champpixs/iStock via Getty Images

Investment Thesis

Freshworks (NASDAQ:FRSH) is a relatively new entrant in the Customer Relationship Management (CRM) industry. The company was listed in the markets in 2021, but like most of the younger companies on the market, it received a rude awakening in 2022 as the markets re-rated the equity risk premiums and cash flows needed to be prioritized. Last year, the company unveiled its multi-year operating plan in its Investor Day presentation, showcasing its product roadmap and its margin expansion strategy to achieve durable growth.

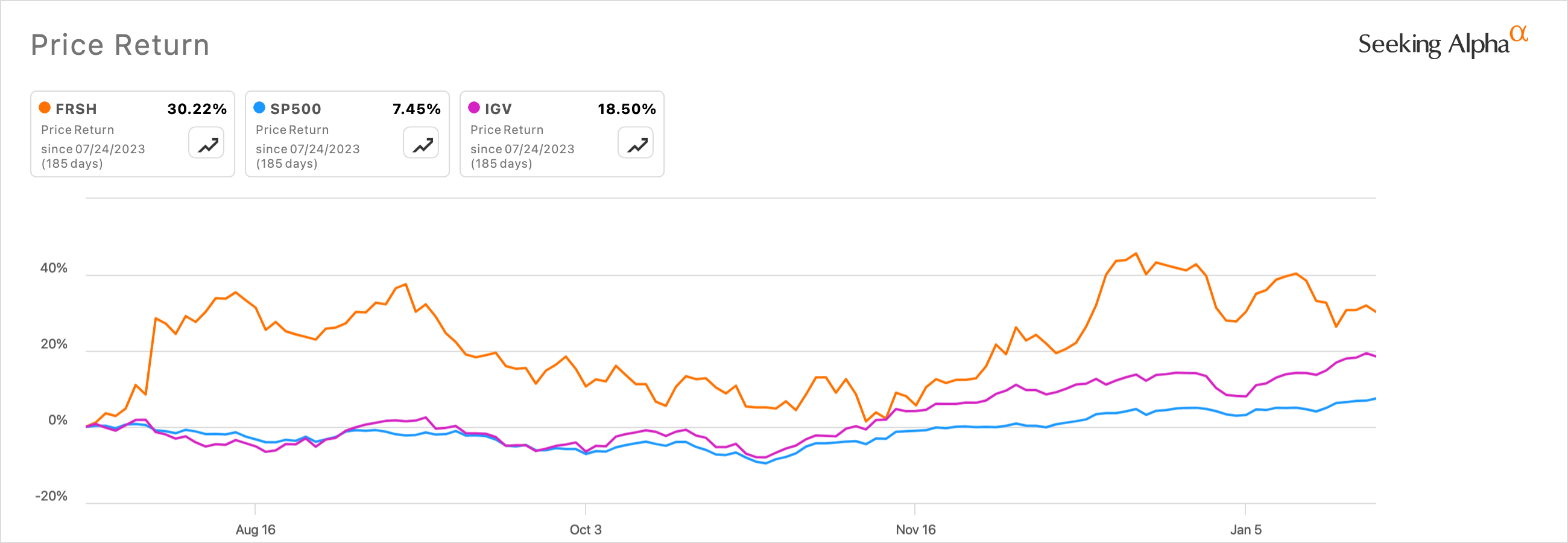

Since the presentation, Freshworks stock has picked up pace to beat the S&P 500 Index (SP500) and the iShares Expanded Tech-Software Sector ETF (IGV) that I use as a benchmark for cloud-based technology stocks.

Seeking Alpha

I believe investors are discounting the value of Freshworks’ market cap as of today relative to the current margin expansion history and future targets of the company.

About Freshworks

Freshworks is a decade-old SaaS company that initially began selling cloud software for the Customer Relationship Management (CRM) space but expanded this offering into the broader Customer Experience (CX) space to include marketing, sales, and automation tools. Over time, the San Mateo, CA-headquartered company leveraged their backend CX platform to further branch out into the higher-margin Information Technology Service Management (ITSM) and Operations Management (ITOM) cloud software markets.

