AzmanJaka

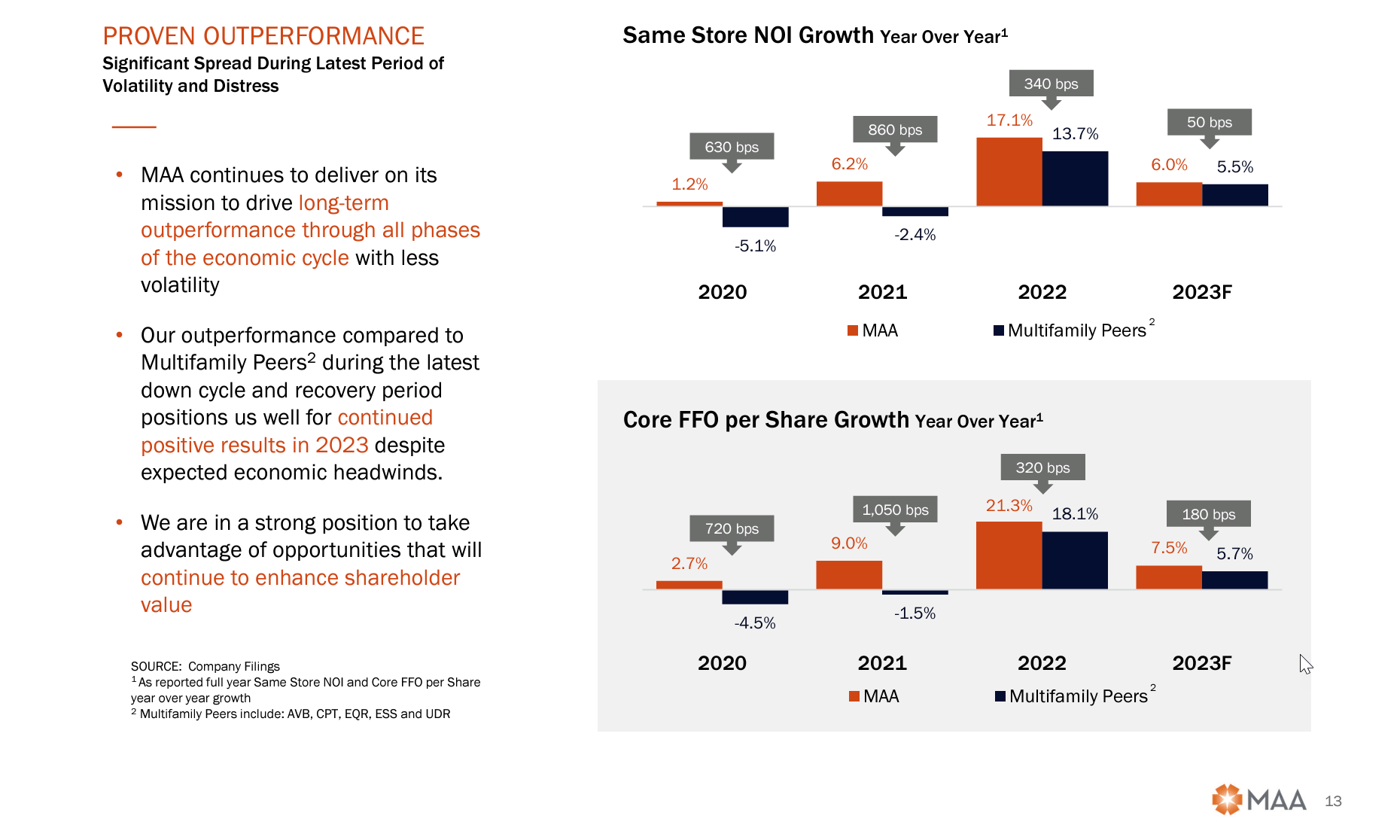

The current market environment could be classified as quite optimistic, in that most stocks seem to be trading at relatively aggressive valuations. Coming off a strong 2023 of stock market returns, excitement over the prospects of AI, and the potential for the Federal Reserve to begin cutting rates has investors feeling confident. As I look for undervalued securities, I’m not finding a ton that possesses a large margin of safety, but I do believe there are still attractive opportunities in the real estate sector, where concerns of higher interest rates have severely impacted stock prices. Such an opportunity exists in the common stock of Mid-America Apartment Communities, Inc. (NYSE:MAA). At a blended P/AFFO of 15.85x and a dividend yield of 4.49%, I believe that MAA could generate double-digit per annum returns over the next 3-5 years as FFO/AFFO grows, and the valuation expands slightly.

