Guillaume

At the risk of exposing you to yet another article on AI, I wanted to share an anecdote with you. Microsoft (MSFT) recently hit the rarefied $3 trillion market cap level and it reminded me of a conversation I overheard between two guys while grabbing a hot-bar at Whole Foods the other day. One said that the best and only way to invest in AI was via Microsoft, while the other was adamant that Nvidia (NVDA) was the proper play. It was a decent discussion, so I hung around longer than usual and got a fresh coffee from an auto-serve machine that was within ear-shot. And it got me thinking, what is the best angle for investing in AI: Semiconductors, software or the hyperscalers?

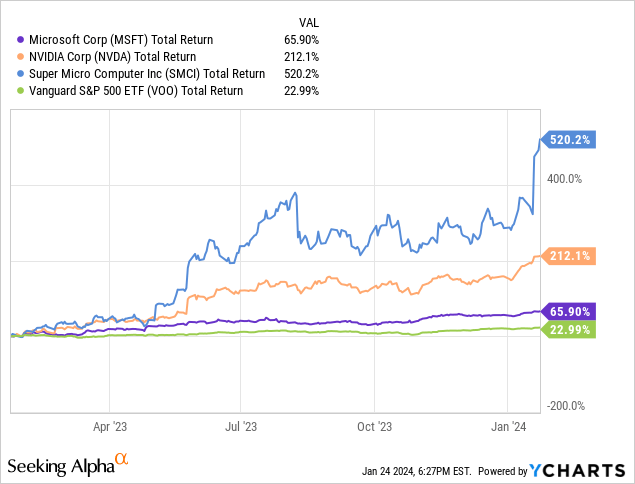

Now, some might advise you simply buy Nvidia, Microsoft and Super Micro Computer (SMCI), call it a day, and – as Tony Soprano would say – just “fuhgeddaboutit!” Indeed, over the past year all three have significantly outperformed the broad market as represented by the Vanguard S&P 500 (VOO) ETF (see graphic below). However, for the majority of ordinary investors, perhaps a more nuanced, less risky, and diversified approach is warranted. Today, I’ll take a look at these three tech sub-sectors – semiconductors, software, and hyperscalers – and discuss the impact AI will likely have on them and why you need to own them. Then, I will offer some specific investment advice to insure you participate in what I consider to be a superior, secular, long-term, growth thesis that will last many years into the future: AI.

Semiconductors

I’m sure you are familiar with the AI investment thesis supporting the semiconductor industry: High-performance computing (“HPC”) requires high-performance processors (like Nvidia’s GPU’s) that are essential to crunching AI/ML algorithms on huge data sets and large-language models (“LLMs”) in order to ring-out the “answers” AI users want to uncover. In order to be highly efficient, HPC requires access to low-latency high-bandwidth data streams which, in turn, require high-speed memory and high-speed networking infrastructure (typically to/from the cloud) in order to keep the processor fed with data. Clearly then, chip-design companies and semiconductor manufacturers that supply the high-performance products in these niche markets are going to be direct beneficiaries of the AI revolution.

Meantime, the semiconductor equipment industry is a critical link in the semiconductor supply-chain because high-end semiconductor equipment technology is, obviously, required to make the highest-performing processors, memory, and networking chips.

Further, if you combine the AI chip supply-chain with demand from a plethora of other tech sub-sectors (IoT, data centers, EVs, 5G smartphones and infrastructure, mobile devices, clean-tech, home networks, just to name a few), the semiconductor sector is no longer the very cyclical industry it once was during the dot.com bust when it was still dominated by PC and automotive demand. Indeed, even during the recent semiconductor “down-cycle,” many semiconductor companies remained highly profitable. These reasons are why, for years now, I have been so bullish on the current and long-term prospects for the semiconductor sector and consider them to be a “must own.”

Software

We all know the story about Microsoft, OpenAI, and ChatGPT (if you don’t, consider reading my article OpenAI: Hoisted By Its Own Petard – And Microsoft’s Big Win and the comment section as well). Obviously, Microsoft has been an early and visible mover in actually monetizing AI by integrating its OpenAI based tool – CoPilot – into its software offerings (and charging a fee for it: $30/user/month for Microsoft 365).

