ilbusca

All financial numbers in this article are in Canadian dollars unless noted otherwise.

Introduction

Earnings season is heating up! This usually means we put a bigger emphasis on railroads, defense companies, machinery producers, financials, and other stocks that are both great economic indicators and fantastic long-term investments.

In this article, we start the railroad earnings season with one of the best North American railroads. That company is the Canadian National Railway (NYSE:CNI), the largest competitor of Canadian Pacific Kansas City (CP), which is a holding of my dividend growth portfolio.

The only reason why I do not own CNI shares is the fact that I own three other railroads already. In addition to Canadian Pacific, I own Union Pacific (UNP) and Norfolk Southern (NSC), which means I have Canadian exposure, “mid-America” exposure, and a wide variety of goods, including bulk, merchandise, and intermodal.

Association of American Railroads

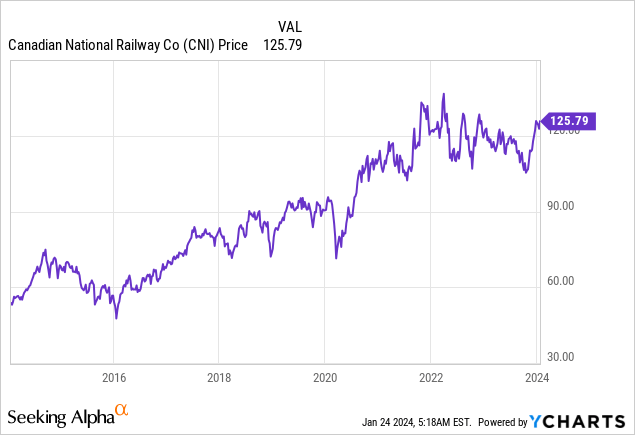

With that in mind, after writing a series of neutral articles last year, my most recent article was bullish when I gave the stock a Buy rating, using the title “Canadian National Has Entered The Buy Zone: Navigating Challenges, Embracing Opportunity.”

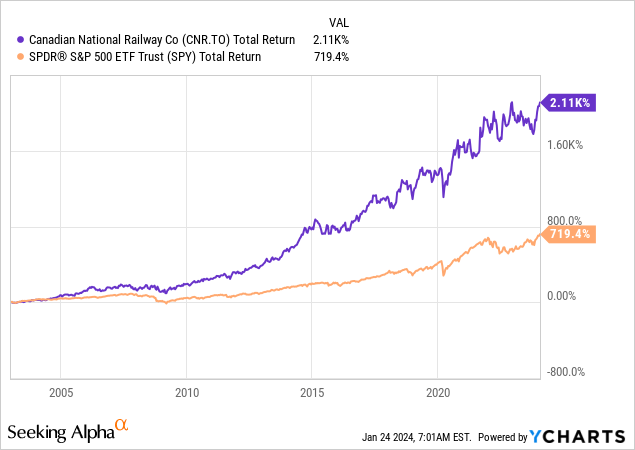

Since then, CNI shares have returned 21%, beating the S&P 500 by roughly 600 basis points.

As the company just released its Q4’23 earnings, there’s no better moment to reiterate the bull case and focus on the value this stock brings to the table for long-term investors.

Also, if you do not own CNI stock, we will also learn a lot about economic developments and what this may mean for other railroad earnings down the road.

So, let’s get to it!

The Bigger Picture

Before we dive into any numbers, let me quickly give you a quick look at the bigger picture.

While the U.S. economy is not in a recession, we are seeing headwinds in cyclical industries.

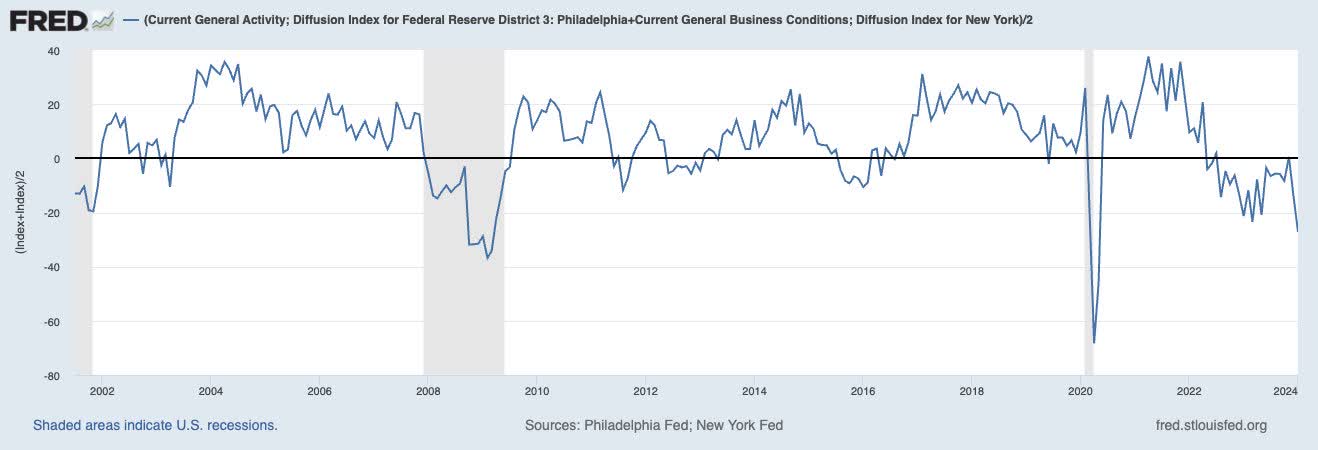

For example, leading economic surveys like the Philadelphia and New York Federal Reserve manufacturing surveys point to a further contraction in manufacturing, which does not bode well for industrial companies like railroads.

