stocknshares

Zions Bancorporation, National Association (NASDAQ:ZION) submitted a decent earnings sheet for the fourth-quarter on Monday that showed a growing deposit base, no incremental credit provisions, but also a continual decline in the bank’s net interest income. A growing deposit base is obviously great for ZION and although the bank is growing its book value, I believe that the risk profile after a major revaluation to the upside no longer makes shares of the regional lender a buy. For those reasons, I am lowering my rating to hold!

Previous Rating

I rated shares of Zions Bancorp. a strong buy after the regional lender reported third-quarter results — A 5.5% Yield Trading At 0.91X BV — due to the large discount to book value that was available at the time and the attractive dividend income an investment in ZION provided. The bank also saw a return of deposits after the regional banking crisis in the first-quarter of 2023 which was resolved almost single-handedly by the Federal Reserve. While deposits are still growing, the net interest income picture is less attractive and with shares trading significantly above book value again, I believe a rating downgrade to hold appears reasonable.

Zions Bancorporation’s Q4’23 results

Zions Bancorporation beat earnings estimates for the fourth-quarter on Monday with adjusted earnings of $1.30 per-share surpassing the consensus by $0.24 per-share. It was a solid earnings report overall even though the regional bank slightly missed on the top line.

Zions Bancorporation

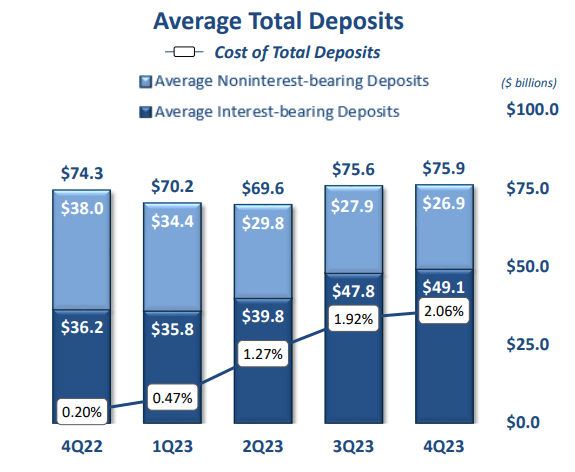

Growing deposit base

Zions Bancorporation is a more than 150-year old regional bank with $87.2B in assets that provides basic financial services to members in its communities. The bank operates in Arizona, California, Colorado, Idaho, Nevada, New Mexico, Oregon, Texas, Utah, Washington, and Wyoming and is focused on the small and medium-sized business lending market.

Zions Bancorporation is a relatively small bank with a market cap of only $6.4B. I first initiated a position in Zions Bancorporation in June 2023 — Strong Recovery Potential — when the collapse of Silicon Valley Bank created unique investment opportunities in the financial markets, largely due to concerns over the deposit situation of regional banks.

Zions Bancorporation’s average deposits dropped off in Q2’23 due to the regional banking crisis impacting depositor confidence, but they snapped back forcefully in Q3’23 as depositors regained their confidence in the stability of the regional banking market. The bank’s average deposits kept growing in Q4’23, but at a much slower rate than in the previous quarter. Zions Bancorporation’s average deposits grew 0.4% quarter over quarter to $75.9B, driven by a growing balance for interest-bearing deposits. In the previous quarter, deposits were up 8.6% Q/Q.

Zions Bancorporation

Fed pivot represents a challenge for Zions Bancorporation’s NII

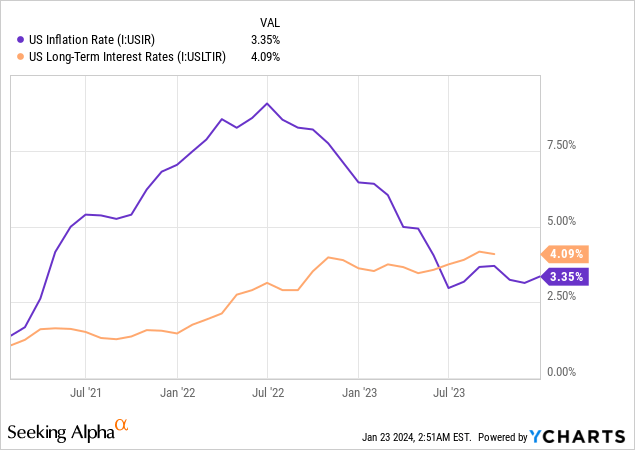

The Federal Reserve recognized in December that inflation has come down a lot over the last year and guided for up to three rate decreases in FY 2024. For banks like Zions Bancorporation, this means that they get to charge less money for credit products such as mortgages, business loans or credit cards. With inflation also falling below the long term interest rate most recently, the Federal Reserve has a strong incentive to end its tightening policy this year.

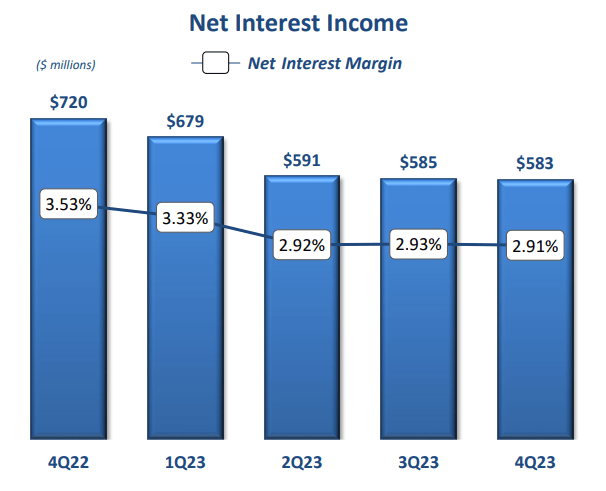

Zions Bancorporation’s net interest income fell in the fourth-quarter, expectedly, and the regional bank reported its fourth consecutive decline in the important net interest income figure. In Q4’23, the bank earned $583M in net interest income which was $137M, or 19% less, than in the year-earlier period. The short term outlook for the bank’s net interest income is not favorable either as the Federal Reserve. Should the U.S. economy show signs of slowing, the Federal Reserve would even have an incentive to out-perform rate cut expectations in FY 2024.