However, it would be simplistic in the extreme to think that Microsoft will be the only beneficiary of AI in the software sphere. Indeed, most all of the leading software companies operate SaaS-based platforms and business models that are driven by annual recurring revenue (“ARR”) subscriptions. These platforms can be very efficiently scaled-up to add new customers and features (i.e. margin expansion) and generate strong free cash flow. As a result, and just like the semiconductor industry, there are many high-growth and differentiated software companies – across a variety of application specific niches – for investors to consider. Many of them are much smaller than Microsoft and therefore offer the potential for significantly higher growth rates. Bottom line: In order to benefit from the AI revolution, investors need direct exposure to the leading software companies.

Hyperscalers

Then we have the hyperscalers: Amazon (AMZN), Microsoft (MSFT), and Google (GOOG) (GOOGL) – each of which have carved out very profitable and growing cloud operations: AWS, Azure, and Google Cloud (“GC”), respectively. Each of these companies is ideally positioned to capitalize on the need for practically all companies to digitize their data and move it to the cloud. The cloud is where the LLMs and the mega datasets are going to reside. In a nut shell, AI is going to be a critical driver of the hyperscaler’s cloud offerings because they can enhance the services, security, efficiency, and cost effectiveness of a customer’s operations.

Combine the cloud narrative with the fact that each of the three big hyperscalers can also leverage AI across businesses other than their cloud segments, and you can see why I feel investors need to have direct exposure to these companies. I already mentioned how Microsoft integrated CoPilot into its Microsoft 365 software. For Amazon, it’s using AI to improve its e-commerce logistics and advertising businesses (among others). Google has been using AI for years with its Deep Mind asset and to optimize monetization of Google Search. The combination of the cloud operations with the ability to monetize AI across other business lines make these hyperscalers compelling investment opportunities.

So What’s An Investor To Do?

Those of you who follow me know that I advise all investors to build well-diversified portfolios. And you have probably already figured out where I am going with this. That is, it’s clear there will be multiple AI “winners” and that it’s critical for investors to have adequate exposure to all three of the technology sub-sectors discussed above: Semiconductors, software, and the hyperscalers.

Now, you could argue that is exactly what you have in your favorite S&P 500 ETF, right? And you would be correct, you do have exposure to all three of those sub-sectors in the S&P 500. However, it’s obviously a significantly watered down exposure, right? That said, and as I have consistently advised investors, I do believe that most ordinary investors should build their portfolios on a foundation of the S&P 500. After all, research shows that the vast majority of ordinary investors (and even the majority of professional money managers …) fail to achieve the long-term returns that they could get by simply investing in the S&P 500 and then, once again, simply “fuhgeddaboutit!”

However, many investors want to exceed the returns of the S&P 500, and that’s why I advise them to also manage a “growth” category within their portfolios. Equities in the “growth” category generally have a higher risk/reward ratio. And this is exactly what we are looking at with many of the AI-centric investment opportunities I am discussing today. The primary risks in these companies is two-fold: market volatility (caused by a variety of factors) and the valuation premium you pay for growth (i.e. discounted future cash flow).

Now, there are three primary ways to invest in the AI revolution: Individual stocks, ETFs, or a combination of the two. My followers won’t be surprised that I advise the combination approach: Owning both some key individual stocks along with some well-diversified ETFs.

Specific Recommendations

For investors who aren’t hardware nerds and don’t know all the ins-n-outs of computer architecture, interface bandwidths, and optical networking interfaces. And for all the investors who are not software weenies and are not up-to-date with all the SaaS-based software platforms, ARR streams, and potential for AI integration and productivity enhancements. And for all of you who simply can’t decide on what hyperscaler might be the best stock because their cloud operations are attached to other businesses which have complex interactions with AI of their own, guess what? I advise you take a diversified approach using ETFs with a smattering of individual stocks that you are familiar with, are comfortable with, and can easily monitor (hopefully with the help of excellent contributors here on Seeking Alpha).

Semiconductor Recommendations

When it comes to the semiconductor sector, and despite my background was as an electronics engineer focused on logic, systems, chip, and architecture design, I have struggled over the best way to participate in the sector as an investor. That’s primarily because there are just so many excellent semiconductor and semi-equipment companies out there that I had trouble picking just a few. That is, I didn’t want to own 10-15 semiconductor companies to get the exposure I wanted and then have to track and monitor them all within a portfolio that already had too many other equity holdings.