A lack of housing affordability has increased demand for apartment homes, particularly in the fast-growing Sun Belt. The work-from-home phenomenon resulted in people migrating from big cities such as San Franciso, to the Sun Belt where MAA has a large presence. This allowed prices to rise at a rapid rate but was also followed up by increasing supply as apartment developers chased returns. While the supply overhang is likely to hurt short-term returns, higher interest rates have resulted in the curtailing of much new development, which should create a very favorable business environment over the next 3-5 years, as the current supply is filled up.

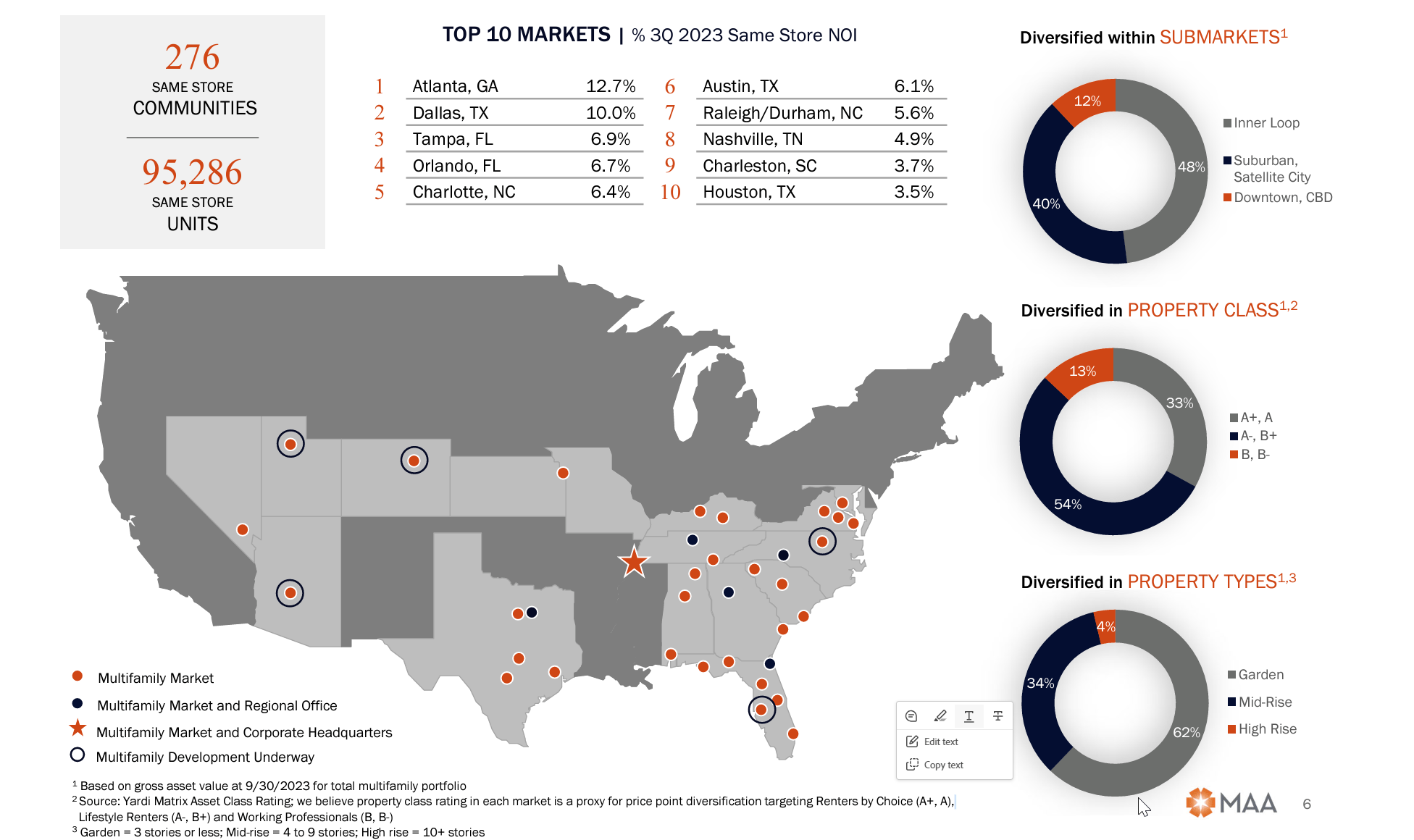

As of September 30th, 2023, MAA had ownership in 101,987 apartment homes, including those in communities under development across 16 states and the District of Columbia. The company has paid 119 consecutive quarters of dividends, stemming from its IPO in 1994. That dividend has never been cut or suspended, including during the Financial Crisis, which says a lot. MAA boasts an A3/A- credit rating and has one of the strongest balance sheets in the industry with net debt to adjusted EBITDARe of 3.4x. As of the end of Q3, MAA has full capacity available on its $1.25B revolver and $625MM commercial paper program, along with $162MM of cash on hand. The company’s $4.44B of total and preferred stock is 100% fixed to protect against rising interest rates. Over the last 20 years, MAA has generated annual total stockholder returns of roughly 11.5%.

Q3 Investor Presentation

62% of MAA’s units are garden units, with another 34% and 2% in mid-rise, and high-rise, respectively. By possessing high-quality properties in highly desired locations, MAA can drive long-term growth and stability. MAA communities are in cities that have faster job growth, and higher household formation and population growth rates. Many companies such as Tesla, Oracle, Caterpillar, etc., have moved their corporate headquarters to more favorable business environments in the Sun Belt, which has helped drive the influx of high-earning people looking for attractive housing options. A massive influx of investment is going into Semiconductors and EVs, with many of the beneficiaries once again being in the Sun Belt. Higher interest rates and higher home prices make down payments more and more difficult to afford. This puts high-earning workers in the market for luxury apartment homes for the period that they are saving up to buy their first home once they have established their family. In MAA’s top markets, the average new lease/income is 22%, which is much more favorable than most mortgage/income ratios.

