Hispanolistic/E+ via Getty Images

Reorganizing an Industry

A recent article in Forbes sent us on a search for an investment opportunity in outpatient diagnostic imaging services. We are focused on RadNet, Inc (NASDAQ:RDNT) as a long-term Buy potential opportunity.

RadNet’s core services include magnetic resonance imaging, computed tomography, positron emission tomography, nuclear medicine, mammography, ultrasound, diagnostic radiology, fluoroscopy, and multi-modality diagnostic imaging. RadNet also develops and sells diagnostic imaging software for digital imaging and picture archiving.

It is a leader in offering less expensive, more accessible, out-of-hospital diagnostic imaging services while building a dedicated Big Data collection as a profit center underpinned by AI-based software development. RadNet’s profitability, revenue growth, and momentum get high marks per Seeking Alpha’s Factor Grades. According to Forbes,

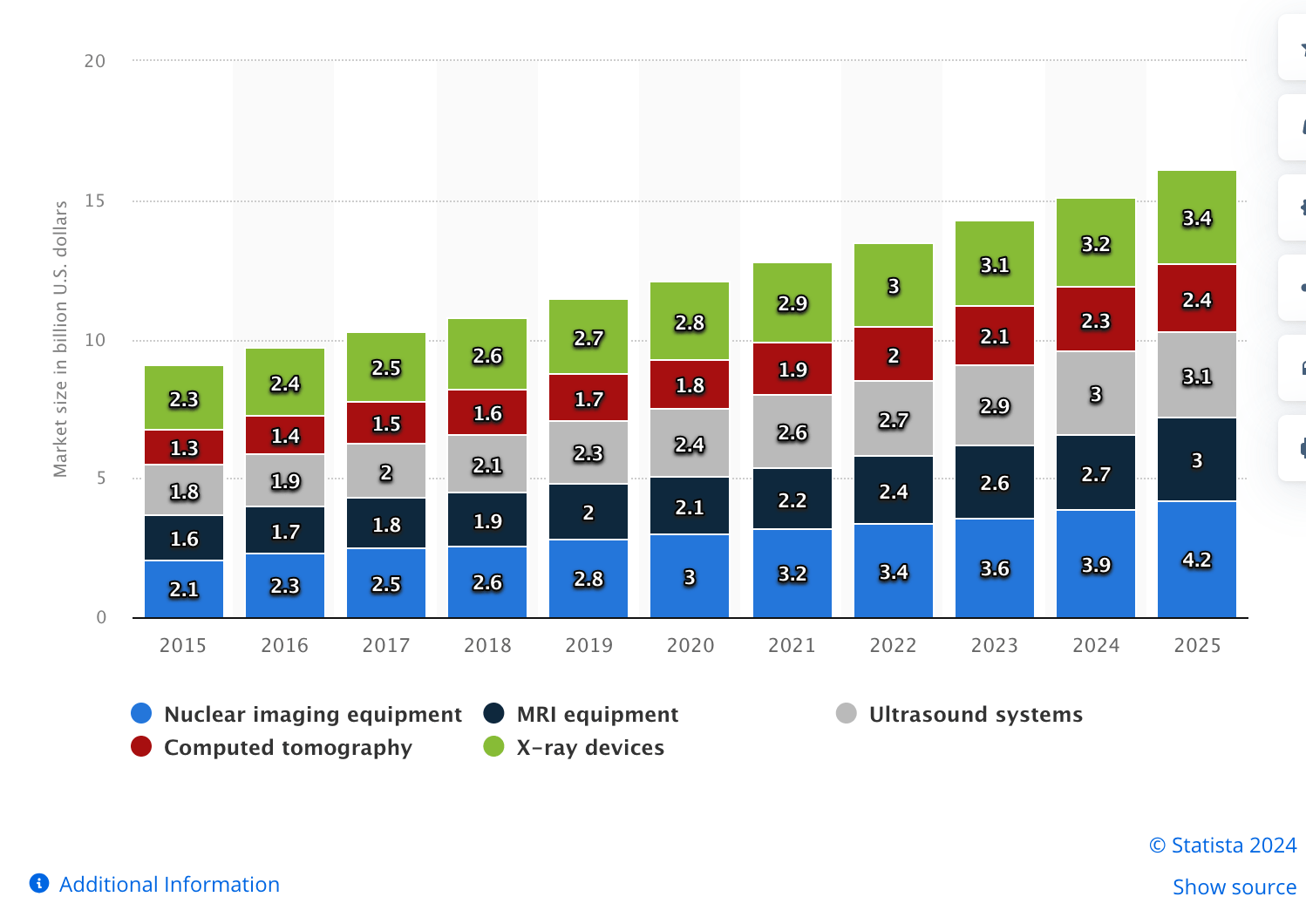

The amount of data generated in healthcare is scaling at a rapid rate of 47% per year. So, how do you manage all that data and use it to improve patient care? Healthcare organizations today are being challenged by a massive amount of data, 90% of which comes from medical imaging. As medical imaging demand increases, so will the number of scans to manage, which can often be large files upward of a few gigabytes.

AI revenue at RadNet tripled in Q3 ’23 over the same quarter the year before and by +21% from Q2 ’23 through Q3 ’23. All this positivity is enhanced knowing it comes from “roughly the same number of center offerings” for breast cancer detection or evidence-based clinical documentation service. In addition to the value created by data collection, AI drives efficiency thus cost savings in business services including the processing of patient scheduling, insurance verification, and revenue cycle functions. The CEO forecasts “EBCD in Southern California… will be fully deployed in all centers by the end of the first quarter of 2024.”