As a result, I ended up making it simple: I established full-positions in both the VanEck Semiconductor ETF (SMH) and the domestically oriented SPDR S&P Semiconductor ETF (XSD).

I chose the SMH ETF because I wanted strong and diversified exposure to Nvidia (the No. 1 holding with a 21.8% allocation) and Taiwan Semiconductor (TSM) – which makes the highest performance chips on the planet and is currently the No. 2 holding with a 9.2% weight. I bought XSD because I liked its equal-weight approach that re-balances into 25 companies with a 4% weight. I have covered both of these ETFs extensively on Seeking Alpha, my latest articles being SMH: You Need Exposure To The Vibrant & Lucrative Semiconductor Sector and XSD: “Xtra” Semiconductor Diversification.

In addition, years ago I found Broadcom (AVGO) to be a compelling opportunity. Broadcom has dominated the high-performance networking market for years because it operates what is arguably the best networking development platform in the industry (i.e. both hardware and software validation). The company’s CEO, Hock Tan, focuses on high-margin businesses and as a result the company generates a ton of free cash flow, enabling Broadcom to be the best dividend growth company in the S&P500 over the past five years (the current annual payout is $21/share). For more information on AVGO, consider reading my Seeking Alpha article: Broadcom: CEO Shakedown – Hock Tan Vs Tim Cook. While the term “rock star” is used way too often in my opinion (right up there with “heros” …), clearly Hock Tan has established that he can hang with any of the best CEOs in the technology sector.

Software Recommendations

As mentioned earlier, my engineering background is in hardware and I know just enough about software to be dangerous. That being the case, I decided long ago to participate in the software sector via a diversified ETF, and the one I chose, and am happy with, is the iShares Expanded Tech/Software ETF (IGV). See IGV: Every Investor Needs Diversified Exposure To The Software Sector for a more detailed description.

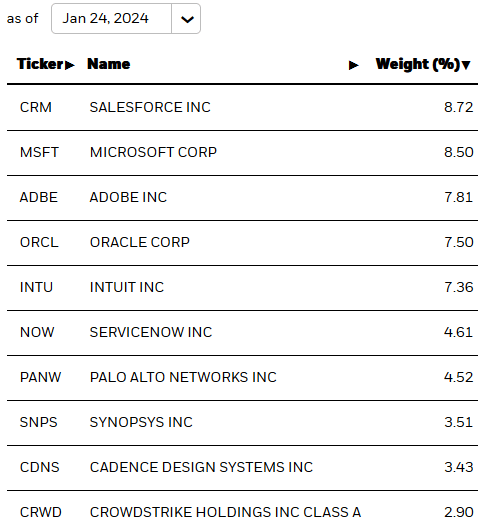

To give you a flavor of the IGV ETF, the current top 10 holdings are:

iShares

As you can see, this is a well-diversified fund across a variety of software applications: Customer relations management (CRM), enterprise software, tax-prep, cybersecurity, and chip-design automation and simulation companies.

Datadog (DDOG) is an up-and-coming software company to consider. DDOG aggregates, monitors, analyzes, and secures data and, being significantly smaller than Microsoft, arguably has a better chance of actually growing faster (see Datadog and 2 Other Sure-Fire AI Winners).

Hyperscaler Recommendations

I would argue that one reason Microsoft is one of only two companies to ever reach a lofty market-cap of $3 trillion is because it operates in two of the spheres we have been discussing here: It’s a software company and also a hyperscaler cloud provider (i.e. Azure).

Google also is a hyperscaler, and one could argue that it too is a software oriented company because at the end of the day “Search” is both a software and networking based construct.

With AWS, Amazon also is a hyperscaler but it’s easy to see that its e-commerce platform, as well as many of its other services (i.e. Prime, advertising, etc), are software driven.

The point here is that, as mentioned earlier, the hyperscalers will benefit from AI not only as a result of their cloud computing offerings, but also because they can leverage AI across their other businesses. That being the case, they’re compelling investment opportunities in my opinion and my advice is that all investors should have direct exposure to at least one of the hyperscalers (if not two, or possibly all three).

