Yuichiro Chino/Moment via Getty Images

Life is what happens to us while we are making other plans. – Allen Saunders

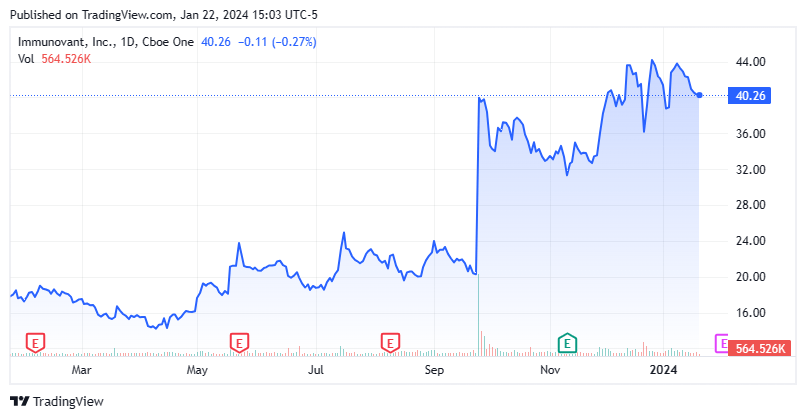

Today, we put mid-cap biopharma concern Immunovant, Inc. (NASDAQ:IMVT) in the spotlight for the first time. As you can see below, the stock has been on a big run since last this summer. The company is targeting some potentially lucrative indications with its primary drug candidate in late-stage trials. Immunovant’s pipeline should have numerous data readouts over the next 18 months as well. Can the rally continue? An analysis follows below.

Seeking Alpha

Company Overview:

This a clinical-stage biopharmaceutical company is headquartered in New York City. Immunovant, Inc. is focused on developing monoclonal antibodies for the treatment of autoimmune diseases. Immunovant is a subsidiary of Roivant Sciences (ROIV) it should be noted.