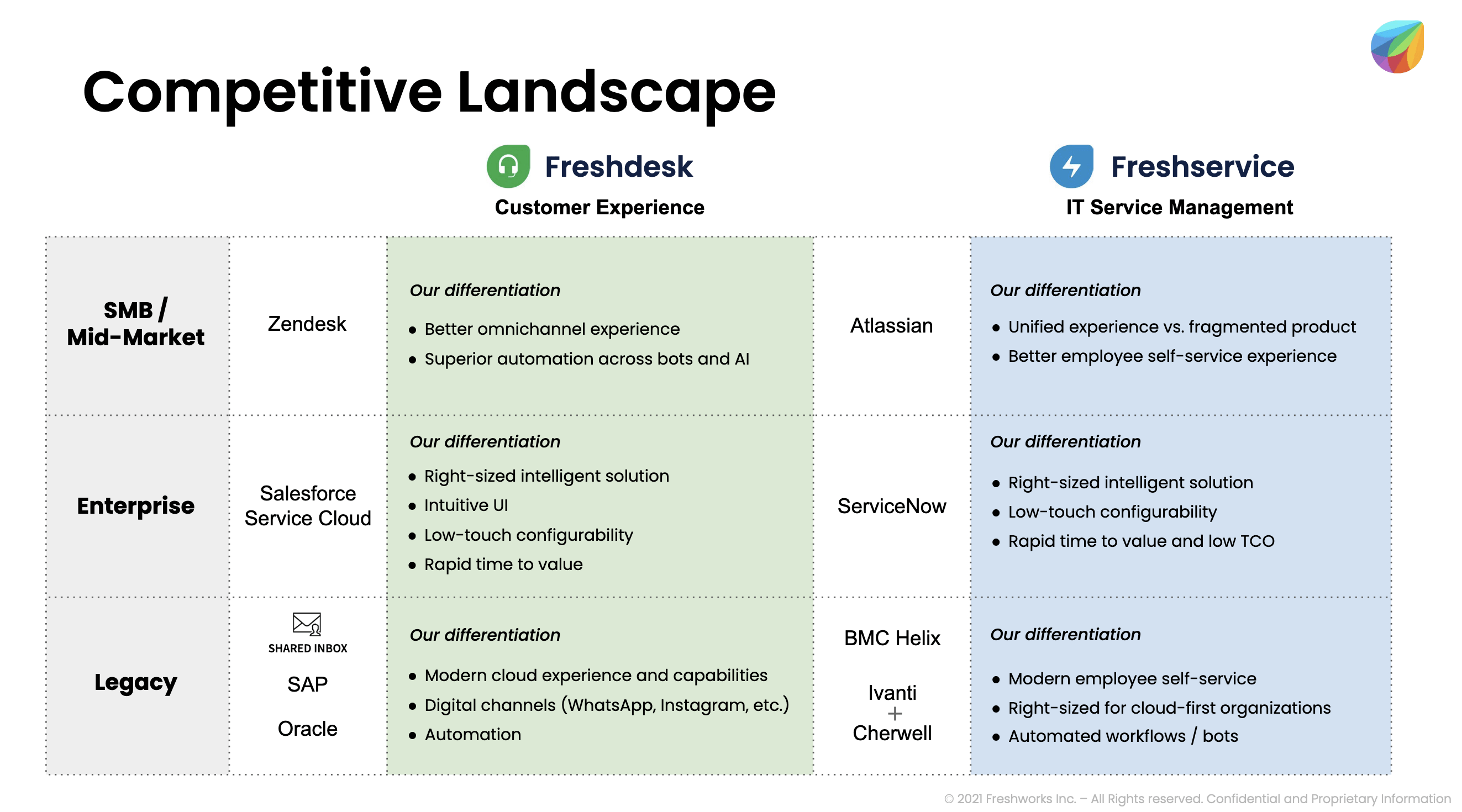

All three cloud software markets are heavily competitive, with some large, successful incumbent companies already existing in each market, which I will cover in the Risks section later. Yet, Freshworks believes its products differentiate from its competitors by appealing to Small & Medium-sized Businesses (SMBs) by shipping products and features that focus on reducing costs and increasing time-to-value for SMBs.

Investor Presentation

Being a SaaS business, metrics such as Annual Recurring Revenue (ARR) and Net Dollar Retention (NDR) will be important in evaluating the growth prospects of the business. After reviewing their most recent FY23-Q3 quarterly filing, I found that the company monitors ARR from customers contributing more than $5,000 in ARR as a percentage of total ARR, so I will specifically review this metric moving forward.