After all, railroads are among the most cyclical companies, as they connect players in almost all supply chains.

Here’s what the average of the Philly Fed and New York Fed surveys looks like:

Federal Reserve Bank of St. Louis (FRED)

Again, while we’re not in a recession yet, we are seeing signs that we may come closer to a recession.

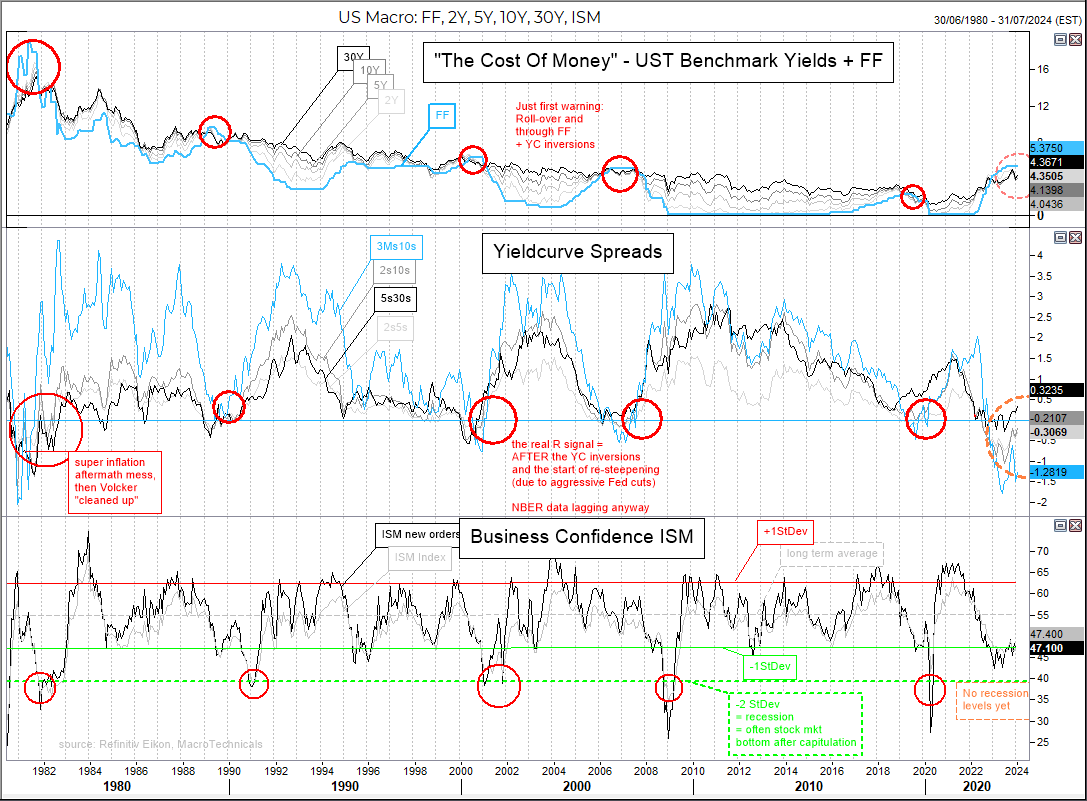

For example, using the chart of a friend of mine, we see a few indicators that point to a recession:

- The “cost of money” is rolling over, hinting at expected rate cuts.

- The yield curve is slowly becoming uninverted, which is a recession signal.

- The ISM Manufacturing Index (highly correlated to the regional Fed surveys I just used) is close to recession levels as well.

- If regional surveys are right, the ISM index may be at recession levels when it reports new numbers in early February.

Twitter: @MacroTechnicals

Don’t get me wrong. I’m not trying to get people to sell anything.

I have not been a net seller of stocks since I started to build a larger long-term portfolio. I also hold no shorts.

The only change I made going into this year is holding a bigger cash position. I increased my savings rate and now hold roughly 15% cash, which I want to use in case economic conditions cause a stock market correction.

If I did not have so much railroad exposure already, CNI would be on my buy list.

Strength Amid Weakness

In light of economic conditions, the company did well.

