ewg3D

Introduction

United Rentals (NYSE:URI) has been recently added to my watchlist after very interesting research. In fact, some SA readers may know how I like industrials and, in particular, machinery manufacturers. More in detail, I have tried to research and understand how increasing infrastructure spending in the U.S. coupled with manufacturing reshoring will impact those companies involved in construction equipment.

United Rentals stands out as one of the most interesting picks. Since the company recently reported its Q4 and FY23 earnings, it is now the right time to go over it and explain why I am keeping a close eye on it to add it to my portfolio.

The Company

United Rentals is the largest equipment rental company in the world, with a primary business in the U.S. and Canada, but with some presence also in Europe, Australia, and New Zealand.

We can see below, it holds 15% of the total market share, which is a big achievement in a fragmented market. With a fleet size covering 4,800 equipment categories and valued at almost $21 billion, United Rentals has the size and the scale to outcompete many small players. Therefore, part of its growth strategy is to pursue strategic acquisitions to expand its core equipment rental business.

URI Q4 2023 Earnings Presentation

In 2023, the company reported $14.3 billion in total revenue (+23% YoY). Its EBITDA margin deserves consideration: 47.8%.

The company considers its target accounts primarily large construction and industrial customers, as well as select local contractors.

As we can see from the graph below, United Rentals serves three principal end markets for equipment rental in North America:

- Industrial and other non-construction, which make up 49% of rental revenue

- Non-residential construction; accounting for 46% of its rental revenue

- Residential construction, which includes remodeling, generating 5% of rental revenue

URI Q4 2023 Earnings Presentation

United Rentals has two reportable segments: general rentals and specialty. As the company explains in its annual reports, the former includes “the rental of “construction, aerial and industrial equipment, general tools and light equipment, and related services and activities”. The latter “includes the rental of specialty construction products”.

The company has some competitive advantages:

- A large and diversified rental fleet that enables it to serve large customers. This is important because the company can address and serve customers whose needs for equipment are big and can spend significant amounts to fund these needs.

- Significant Purchasing Power. United Rentals can purchase large amounts of equipment, contractor supplies, and other items. As a result, it can negotiate favorable pricing with its suppliers. This enables it to outcompete on price many smaller peers.

- National Account Program. The company has the power to pay a big sales force dedicated to establishing and expanding relationships with large companies. The company considers “national accounts” those customers with potential annual equipment rental spend of at least $500,000. With key accounts, the company has a policy of establishing a single point of contact to provide customer service management that is more consistent and satisfactory.

- Operating Efficiencies. The company’s business model has one of its main pillars in equipment sharing among its branches. This means that each branch within a business region can access equipment located elsewhere in the same region. The outcome can be easily understood: equipment utilization increases because the idle equipment at one branch can immediately be rented through other branches. In addition, this practice helps the company save on capital spending

- Strong Brand Recognition. The company is by now known as the largest equipment rental company in the world. This helps it attract new customers and build customer loyalty.

- Geographic and Customer Diversity. Given its size, the company is well-ramified and can therefore benefit from very different economic situations and needs.

Moreover, there are two macro-trends which stand out as true tailwinds:

-

There is a secular shift toward renting equipment because renting is accounted for as an operating expense without impacting the balance sheet and making capex explode.

- The return of manufacturing in North America goes along with investments in many related infrastructures coupled with new factories and facilities. North America will be full of construction sites.

This is confirmed by the graphs shown below: the U.S. equipment rental industry has sharply outpaced the total non-residential activity. The market size grows steadily and in 25 years it has moved up from around $15 billion to more than $55 billion.

URI Q4 2023 Earnings Presentation

The company’s financial strategy to profit from these secular trends is quite easy to understand. It focuses on improving the profitability of its core equipment rental business. This is done through “revenue growth, margin expansion, and operational efficiencies”, as we can read in the last annual report available.

Until 2023, the company paid no dividends, even though it was able to generate billions in free cash flow. But last year the company changed its policy and started rewarding generously its shareholders through buybacks and dividends. Just in 2023, the company returned $1.5 billion (3.5% of the current market cap) under these two ways. In 2024, the company intends to complete $1.5 billion of share repurchases. Recently, the company increased its quarterly payment by 10% to $1.63 per share, or $6.52 per share annualized. In total, United Rentals should return over $1.9 billion to shareholders this year, equating to almost $30 per share, for a total yield of 5% based on the current share price.

Financials

United Rentals has been able to steadily grow its top line together with its EBITDA and its EPS, as we can see from the three graphs shown below. The pace of this growth is quite quick: we are talking about a 5-year CAGR above 12%.

