dimdimich

Co-authored by Treading Softly.

Where I grew up, the rain was always cold. It didn’t matter whether it was the dead of summer or the middle of winter; if it rained, the drops were always cold on your skin. Now, I’m living further south. The rain is warm in the summer, almost like bathwater, and it can still be cool in the winter, but it is never cold like it was growing up. It’s always interesting how the same event in two different locations can have completely different results.

The same can be true when you look at the market or with the workforce. If you were to walk up to your boss and offer him thousands of dollars, but require that he pay you every single month, or three months, money back for perpetuity, he would laugh at you. Yet, that’s what we can do with the market when we invest for income. Unlike the workforce, where you were trading your valuable lifetime for income, you can find quality companies, provide them capital, and have them pay you dividends or interest. This way, rain or shine, it can be raining dividends into your account – no more work required.

Today, I want to look at two great picks that are able to rain dividends into your account.

Let’s dive in!

Pick #1: GHI – Yield 8.8%

Greystone Housing Impact Investors (GHI) is a partnership (which issues a K-1) with a dual strategy.

Its original core business is owning “mortgage revenue bonds” or MRBs. These are bonds originated by state housing agencies to encourage the development of affordable housing. For investors, there is the extra incentive that the interest from these bonds is federally tax-exempt, a benefit that GHI passes along to shareholders through the partnership structure.

GHI’s second strategy has grown over the past 5 years. GHI started a JV (Joint Venture) where they provide capital for the construction of new multi-family housing. The JV builds the apartments, leases them up, and then sells them to other investors for a profit. A fully occupied apartment is worth a premium compared to the cost of construction. This results in large but lumpy returns for GHI. GHI has expanded this strategy in recent years and now has three JV partners executing it.

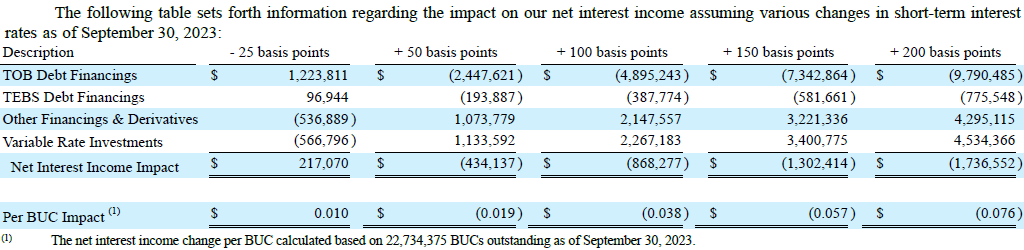

The MRB strategy is inherently a debt investment. Like many other debt investments, it is a strategy that has struggled in a rising interest rate environment. Rising interest rates are slightly negative to earnings, and declining interest rates would be slightly positive. Source.

GHI Q3 2023 10-Q

MRB investments do carry credit risk. While defaults are rare, they do happen. When they do, GHI can foreclose on the property, or more frequently, the borrower gives them the deed instead of a foreclosure. This is how GHI ended up owning and operating Suites on Paseo a 384-bed student housing property in San Diego California. GHI owned a $35 million MRB on the property and when the non-profit organization defaulted, GHI got the deed to the property and has been getting the cash-flows from the property since. Since COVID, the cash flows from the property have been minimal, essentially just covering the expenses. GHI recently sold Suites on Paseo to an affiliate of the University of San Diego for $40.7 million, fully exiting the investment. This illustrates the options that GHI has available to mitigate the impact of borrowers that default.

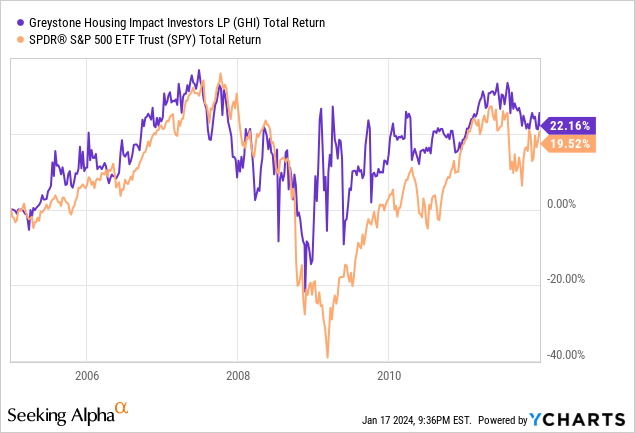

During the GFC, GHI did see a rise in defaults but was able to mitigate them and only reduce its distribution by 8%. As a result, despite being in the real estate sector at a time that was horrible for real estate, GHI outperformed the S&P 500 through the recession.