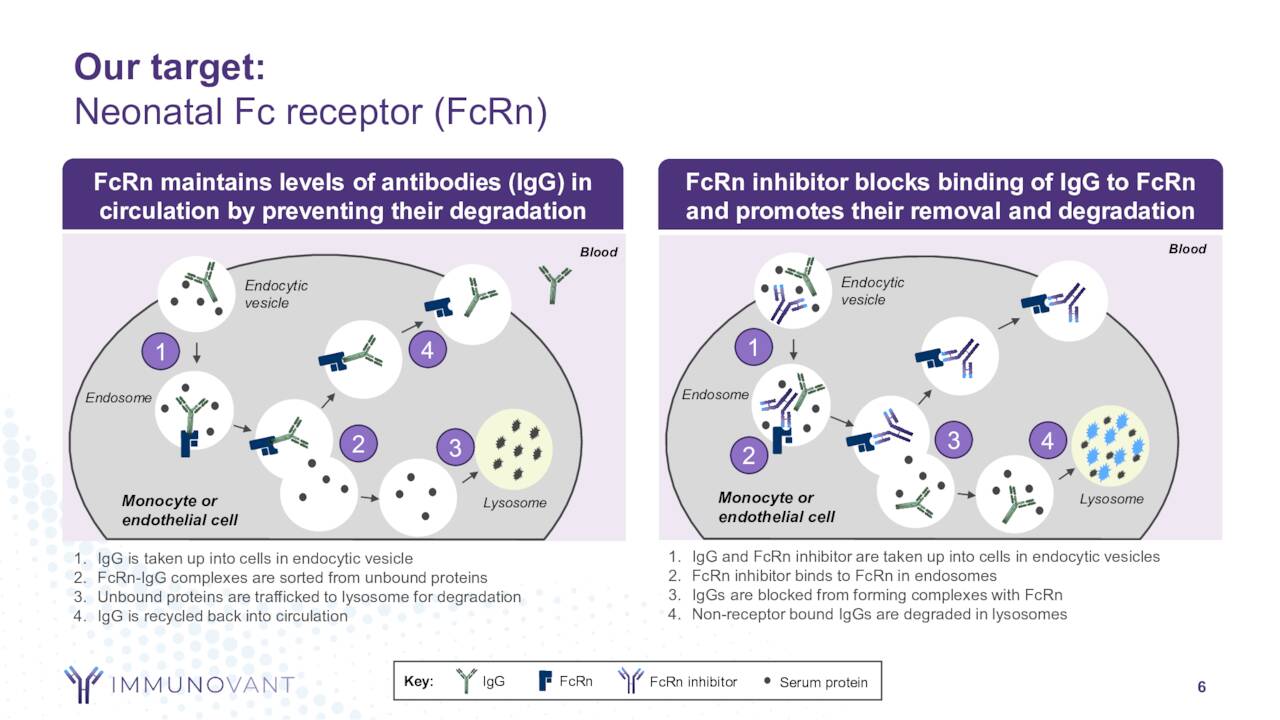

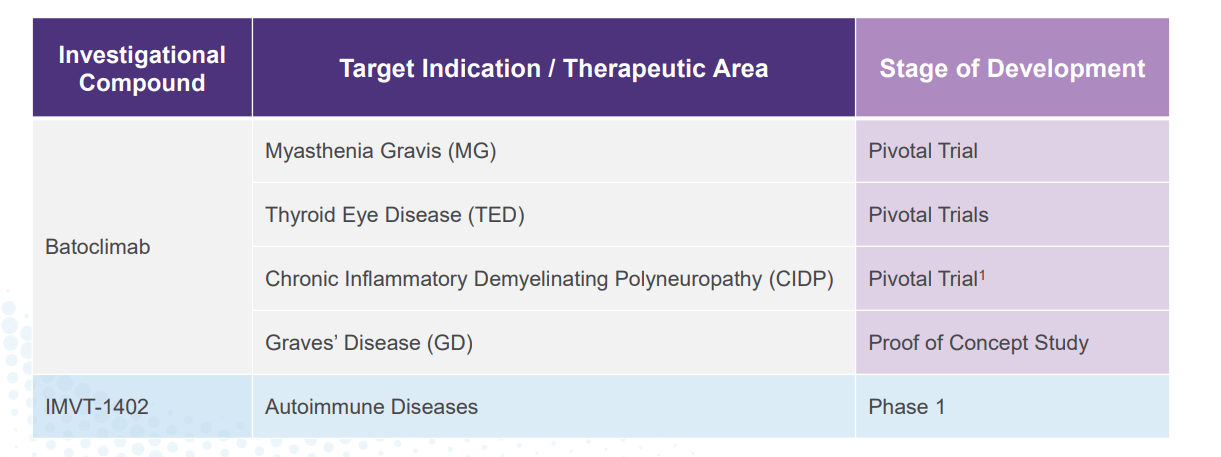

Its lead drug candidate is called batoclimab. This is a novel fully human monoclonal antibody that targets the neonatal fragment crystallizable receptor that is being developed as a potential treatment of myasthenia gravis, thyroid eye disease, chronic inflammatory demyelinating polyneuropathy, and Graves diseases, as well as warm autoimmune hemolytic anemia. The stock trades around forty bucks a share and sports an approximate market capitalization of $5.8 billion.

August Company Presentation

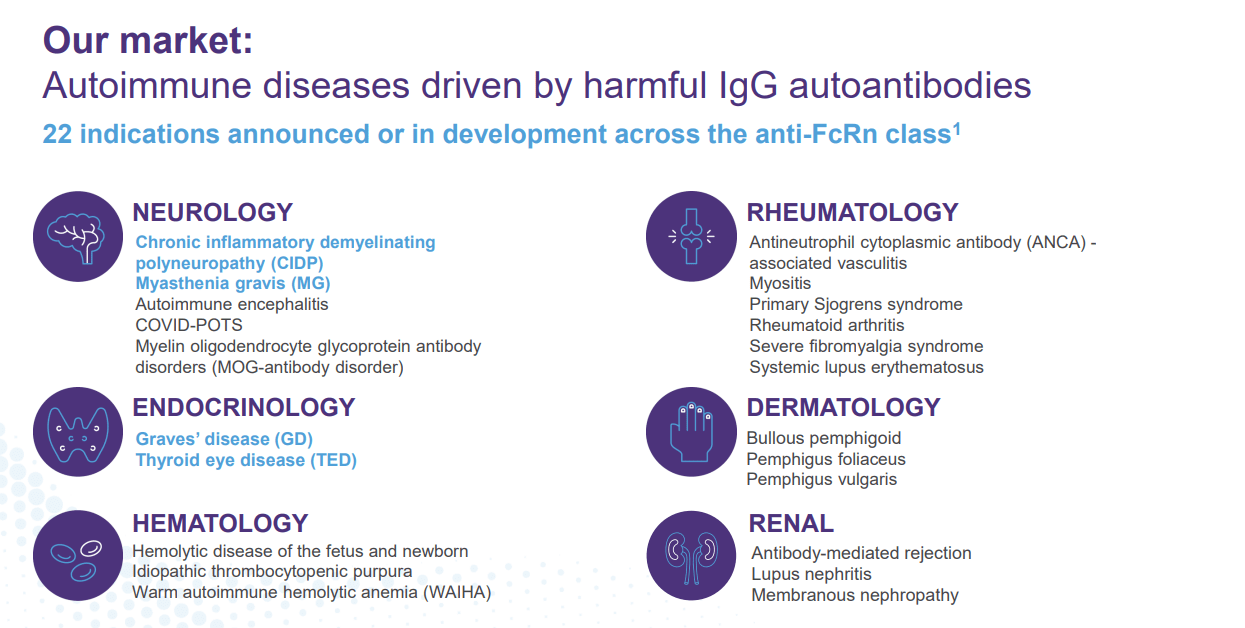

Immunovant is targeting underserved autoimmune disease indications within its developmental pipeline.

