Investment thesis

International Seaways (NYSE:INSW), Inc. is a US-listed small-cap company doing business in international shipments of crude oil and oil products.

Over the past couple of years, 85% of revenue came from contracts that were concluded at spot rates, which has allowed the company to benefit when maritime shipping went through periods of turbulence. For example, as shipping companies have responded to the increased risks associated with Houthi attacks in the Red Sea by diverting ships to alternative routes, International Seaways shares have risen more than 15%.

The company operates a large fleet, which is slightly younger than the average market age. In 2023 it took delivery of three new dual-fuel VLCC tankers, which are much sought after in the market. Plans are to take delivery of two LR1 tankers at the end of 2025.

We have not previously covered International Seaways, so in this review, we will take a closer look at the company’s business structure.

We anticipate that the company will earn a revenue of $1 083 mln (+25% y/y) in 2023, and $945 mln (-13% y/y) in 2024. Revenue is set to decline on the back of a decrease in spot rates. The company’s EBITDA will total $742 mln (+34% y/y) in 2023, and $580 mln (-22% y/y) in 2024. The rating is HOLD.

The business of International Seaways

Incorporated in 1999, International Seaways, Inc. is engaged in the ownership and operation of Marshall Islands-flagged, oceangoing vessels that transport crude oil and oil products around the world.

Before October 2016, International Seaways operated under the parent company Overseas Shipholding Group, Inc. Then a deal happened that led to the emergence of two businesses – OSG and INSW – that had separate management and ownership. On July 16, 2021, International Seaways completed a merger with Diamond S Shipping, creating a joint fleet of 102 ships and making the company the US second-biggest tanker company by the number of ships and third-biggest by deadweight.

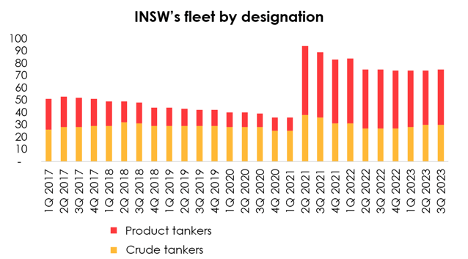

Since then, the company has cut down its fleet as part of an upgrade program, so it currently numbers 30 crude oil tankers and 45 oil-product tankers. The average age of International Seaways’ fleet is 12.6 years, compared with the market average of 12.8 years, which the company noted in its third-quarter presentation.

Invest Heroes Stefan Lambauer/iStock Editorial via Getty Images

According to INSW’s financial results for the past 12 months, crude oil tankers and oil-product tankers make an equal contribution to the company’s revenue. Of the total fleet, as of 3Q 2023, 81% of tankers are owned by the company, and the remaining 19% are leased.

Let’s now take a look at the markets for crude tankers and product tankers separately.

Tanker shipping: crude oil

The company uses the following three types of tankers to ship crude oil:

- VLCC (Very Large Crude Carriers) – large tankers with a deadweight of 200-320 thousand tons (deadweight, or DWT, is a measure of how much weight a ship can carry, including the weight of cargo, fuel, fresh water, ballast water, provisions, passengers and crew).

- Suezmax – oil tankers capable of passing through the Suez Canal with full load; they have a deadweight of 120-180 thousand tons.

- Aframax (AFRA – Average Freight Rate Assessment). Non-OPEC oil exporting countries use this type of tanker because their ports and approach channels are unable to accommodate larger tankers. These tankers have a deadweight of 75-120 thousand tons.

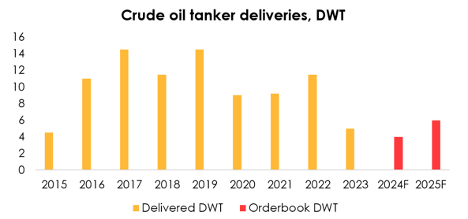

Forecasts from BIMCO and Danish Ship Finance agree that demand for crude oil tankers is expected to exceed supply in both 2024 and 2025. The number of orders to build new vessels of this type will increase too late to alleviate the tightness in 2024 and 2025. The reason: the lack of available slots at shipyards.

MISC

Tanker deliveries are expected to fall to 3.5-4 mln tons of deadweight in 2024, the lowest in at least two decades, before they will rise to about 6 mln tons in 2025, also a low number historically.

Danish Ship Finance

The EIA expects a slight excess of demand over supply in 2024 and, conversely, a slight oversupply in 2025.