The MRB strategy proved to be reliable, even in very difficult times.

Today, GHI is more diversified. The Vantage JV has provided increasingly large returns in recent years, and investors have benefited through numerous “special” and “supplemental” distributions. While GHI had to reduce the distribution during COVID, today it is paying $0.37/quarter, which is more than it paid in 2019. Plus, it will be paying a $0.07 supplemental distribution payable in units in January. While it hasn’t announced it yet, the Q3 earnings report stated the intention to also pay a $0.07 supplemental distribution for Q1 2024.

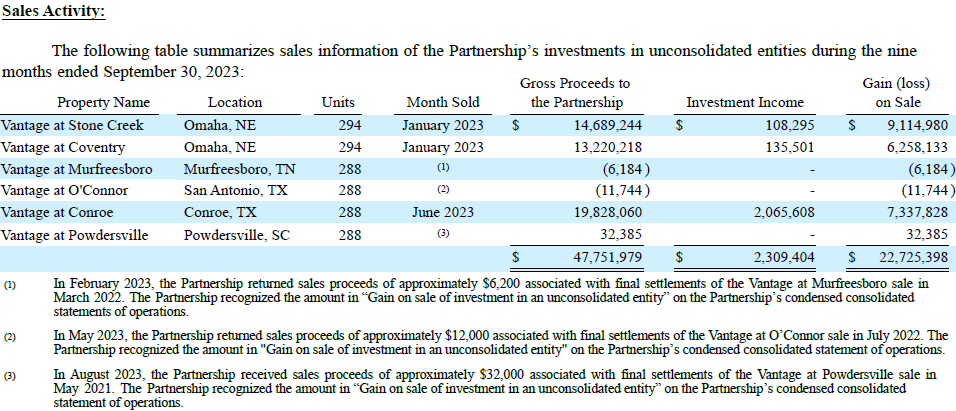

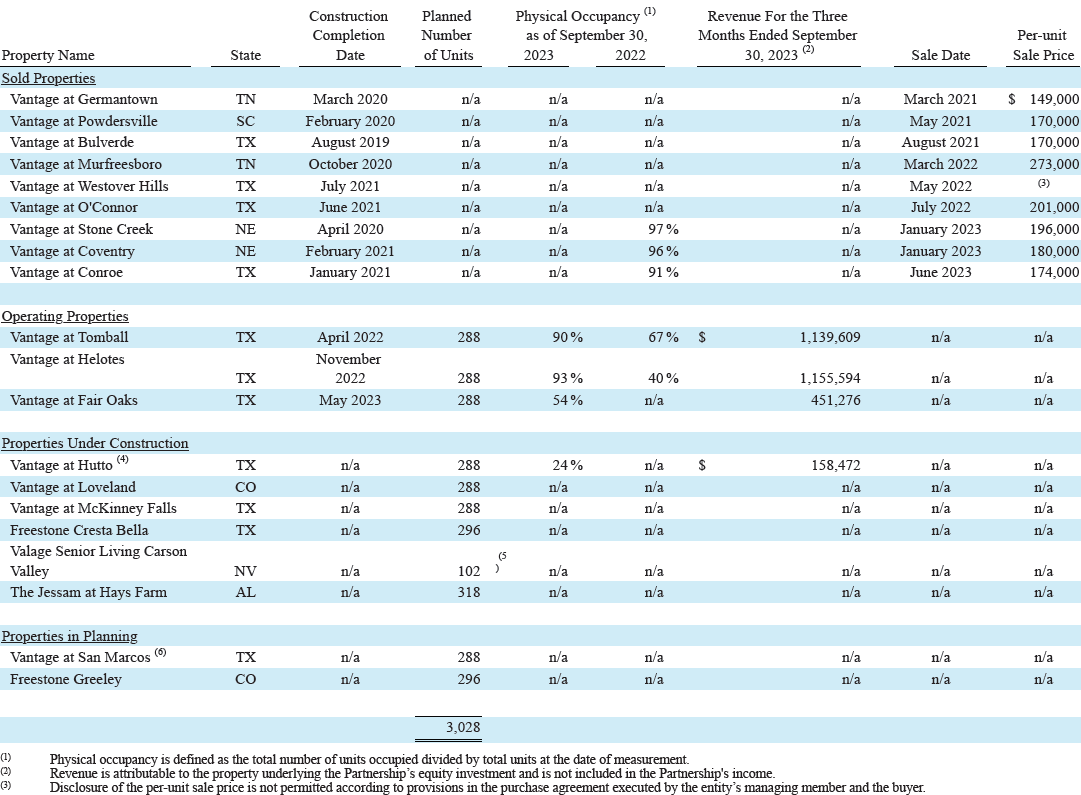

The source of these distributions is their JV strategy. Here is a breakdown of properties in JVs that sold in the first 9 months of 2023:

GHI Q3 2023 10-Q

Note that the gains on sale of $22.7 million are substantial compared to the $47 million in proceeds. However, this is not a fast process; the three properties sold in 2023 were initially started in 2018-2019.

GHI Q3 2023 10-Q

COVID was certainly a disruption in the timeline for these properties, but we should expect an investment cycle of 3-5 years from the start of construction to the sale of the property.

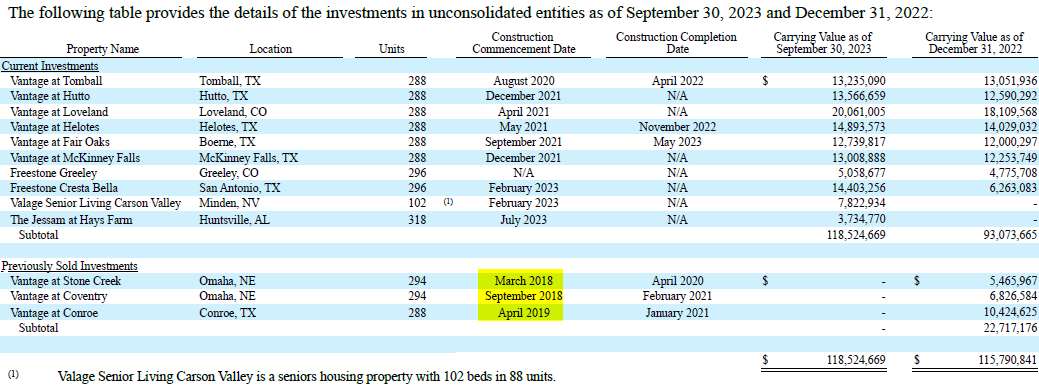