January Company Presentation

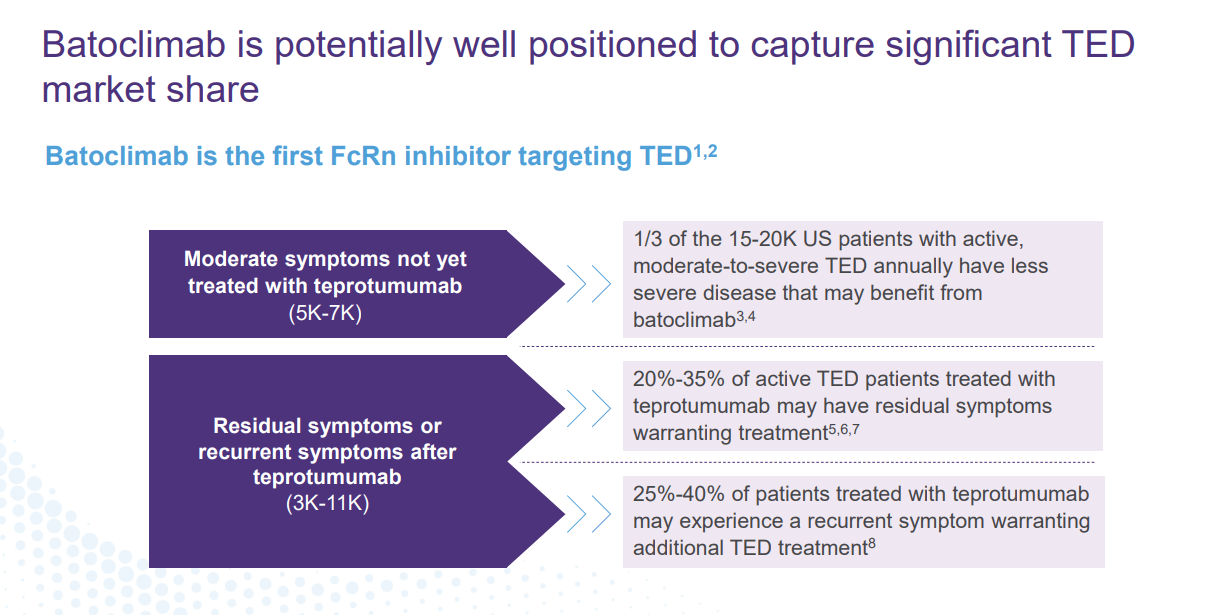

The company’s primary drug candidate is called Batoclimab which is the first FcRn inhibitor targeting Thyroid Eye Disease or TED.

