JHVEPhoto

Introduction

The Lonza Group (OTCPK:LZAGF) is a chemical and biotech company providing high quality ingredients to the pharmaceutical industry, where it has been building and maintaining long-term relationships with its customer base. It recently started an aggressive expansion program in the CDMO space, where it acts as a third party manufacturer of drugs or components for drugs. Lonza continues to invest in growth and has outlined an ambitious plan to increase its revenue by a double-digit number between now and 2028.

Yahoo Finance

Lonza is a Swiss company and has its main listing in Switzerland, where it’s trading with LONN as its ticker symbol. The average daily volume in Switzerland is roughly 260,000 shares per day. This represents a monetary value of 110M CHF per day. I will use the Swiss Franc as base currency throughout this article.

A look at the capital markets day projections

Capital Markets Days usually are very interesting as companies go out their way to explain their mid-term guidance to the shareholder base. While most companies provide short-term guidance on an annual basis, it’s sometimes better to have a better understanding of what a company is envisaging a few years out. Lonza Group held its capital markets day in the fourth quarter of last year, and as it provided updated guidance for 2024-2028, it makes sense to have a closer look to see if I need to update my expectations.

And Lonza’s growth projections didn’t disappoint me; they did disappoint the market as Lonza saw its share price drop by about 15% when it published its long-term projections, but the company’s guidance is actually pretty robust.

Lonza expects to increase its revenue by approximately 11%-13% per year on a constant exchange rate basis, while the EBITDA margin should increase to 32%-34%. This basically means Lonza expects to generate higher revenues and higher margins, as the core EBITDA margin was just 30% in the first half of 2023 and 29.8% in 2023.

Lonza Investor Relations

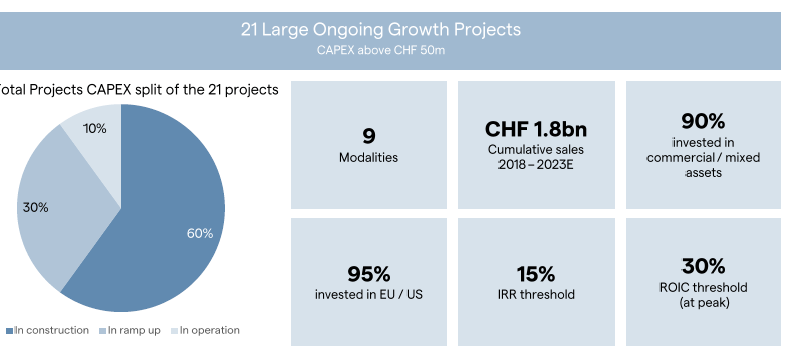

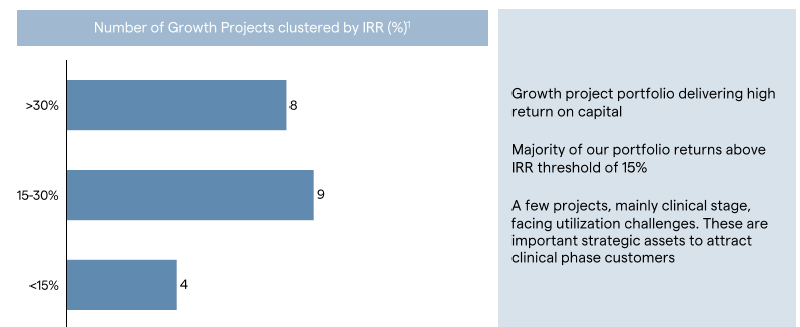

And as the EBITDA will very likely increase, the company will keep the leverage limited to just 1.5-2 times the core EBITDA. That’s just an anticipated maximum, as the current debt ratio is just 0.6 times the core EBITDA as of the end of 2023. The growth will come from the 21 projects that are currently either already contributing to the total result or are under development. Lonza has an internal target that the projects it embarks on should have an IRR of 15%. And indeed, as you can see below, the vast majority of the projects indeed does meet that threshold with eight projects that should generate an IRR of in excess of 30%.