In its 10-Q, GHI provides us with the current pipeline of construction:

GHI Q3 2023 10-Q

GHI has been averaging the sale of three properties per year with this strategy. There are three properties where construction was complete as of Q3 2023, and those are likely to be marketed for sale in 2024. There are another eight projects that are in various stages of development.

The size of future supplemental distributions will be determined by how many of these properties they can sell and the size of the gains they can sell them for.

The $0.37/unit distribution is attractive on its own and should become even more secure as interest rates decline, leading to higher returns from GHI’s MRB strategy. The supplemental distributions are going to be more variable, but GHI’s business model means that it is reasonable for them to be fairly frequent. They should be treated as the “cherry on top”, and at least in Q1 2024, we get to enjoy another cherry.

Pick #2: RQI – Yield 8.1%

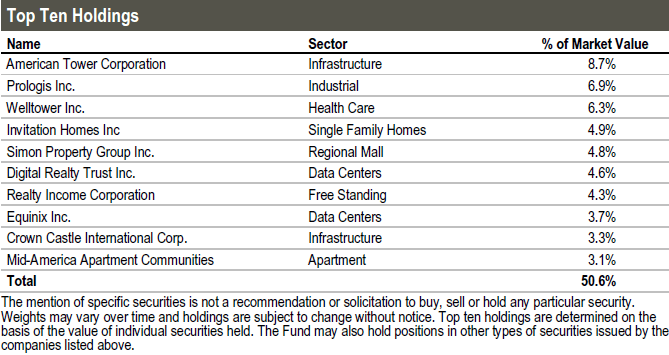

Cohen & Steers Quality Income Realty Fund (RQI) is a CEF (Closed-End Fund) that invests in U.S. REITs. RQI’s strategy is quite simple – it buys REITs that are generally regarded as the cream of the crop in their respective sectors. RQI’s top 10 holdings are rather heavy, with over 50% of the portfolio allocated to them. Source.