January Company Presentation

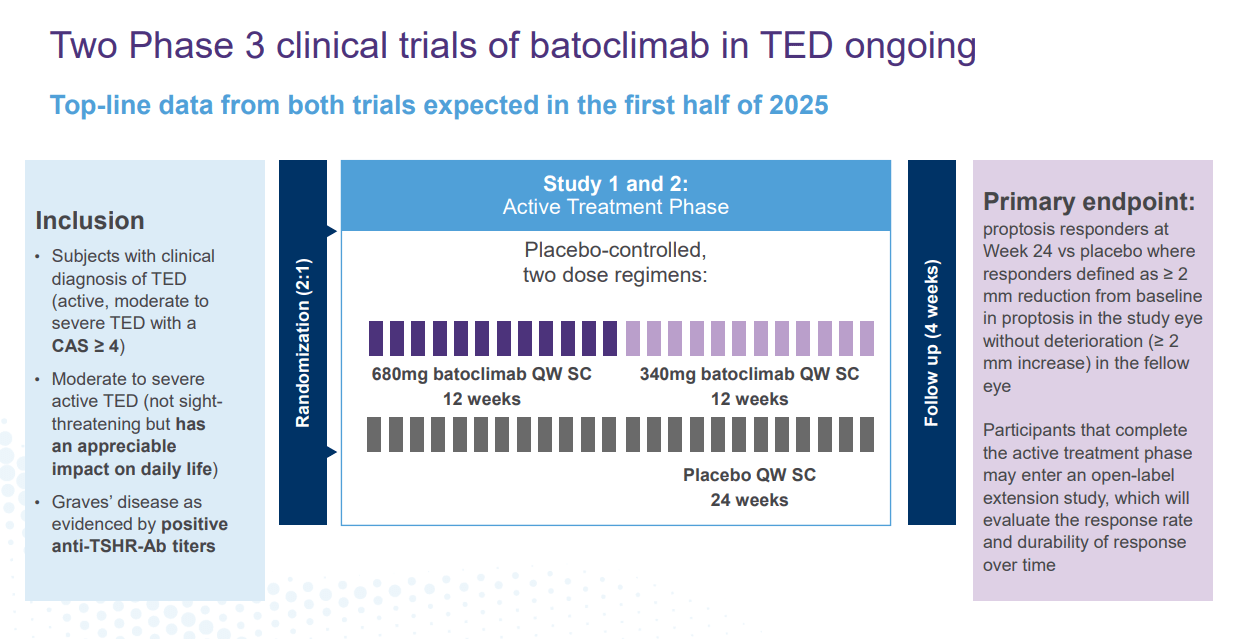

Currently, this drug candidate is being evaluated in two Phase 3 studies to treat TED. Top-line data from both trials are scheduled to be out sometime in the first half of 2025.

January Company Presentation

If eventually approved to treat TED (likely in 2026 based on successful study results), Batoclimab could take market share from the current standard of care Teprotumumab, also known by the brand name TEPEZZA. This compound generated sales of $1.97 billion in 2022.