According to the EIA, global oil demand will climb by ~1% in 2024, reflecting a slow growth of global GDP and the declining share of this fuel in the structure of consumption by motor vehicles. Growth will be mainly driven by non-OPEC+ countries such as the US and Brazil, while OPEC+ supply, especially from Saudi Arabia and Russia, will depend on voluntary production cuts in 2024.

There are expectations that demand for VLCC will rise in 2024 as the US and Brazil ramp up their long-haul crude oil exports.

According to research by Danish Ship Finance, most barrels from the Middle East are shipped on VLCCs and currently makeup ~40% of China’s seaborne crude imports. Assuming the voluntary oil production cuts by Saudi Arabia and other OPEC members remain in place, OPEC countries in the Middle East will only be able to increase total seaborne exports by 300,000 barrels per day in 2024. China will have to add import volumes from other countries to meet its expected 600,000 barrels per day increase in oil demand. For example, China’s imports from the US and Brazil were a key reason why demand for VLCCs climbed in 2023, and the number of VLCCs going from these countries to China has doubled over the past 6 years. If the trend continues, and with the number of tankers in the fleet remaining almost unchanged, the utilization of the VLCC fleet will increase.

Environmental requirements create hurdles for VLCC vessels.

Almost all VLCC vessels that transported crude oil from Brazil or the US to China in 2023 used conventional fuel, and about a third were more than 10 years old. The Brazil-China and US-China routes stretch over significant distances and require a lot of fuel, which prompts the release of large quantities of greenhouse gases. Older VLCC ships will likely have to reduce speed to meet emission regulations, which will mean longer travel times. That will result in higher utilization of the VLCC fleet and increased demand for dual-fuel tankers.

Thus, in 2023 both freight rates and prices for used crude oil tankers consistently remained at elevated levels. Newbuilding prices also reached all-time highs and this trend is drawing support from the rising demand for dual-fuel tankers.

In 2024 demand is expected to exceed supply with little potential for deliveries of new tankers. However, the imbalance will be smaller compared with 2023, so rates will continue to decline from peak levels as part of seasonal fluctuations. Additional demand for VLCCs could arise if China moves to ramp up oil imports from Brazil and the US.

In 2025 more tankers will enter the market, but demand is expected to grow slower than supply and, as a result, rates will continue to decline. Due to high fleet utilization, we do not think that rates will reach pre-crisis levels.

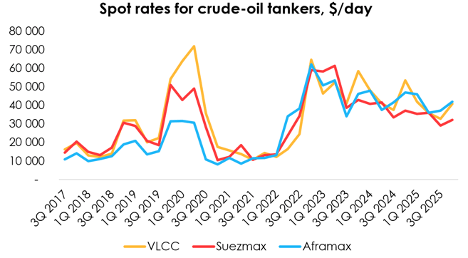

Therefore, here’s the performance of quarterly spot rates for VLCC, Suezmax, and Aframax tankers that we expect, taking into account seasonal fluctuations.

Invest Heroes

The table below shows average annual spot rates for the three types of tankers.

Invest Heroes

Tanker shipping: oil products

The company uses the following three types of tankers to ship oil products:

- LR2 (Long Range 2) – these vessels can call at most major ports and be used to carry both crude oil and oil products. They have a deadweight of 80-160 thousand tons.

The LR1 and MR types of vessels, which have a smaller size, are used to transport oil-product cargoes over relatively short distances, for example from Europe to the US East Coast. Their smaller size allows them to access most ports around the world.

- LR1 (Long Range 1) – a deadweight of 45-80 thousand tons.

- MR (Medium Range) – a deadweight of 25-45 thousand tons.

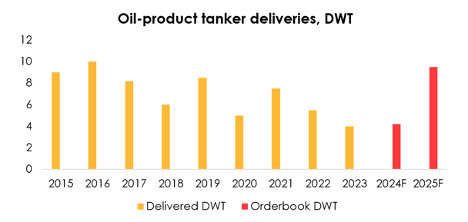

Forecasts from BIMCO and Danish Ship Finance agree that demand for oil-product tankers will almost equal their supply in 2024, while they will be in excess supply in 2025 due to scheduled deliveries of new tankers. According to aggregate estimates, the fleet of oil-product tankers will grow by ~2% in 2024 and by ~4.5% in 2025.

Therefore, supply will expand faster than demand in 2025, which is likely to remove any shortages and make chartering schedules less tight.

Danish Ship Finance

Future hull surveys and upgrades of exhaust gas cleaning systems (scrubber) could occasionally offset the expansion of the global fleet by up to 2% in 2024 and 2025, reducing the risk of excess capacity.