RadNet is on the cutting edge of a burgeoning healthcare prevention and early intervention movement using diagnostic imaging services.

Diagnostic Imaging Growth (Statista)

Expansion Plans

RadNet is expanding diagnostic imaging services from just housed in expensive hospitals into more accessible, lower-cost, off-site facilities; the data these devices collect are being sold as Big Data to university schools of public health, medical care planning agencies, and insurance companies.

RadNet is not forsaking its hospital-based imaging services relationships. RadNet and Cedars-Sinai Medical System in Southern California are in new joint ventures resulting in 7 to 10 additional diagnostic imaging centers. In our experience with working to build maternal child health care centers out of the office of the U. S. Surgeon General, off-site centers can feed patients into hospitals and physicians for better care with early detection and intervention. Aligning with a big-name hospital adds gravitas to RadNet’s reputation and brand.

On January 24, ’24, Seeking Alpha reported that RadNet and Arizona Diagnostic Radiology Group entered into a joint venture to acquire seven outpatient imaging centers in Phoenix Arizona from Evernorth Care Group. In December 2023, RadNet announced the launch of MammogramNow. It is a pilot screening mammography service that debuted in a big-box Supercenter in Milford, Delaware, about 8 weeks ago. The service uses the company’s DeepHealth® technology. Placed in a retail environment, RadNet hopes to increase accessibility and, potentially, early detection of cancer.

RadNet is in a position to lower overhead costs of operations for the burgeoning diagnostic imaging business. We like that management is sticking to the knitting of its business plan; it will also, we conclude, stimulate more testing by reducing costs to insurance companies and lower out-of-pocket expenses for patients increasing the pool of potential clients. The last 6 articles analyzing RadNet on S A extend back to 2021. They and 5 Wall Street analysts as reported on S A covering RadNet are all bullish. We are bullish too at this time.

