pcess609

Thesis

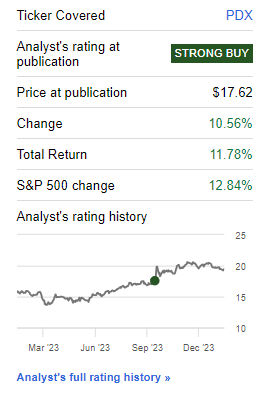

We were eagerly awaiting the portfolio update from Pimco regarding their newly minted PIMCO Dynamic Income Strategy Fund (NYSE:PDX) CEF, which we covered with a ‘Strong Buy’ rating back in 2023 when the conversion was announced:

Prior Rating (Seeking Alpha)

As a reminder, back in September 2023 the fund changed its mandate from an Energy CEF into a more broad mandate, and supposedly credit oriented fund:

NEW YORK, Sept. 22, 2023 (GLOBE NEWSWIRE) — PIMCO Energy and Tactical Credit Opportunities Fund (NYSE: NRGX) (the “Fund”) announced that it will change its name, ticker symbol, investment objectives and guidelines, and portfolio manager lineup, as further described below. Pacific Investment Management Company LLC (“PIMCO”), the investment manager of the Fund, expects that the changes will reduce the Fund’s focus on investments linked to the energy sector in favor of a primarily income-oriented objective and broader, multi-sector credit mandate.

On the back of this corporate action we wrote our initial piece, where we were expecting the fund to go overweight credit, and similarly to other Pimco credit CEFs experience a substantial narrowing of its discount to NAV.

Pimco does not seem to be in the business of updating their portfolios every month on their website, even when the fund completely changes mandate. We dropped them a note two weeks back since there was no update since September 2023 on their website regarding the fund composition. We do not like running blind risk, and we noticed the weak correlation for PDX with other credit CEFs during recent market moves. We never got a response, but it seems that now the portfolio has been updated.

The ‘revised’ portfolio – not what you would expect

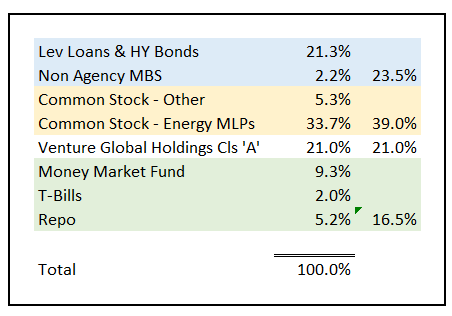

Boy oh boy are we surprised by what we are seeing in the ‘revised’ PDX portfolio. The parsing on the Pimco website is misleading, so we encourage investors to download the individual holdings Excel, which you can find here and go through every line item. By going through the respective Excel we come up with the following aggregation:

Fund Holdings (Pimco / Author)

We have 21.3% of the collateral assigned to ‘traditional’ leveraged loans and high yield bonds and 2.2% allocated to non-agency MBS bonds. That makes the total credit component of this CEF only 23.5%. By far the largest component here is made up of energy equities at 33.7% and the private investment in the Venture Global LNG project at 21%. Energy equity thus still represents over 54% of the fund’s collateral.

The energy equity sleeve is a mix of MLP names and E&P producers. For example we have EQM Midstream Partners LP (EQM) in the collateral pool as an MLP, alongside names such as Antero Midstream (AM) and pure E&P names such as Matador Resources (MTDR).

What is surprising as well is the fact that the CEF contains equity in names which have absolutely nothing to do with what one would expect: the fund has a 2.6% position in AT&T (T) common stock, and a 1.6% collateral position in Organon (OGN) a women’s health provider. We did not expect these kind of equity positions to still be here, and they do not make sense within the overall framework of the revised fund (as far as we are concerned).

Venture Global – a concentrated bet on LNG

Let us also shed some more color on Venture Global, a private investment made by the fund:

Venture Global is a long-term, low-cost provider of U.S. LNG sourced from resource rich North American natural gas basins. Venture Global’s first facility, Calcasieu Pass, commenced producing LNG in January 2022. The company’s second facility, Plaquemines LNG, is under construction and expected to produce first LNG in 2024. The company is currently constructing and developing over 70 MTPA of nameplate production capacity to provide clean, affordable energy to the world. Venture Global is developing Carbon Capture and Sequestration (CCS) projects at each of its LNG facilities.

LNG export facilities are a physical necessity for the U.S. to arbitrage the massive differentials in natural gas prices in the U.S. versus Europe or Asia. They represent the physical means of transforming gas into a liquid:

Liquefied natural gas is created by cooling natural gas and reducing its volume- making LNG easier, safer and more efficient to ship around the world.

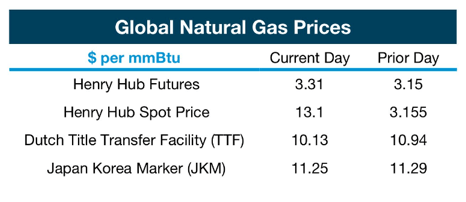

Transforming natural gas into a liquid allows for the easy transportation via ships of large quantities of the commodity, and the monetization of the following geographic spread:

Natural Gas Prices (NatGasCollector)

You are reading the above chart correctly – in Europe gas prices are 3x the ones in the U.S., while in Asia it is close to 4x. By taking cheap U.S. gas and transforming it into liquids, companies can realize significant profits by selling the same commodity in Europe or Asia.