January Company Presentation

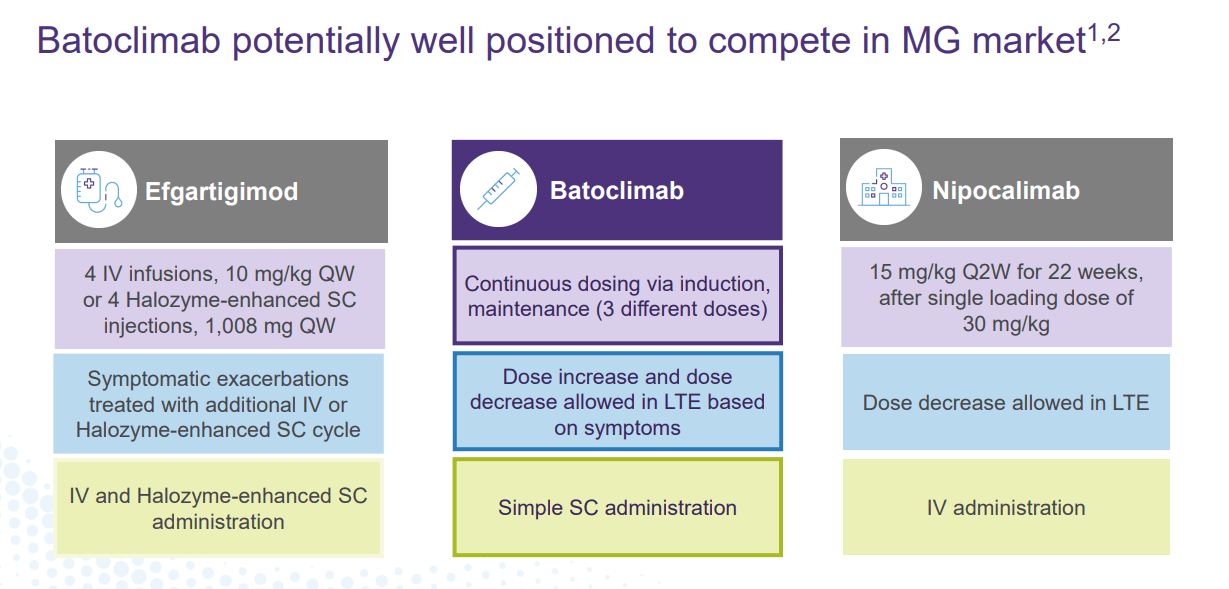

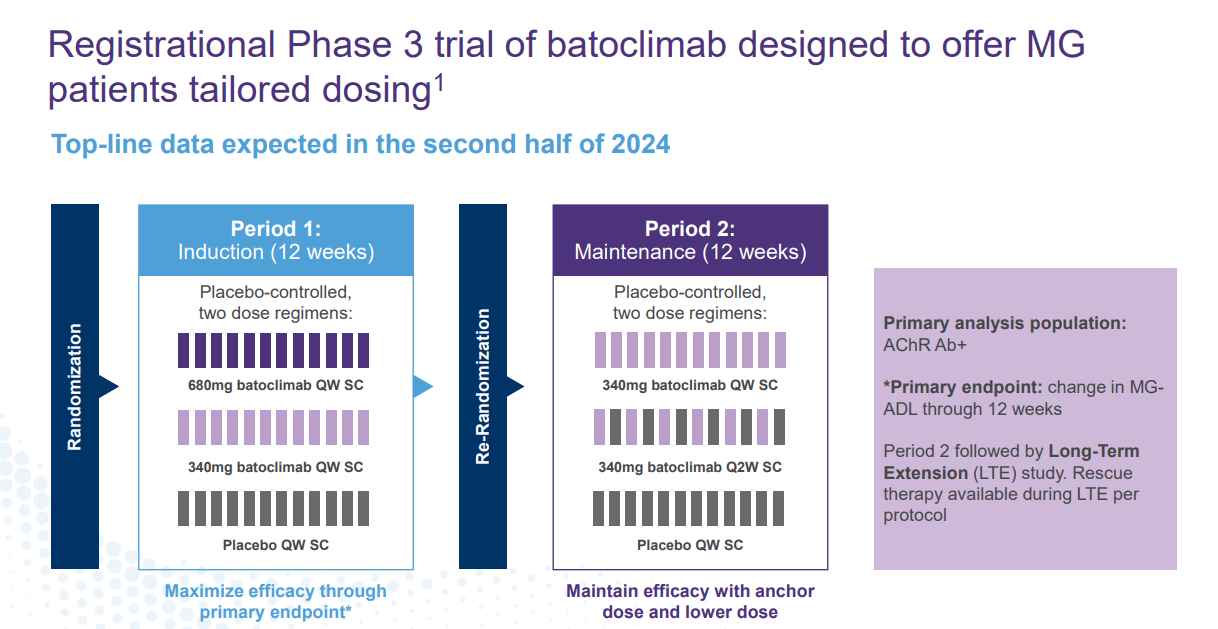

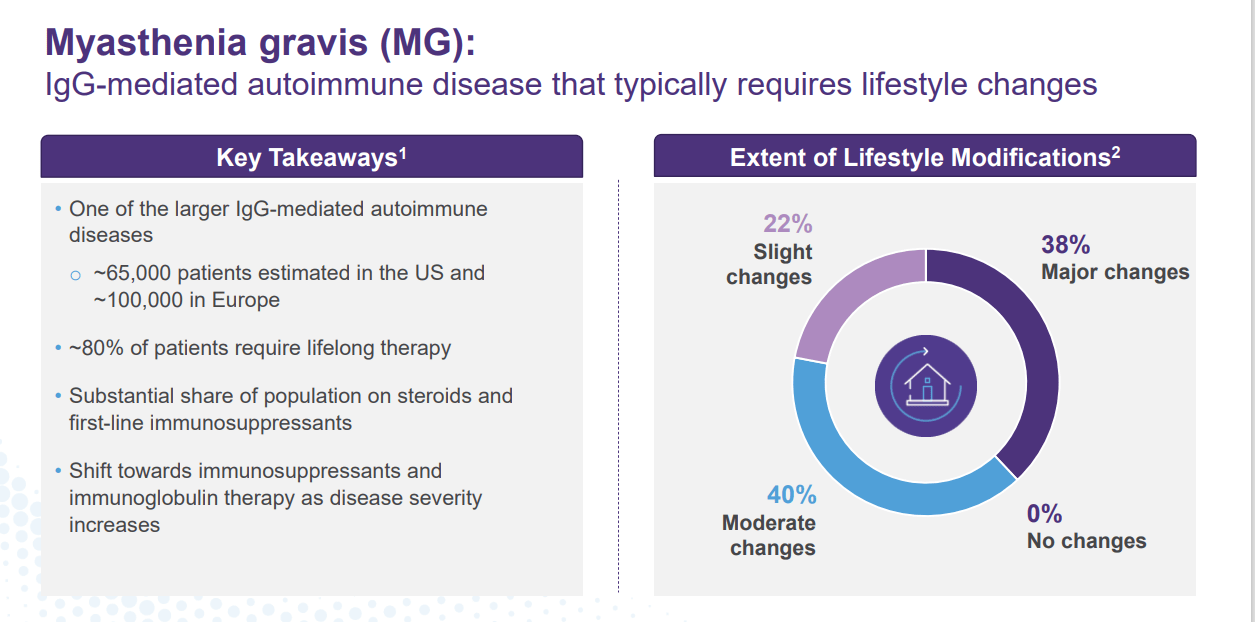

This is not the only indication that Batoclimab is in pivotal trials for right now. The compound is also in a Phase 3 study Myasthenia Gravis or MG. Top-line results from that trial should be out in the second half of this year. If approved, Batoclimab has attributes that should allow it to garner market share from other approved treatments in what is a fairly significant market.

