Dragon Claws

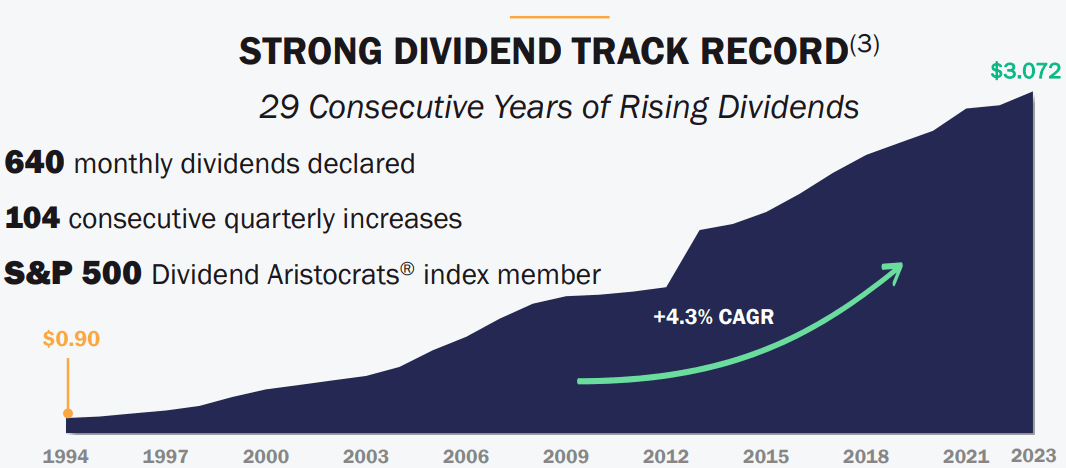

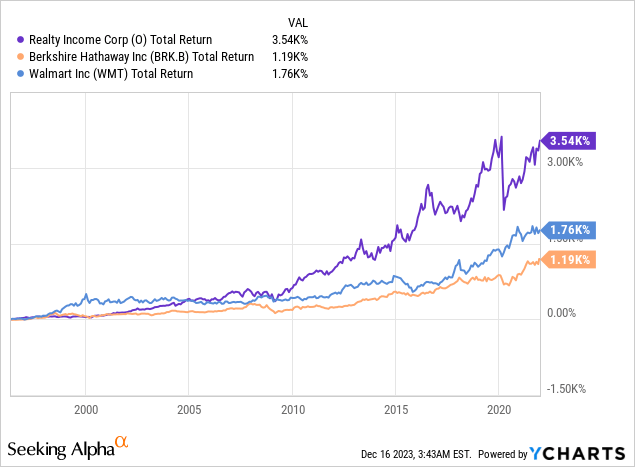

Realty Income (O) is the most popular REIT (VNQ) in the world and it is pretty simple to understand why. It has managed to grow its dividend for nearly 30 years in a row, even despite the dot-com crash, the great financial crisis, and the pandemic. Moreover, it has managed to generate ~15% average annual total returns over this same period, beating even the likes of Berkshire Hathaway (BRK.B) and Walmart (WMT):

Realty Income

But I am sure you have heard the saying that past performance is not indicative of future results and this applies particularly well to Realty Income.

Its past performance was achieved in large parts because the company was small in size and so each new acquisition moved the needle for them. Moreover, it had little competition, it had access to very cheap capital, and this allowed it to buy properties at high cap rates and earn large spreads over its cost of capital.

But things have changed…

Today, the company is massive with a $50+ billion market cap and this means that they have to acquire a huge amount of properties to move the needle. Moreover, new competitors have emerged, interest rates have surged, and spreads have compressed considerably. This is now forcing Realty Income to step into new property sectors, but the REIT market has historically punished such behavior with lower valuation multiples because most investors prefer REITs to remain specialized in one niche.

As a result, Realty Income’s growth has slowed down, its multiple has compressed, and it has become one of the worst-performing REITs in its peer group.

So I would argue that Realty Income isn’t the best net lease REIT anymore. On the contrary, it is now arguably amongst the worst.