A re-prioritization of growth objectives with a boost of margins

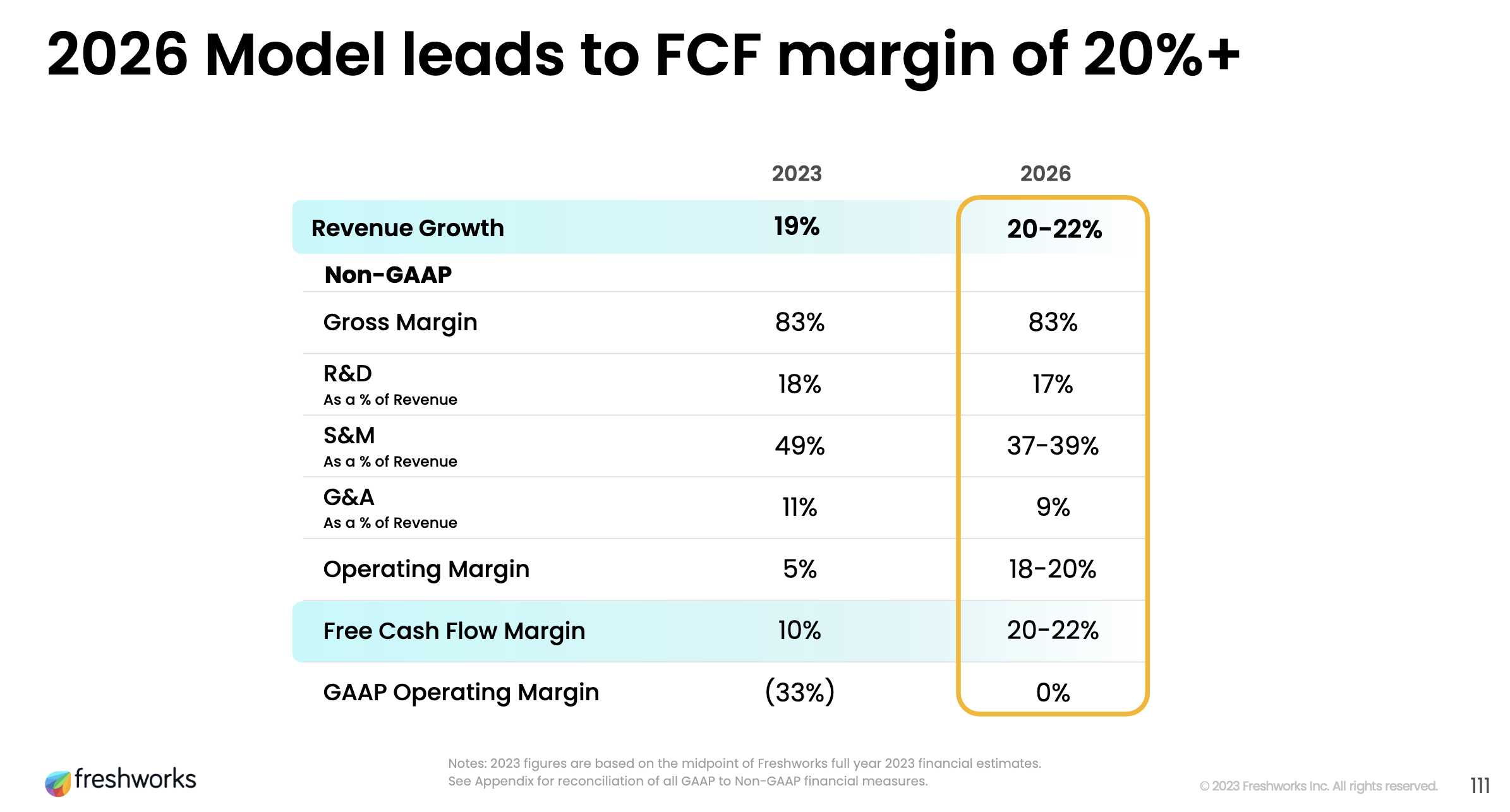

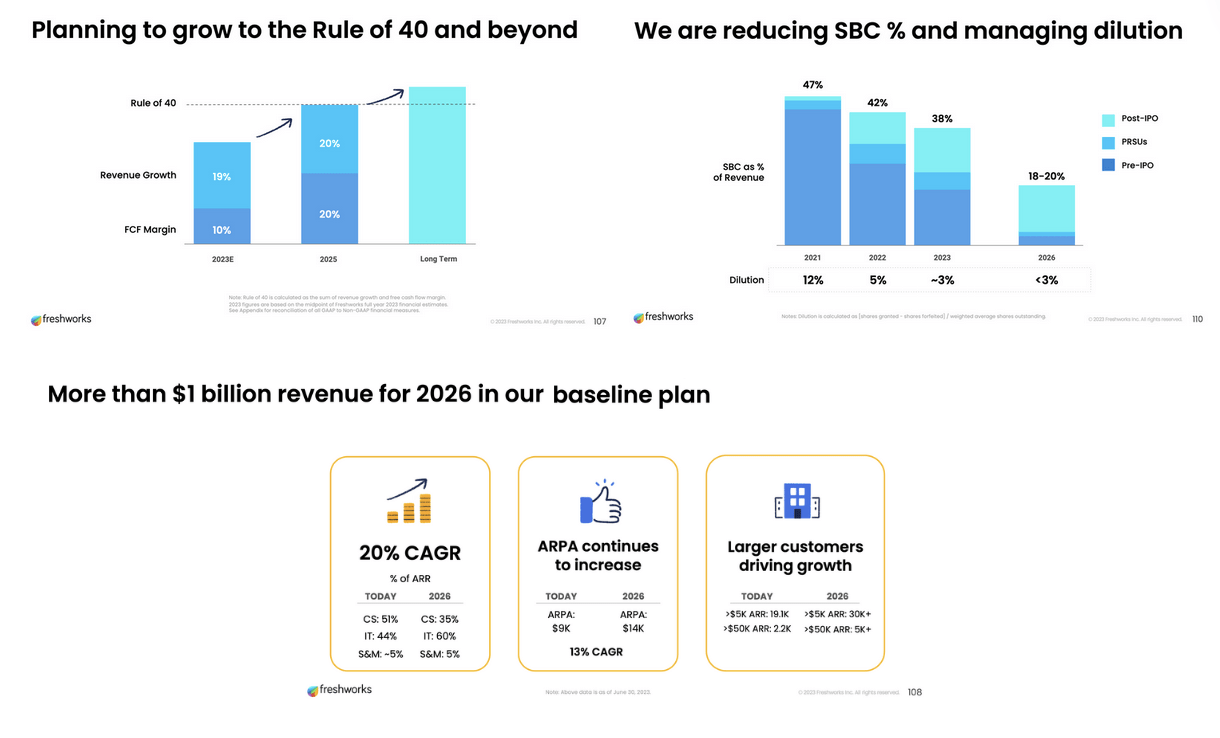

In their Investor Day presentation in July last year, Freshworks laid out its three-year operating plan for prioritizing margins in addition to its growth targets, as shown in the screenshot below.

Investor Day Presentation, August 2023

I will come back to this screenshot later since I will use management’s targets in my valuation model, but for now, I will note that some of the line items, such as Operating Margin and FCF margins, have quite an aggressive ramp up in a span of three years. When reviewing some of the previous management commentary, I see that management has prioritized a few initiatives in their operating strategy, such as renegotiating infrastructure spend with AWS, their primary infrastructure provider, and adopting cost-effective Go-To-Market strategies leading to lower Sales & Marketing spend. In the FY23-Q2 earnings call, management noted:

All this (these initiatives) led to a significant outperformance for non-GAAP operating profit of $11.7 million and non-GAAP operating margin of 8% in Q2. Given the many changes we’ve made over the past year, I’m pleased with the tangible improvements we’re making in our efficiency.