January Company Presentation

January Company Presentation

January Company Presentation

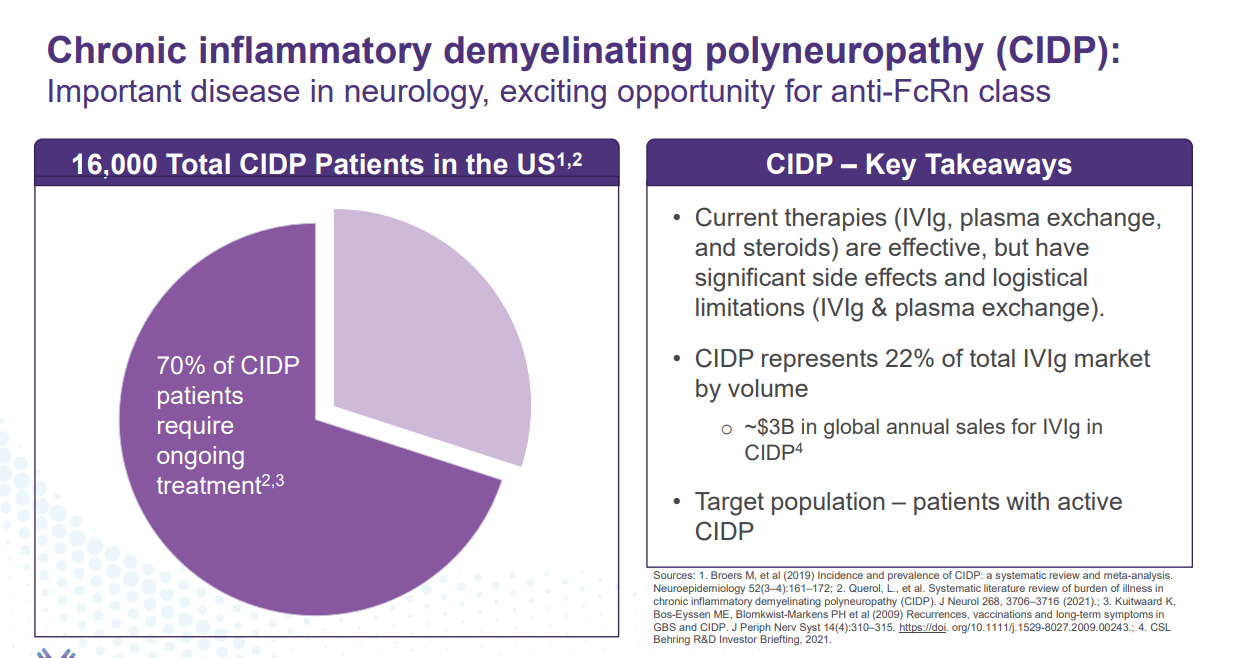

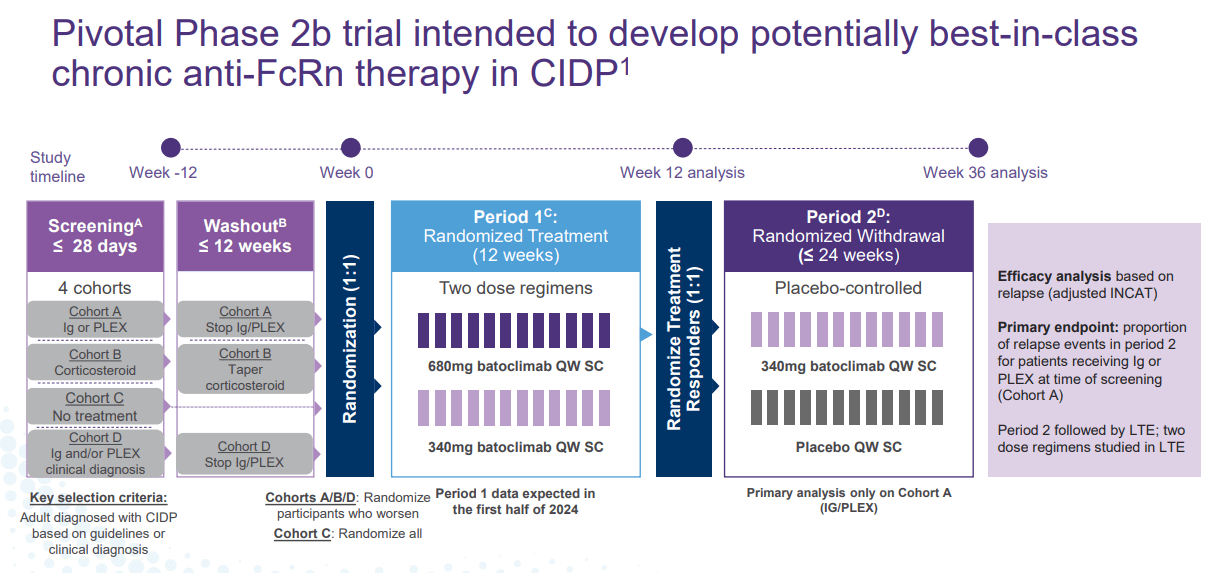

Batoclimab is also targeting Chronic Inflammatory Demyelinating Polyneuropathy or CIDP, another potential large market.

January Company Presentation

The compound is currently being evaluated to treat CIDP in a pivotal Phase 2b trial. Initial data from those efforts should be disclosed sometime in the first half of 2024.

