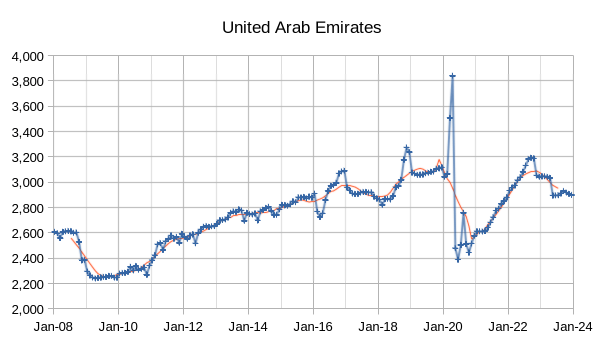

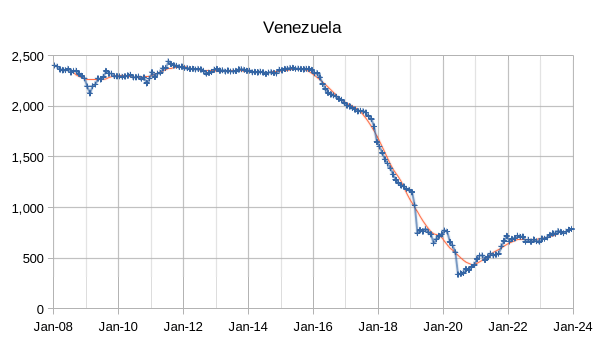

zhengzaishuru

A guest post by D Coyne

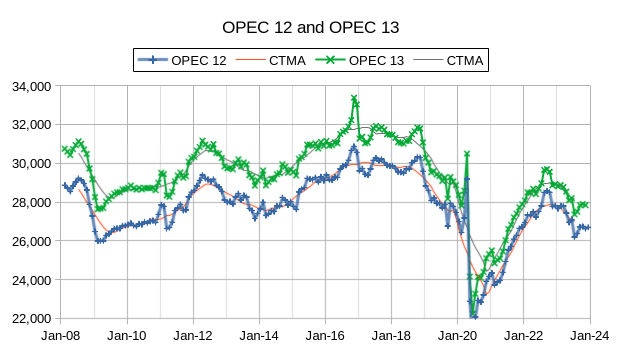

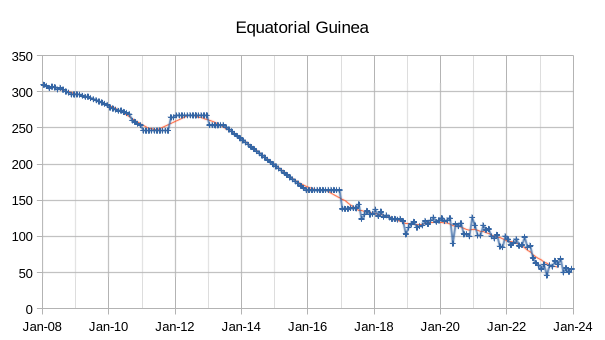

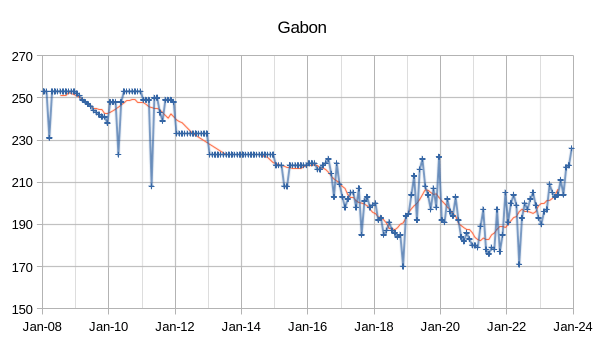

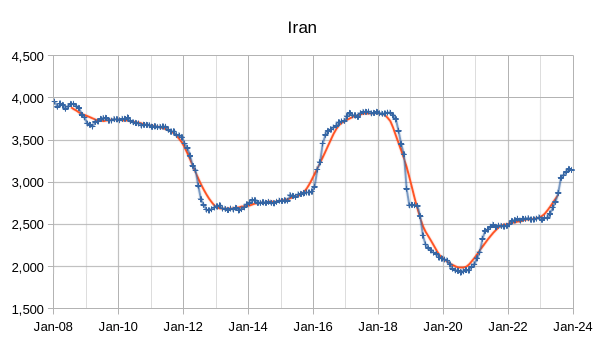

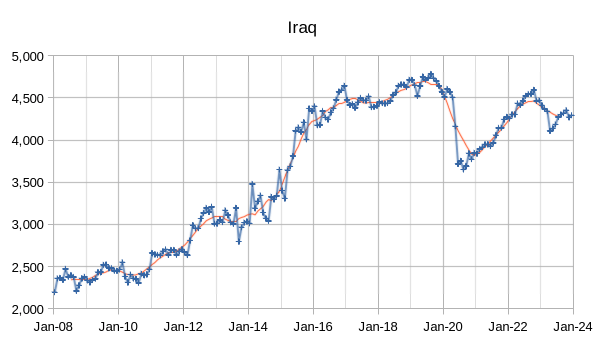

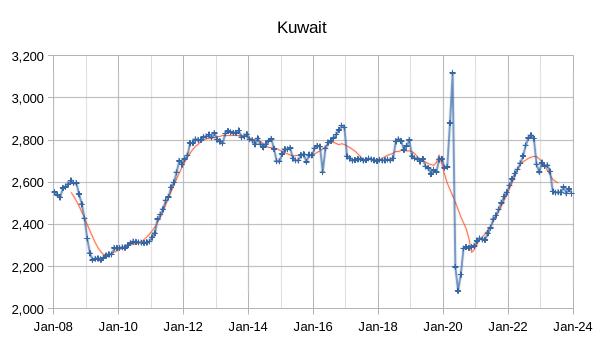

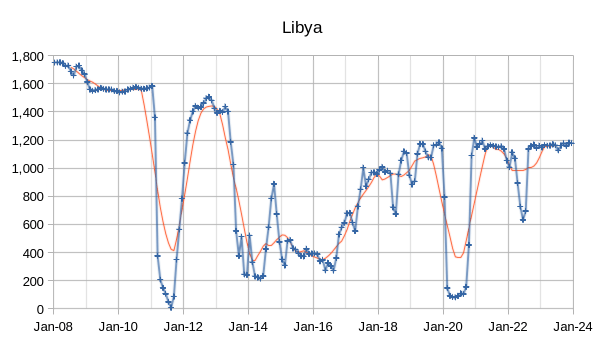

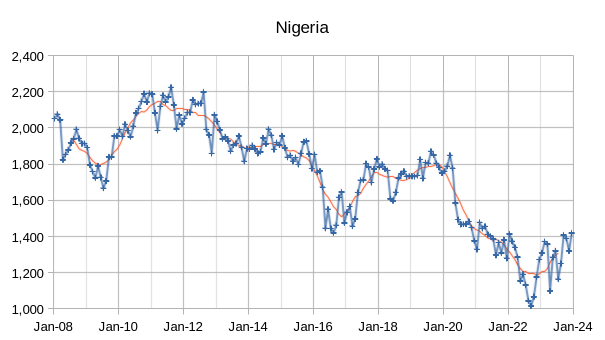

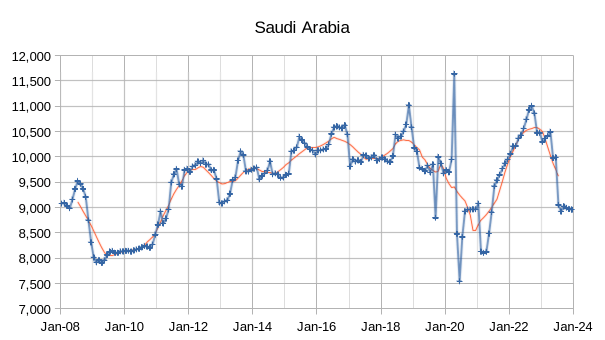

The OPEC Monthly Oil Market Report (MOMR) for January 2024 was published recently. The last month reported in most of the OPEC charts that follow is December 2023 and output reported for OPEC nations is crude oil output in thousands of barrels per day (kb/d). In many of the OPEC charts that follow the blue line with markers is monthly output and the thin red line is the centered twelve month average (CTMA) output. For the first chart I compare OPEC- 13 with OPEC -12 due to Angola deciding to leave OPEC and reducing the number of OPEC nations by one.