Lonza Investor Relations

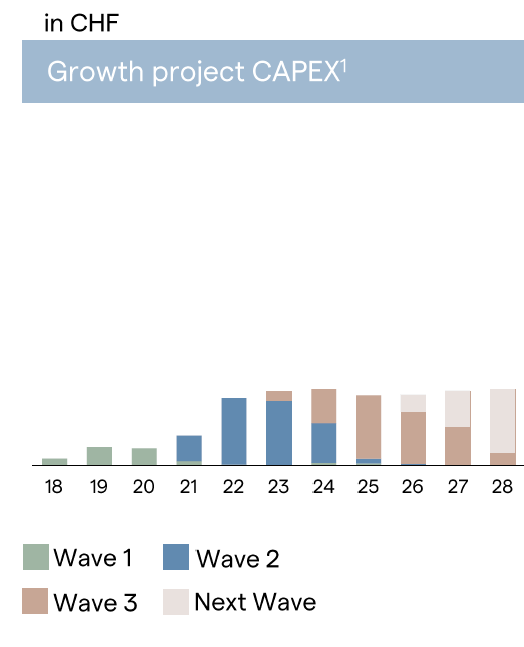

The heavy lifting will be done in 2024 and 2025. As you can see below, the total growth capex decreases from 2026 on, but I am sure the company will find new growth projects by then.

Lonza Investor Relations

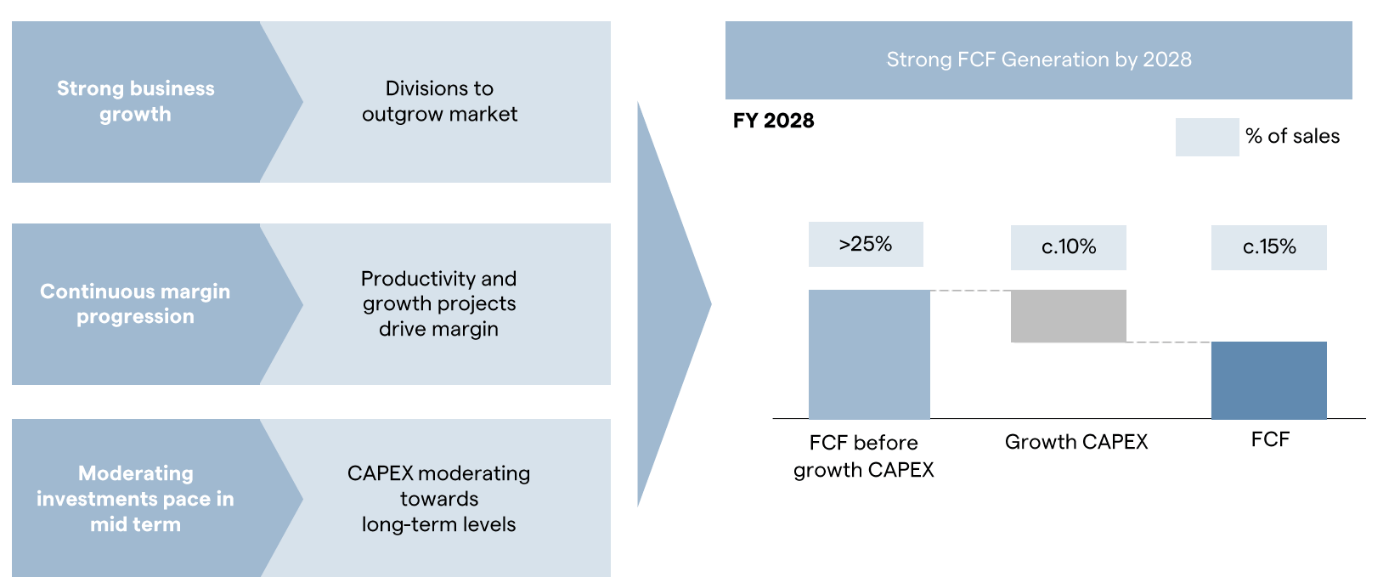

Those new growth investments sound pretty interesting, and Lonza has provided very firm free cash flow conversion metrics. By 2028, it wants to convert 25% of its revenue in underlying free cash flow while the growth capex will likely absorb 40% of that free cash flow, resulting in a free cash flow conversion of 15% on a reported basis.