RQI Factsheet

You could buy these holdings directly – and if you want to, don’t let us stop you. Every name on this list screams “quality!”. So why buy a CEF when you could buy the stocks directly?

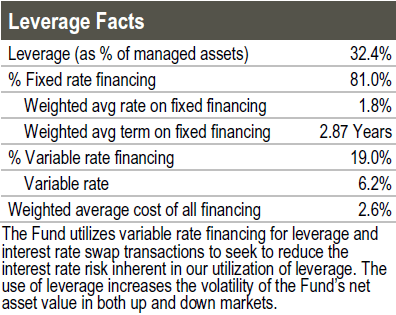

1. Cheaper leverage – RQI is leveraged at approximately 30% of assets. I wouldn’t recommend doing that in your brokerage account; leverage is always better on someone else’s balance sheet. Besides, with swaps, RQI is paying a weighted average interest rate of only 2.6%. Your margin account isn’t going to let you leverage up that cheap!

RQI Factsheet

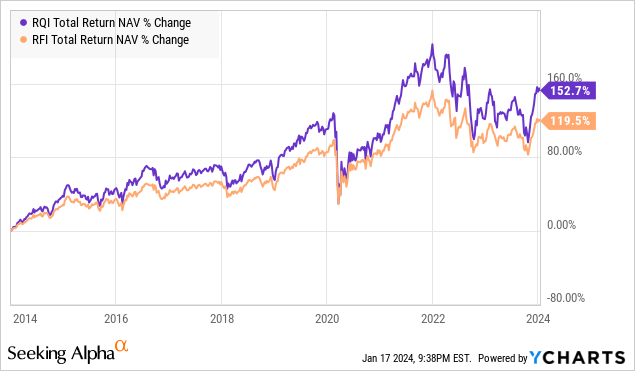

Leverage is a double-edged sword. It increases total returns when the portfolio goes up, and it decreases them when it goes down. Over long periods, RQI has outperformed its sister fund Cohen & Steers Total Return Realty (RFI), which has similar holdings without leverage.

RFI is an attractive option for those who find volatility too stressful. However, in the long run, RQI is likely to continue to provide higher returns.

2. Immediate discount – RQI is currently trading at a 6% discount to NAV. REIT prices rallied at the end of 2023 as the market became increasingly enthusiastic about the idea that the Fed would pivot. Lower interest rates are generally seen as a positive for equity REITs. As the eventual pivot approaches, we expect that REIT prices will continue to rise. If you can get an extra 6% off today, it provides that much room for upside. When the market gets bullish, RQI is a CEF that is capable of trading at a modest premium to NAV.

3. Higher dividends – Like all CEFs, RQI’s dividend includes both income and capital gains. The distribution is set at a level that management believes it will be able to sustain over the long run with capital gains. The reason we don’t hold every REIT on RQI’s top 10 list is that most of them have yields that are lower than our target goals. RQI’s yield is within our target. In short, RQI allows us to follow our investment strategy as an income investment, while gaining exposure to high-quality REITs that wouldn’t otherwise fit our goals. Let the expert management team at RQI decide when to sell and which holdings to sell, while you sit back and collect income.

REITs have momentum coming into 2024. While that could be stalled in the near term if the Fed is slower to pivot than many imagine, it is almost inevitable that the Fed will pivot sometime this year. RQI holds a portfolio that has been benefiting from the market’s enthusiasm towards cuts and will continue to benefit when they actually happen.

Conclusion

With GHI and RNP, we can benefit greatly from real estate. GHI plays a pivotal role in the much-needed, affordable housing landscape through its mortgage revenue bonds investments, as well as through its development of multi-family homes. RQI gives this exposure to a vast number of REITs that will benefit when interest rates start to fall, but also own key real estate all over the country.

Historically, there have been two major generators of long-term wealth. The oldest is being a landowner – someone who owns property can benefit from the value change and the use of that property. The second is the stock market, which arguably has been a greater generator of wealth than anything else in all of human history. When it comes to your retirement, you’re able to have exposure to both through these two picks. This way, not only are you able to enjoy your retirement with strong income pouring into your account, but you’re also able to maintain exposure to the very things that have proved to generate long-term wealth.

That’s the beauty of my Income Method. That’s the beauty of income investing.

Q2 2024 Earnings Call Transcript")