When the World was at its CTMA peak for C+C output in 2018, OPEC-12 crude output was about 29830 kb/d and by December 2023 OPEC-12 crude output had fallen to 3130 kb/d below OPEC-12 output at the World C+C CTMA peak in 2018.

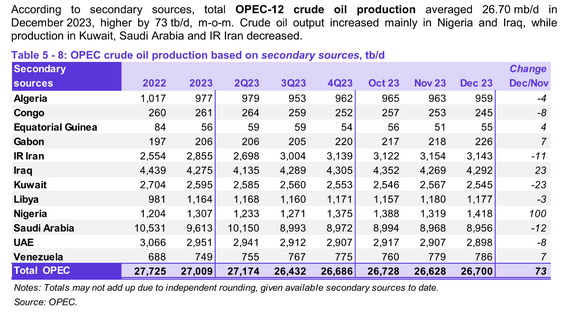

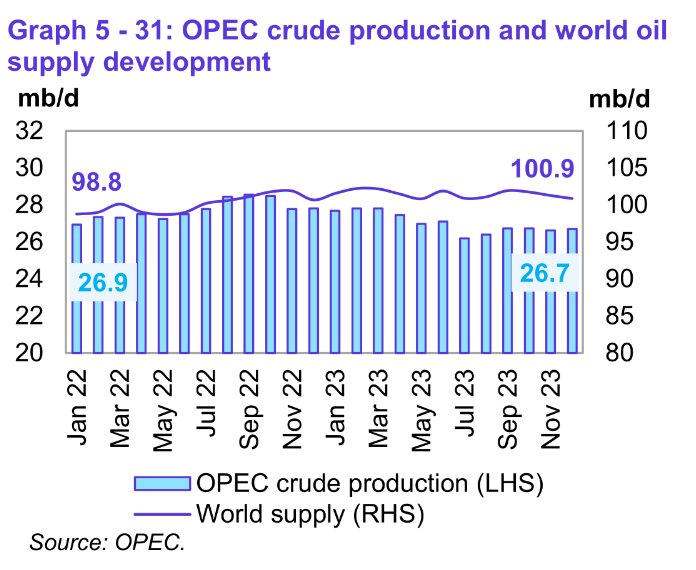

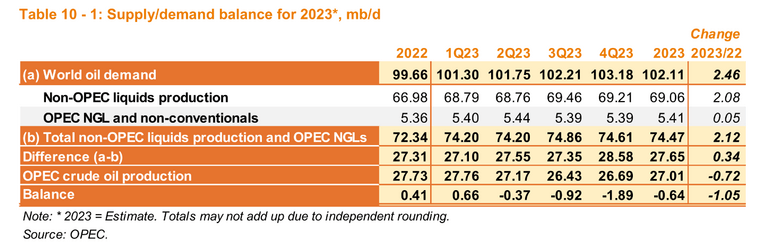

Preliminary data indicates that global liquids production in December 2023 increased by 0.2 Mb/d to average 101.9 Mb/d compared with the previous month. Liquids supply was 2.1 Mb/d higher than 23 months earlier and OPEC crude output was 0.2 Mb/d less than 23 months earlier.