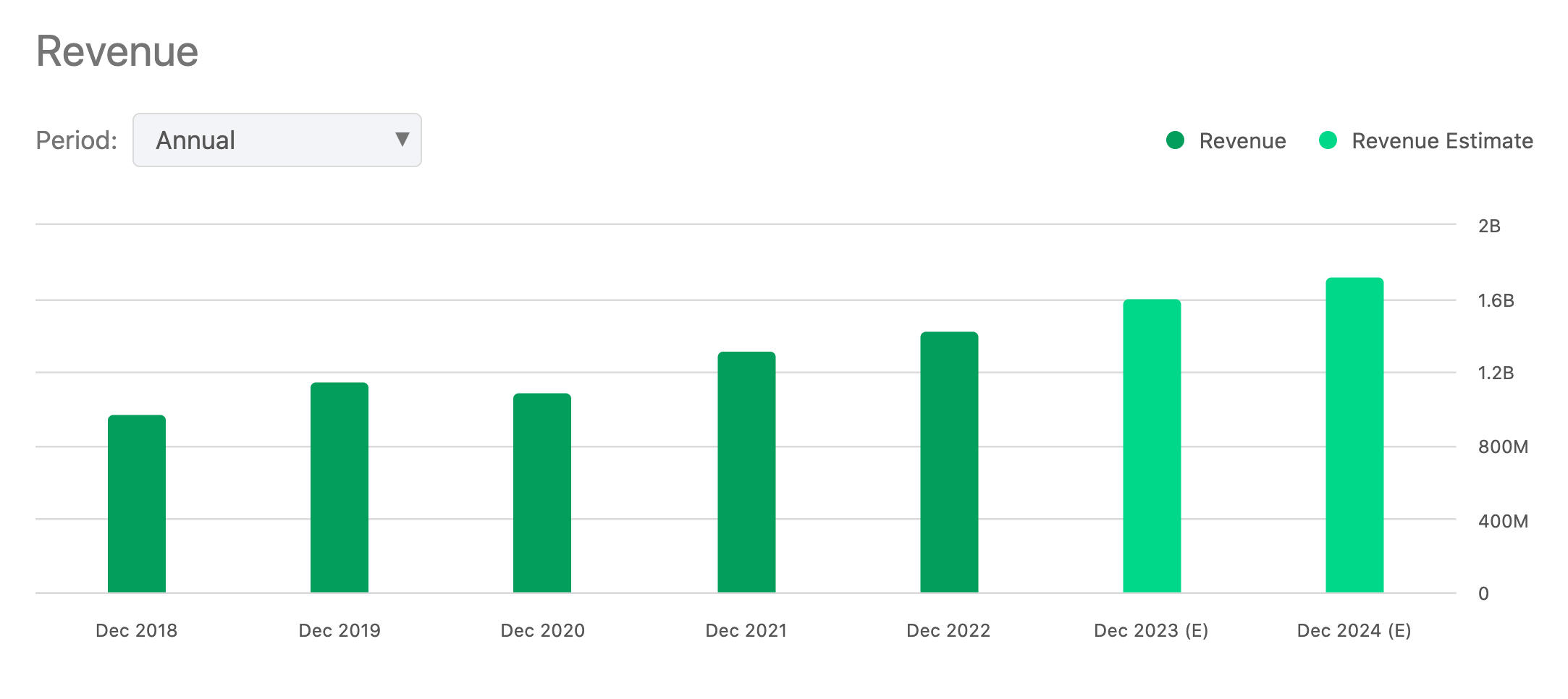

Except for 2020 when social distancing and extra care to avoid medical setting was the rule, RadNet revenue has annually increased. Indicators are it will continue to rise from organic growth, partnerships, and, in part, because of the management’s M&A activity. According to Mergr.com, RadNet acquired 9 companies, 4 in the last 5 years. RadNet’s largest acquisition to date was in 2015 when it acquired Diagnostic Imaging Group for $57M. 56% of the companies acquired operate in healthcare and 34% in IT proving the plan is to expand and sell Big Data, most likely to university schools of public health, medical care planning agencies, and insurance companies.

Annual Revenue (Seeking Alpha)

Risks

We see risks to be weighed and regularly monitored. First, the share price has been on a tear this year climbing from $16.29 on November 14, 2022, to a 52-week high of +$39 per share. The share price is +184% over 5 years, +6.3% YTD, and ~+80% over the last 12 months. We believe the share price has the potential momentum to move into the low-$40s over the next two quarters but the price can drop on profit taking or by missing analysts’ estimates for Q4 and FY ’23. Short interest seems a safe 3.77% with over 5 days to cover but the levered/unlevered Beta of RadNet stands today at 0.95 making it susceptible to the vagaries of the stock market trends.