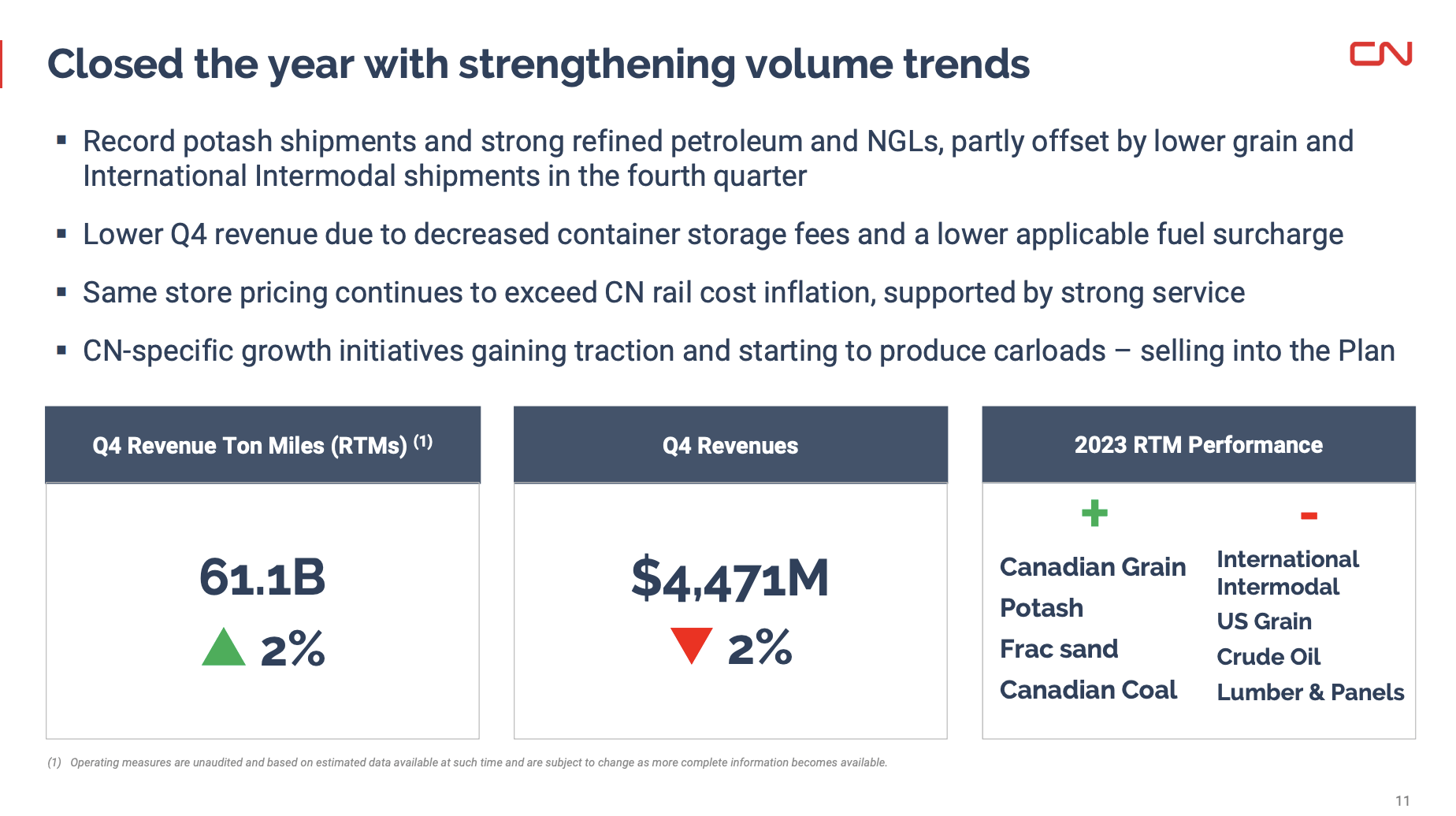

Despite a 2% decline in fourth-quarter revenues, key operational metrics, such as Revenue Ton-Miles (RTMs), increased by 2%, indicating operational resilience.

Canadian National Railway

Diving into the details, as we can see in the overview below, petroleum and chemical volumes showed a significant increase of 12%, excluding crude oil.

The metals and minerals segment experienced a 3% growth in RTMs, with positive trends across various components, except for iron ore, where RTMs were down due to a shift in shipment patterns.

Bulk shipments, particularly fertilizers, witnessed a substantial 85% increase, as the company handled incremental domestic and record potash exports using its available capacity in the Eastern and Southern regions.

Coal performance varied, with Canadian coal up 5% and U.S. coal down 9%. Forest product volumes, however, were down by 5%, reflecting softer market conditions.

