Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

For a long time it looked like the financial crisis aftermath had practically killed the single-name CDS market.

A decade ago even Deutsche Bank — once a monster in credit default swaps — stopped trading them. The decline in trading volumes of CDS referencing individual companies and countries was so dramatic that it was imperilling the somewhat healthier CDS index market. When Blackstone Group’s GSO unit started pulling some delightful shenanigans people feared the end was nigh.

Not any more! While it’s not quite as epic and exhilarating a comeback as 2019 Liverpool-Barcelona (please don’t leave, Jürgen!), there’s been a pretty remarkable recovery in recent years.

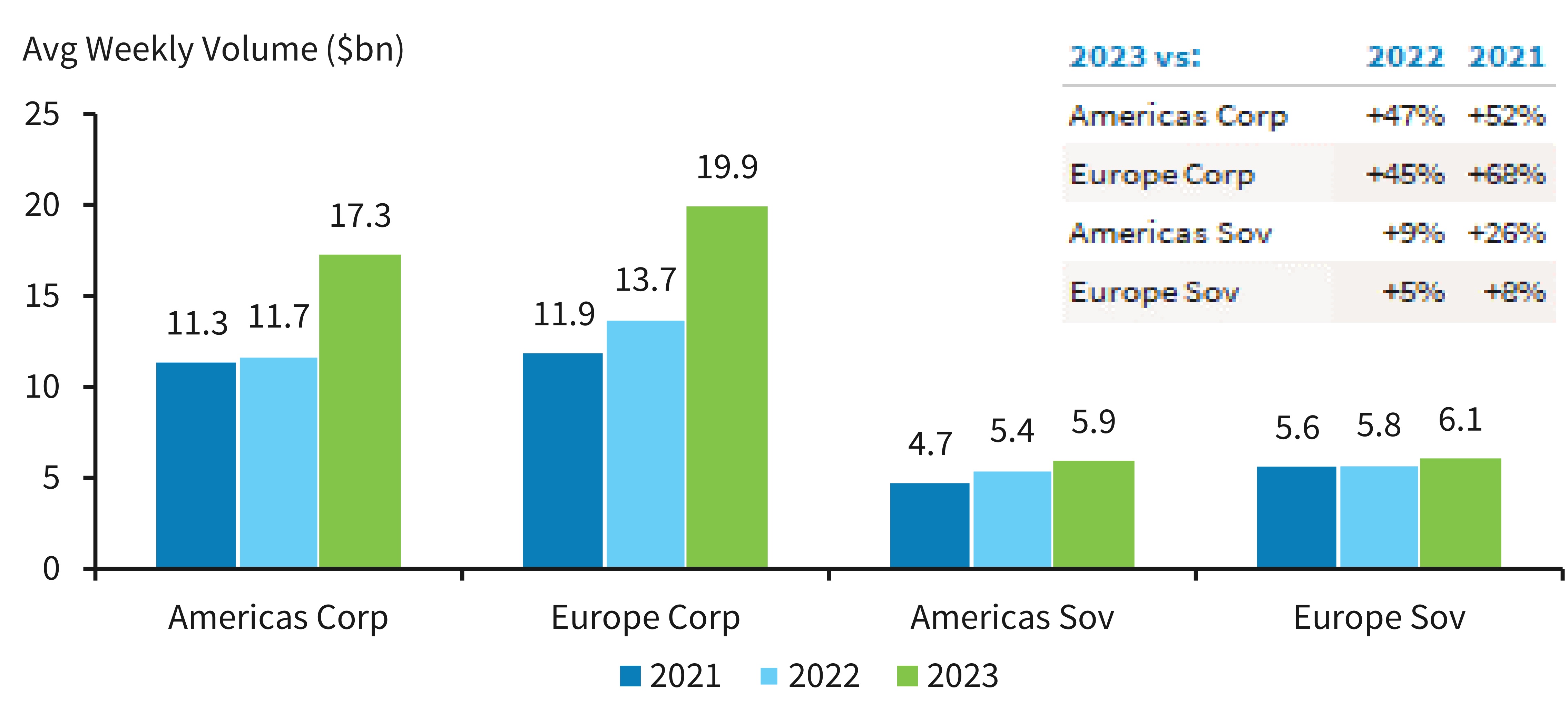

Alex trailed the single-name CDS trading upswing last summer, and we now have the final tally. The market smashed it in 2023 with a ca 50 per cent jump in average weekly trading volumes in corporate CDS, and a healthy increase in sovereign CDS as well.

From Barclays (zoomable version):

“We view the gains as consistent with a shift away from general macro concerns and more toward credit selection,”, according to Barclays:

For the US, anecdotal evidence suggests that the uptick in activity occurred across investor types, with hedge funds particularly active, but we believe that the need for banks to hedge idiosyncratic/counterparty risk (and the willingness of other investors to provide an outlet for that demand) was an important driver of volumes for index and non-index names alike. Index arb also remained active, with the skew offering numerous opportunities for “reverse arb” attempts.

As in the US, European corporate CDS volumes are up meaningfully — lower in percentage than the US, but higher in absolute terms. This fits with a general sense that single-name CDS is a bear market product, with interest increasing as idiosyncratic risk rises. European sovereign CDS have posted a small increase y/y, but less than that of sovereign CDS in the Americas. This also makes sense to us given the lack of concern about European Union integrity.

The only thing that saw an even healthier pick-up in trading volumes was total return swaps on investment-grade debt, and that’s a tiny market (weekly average trading volumes of $600mn, compared to $17.3bn for single-name CDS).

Obviously trading volumes are still piddling compared to pre-GFC levels, but this means single-name CDS leapfrogged investment-grade corporate bond ETFs and loans to be the sixth most active segment of the credit markets. Huzzah!

Does this matter? No, not enormously. But it’s a slow Friday, several posts have already been spiked for being even more unremarkable, and Alphaville has a soft spot for the CDS market.

Q2 2024 Earnings Call Transcript")

{kind=link}