January Company Presentation

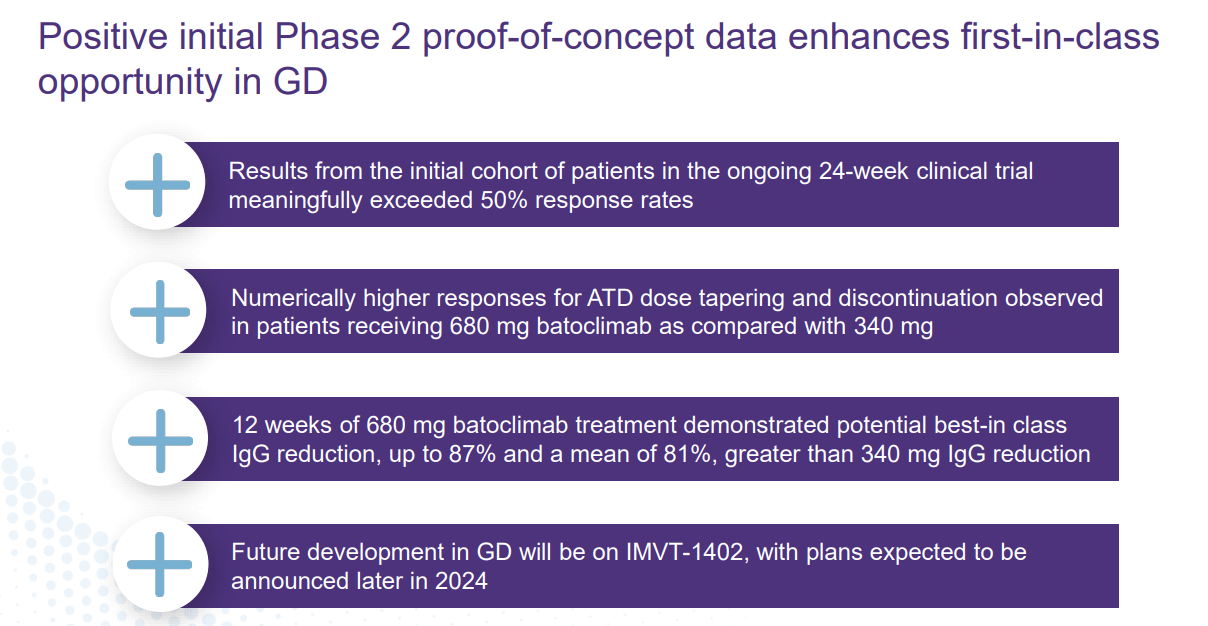

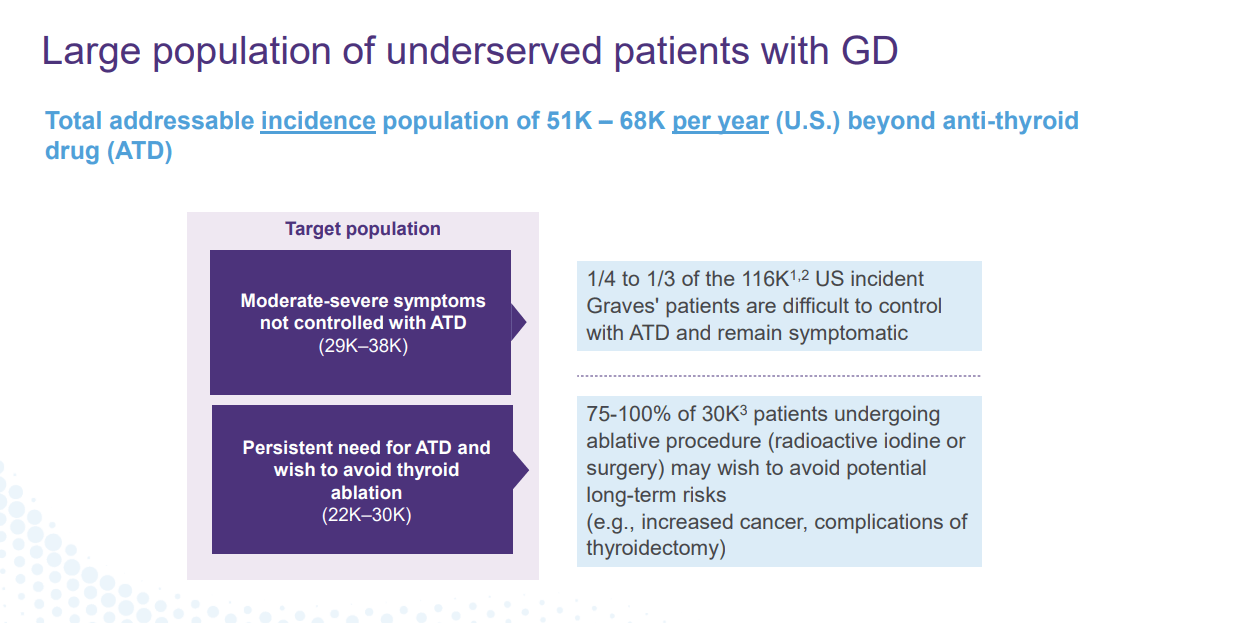

At the close of 2023, Immunovant also posted encouraging preliminary Phase 2 results for its drug batoclimab in the treatment of Graves’ disease.