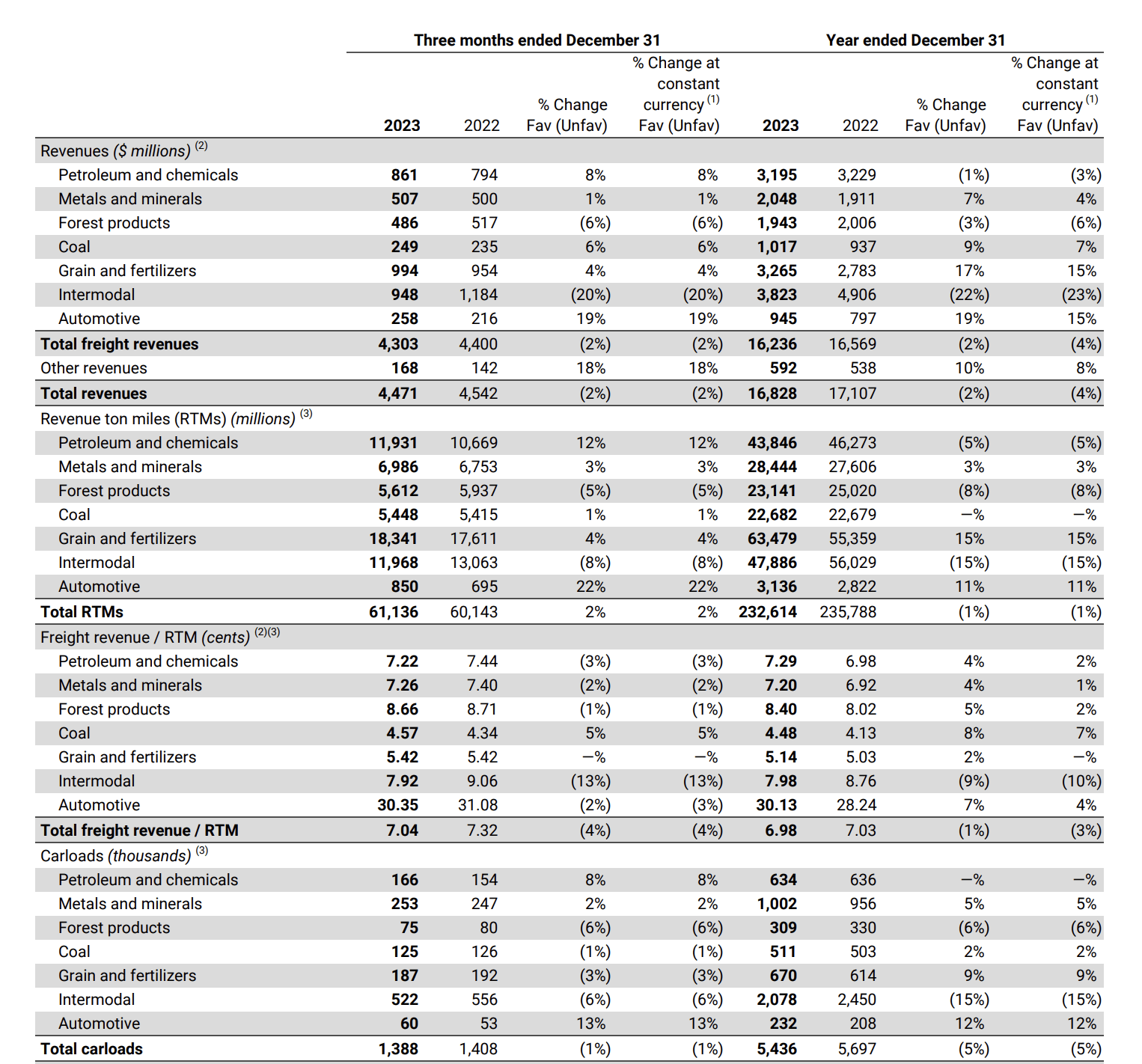

The table below gives you a full overview of these numbers, including total freight revenues, total RTMs, freight revenue per RTM, and carloads.

Canadian National Railway

With regard to consumer-focused goods, the international intermodal faced challenges, with an 11% decrease, primarily attributed to the lingering effects of a port strike.

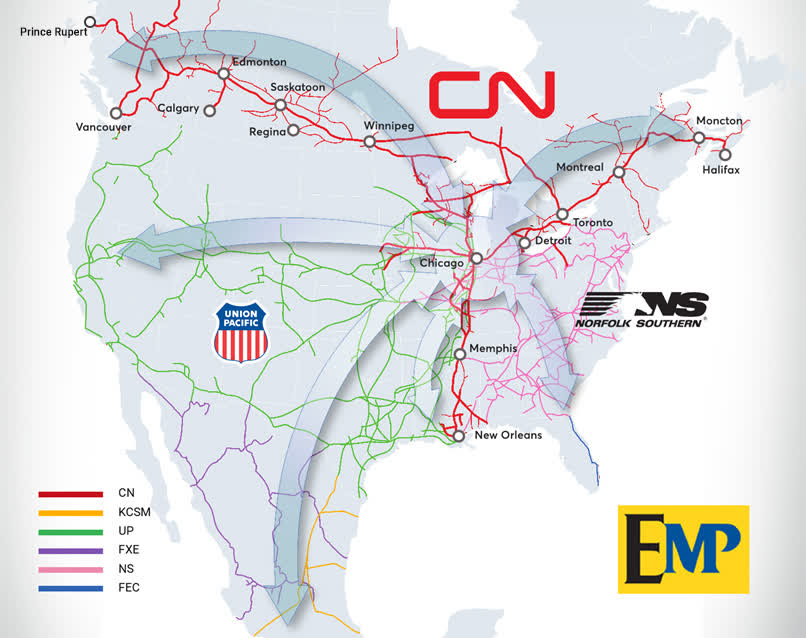

However, domestic intermodal showed resilience, mitigating market softness through the implementation of company-specific initiatives such as Falcon and EMP.

EMP, for example, is its program to improve intermodal operations, partnering with Union Pacific and Norfolk Southern to create a network that benefits all three players in North America.

Canadian National Railway

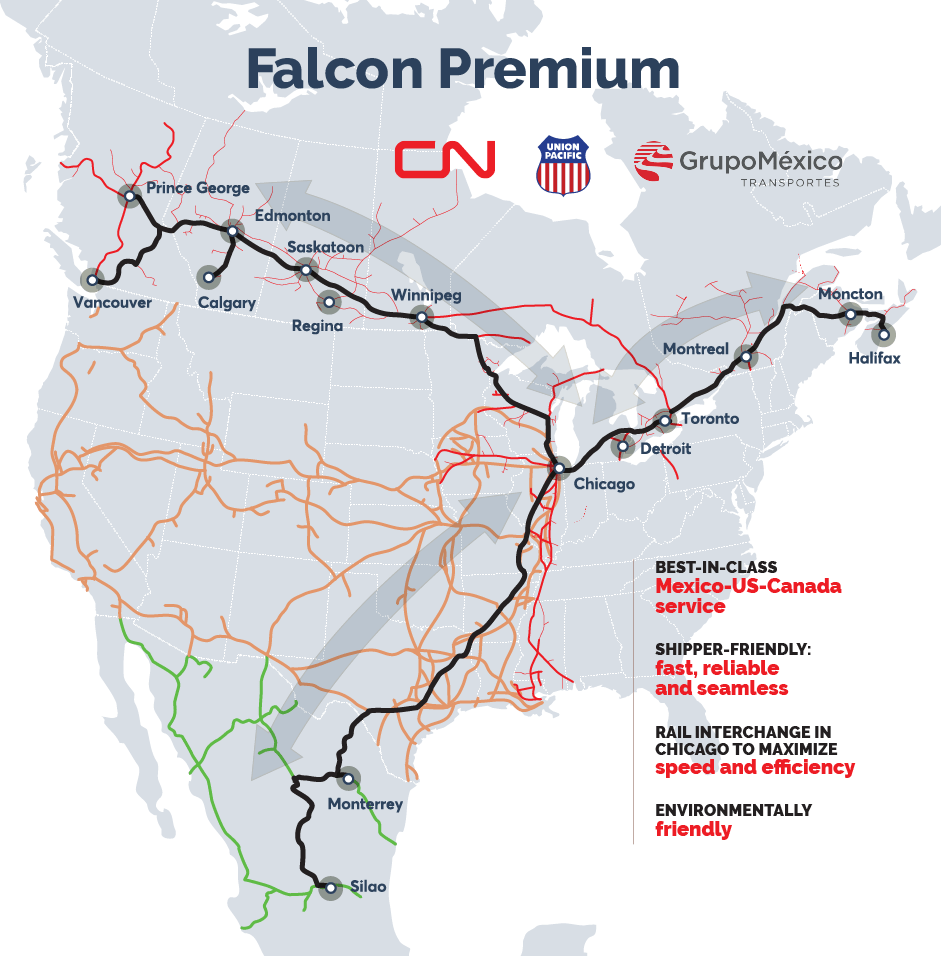

Meanwhile, the company’s Falcon Premium service is a collaboration with Union Pacific and GrupoMéxico to get better access to Mexico’s market.