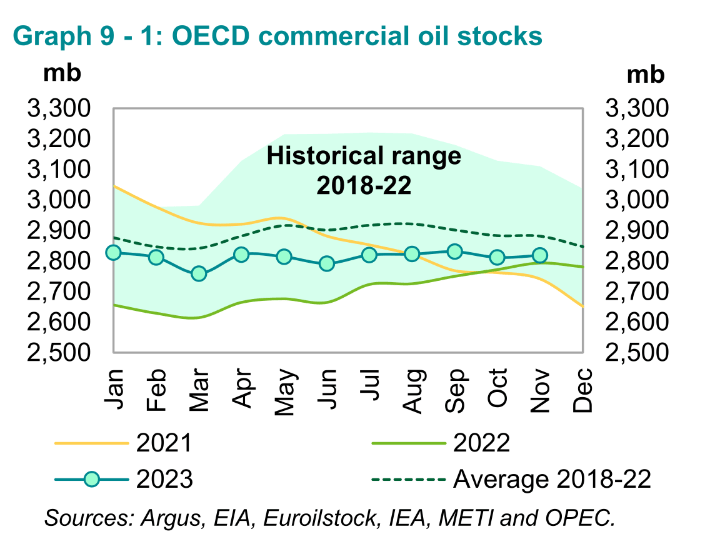

OECD Commercial Oil stocks were 7.3 Mb higher in December than last month. At 2,819 Mb, they were 25 Mb higher than the same time one year ago, but 62 Mb lower than the latest five-year average and 122 Mb below the 2015–2019 average.

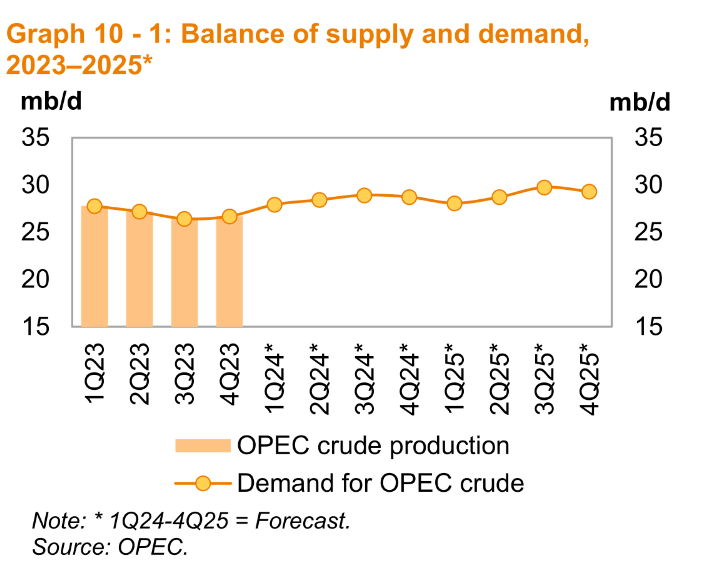

The chart above looks at demand for OPEC-12 Crude which is close to 30 Mb/d for 2025Q3 based on OPEC forecasts of non-OPEC liquids supply and World Liquids demand. The peak centered 12-month average output for OPEC-12 was in April 2017 at 30.06 Mb/d. Note, however, that the smaller OPEC-8 producers have seen reduced output since 2017.

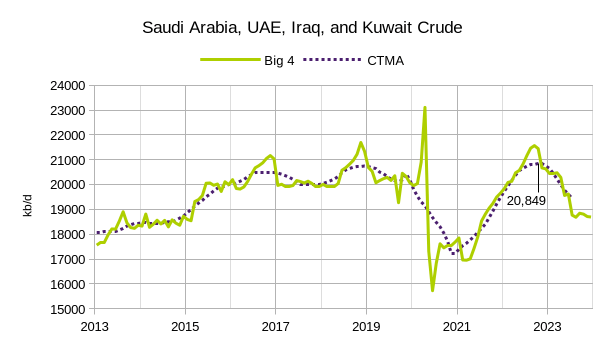

The recent peak for the “Big 4” OPEC producers is 20849 kb/d and the rest of OPEC, which is likely producing at maximum output, is producing 7563 kb/d for their most recent CTMA output. Adding these together gives an output of 28,411 kb/d for OPEC-12 which may be their maximum sustainable output.