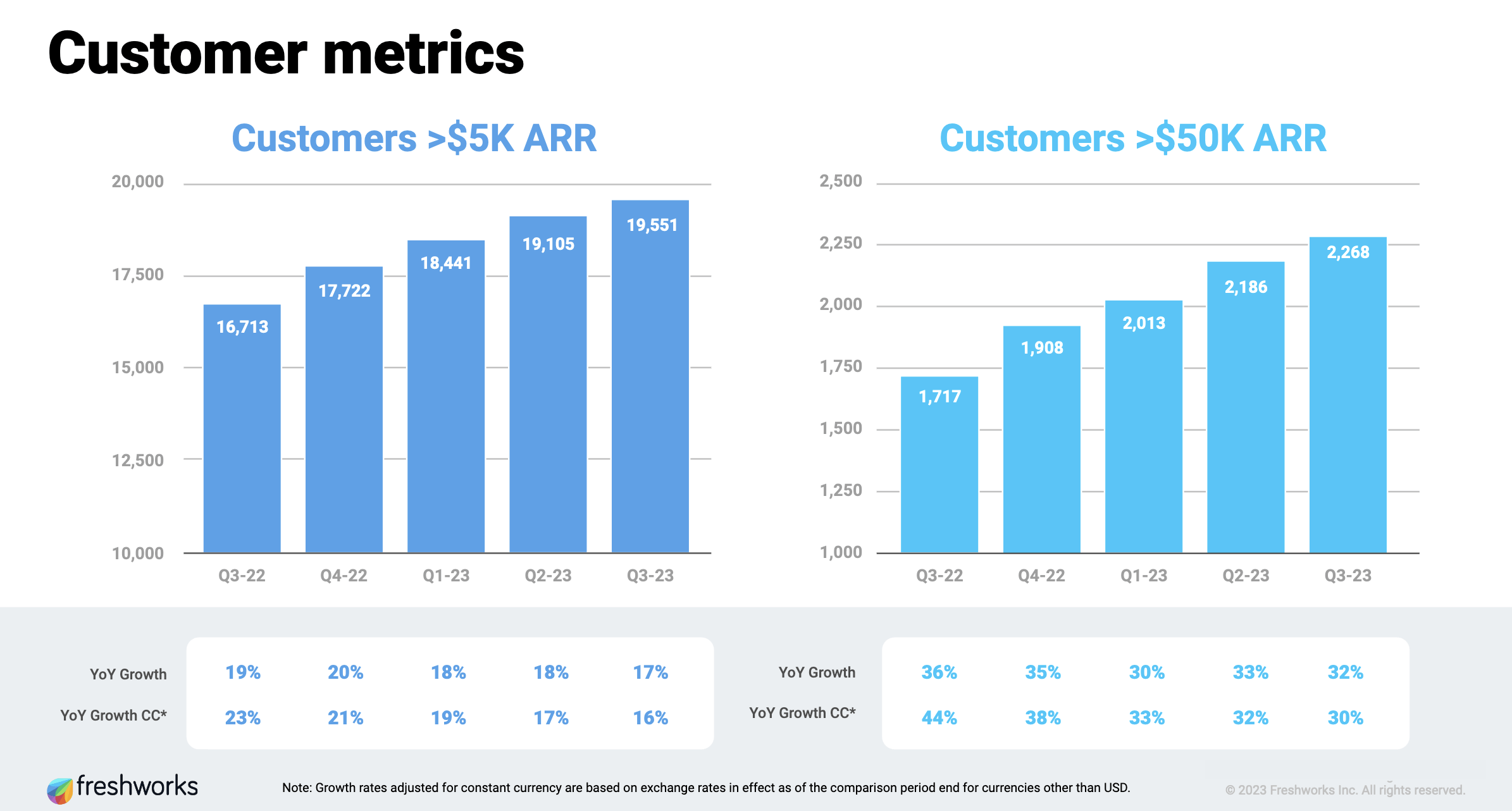

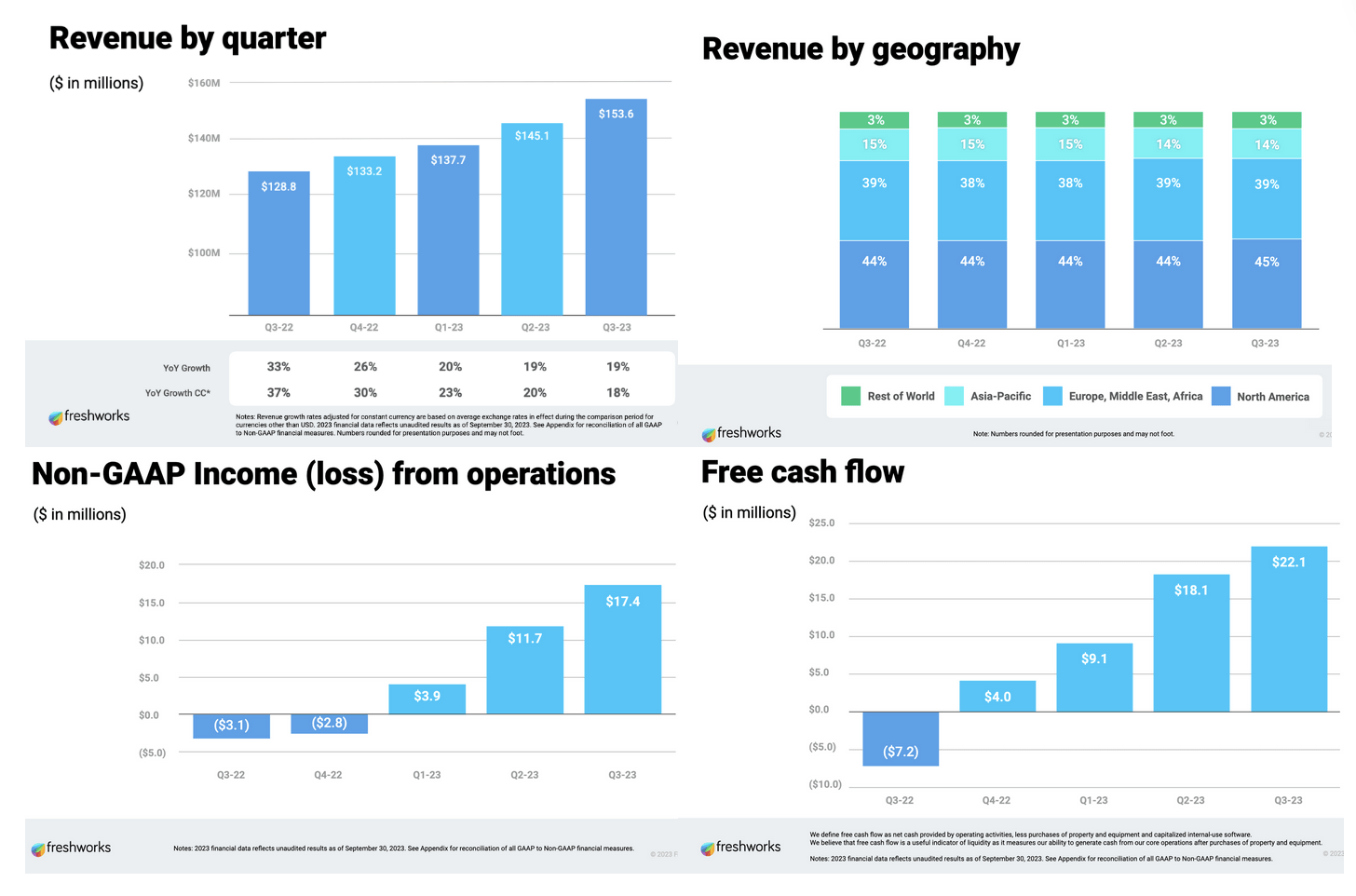

However, something that caught my attention was the company’s pivot to acquire larger customers while also focusing on their existing SMB customers. Take a look at the chart below, which compares growth in Customers >$5K ARR (SMBs) vs. Customers >$50K ARR (Large Enterprises):

FY23 Q3 investor presentation

In the chart above, which can be found in their FY23-Q3 investor presentation (Slide 11), I see that y/y growth from their enterprise customers is growing much faster than that from their SMB customers, growing at +30% growth rates, now for the fifth quarter in a row. I do think this is an accretive pivot for Freshworks so that it can stop leaning completely on SMBs. Moreover, enterprise customers usually have larger budgets, and the acquisition of large customers like enterprises will help Freshworks weather any seasonalities that are associated with smaller customers.

In addition, I believe enterprise customers will also help in boosting adoption of Freshworks’ AI products, such as customer service chatbots, copilots, and insights AI tools built on Freshworks’ Freddy AI platform. Management plans to launch these AI tools as add-ons to the existing subscription plans and offer them to all customers starting this quarter, per management’s commentary in the FY23-Q3 earnings call.

On reviewing their financial metrics, I find it encouraging to see strong growth in Freshworks’ numbers, as can be seen below.

FY23 Q3 investor presentation

I also observed the huge bump in their FY23 Q2 operating income and free cash, which coincides with the increase in the Customers >$50K ARR (Large Enterprises) that was seen in the same FY23 Q2 quarter as we saw earlier.