This is a measure to benefit from economic re-shoring, Mexico’s increasing importance in the rail industry, and to compete with Canadian Pacific, which now owns the first network covering all three North American nations through a single railroad.

Canadian National Railway

Furthermore, with regard to the economic environment, despite a 2% decline in fourth-quarter revenues, the company is optimistic about a gradual return to pre-COVID volume levels.

Factors contributing to this outlook include increased drilling in Northeast BC, new interline partnerships targeting truck volumes, and positive expectations in the economy, particularly in lumber and panels.

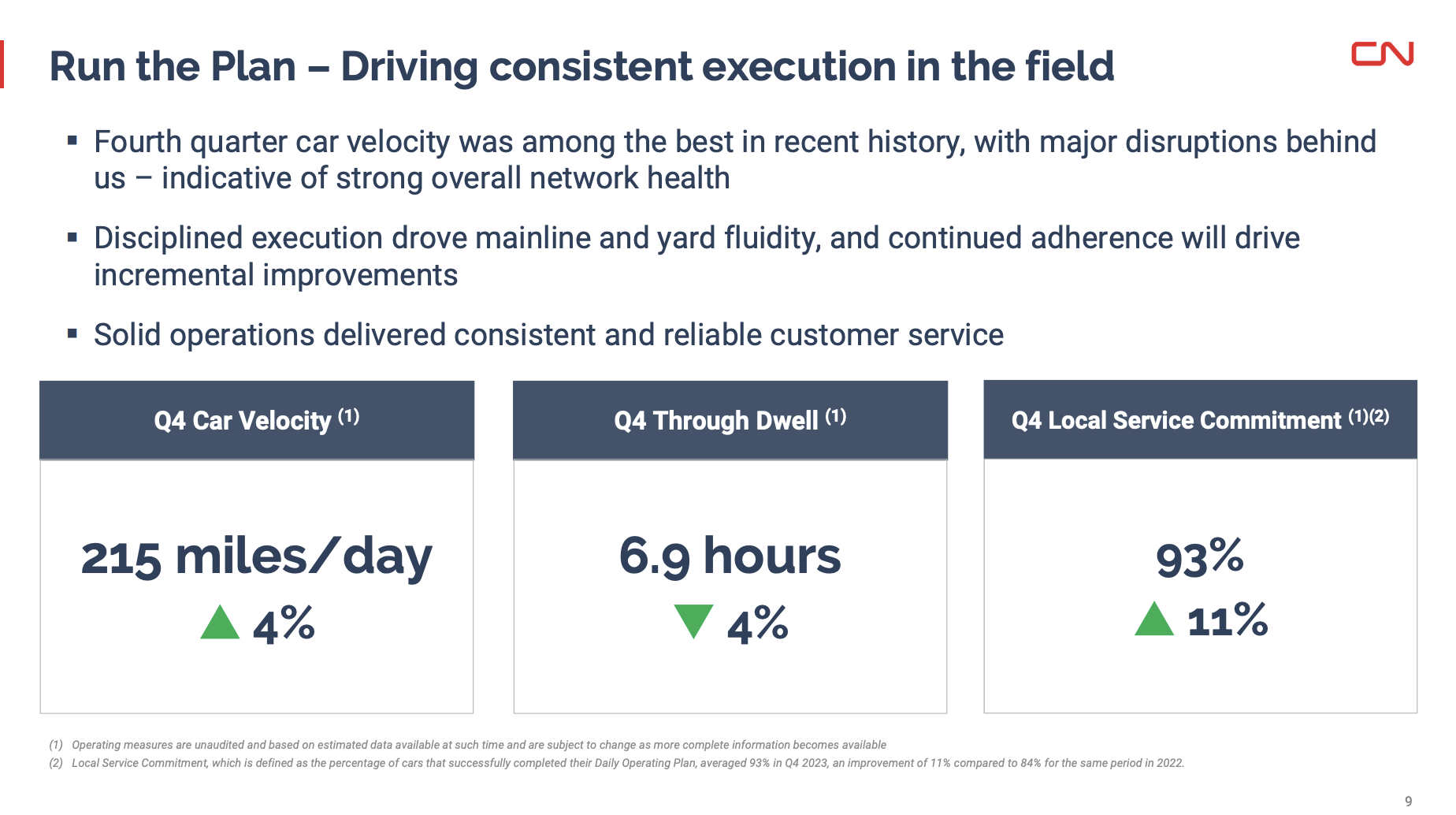

Speaking of improvements, the company improved its operations even further, which is critical in an industry that battled inefficiencies after the pandemic, although this impacted U.S. railroads more than the two Canadian railroads.

In addition to achieving a record-low industry rate among employees, the company achieved an origin train performance of 90%. However, during its earnings call, the company mentioned room for improvement in destination train performance, which stood at 70%.

Furthermore, the impact of the new Canadian Work/Rest Rules on crew scheduling added new complexities, which require more efforts to improve operations.

Nonetheless, there was also good news:

- Car velocity averaged 215 miles per day in Q4, a 4% improvement over the previous year.