While we are currently bullish on the market pre-election, inflation remains a headwind, and the federal budget impasse and deficit might slow down federal spending on healthcare. Others are concerned, too, for 2024. Moreover, Republicans are eyeing deep cuts to Medicare which accounts for 23% of RadNet’s billings.

In June ’23, there were losses on noncash interest rate swaps to deleverage the debt-to-equity balance and accelerate growth. The AI segment is likely to continue losing money and risk is heightened by the company’s substantial debt. By late October, the share price was down to about $25.42.

Share Price Moves (Seeking Alpha)

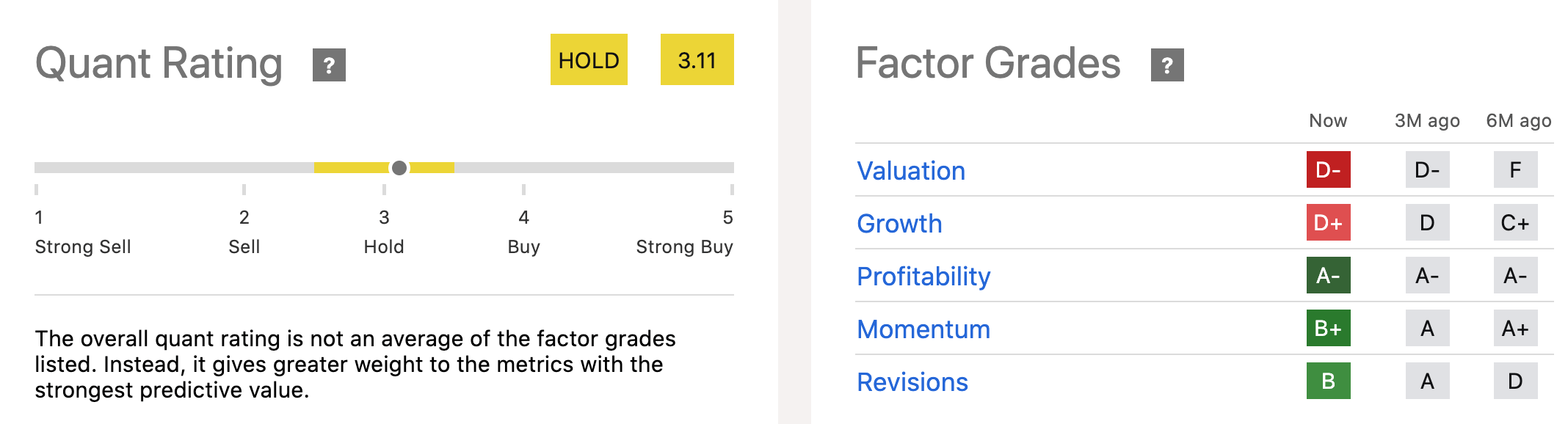

Seeking Alpha gives RadNet an F for its valuation. The Forward Non-GAAP PE ratio is a whopping +87. On January 23, ’24 SA’s Quant raised RadNet’s Valuation from F to D- and the Quant Rating began creeping to the buy-side of the rating bar.

Quant Rating & Factor Grades (Seeking Alpha)

Risks are obvious when investors consider RadNet’s valuation metrics in comparison to the healthcare sector median metrics. Gross profit ticked up but remains at a disappointing 21.23% compared to the sector median of over 57%. Another analyst has RadNet’s gross margin at 15.01% which is worse than 91% of 216 other firms.