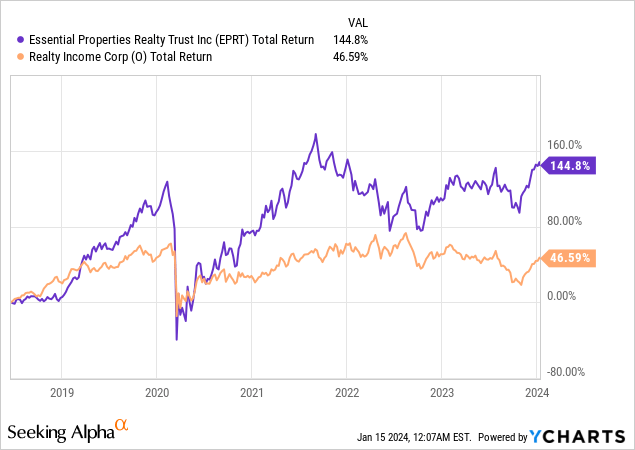

My Top choice is Essential Properties Realty Trust (EPRT).

It has massively outperformed Realty Income since going public and I don’t see that changing anytime soon. Here are three reasons why:

Reason #1: Far Better Growth Prospects

EPRT is a net lease REIT just like Realty Income, but it has managed to earn roughly 3x higher returns since going public in 2018:

This outperformance is the result of its ability to grow at a faster pace.

To give you an example, just this year, EPRT has been guided to grow its FFO per share by 7% in 2023, which is 3x faster than Realty Income:

Essential Properties Realty Trust

This faster growth rate is the result of a few things.

First of all, EPRT is more than 10x smaller in size, so new investments will have a much larger impact on its bottom line. Realty Income’s huge size is a big disadvantage for any REIT that’s seeking to grow externally because it is just a lot harder to grow from a $50 billion base. It needs to acquire over 10x as many properties, so it cannot be as selective.

| Essential Properties Realty Trust (EPRT) | Realty Income (O) | |

| Market Cap | $4 billion | $50+ billion (post-SRC merger) |

Moreover, EPRT has a better business model that earns larger spreads on its new investments.

Instead of targeting net lease properties that are occupied by big-name tenants like Walgreens (WBA) and Dollar General (DG), EPRT is focusing instead on net lease properties that are occupied by smaller middle-market companies. There is far less competition for these properties and it allows EPRT to buy them at higher cap rates, larger rent escalations, and stronger lease terms.

| Middle-market tenants | Big-name tenants | |

| Cap rates | ~7-8% | ~5-7% |

| Rent escalators | ~2% | ~1% |

You would think that smaller tenants would be riskier, but this is not necessarily true because what EPRT lacks in the credit quality of its tenants, it can make up by structuring stronger leases with access to the property-level financials, corporate guarantees, and master lease protections. It also typically buys the properties at a discount to their replacement cost, which limits downside risk whereas other investors will commonly pay a premium for the credit quality of the tenant, but this credit can then worsen over time.

In fact, Realty Income’s biggest tenant, Walgreens was just recently downgraded to “junk” status – causing all of its properties to drop in value.

Realty Income

The proof that EPRT isn’t riskier is in how it performed during the pandemic. That was the worst possible crisis for the company and not even that could take it down. It kept earning steady cash flow and managed to grow faster than Realty Income through the crisis.

Why isn’t Realty Income going after these properties? The answer is that they simply don’t move the needle for them. The ticker sizes are smaller for these properties at $3 million on average so it just doesn’t make sense for a company with a $50 billion market cap.

Reason #2: Less Impacted By the Surge in Interest Rates

Another reason why EPRT is likely to keep outperforming Realty Income is that it has a stronger balance sheet.

It has far less debt:

Essential Properties Realty Trust

And it also has fewer debt maturities in the coming years.

Realty Income has quite a bit of debt maturing this year and next year, but EPRT does not have any maturities until 2027:

Essential Properties Realty Trust

Reason #3: No Premium For Faster Growth

Finally, despite having a stronger balance sheet and growing at a far faster pace, the valuations of both REITs are fairly similar. Adjusted for EPRT’s lower leverage, it may be even slightly cheaper than Realty Income

| Essential Properties Realty Trust (EPRT) | Realty Income (O) | |

| FFO Multiple | 14.5x | 14.3x |

I believe that Realty Income’s cult-like following has kept it trading at a valuation that’s comparable to stronger peers that are growing faster.

And since you are not paying a premium for the faster growth, I don’t see why EPRT wouldn’t keep outperforming going forward.

Bottom Line

Don’t fall in love with your stocks.

Realty Income has done great in the past and I think that it will do alright in the future as well.

But don’t make the mistake of buying it based on its past performance.

Its outlook has deteriorated and I think that many of its close peers, including EPRT, will do a lot better going forward.

Q2 2024 Earnings Call Transcript")