- Dwell time showed a notable 4% improvement over the same period.

- Network train speed, while flat in Q4 compared to the previous year, demonstrated a 5% improvement on a full-year basis.

Canadian National Railway

On top of all of this, the company is taking more radical steps to improve its business, including the acquisition of CBNS, which is expected to provide opportunities to densify the eastern part of the network in the coming years.

We are proud to be partnering with Genesee & Wyoming to serve existing customers on this line. This partnership will further reinforce CN’s presence in eastern Canada where we believe there will be a growing role to play in the competitiveness of North American trade. It will also enable our network to reach new opportunities in the longer-term, further advancing our strategic agenda of accelerating profitable, sustainable growth. – Canadian National

Additionally, the agreement to purchase Iowa Northern is viewed as a positive step, as it will enhance market access in the Midwest and deepen the network reach, particularly in the Ag business sector.

IANR serves upper Midwest agricultural and industrial markets covering many goods, including biofuels and grain. This transaction represents a meaningful opportunity to support the growth of local business by creating single-line service to North American destinations, while preserving access to existing carrier options. – Canadian National

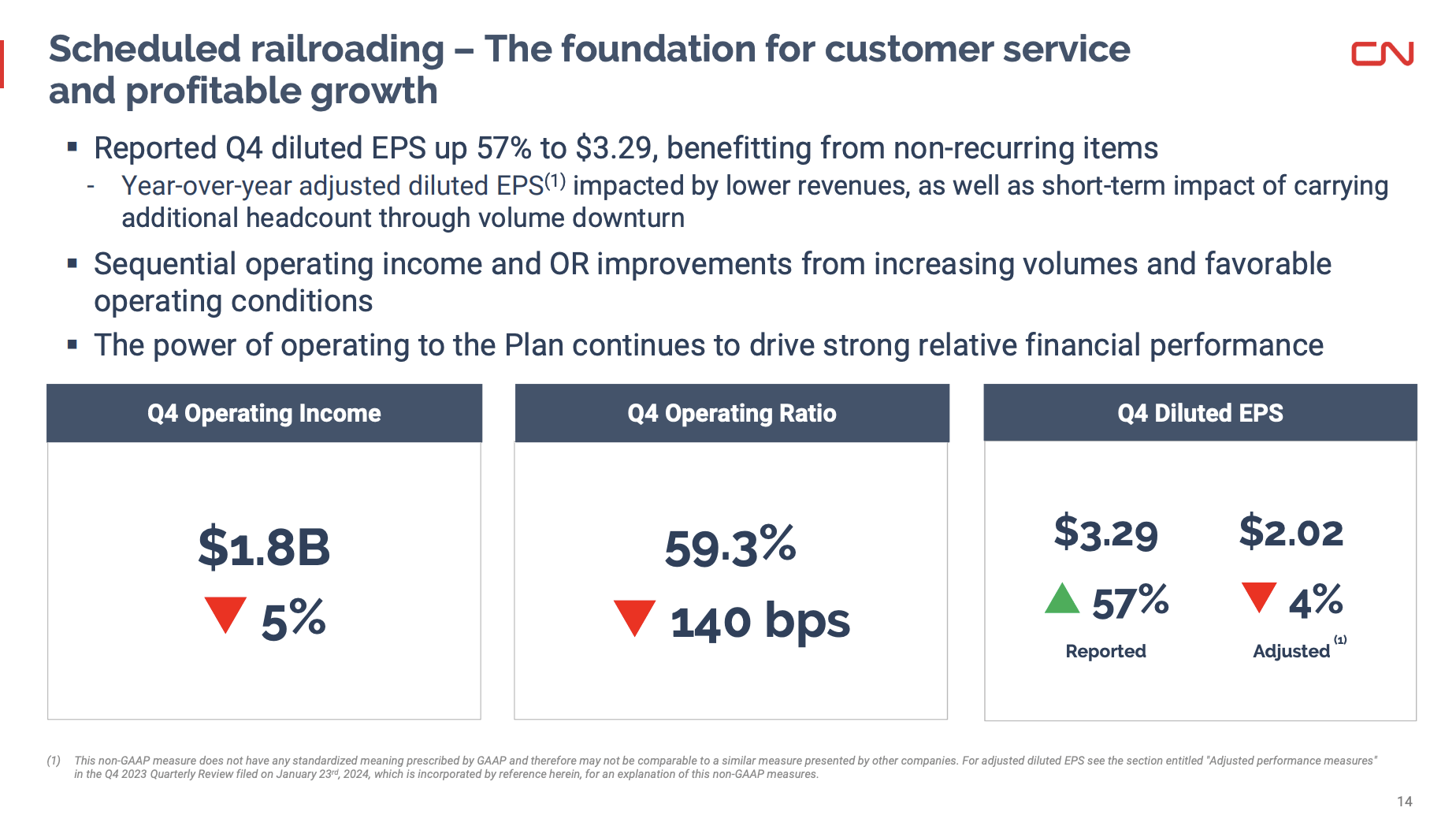

With all of this said, the bottom line during the quarter was weak, as the company reported a 4% decrease in adjusted earnings per share compared to the same period last year.

The operating ratio for the quarter stood at 59.3%, which was a deterioration of 140 basis points.