Zions Bancorporation

Zions Bancorporation does have solid credit quality

Zions Bancorporation did not occur any charges with regard to its credit portfolio in the fourth-quarter and reported $116M in Q4’23 net earnings. The bank’s average quarterly amount of credit provisions in the first three quarters was about $44M, so the lack of a charge here was a positive surprise in the earnings report. The absence of credit loss provisions in Q4’23 obviously indicates solid quality for Zions Bancorporation’s loan portfolio.

Zions Bancorporation

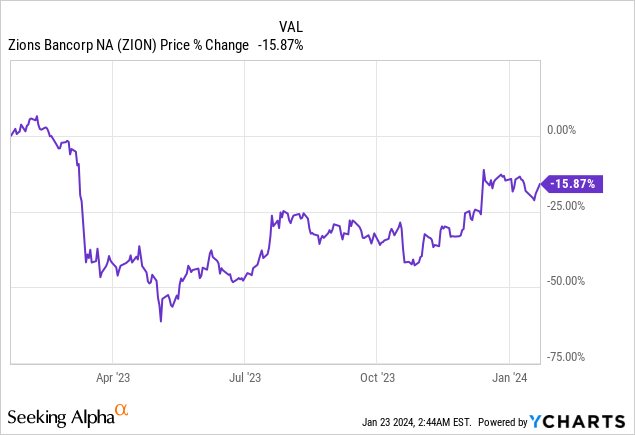

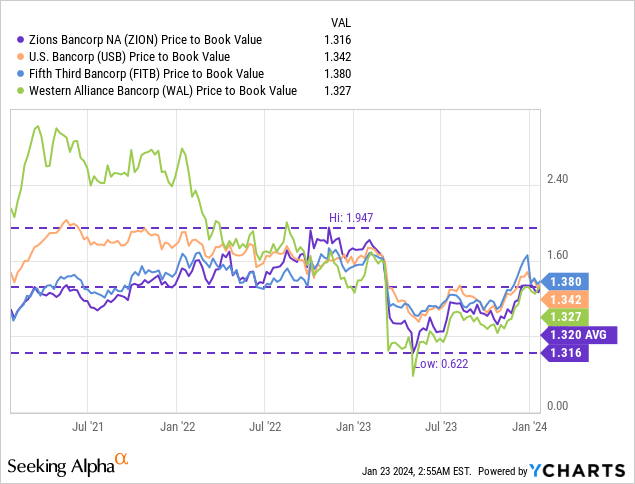

ZION Is Now Trading At A Massive Premium To Book Value Again

I recommended Zions Bancorporation as a buy in the second-quarter of FY 2023 due to what I believed were excessive fears about the stability of the regional banking industry. Zions Bancorporation was trading at 0.96X book value back then which was significantly below the longer term average P/B ratio. In the last three months, a major revaluation to the upside has taken place, in part due to relief over falling inflation and due to a broadly rallying stock market.

According to Zions Bancorporation’s Q4’23 earnings report, the bank had a book value of $35.44 per-share at the end of December, implying a 7.7% Q/Q growth rate. Zions Bancorporation’s shares are now priced at a premium to book value exceeding 30% and shares have revalued to their 3-year average P/B ratio as well, which I previously stated was likely to happen once trust in regional banks and their deposit flows was restored. As a result, I believe shares of Zions Bancorporation are about fairly valued now (my FV estimate range is ~$42-43, based off of ZION’s historical P/B valuation average).

Banks like U.S. Bancorp (USB), Fifth Third Bancorp (FITB) and Western Alliance (WAL) have also seen similarly strong price increases and have revalued to their pre-crisis valuation as well. I have closed all of my positions in banks that I opened during Q1’23 and Q2’23.

Risks with Zions Bancorporation

Zions Bancorporation is set to see lower net interest income in FY 2024, but the bank’s deposit situation is healthy, and so is its credit profile. A strong U.S. economy could further support Zions Bancorporation’s earnings, loan and deposit growth and as long as the bank stays out of trouble with its loan quality, there is theoretically a chance for valuation growth. I do see slower deposit and net interest income growth going forward as the bank’s deposit base has been fully restored.

Final thoughts

Zions Bancorporation had a strong fourth-quarter with a high-single digit growth rate in book value, strong credit quality and a growing deposit base. However, I bought Zions Bancorporation last year in order to benefit from a revaluation of the bank’s shares driven by a restoration of its deposit base and the possibility of a return to a pre-crisis P/B valuation in a normalized banking environment. Shares of Zions Bancorporation have now returned to a pre-crisis P/B ratio of 1.3X and I believe that the weak outlook for net interest income in a low-rate world creates a somewhat unattractive picture for incremental valuation upside at ZION’s current valuation level. As a result, I am down-grading shares of ZION to hold. For personal reasons, I have closed my investment and no longer hold any shares in the regional lender.

Q2 2024 Earnings Call Transcript")