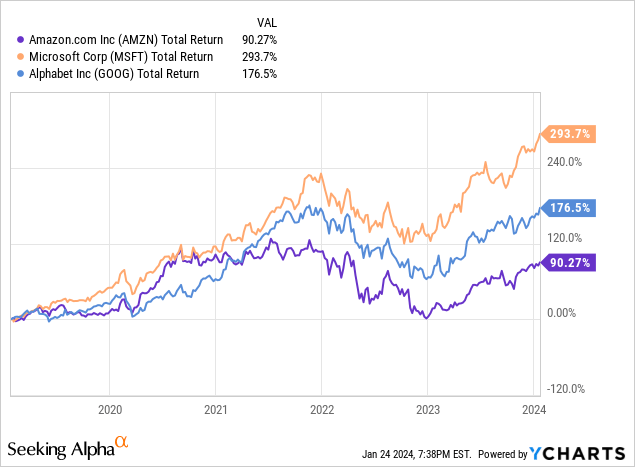

The chart below shows a five-year total returns comparison of the three big hyperscalers:

Interestingly enough, the market leader in cloud (Amazon’s AWS) is the poorest performer over the past five years. However, I attribute that primarily to the fact that AMZN was investing heavily in infrastructure to capitalize on its e-commerce growth potential due to COVID-19. I expect the company to make a strong comeback as capex declines and monetization of prior spend (and AI …) comes to the fore.

The Lines Are Blurring

Investors should forget the antiquated notion that semiconductor, software, and hyperscalers somehow operate in a single tech sub-sector or “silo.” I say that because the fact is many of the best positioned companies to benefit from AI have operations that bleed into areas other than the one in which they are typically defined to exist.

For example, one of “semiconductor company” Nvidia’s critical competitive advantages lies in its CUDA software platform. CUDA enables users to easily optimize running their applications on Nvidia’s GPUs (you can get a free CUDA toolkit here). So, in essence, Nvidia is both a semiconductor and a software company.

Similarly, “semiconductor company” Broadcom – primarily known for being a supplier to Apple (AAPL) and as a provider of high-end networking products – has used M&A to establish itself as a major player in the enterprise software space. Indeed, as I explained in an earlier Seeking Alpha article (see Broadcom: A 20:1 Stock Split Is Likely), Broadcom’s acquisition of VMWare was likely motivated in part by what Hock Tan explained on the Q4 conference call:

Well, as you may be aware, in the last VM Explore in Las Vegas, VMware came out and announced in partnership with NVIDIA, the VMware Private AI Cloud Foundation. Another way of describing it is, the VMware Cloud Foundation Software Stack, the whole VCF stack runs Nvidia coder, runs the Nvidia GPU. That is the partnership. So, if you’re an enterprise, it’s a very easy step to get into gen AI analytics because the data center that you as an enterprise own on-prem that runs VCF will by default run the Nvidia GPU software stack as well. Another way to put it, it virtualizes the Nvidia GPU.

So, if you are Hock Tan and Broadcom, what better way to sell more high-speed networking equipment than to offer your enterprise software customers an integrated and easy way to run AI analytics on Nvidia’s GPUs? After all, as explained before, efficiently running AI/ML algorithms on Nvidia’s high-performance GPUs requires low-latency high-bandwidth access to data. Thus, these customers will need high speed-networking infrastructure to keep feeding data to/from the GPU.

My point is this: Some of the best positioned companies to benefit from AI going forward have operations that blur across traditional sub-sector definitions and are increasingly both semiconductor and software companies. In addition, note that both Amazon and Google have been designing AI specific chips for years (if memory serves, Google is now on its fourth generation AI silicon).

Risks

Now, obviously the broad market indexes, the tech-sector, and many of the leading AI names are all currently trading at or near all-time highs. That being the case, I advise investors to take a patient approach to investing in the themes discussed above. That is, start with a top-level strategy and then determine what percentage of your portfolio you would like to allocate (if any) to the three tech sub-sectors mentioned in this article. Then determine which specific equities within each of those sub-sectors you want to own. Please don’t get hung up on my specific picks. While the hyperscaler options are relatively limited and straight forward, there are many different semiconductor and software companies and ETFs to choose from. If you don’t like my selections, do you own homework and make your own choices. The important thing is to be comfortable and committed to owning these equities for years to come.

Then, establish small starter positions in each of your choices and plan to scale-into (or dollar cost average if you prefer) those positions over time. It took me a couple of years to establish a full-position in the Nasdaq-100 Trust (QQQ), but doing so enabled me to take advantage of market volatility and not go “all-in” at the top. In the era of zero commissions, it’s much easier to economically scale-into your positions over time.