Lonza Investor Relations

This, in combination with the now known revenue generated in 2023, allows us to calculate the anticipated 2028 free cash flow result. If our starting point is 6.7B CHF in revenue and the revenue CAGR is anticipated to be 11%-13% per year, using the lower end of that range would result in a total revenue of 11.3B CHF in 2028. This means that on an underlying basis and excluding the growth in capex, the free cash flow result would come in at 2.8B CHF. Divided over an anticipated share count of 70M shares (assuming the company will continue to buy back stock), this represents a free cash flow result of 41 CHF per share (excluding growth investments). If the company continues to spent 10% of its revenue on growth capex,

The autonomously generated cash will be very helpful to meet those targets

The company released its full-year financial results on Friday, and it’s always interesting to see how much free cash flow it generates to ensure it can finance a substantial portion of its growth ambitions using its own cash and cash flow.

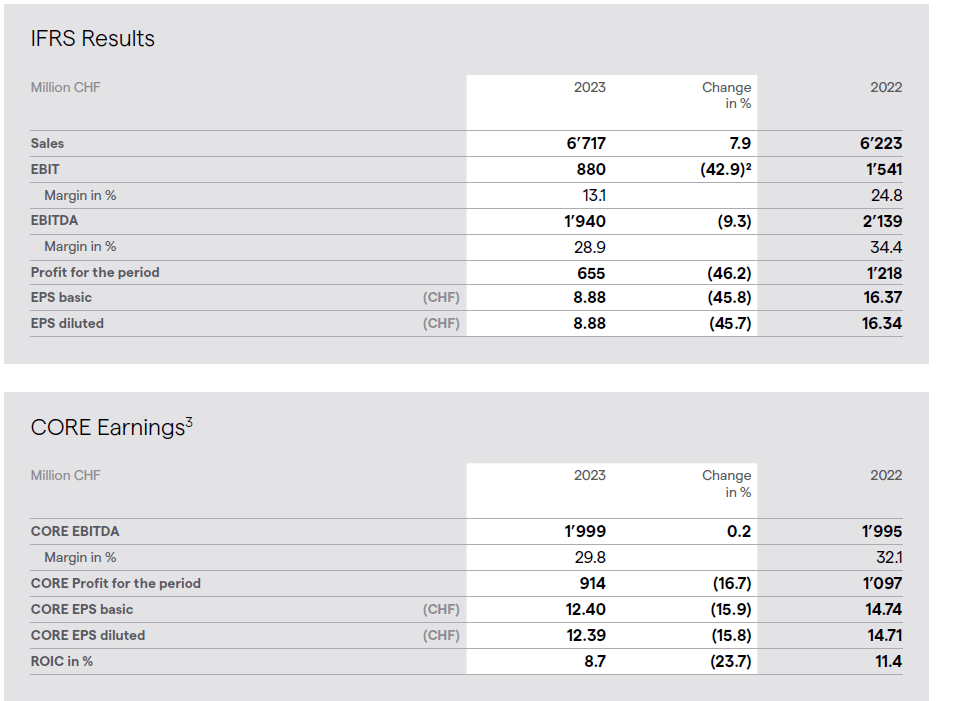

During FY 2023, Lonza saw its revenue increase by almost 11% on a constant FX basis, resulting in a total revenue of 6.7B CHF while the core EBITDA margin was 29.8% which means that despite the higher revenue, the EBITDA was flat.