Canadian National Railway

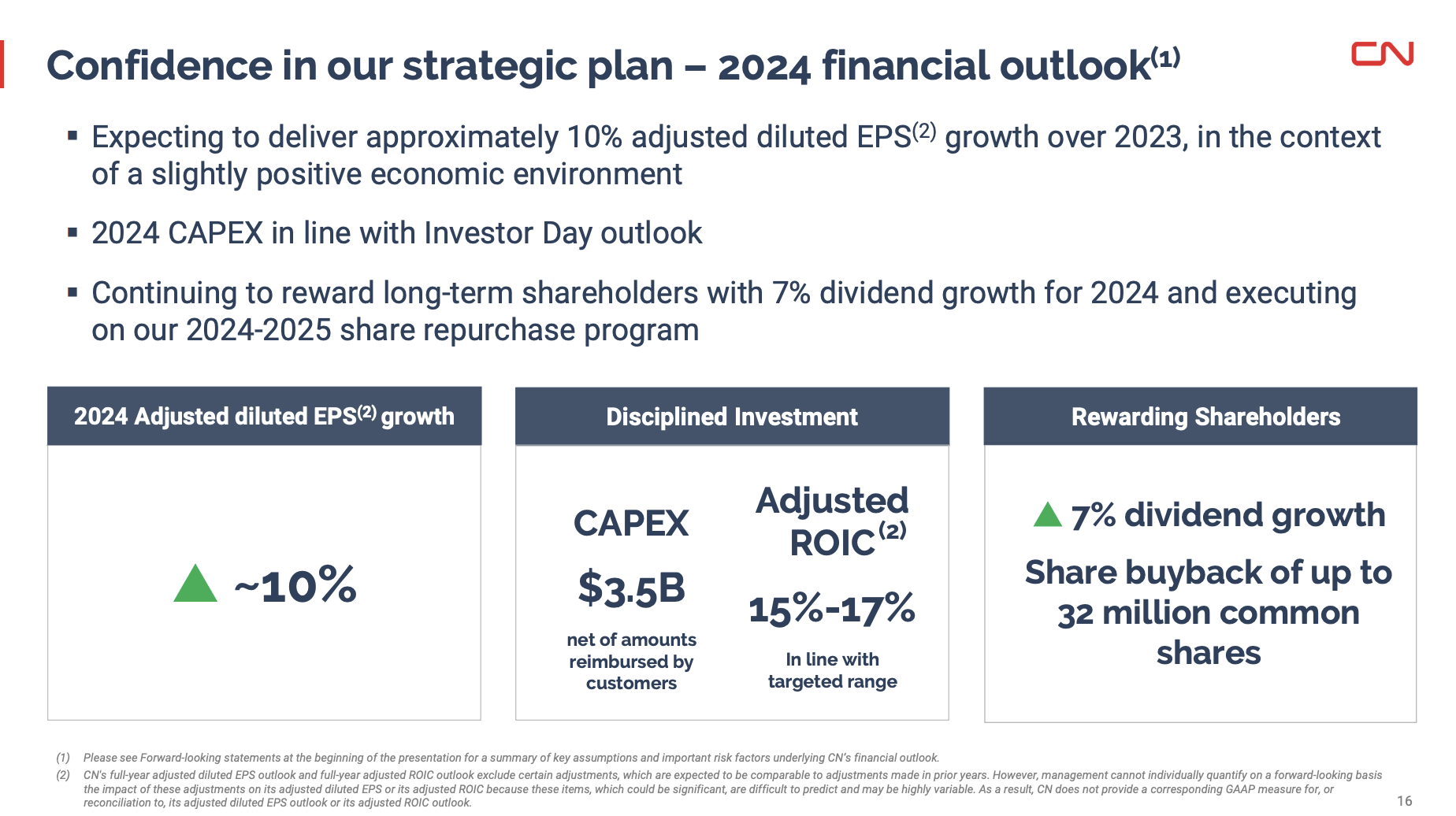

As these numbers were decent – especially in light of economic challenges – the Board of Directors approved a 7% dividend increase for 2024, marking the 28th consecutive year of dividend growth.

Additionally, a new share buyback program of up to 32 million shares, totaling around $4 billion, was announced.

Canadian National Railway

This program is scheduled to run from February 1st, 2024, to January 31st, 2025.

Essentially, the decision to increase shareholder value through both dividend payments and share repurchases demonstrates the company’s commitment to returning value to its investors through direct distributions and indirect distributions that improve the per-share value of the business.

After hiking its dividend by 7%, it now pays $0.845 per share per quarter. This translates to a yield of 2.0%.

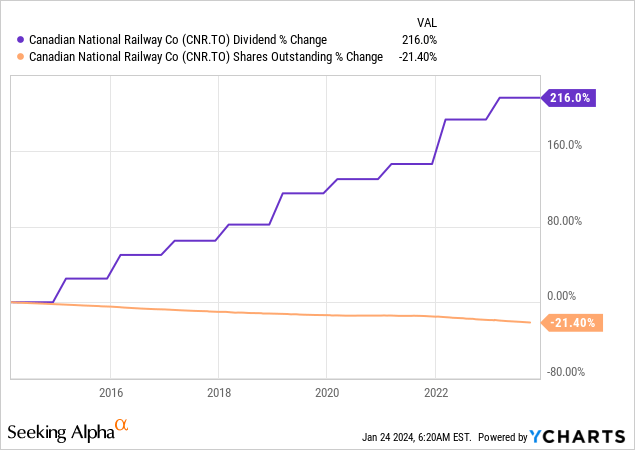

The five-year dividend CAGR is 12%.

Over the past ten years, CNI has bought back more than a fifth of its shares and more than tripled its dividend.

With that said, what about its future?