January Company Presentation

Batoclimab, it should be noted, is the first and only anti-FcRn program targeting this rare affliction.

January Company Presentation

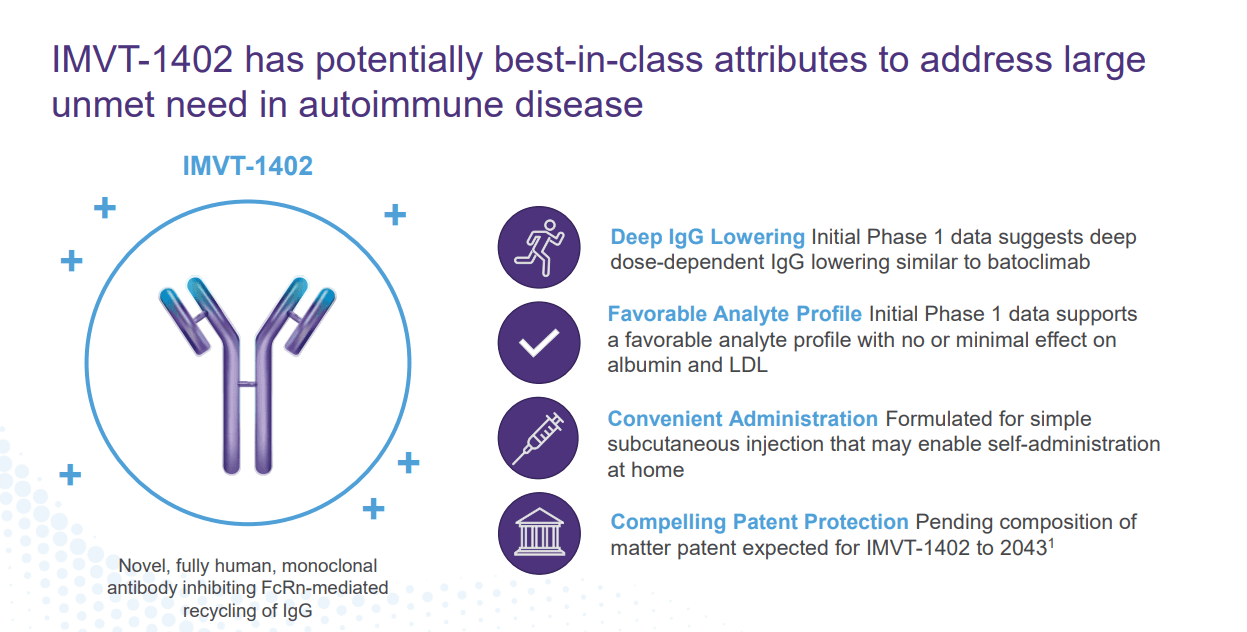

The company also has another compound in development ‘IMVT-1402’ but it is too early stage to be germane to this analysis. It should be noted, some positive early-stage results around IMVT-1402 were posted in late November.

January Company Presentation

Analyst Commentary & Balance Sheet:

Since the company posted its third quarter results on November 9th, eleven analyst firms including UBS, Citigroup and Piper Sandler have reissued/assigned Buy/Outperform ratings on the stock. Price targets proffered range from $48 to $57 a share.

Just under 12% of the outstanding float in the shares is currently held short. Several insiders were frequent and consistent sellers of the shares throughout 2023. So far in 2024, they have disposed of approximately $360,000 worth of equity collectively. After executing a just over $450 million secondary offering right after quarter close, the company ended the third quarter with just over $735 million in proforma cash and marketable securities on its balance sheet factoring in that capital raise. Immunovant had a net loss of $58.7 million in the third quarter. The company listed no long-term debt on its 10-Q filed for Q3. Despite the recent capital raise, the company did file a prospectus for a mixed shelf offering in November.

Verdict:

There is a lot to like about Immunovant’s developmental trajectory. It has a potential blockbuster drug in development targeting several potential lucrative indications. Numerous data readouts are on the horizon and the company recently addressed its near-term funding needs. Given the wholly owned nature of its primary asset, Immunovant could also make a potential buyout target as well.

That said, the stock has nearly doubled from its recent lows in late September. A lot of good news now seems already baked into its current stock price. Therefore, I would wait for a pull back into the low $30’s before I would start to accumulate a small holding in this intriguing name. Options are available against the equity, so a covered call strategy is viable on this stock as well.

It’s choice – not chance – that determines your destiny. – Jean Nidetch

Q2 2024 Earnings Call Transcript")