Q3 Investor Presentation

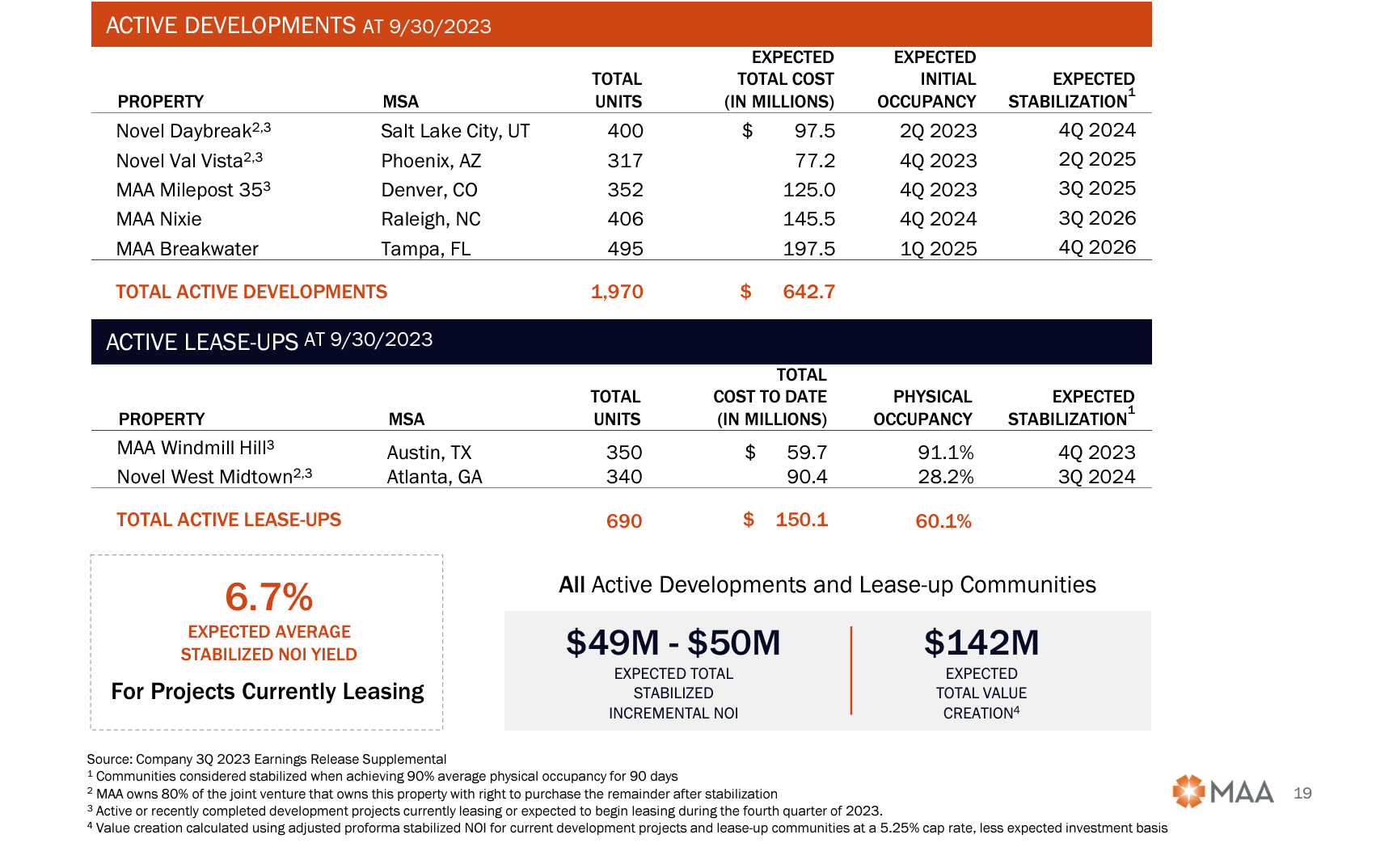

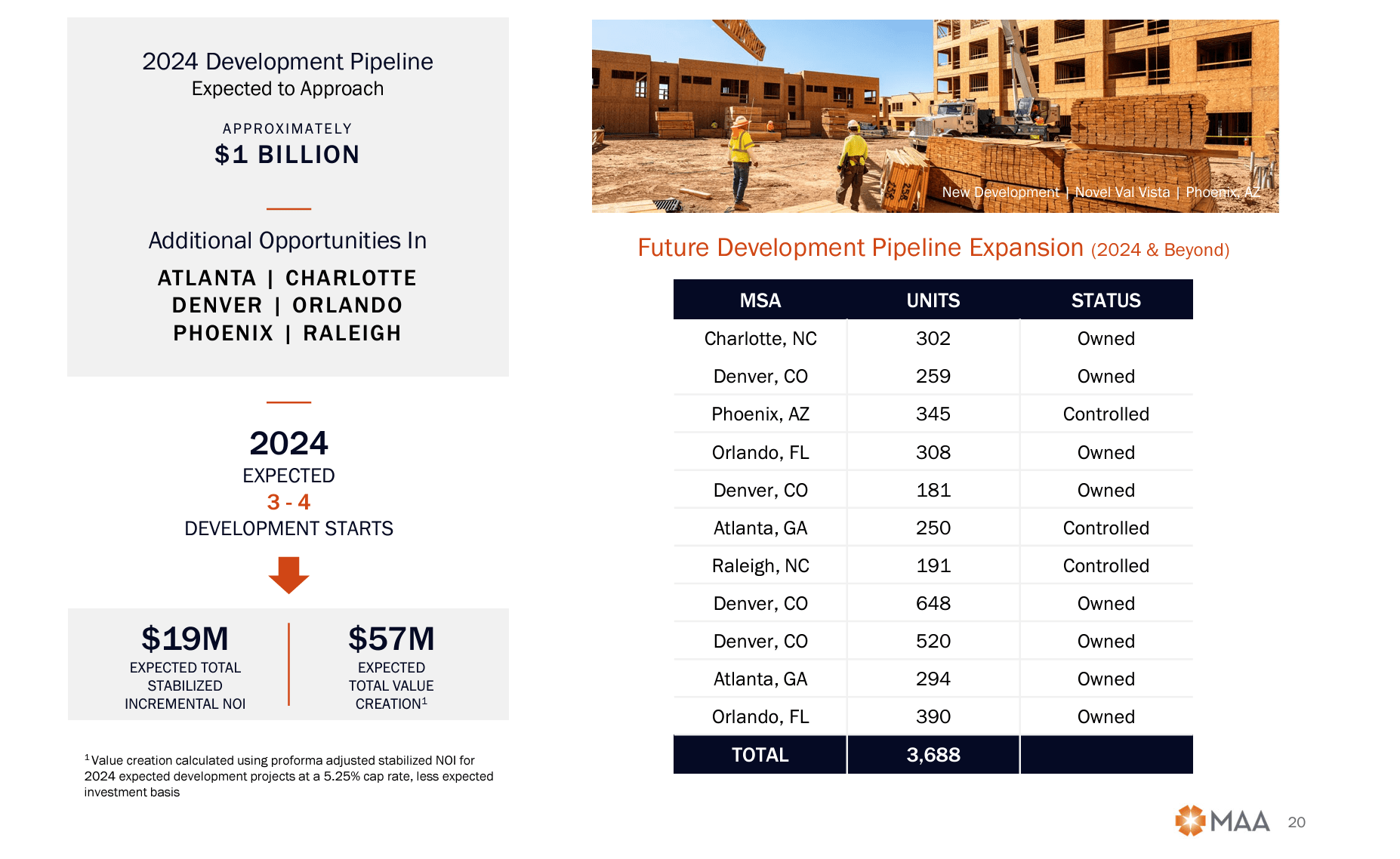

Between 2020-2022, MAA identified approximately 14k units for redevelopment across its Same Store portfolio to create additional rent growth. At a cost of roughly $6k per unit, average rents increased by 9.5% in 2020, 12.2% in 2021, and 10% in 2022. An average redevelopment cost of around $6,500 in 2023 resulted in an average rent growth of 7-8%. The company sees another 14K of near-term redevelopment opportunities, which should enhance annual revenue by about $19.7MM on a total spend of around $89.5MM. At a 5.9% cap rate, this would be worth $333.9MM, or net value creation of $244.4MM.

MAA was expected to spend roughly $200MM in acquisitions and around $250MM in development funding for 2023. We will get the final numbers that they spent when the company reports earnings on February 7th, where we should also get some updates on spending plans for 2024. Apartments are not generally a highly volatile industry outside a major recession, so I’d expect 4th quarter results to be relatively stable, with guidance being the most important factor for stock performance. Importantly, the company did not need to issue debt given its pristine and conservatively financed balance sheet. Total corporate overhead is around $126.5MM, and around $4.5MM is spent on income taxes, given the REIT structure, where most taxes are paid by shareholders. Sunbelt demand is likely