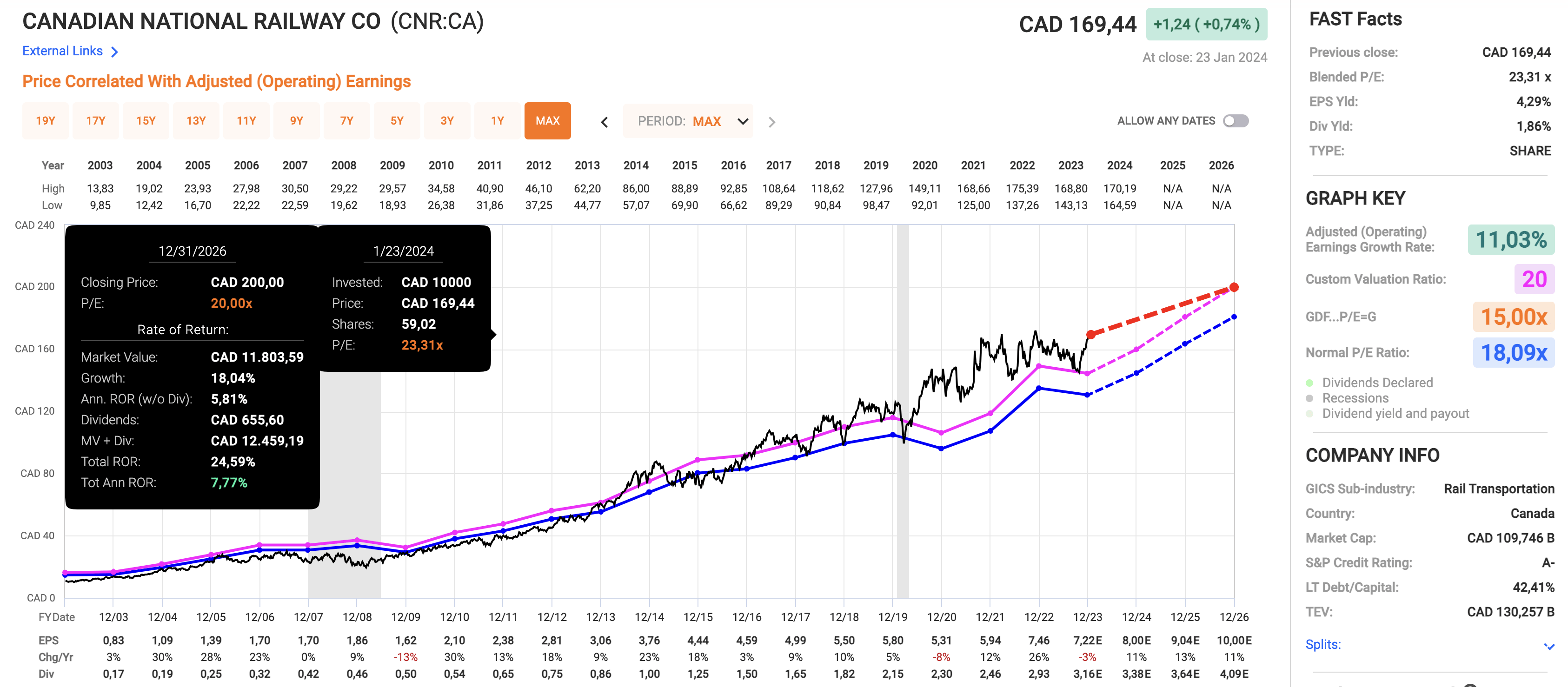

Looking Ahead & Valuation

During its earnings call, the company highlighted its outlook as well, as it expects a more favorable economy in 2024.

It highlighted the expectation of mid-single-digit volume growth based on various factors, such as the aforementioned increased drilling in Northeast BC, new interline partnerships, and positive economic developments.

The company expects to achieve about 10% EPS growth in 2024 compared to 2023.

Analysts agree with the company.

Using the data in the chart below:

- Analysts expect the company to grow its EPS by 11% this year, followed by 13% growth in 2025 and 11% growth in 2026.

- While these numbers are subject to change, they hint at very consistent growth that would warrant a valuation multiple slightly above its long-term normalized EPS multiple of 18.1x.

- Since 2016, CNI has consistently traded close to 20x earnings, which is a valuation that makes sense if it is able to maintain double-digit annual EPS growth backed by tailwinds like economic re-shoring, a stronger intermodal network, and secular tailwinds in commodity shipments like fertilizers.

FAST Graphs

Purely based on the numbers above, the company’s implied annual return is 7.8% through 2026, based on a 20x multiple, its dividend, and its expected EPS trajectory.

Since 2003, Toronto-based CNR shares have returned 15% per year, allowing the stock to outperform the market.

With that said, I’m struggling a bit with what rating to give the stock.

- On a long-term basis, I remain bullish on CNI, as I believe it is one of the best railroads in North America, capable of consistent dividend growth, buybacks, and capital gains.

- After its recent stock price surge, a lot of good news has been priced in, while double-digit EPS growth in 2024 could be at risk if leading indicators like the ISM Manufacturing Index do not bottom soon.

Based on these findings, I decided to go back to a Neutral rating, which I will upgrade if the stock were to decline 10% to 15%, improving the risk/reward, or if we get strong signs of an economic bottom over the next three months.

In other words, if I did not have significant railroad exposure, I would closely watch CNI here for a potential entry in the months ahead, as I believe economic conditions could pave the way for a correction.

Takeaway

Despite the challenging economic environment, Canadian National Railway showed resilience in its fourth quarter.

Despite a 2% decline in revenues, operational metrics like Revenue Ton-Miles increased by 2%, proving the company’s strength amid weakness.

While the bottom line saw a 4% decrease in adjusted earnings per share, the Board’s approval of a 7% dividend increase for 2024 marks the 28th consecutive year of dividend growth. This commitment to shareholder value is further emphasized by a new share buyback program.

Looking ahead, CNI projects a more favorable economy in 2024, expecting mid-single-digit volume growth and a 10% EPS increase. Analysts support this outlook, anticipating consistent growth beyond 2024.

However, due to the recent stock price surge and economic developments, I believe some caution is warranted, making CNI a better buy on potential weakness.

Q2 2024 Earnings Call Transcript")