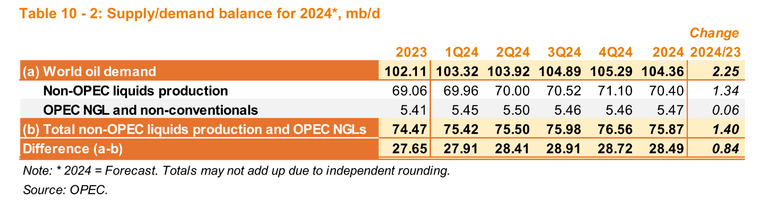

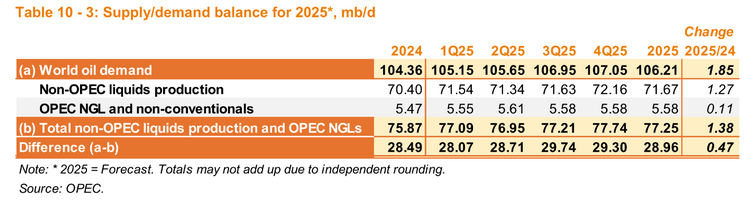

We can see that by 2024 OPEC may not be able to meet the average annual demand for OPEC crude at 28.49 Mb/d. If the OPEC demand forecasts for World liquids are accurate and their Supply forecasts are also accurate, we would expect to see oil prices rise in 2024.

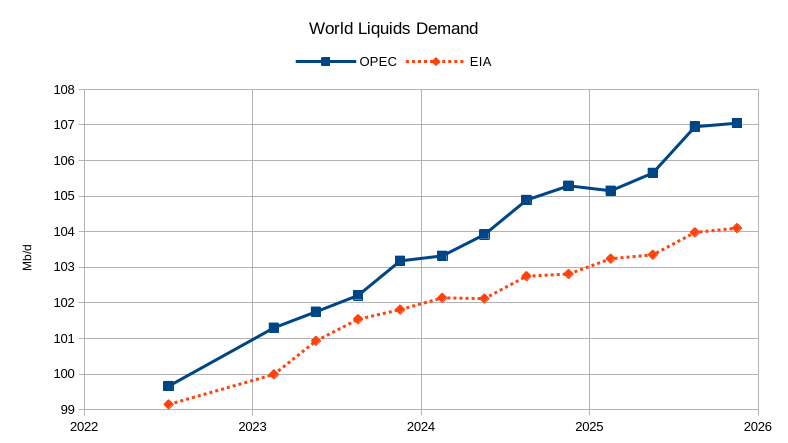

The chart above compares the World liquids demand forecasts from the OPEC MOMR with the EIA’s STEO. There is a widening difference, which reaches nearly 3 Mb/d by 2025Q4. My guess is that the EIA forecast will be closer to reality than the OPEC forecast.

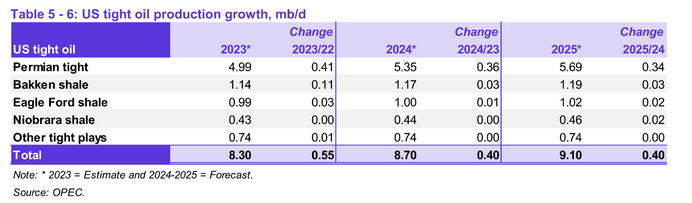

The OPEC forecast for US tight oil output has been revised lower since last month though it may still be optimistic at current oil and natural gas price levels. If prices increase by 10-15%, this forecast might be reasonable.

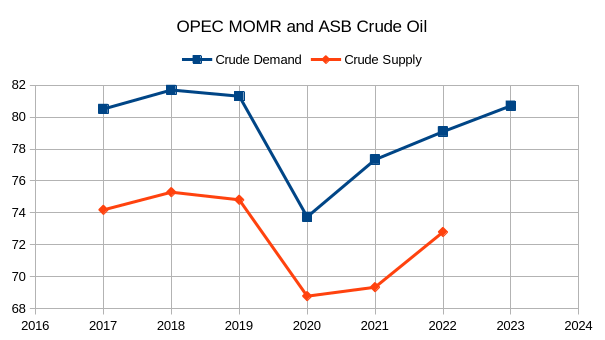

The chart above uses OPEC’s Annual Statistical Bulletin (ASB) for Crude oil supply and the OPEC MOMR Refinery Operations section for refinery crude throughput which is the best measure of crude oil demand. There may be a difference in the way these two reports define crude oil, perhaps the refinery throughput includes some condensate, though the number is lower than the estimate for C+C refinery throughput in the Statistical Review of World Energy 2023. Note that through 2023 crude oil demand remains below the peak in 2018 (80.72 Mb/d vs. 81.7 Mb/d).

Editor’s Note: The summary bullets for this article were chosen by Seeking Alpha editors.

Q2 2024 Earnings Call Transcript")