tadamichi

The Royce Value Trust (NYSE:RVT) is a small-cap-focused CEF that invests in companies with high ROIC and strong fundamentals. According to RVT’s policy, there is also a valuation component, which guides the final investment decision-making (i.e., there has to be a discount to the underlying value).

In essence, we can classify RVT as a small-cap and value-focused Fund for which quality such as strong balance sheets and solid debt coverage metrics play also an important role in the overall asset allocation strategy.

Let’s now explore RVT’s structure and portfolio in a bit more detail and then form an opinion as to whether the Fund is an attractive investment case.

Thesis

Currently, RVT carries ~ $1.8 billion in AuM, which is quite significant in the context of average small-cap actively managed funds. Thanks to the scale, RVT is also rather diversified with 393 companies in the portfolio that are nicely spread across different industries.

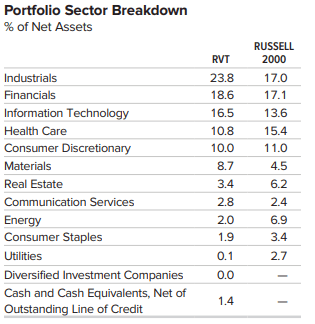

Royce Value Trust Factsheet

If we compare RVT to Russell 2000, we will notice notable differences in the sector allocations, where RVT has assumed a higher skew towards industrials, technology, and materials. Conversely, RVT has deemphasized health care, real estate, and energy.

It obviously depends on the underlying securities, but from this, we could conclude that RVT has minimized investments in very interest rate sensitive areas and instead allocated into positions that are inherently more stable.

For example, the fact that there is a much lower bias toward small-cap real estate could be viewed as a step in a more conservative direction considering the current backdrop of struggling commercial real estate stock.

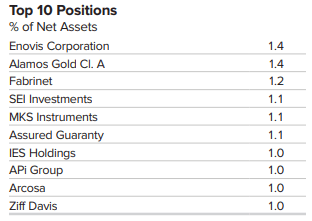

Furthermore, the situation in the Top 10 positions looks safe and well-diversified, where these largest names (see below) account for only ~11% of the total net asset exposure.

Royce Value Trust Factsheet

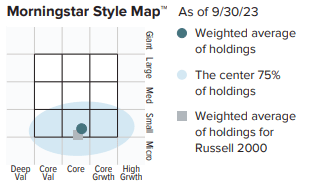

Now, if we peel back the onion a bit and assess the characteristics of the underlying positions, we will notice strong similarities with the Russell 2000.

Royce Value Trust Factsheet

In other words, according to Morningstar classification, most holdings concentrate in the “core” area, which means that RVT does not introduce a tilt either on the small-cap growth or value stocks. This is almost perfectly in line with the Russell 2000.

Royce Value Trust Factsheet

The portfolio company characteristics confirm this. As of now, RVT’s investments have a P/E ratio of 16x and a P/B ratio of 2.1x, which is neither high nor extremely low. Granted, in the context of the S&P 500 and more popular growth stocks, these ratios are very low and seemingly attractive (as it is usually the case).

Finally, when it comes to the fee level and structure, RVT is nicely positioned for investors. For instance, the annualized operating cost of the Fund (which includes the advisory fee) was 1.05% for 2023. This is low given the nature of the CEF – actively managed in small-cap space.

Then there is an interesting nuance stemming from the performance fee perspective, which states that RVT will charge no fees for months in which the performance over the trailing 36-month period lands at negative territory. It is very unique and “unit holder friendly” to say the least.

In a nutshell, RVT is a well-structured CEF that is sufficiently diversified with relatively minor, but positive deviations from the Russell 2000.

In my opinion, RVT provides an interesting opportunity for value-focused investors, who prefer dividend income over capital appreciation.

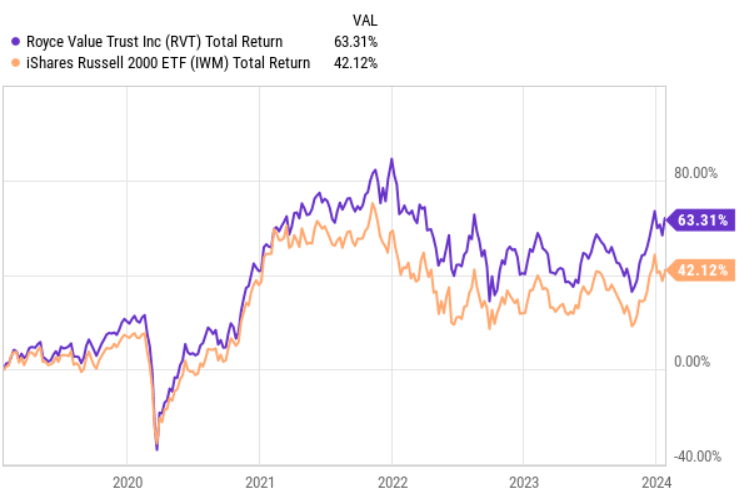

Historically, RVT has outperformed the Russell 2000 in a fairly consistent manner. Obviously, the correlation has been strong, but RVT has managed to deliver a slight alpha relative to the index.

YCharts

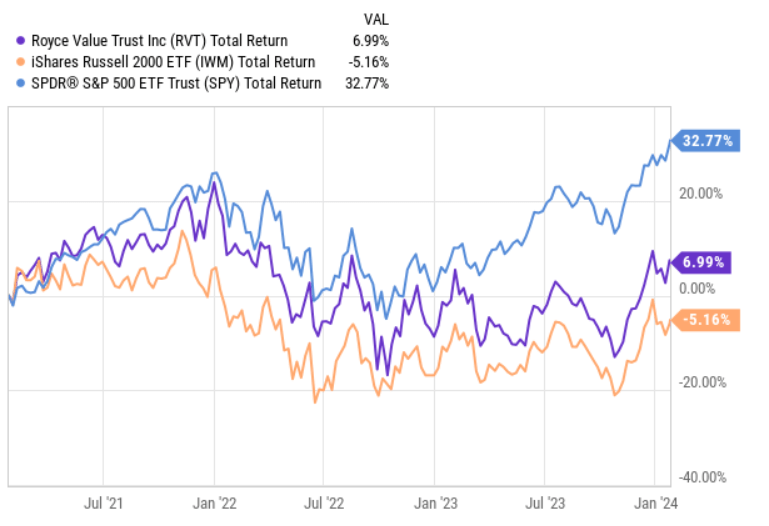

Even in the trailing 3-year period, RVT has exceeded Russell 2000, while maintaining tight correlation levels (even with the S&P 500).

However, since early 2023, the S&P 500 has positively diverged from the small-cap space (including RVT), registering alpha at ~ 26%, which creates an interesting entry point in RVT.

YCharts

Now, while RVT embodies rather similar risk and return factors as the Russell 2000, from the yield perspective there is a significant difference. Namely, RVT currently offers a yield of ~8%, which is about ~6.5% above what the index provides. The key reason for this lies not so much in the industry mix, but more in the security list, where RVT has clearly opted for higher-yielding names.

The bottom line

All in all, RVT is a vehicle that suits well for small-cap and value-focused investors, who also prefer high dividend income.

Currently, it seems that there is an attractive opportunity to enter RVT given the recent divergence from the S&P 500 and relatively high dividend yield of 8%, which in turn could provide acceptable streams of income, while investors, who believe in small-cap and value premium get awarded.

Q2 2024 Earnings Call Transcript")