to continue being very strong over the next several years, while apartment supply is projected to peak in 2024. Employment has been quite stable and home affordability is very low, which provides a nice tailwind in MAA’s properties. New supply is likely to be quite aggressive with pricing concessions, so I’d look for 2024 to be kind of a trough year for growth. Management is focused on the basic blocking and tackling of the business such as unit development and repositioning. MAA’s strong balance sheet and low debt costs also allow it to be an acquirer of assets that might become available given the stress in the industry due to higher financing costs. MAA has $400MM of 4% debt maturing in June of 2024, so we’ll see if they look to refinance that debt or use their cash and revolver.

Q3 Investor Presentation Q3 Investor Presentation Q3 Investor Presentation

MAA has a clear mid-term line of sight on growth with an active development campaign in many of the hottest markets. Mr. Market has sold the stock off based on short-term supply concerns, which should begin to alleviate as we get into 2025 and 2026. While higher interest rates are negative for potential debt refinancing, these are assets that will produce cash flows for many decades into the future, across a multitude of interest rate cycles. Few companies are better positioned to deal with volatility and stress such as what comes with recessions than MAA. As weaker competitors run into trouble, MAA stands ready and willing to take advantage and enhance its market share.

As of the end of Q4, MAA’s Occupancy rate stood at a very healthy 95.5%, while YTD blended lease-over-lease pricing growth was 2.6%. New leases were down 1.2% YTD, while renewal leases were up 6.2%. The company projected full-year 2023 property revenue growth of 6.25%, with effective rent growth of 7%, along with average physical occupancy levels of 95.6%. Property expense growth was projected at 6.5%, with real estate tax growth of 5.75%, while property NOI growth was projected at 6%.

Full-Year 2023 Core FFO/Share is projected to be up 7.5% YoY to $9.14, which would equate to a P/FFO of about 14.22, which is down from an average of roughly 15.5. FFO is projected to be roughly flat in 2024, while rising to $9.43 and $10.31 in 2025 and 2026, respectively. If the stock were to trade at 15x FFO at the end of 2026, the price would be around $154, and total returns would be right around 10% per annum when factoring in the dividend. There is upside beyond that, but these are conservative assumptions. I believe this is likely a better return than what the overall market will average over the next several years, as I think equities are overvalued. I also believe that MAA offers very dependable cash flows and lower volatility than most equities. I view MAA as a very attractive buy and hold at current prices and have been buying more and more of the stock on dips.

Q2 2024 Earnings Call Transcript")