URI Q4 2023 Earnings Presentation

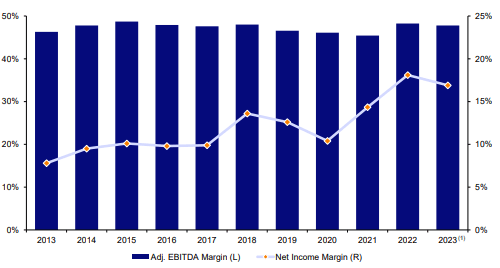

Moreover, while growing its revenue, United Rentals shows to be well-managed as its net income margin has grown steadily even in case of declining EBITDA margin, as we can see from the graph below. Currently, the company reports a net income margin above 15%, which is high considering we are talking about a business linked to machinery manufacturing.

URI Q4 2023 Earnings Presentation

If we look at its balance sheet, we see a progressive improvement in its leverage ratio, which is now below 2. This makes me think United Rental’s will soon achieve an investment-grade rating which will attract more capital.

URI Q4 2023 Earnings Presentation

Risks

A risk the company faces is that its services and products are sensitive to the exploration activity of oil and natural gas companies. We know this can be a very volatile market, depending also on government policies and commodity price volatility. However, given the growing need not only for energy but for minerals and rare earth metals, we can expect mining activity to go on and perhaps shift from oil to these other two fields.

FY 2023 Results

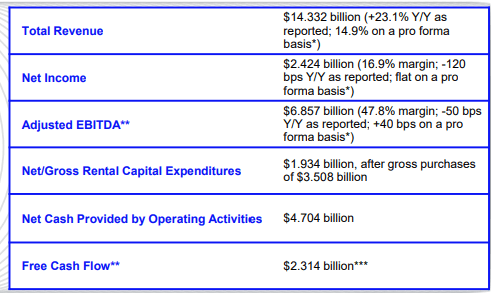

Since the company recently reported its Q4 earnings, it also gave us an overview of what happened during the last fiscal year. As we have already said earlier, United Rentals reported $14.3 billion in revenue. Its net income grew 16.9% YoY to $2.4 billion. Free cash flow generation was a very good $2.3 billion.

URI Q4 2023 Earnings Presentation

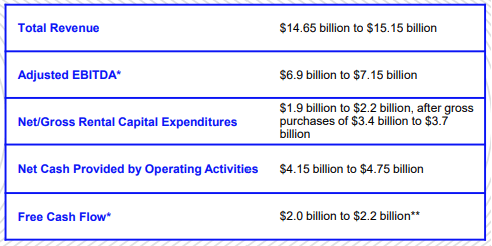

At the same time, the company gave its outlook for 2024. We should not expect double-digit growth because total revenue should be between $14.6 billion to $15.15 billion. EBITDA margin should stay above 47% while FCF should come in above $2 billion. After all, the company’s profitability grade is an A+.

URI Q4 2023 Earnings Presentation

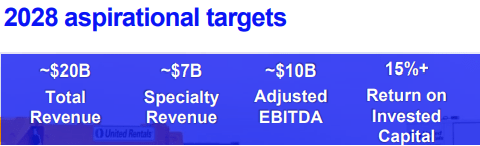

This positions the company well on track to achieve its 2028 goals: $20 billion in total revenue with an adj. EBITDA at a 50% margin and a 15%+ ROIC.

URI Q4 2023 Earnings Presentation

Valuation and Conclusion

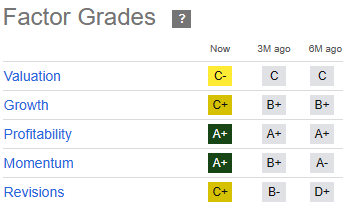

If we look at Seeking Alpha’s Quant Ratings, we see an interesting situation. The company has outstanding grades for its profitability and its momentum. Being a long-term investor, I consider much more important the first grade rather than the second.

Seeking Alpha

But I also consider a C+ quite good for the company’s growth, considering the industry it operates in. And, even more interestingly, although the company trades at ATHs, its valuation grade is still reasonable and is a C-. However, we need to consider that the stock jumped up around 13% after earnings and this is not yet considered in these grades.

If we look more in-depth at the valuation, we find reasonable multiples: a fwd PE of 16.6; a fwd EV/EBITDA of 8, a fwd P/FCF of 9. All of these multiples show that the stock is trading at a discount to the general market. But, I ask myself, does a business so well-run need to trade at a discount rather than a premium?

My answer is no and my DCF goes in this direction too. If I plug in it the latest financials available, the result is clear: the company’s fair value is around $763 a share.

Author

This is why I actually rate the stock as a buy, even though I don’t often do this when we are at ATHs. However, the bull case and the company’s fundamentals seem to be so strong making me confident this stock will move along with the success of its underlying business.

Q2 2024 Earnings Call Transcript")