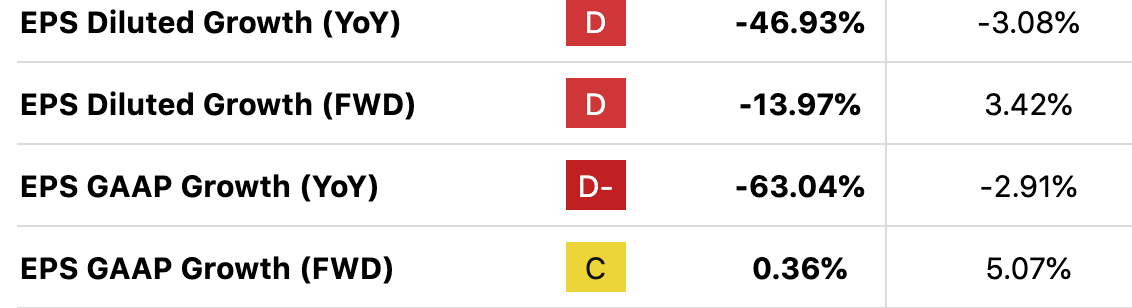

EV to Sales, Price to Sales, and Price to Cash Flow are exceptions to poor valuation and growth metric comparisons to the sector medians. All three rate in the B range. EPS Growth compared to the sector median concerns us the most and future misses leave investors particularly vulnerable

EPS Growth Comparisons (Seeking Alpha)

One more downside is the total debt which is higher Y/Y since 2018. The total debt on the balance sheet as of September 2023 hit $1.53B. It “is the sum of all current and non-current debts.” On the company’s recent 10-Q report, as of September 30,’23, RadNet holds $337.88M in cash and equivalents and $167.7M in accounts receivables.

Tailwinds

Earnings appear to be improving as revenue grows. We hold with Y/Y EPS estimated increases of 117% in FY ’23 over ’22 and 32% in FY ’24. A lot depends on government budgeting for diagnostic imaging and greater use of AI software to reduce labor costs.

Some insider selling trading between May and December ’23 took place but in December insiders bought again in the $34 range at last report. A record number of 22 hedge funds owned RadNet shares buying in when the stock was selling in the $20s. Six sold out by the end of Q3 ’23 but more funds still own shares going into Q4 ’23 than any time over the last 18 months. 12% of the outstanding shares are owned by corporate insiders, 80% by institutions, and 8.3% by the public.

A report on Global Clinical Diagnostics Market 2024 Report, History and Forecast 2019-2031, Breakdown Data by Manufacturers, Key Regions, Types and Application, concludes the movement to bring diagnostic imaging to the people has tremendous potential. Worldwide, clinical diagnostic data see North America’s market growing at an annual CAGR rate of 5.5%. Europe’s diagnostic imaging market will grow at a CAGR of 6.6%. Unfortunately, or through better diagnosis capabilities, rates of cancers are rising for people under 50 creating greater demand for services RadNet offers. Out-of-hospital cost savings are estimated to reach 62%.

Medical Economics claims, in a January 2024 newsletter, that “the majority of imaging procedures can be performed in most outpatient facilities… while enhancing the patient experience.” RadNet’s management assured shareholders in their last talk that the company’s potential growth will be enhanced as it moves into underserved communities and increases Cloud and AI usage. Already

Over 500 cancers have been diagnosed that otherwise would have gone undetected while at the same time, callback rates have been significantly lower and radiologist productivity and accuracy has been increased, an immense amount of data has been collected, which we will be sharing with payers in support of eventually receiving third-party reimbursement for this service.”

We foresee RadNet and other diagnostic imaging companies having another pool of more than 102K self-designated general and family practitioners who can make use of these devices and services. The NIH foresees general practitioners having “access to diagnostic imaging provides an avenue to timelier diagnosis, a consequent reduction in referrals to hospital-based specialists and emergency departments, and improved quality of patient care and disease outcomes.”

The company’s ~$157M in annual operating cash flow, substantial current assets, and an environment of interest rate stabilization mitigate substantial risk over company debt.

Takeaway

Since 2021, six S A articles from analysts assess the stock as a Buy opportunity and we make it 7 in a row, especially on any dips in the share price. Diagnostic imaging is a growth industry in the expanding healthcare industry. RadNet provides an essential service. But RadNet has some heavy-hitter competition that can work to investors’ advantage; M&A activity is rebounding, even set to rally, in our opinion, and that might be a factor in the minds of shareholders and investors.

Q2 2024 Earnings Call Transcript")