Valuation Models suggest strong upside

Moving on to estimating the value of Freshworks, I will use some of the targets that management had issued in their long-term guidance that I called out in the earlier section. Management has suggested earlier that they will be using the Rule of 40 business metric that is usually seen in SaaS business companies as Freshworks’ north star goals.

FY23 Q3 investor presentation

Before I move on to the actual valuation, I do want to note that the only debt the company carries is in the form of a long-term operating lease for office spaces. The present value of these operating leases amounts to $30.8 million, but with over 1.2 billion in cash and cash equivalents, I do not see any risk from outstanding debts.

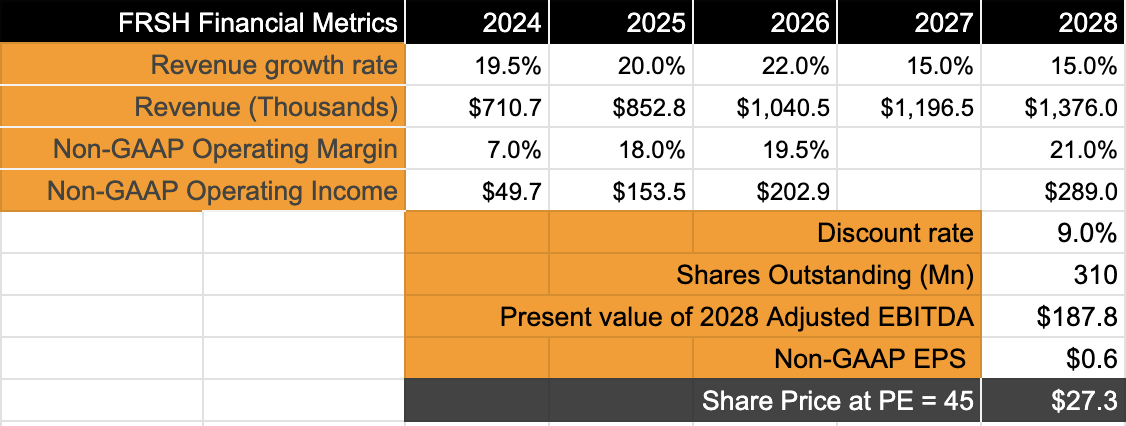

Consensus estimates put Freshworks revenue at 19.4%, which I will take as my base case assumption. Assuming revenue to grow at an average annual pace of 20.5% to $1.04 billion in FY26, I will put my estimates in line with Freshworks’ internal goals to grow to a $1 billion company by FY26. After that, I expect growth to taper off slightly in my base case. I expect operating margins to grow significantly from their 7% projected margins in FY24 to management’s base case of 20% in FY26. After that, I expect continued gains in operating income driven by sustained focus on generating free cash.

Author

Based on these assumptions, I expect operating income to grow at a CAGR of 55%, which is very impressive. These growth rates call for a PE of at least 45 since Freshworks will be growing its income almost 7 times faster than the S&P 500’s average 8% income growth rate. I see at least 23% upside from current levels.

Risks & Other Factors to Consider

I had mentioned earlier about the ITSM, ITOM, and CX markets that Freshworks operates in. These markets are fiercely fought by some large and successful incumbents, such as Salesforce (CRM), HubSpot (HUBS) in the CRM space, ServiceNow (NOW), and Atlassian (TEAM) in the ITSM/ITOM space. Moreover, new entrants like Klaviyo (KVYO) directly compete with Freshworks. While Freshworks focuses on SMBs, its expansion into the larger enterprise market may be difficult due to the success of large companies that already hold leadership positions. But the growing trends in Freshworks’ larger enterprise customers we saw a couple sections earlier along with Freshworks’ product differentiation strategy encourage me.

Another risk that Freshworks faces is the possibility of economic downturns. Since a large part of Freshworks’ user base is still SMB customers, it does face the risk of cyclical trends in its sales cycles in cases of recessions and economic downturns. However, here again, I believe these fears are overstated since the macroeconomic situation is getting better, and economic projections for 2024 are looking up. Moreover, Gartner’s projections for worldwide IT spending to increase by 8% will give Freshworks a further boost.

Conclusion

In summary, the current value of Freshworks does not reflect the projections that its management is guiding based on its FY26 targets. Their enterprise-focused customer acquisition strategy, together with their margin expansion plans, is enough for me to believe that there is more room for the valuation to expand. I rate Freshworks as a strong buy.

Q2 2024 Earnings Call Transcript")