Over the years, I have figured out that I’m much better at establishing small starter positions, being disciplined and taking advantage of market volatility by adding to already established positions during market weakness. And being long-term oriented as compared to being more of a short-term trader.

Higher interest rates always pose a significant risk to the tech sector. We saw what happened in 2022 after Russia invaded Ukraine. That act broke the global energy and food supply-chains, and – although not well reported in the press for some reason – was the primary cause of a rapid spike in global inflation (i.e. oil went to $120/bbl+). That resulted in higher interest rates and effectively ushered in the 2022 bear market which was particularly brutal for the technology sector.

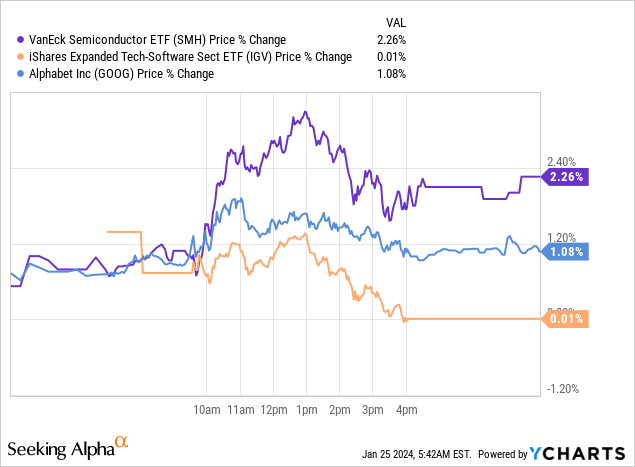

Indeed, just yesterday (Wednesday), tech stocks had a very strong rally right from the start of trading. However, around 1 p.m. (see chart below) tech sold off rapidly and significantly when news that the U.S. 10-year and 2-year Treasury Notes auction went off weaker than expected, and that rates on each rose more than three basis points:

Summary and Conclusion

While some investors and analysts like to frame investments in AI as “hype,” I take a very different and long-term view of the development: AI today is a primary technology inflection point that will be a driver of innovation and productivity for many years to come. There are three primary ways to participate in AI: Semiconductor, software, and the hyperscaler companies. I’m a big fan of all three, and advise investors to take a well-diversified approach via ETFs along with some direct exposure by owning a few choice individual companies. Each investor is different and one size certainly does not fit all. Let your own personal situation and considerations (i.e. age, retired/working, income, goals, risk tolerance, etc) guide your decision making on how to invest in AI. Just make sure you do have exposure to the AI catalyst going forward and for years to come. And I wish you success at doing so.

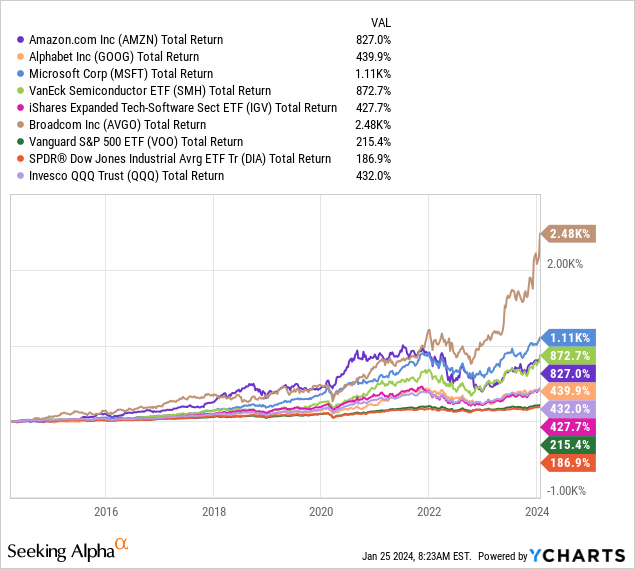

I’ll end with some “food for thought”: A 10-year total returns comparison of some of the equities discussed in this article. Note the significant out-performance of the technology stocks and ETFs as compared to the broad market averages – the S&P 500 and DJIA – as represented by the VOO and (DIA) ETFs, respectively. In my opinion, it’s highly likely that the trend will continue over the coming decade as well (and for years to come after that).

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")