There is also a significant geopolitical component to natural gas. Russia had built a virtual monopoly in Europe throughout the past decade via its cheap natural gas. The thought process was that Europe would be so dependent on Russian gas that they would not intervene in Ukraine for fears of getting their supply cut-off. The Russian plan did not work as expected, with Europe making a significant pivot away from Russia via the construction of new import LNG facilities:

The EU’s decision to diversify natural gas supply away from Russia in 2022 prompted a large-scale expansion of the bloc’s LNG import capacity and triggered an increased dependence on LNG supplies, with Europe seeing a 60% year-on-year increase in imports in 2022. The trend has continued through 2023, with S&P Global data showing European import figures on track to surpass last year’s record of 125.9 million mt of LNG (173 Bcm).

Source: S&P

Biden strikes again

Commodities are an interesting asset class but a political punching-bag, especially from an ESG perspective. Venture Global has just found out how politics can derail business:

Jan 24, 2024: In a potential victory for environmental advocates, the Biden administration is apparently putting pressure on a federal agency to delay approvals of U.S. liquefied natural gas export terminals, particularly a controversial plant on the southwest Louisiana coast, amid calls from environmentalists to stymie LNG projects altogether, according to a New York Times report. The White House has told the Department of Energy to broaden its review of CP2 LNG to consider its impact on climate change, the New York Times reported, citing anonymous sources

Announced in 2021, CP2 is the third planned LNG terminal from Venture Global:

U.S. LNG Capacity (Energy Research)

Calcasieu Pass 2 was supposed to come to market in 2026, thus providing further volume to the U.S. LNG capacity. While we do not know how the regulatory approval will ultimately work out, it will be delayed for sure, if not fully nixed. They might just kick the can down the road for the next administration to make a decision, but irrespective of the actual outcome, the initial business plan and IRRs have taken a hit. There will be a valuation impact to Venture Global from this political action.

With the current collateral do not expect the discount to narrow

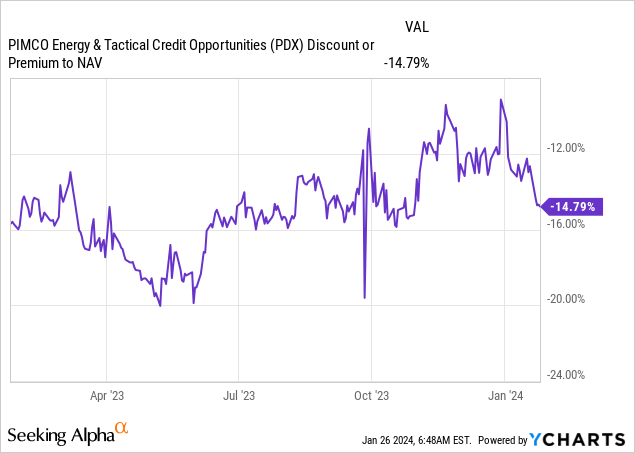

One of the original premises of our ‘Strong Buy’ rating was around the significant potential for gains given the very wide discount to NAV exposed by the CEF. If we look at other Pimco credit CEFs we will notice they trade flat to NAV or at a premium, highlighting the market’s view and appetite for Pimco as a credit manager.

Our expectation was for PDX to be heavily overweight credit (i.e. more than 60%) after its mandate change, and thus be perceived as a credit fund by the market. Let us see what the CEF actually did:

In effect we have seen no narrowing in the discount to NAV. This is surprising without any context, but when delving into the collateral we can clearly see why – the CEF has not become a credit CEF, but still remains very much of an Energy CEF.

There is nothing wrong with energy in today’s market, and we like natural gas MLPs and E&Ps here for example, but the point is that PDX is very much still an energy CEF and will continue to trade like one, i.e. with a large discount. The market has historically assigned MLP CEFs very high discounts after the Covid meltdown, and still trades them with unusual wide ones. We have seen activist funds such as Saba score victories by pressuring managers of MLP CEFs into taking corporate actions to narrow said discounts.

Until PDX becomes a true credit CEF expect the large discount to NAV to persist. Right now this is a 60% Energy, 23% Credit, 17% Cash fund with unusual holdings such as AT&T equity. Until we see over 60% Credit and a clean collateral pool (the Common Stock – Other bucket should disappear) there is little hope for the discount to narrow in our opinion.

Conclusion

We would have liked to see PDX become a true credit CEF, where its market moves would be determined by interest rates, credit spreads and duration. Instead PDX remains an energy CEF, with a large MLP and E&P equity component, and a large private equity stake in an LNG export facility. While energy looks good at the current valuation levels this is not what is needed for the PDX discount to narrow. In our opinion, until PDX cleans up its collateral pool and has credit as its main component (over 60% of the holdings), the fund will continue to trade at a wide discount to NAV. As we have seen with the latest political action around Calcasieu Pass 2, regulatory issues are front and center in the energy space, and they are not predictable. We expect some sort of negative valuation impact to the fund’s Venture Global stake from this political development. With our initial thesis not materializing we are going to reduce our exposure to this name, and move the CEF to Hold.

Q2 2024 Earnings Call Transcript")