Lonza Investor Relations

As the image below shows, the company indeed reported a total revenue of 6.7B CHF, on which it generated a gross profit of 1.95B CHF and an EBIT of 880M CHF. That’s not really comparable with the 1.54B CHF EBIT in 2022 as the latter includes a 199M CHF gain on the divestment of a division. Looking at Lonza’s own financial results, the net income of 655M CHF was not that great and the attributable profit of 654M CHF represented an EPS of just 8.88 CHF.

Lonza Investor Relations

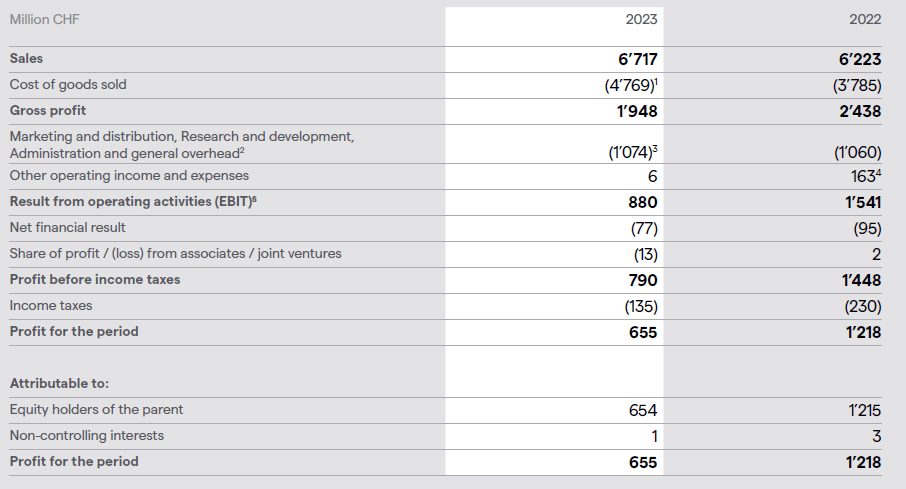

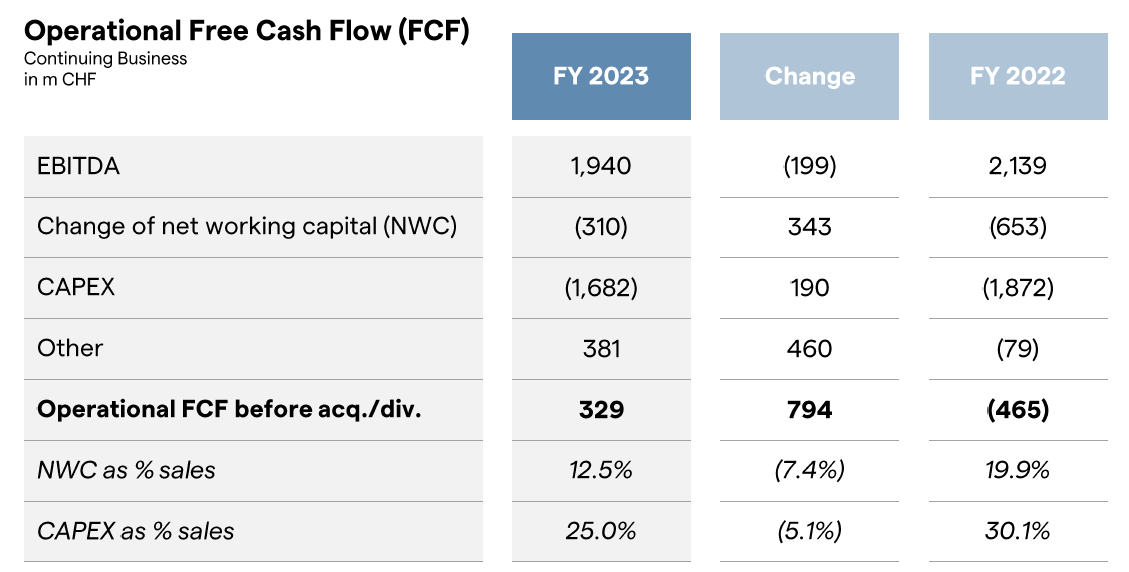

Moving over to the cash flows: As you can see, the company reported an operating cash flow of 1.39B CHF and adjusted for lease payments and working capital changes, the adjusted operating cash flow was 1.3B CHF.

