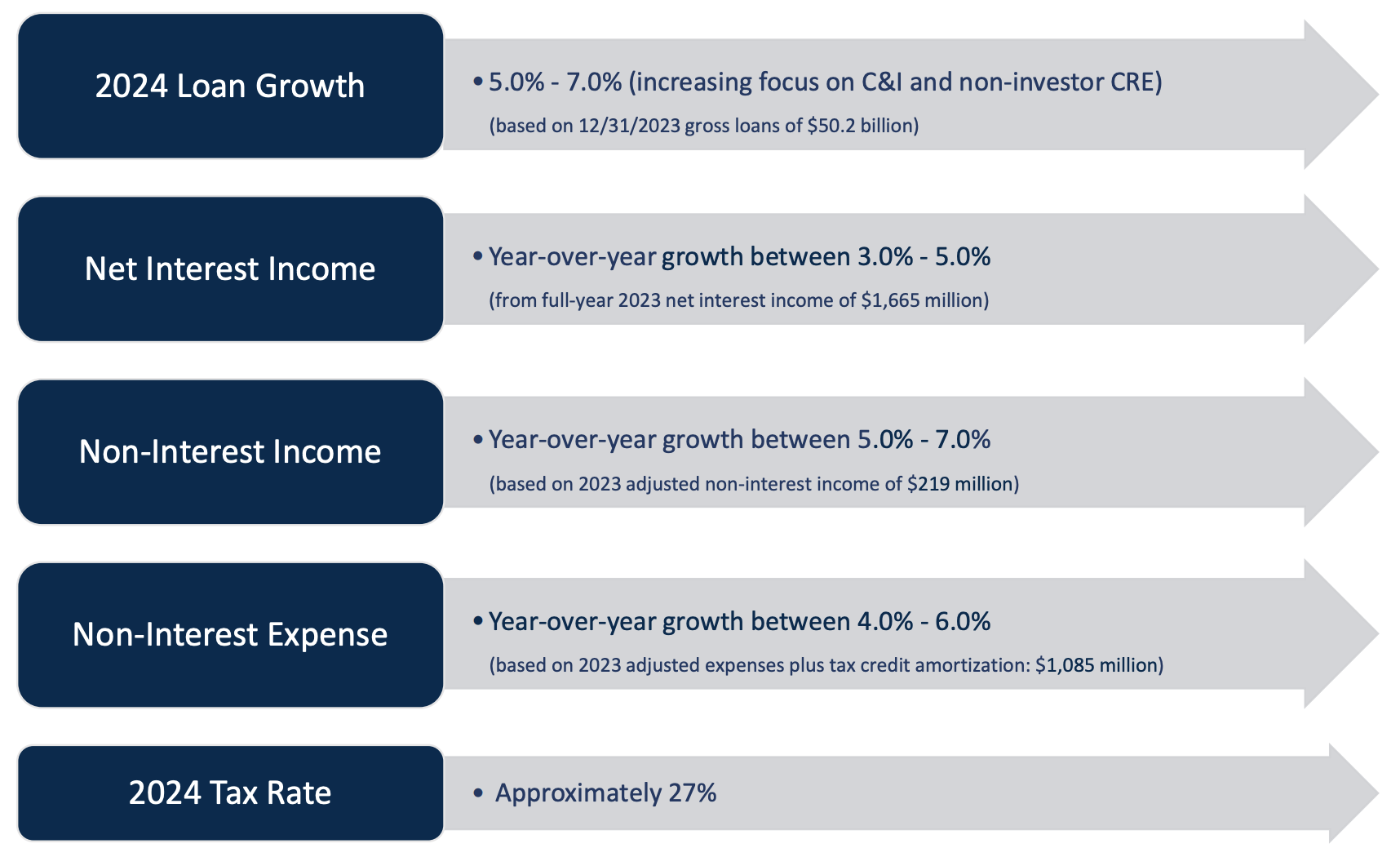

Speaking to growth plans in 2024, management is focused on growing core deposits, increasing C&I lending, and increasing fee revenue, to reduce its sensitivity to interest rates. Many regional banks will be pulling back on loan growth in 2024 given smaller deposit bases, but VLY’s solid 2023 deposit performance will allow it to go on offense next year. As you can see below, Valley expects to grow loans and net interest income in 2024. Based on guidance, Valley expects net income to rise by about $20 million in 2024, or about $0.04 to about $1.10.

Valley National Bank

I continue to view Valley as a relatively defensive bank. Now, if interest rates fall significantly further, it may see less benefit than other regional banks with large unrealized securities portfolio losses, as capital concerns around those banks fade. By the same token, if rates stay higher for longer, Valley should outperform. VLY is a quintessential boring bank, taking deposits and making asset-backed loans. This model has proven successful in 2023.

Its Q4 deposit performance was a bit weaker than prior quarters, but its decision to cut rates is a positive heading into 2024. Given its strong deposit performance over the past year, management deserves the benefit of the doubt on this decision, and if it holds deposits in Q1, I expect shares to react positively. With $1.10 in earnings power, shares are about 9.5x earnings. While much of the upside has already occurred, I can see the stock moving towards $11 or 10x earnings, providing a ~10% total return. As such, I would continue to own VLY as a relatively defensive bank in your portfolio.

Q2 2024 Earnings Call Transcript")