Lonza Investor Relations

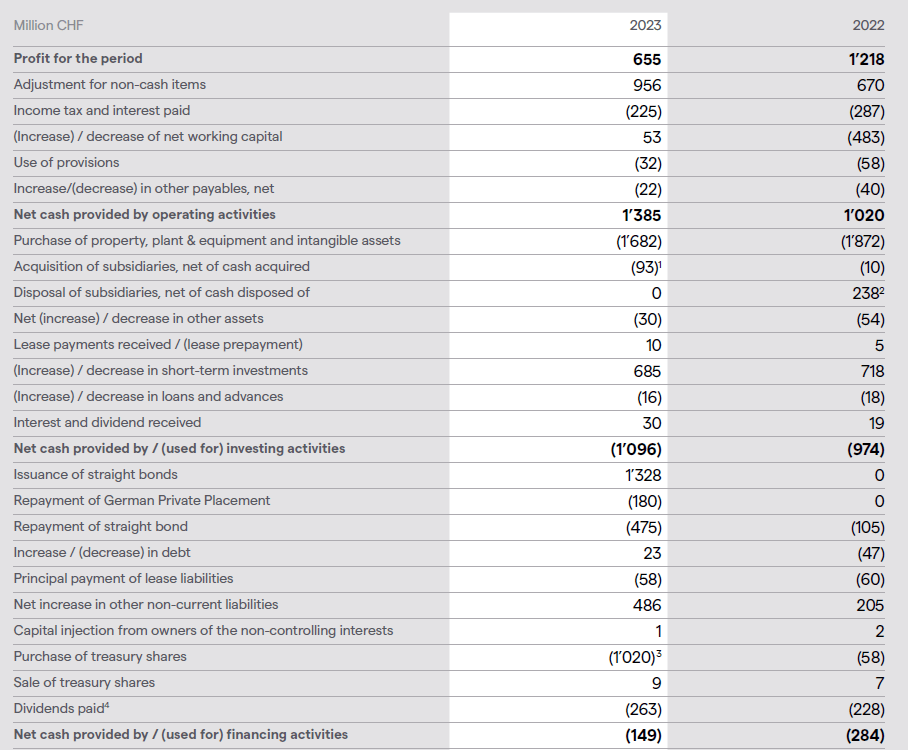

As you can see above, the company spent 1.68B CHF on capex, which means Lonza was definitely free cash flow negative despite the company’s claims it generated a positive free cash flow of 329M CHF. The explanation for that discrepancy is simple: Lonza reports the “operational free cash flow” which excludes the interest and tax payments. Both methods are correct, but I prefer to include interest and tax payments.

Lonza Investor Relations

It will be interesting to see the company’s performance in 2024. Although Lonza confirmed its guidance for the 2024-2028 period, its official guidance for 2024 is somewhat disappointed as it expects a flat revenue and a core EBITDA margin in the high twenties. That’s fine considering I’m more interested in the longer term outlook, but it does mean the 2025-2028 period should show stronger growth results than the four-year average.

Investment thesis

The market reacted quite negatively when Lonza initially announced its guidance for 2024-2028, but I think the targets are now transparent and very straightforward. And perhaps even more important, these targets appear credible. While the company’s 2023 results weren’t great and even 2024 won’t bring any improvement, I have a more long-term outlook, and given the company’s 2028 guidance implies a free cash flow result per share of 41 CHF per share, I’m willing to be patient.

I may initiate a long position in Lonza in the near future, as I don’t mind starting to build a position when the market clearly isn’t impressed with Lonza’s performance.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")