Rising sales of electric vehicles are a factor that restrains the growth in demand for traditional fuels.

According to the IEA, electric vehicle sales shot up from about 1 mln units to more than 10 mln units from 2017 to 2022. In the prior five-year period, from 2012 to 2017, EV sales jumped from 100,000 units to 1 mln units, highlighting the exponential growth of the sales. The share of EVs in total vehicle sales expanded from 9% in 2021 to 14% in 2022 – and that’s more than 10 times higher compared with 2017. In 2023, electric vehicle sales made up 18% of the global total for car sales.

However, the world is still highly dependent on traditional motor fuel.

The International Energy Agency estimates that motor vehicles make up about 60% of the current global demand for oil. This demand is steadily recovering, although motor fuel consumption, for example in the US and the European member countries of the OECD, has not yet reached pre-Covid levels.

Demand for motor fuel is expected to decline over the long term.

Risks to further growth in demand for motor fuel could include subdued global GDP growth, the increasing penetration of electric vehicles, and the continuing trend toward hybrid work.

Eliminating the use of fossil fuels in transportation, especially in the automotive industry, is one of the key strategies aimed at achieving carbon neutrality in the global economy. For example, the EU intends to ban the sale of new cars with gasoline and diesel engines starting from 2035, while the US and China are putting this goal off to a more distant future. The International Energy Agency predicts that automotive vehicles will cease to drive growth in oil demand by the end of the current decade.

Thus, in 2023, freight rates, although still close to historic highs, gradually declined during the year, even as total demand for seaborne supplies of refined products exceeded the levels that were recorded over the same period in the last six years. The prices of used tankers and the prices of newbuilding continue to rise, indicating strong demand for such shipments.

In 2024, as we expect, spot rates will gradually decline, but will be highly sensitive to geopolitical tensions.

In 2025 the fleet is expected to expand the most since 2016 in terms of deadweight. Combined with a demand that could rise by a mere 1% or so, this will put further downward pressure on spot rates.

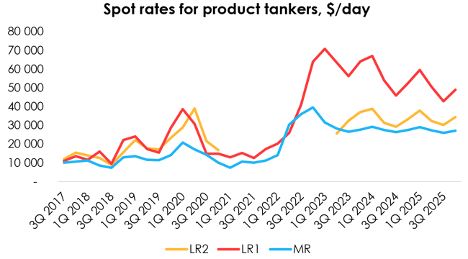

As such, we expect quarterly, seasonally-adjusted spot rates for LR2, LR1 and MR tankers to be as follows.

Invest Heroes

The table below shows average annual spot rates for the three types of tankers in question. In 2021 and 2022 the only LR2 tanker in International Seaways’ fleet operated under a fixed contract, so spot rates are not applicable to these years.

Invest Heroes

Spot and longer-term contracts

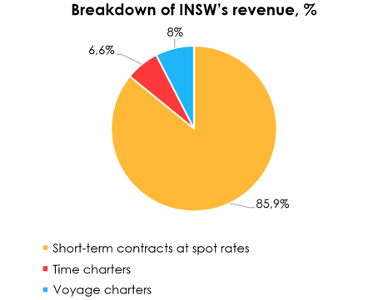

The company derives revenue by providing services through:

- short-term contracts at spot rates;

- time charter contracts for periods ranging from a few months to a few years;

- voyage charters, which are short-term contracts for the period of duration of each specific voyage.

Over the past two years revenue from short-term contracts made up on average more than 85% of the company’s total revenue, while time charters did about 7%, and voyage charters about 8%.

Invest Heroes

Fixed-rate time charter contracts are currently in place for three VLCCs (7-year contracts), two Suezmaxes (until 2024 and 2025), one Aframax (until 2026) and five MRs (duration varies from a few months to 2 years). Fixed rates are mostly lower than spot rates.

Voyage charters generate revenue not only from payments for hiring a vessel but also from lightering services (operations to transfer oil and LNG cargoes from ship to ship).

Financial results

We forecast the company’s revenue based on the number of revenue days for each type of its tankers and the charter rate of their contracts.

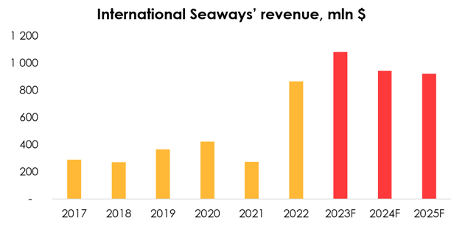

Therefore, we expect the company to earn a revenue of $1 083 mln (+25% y/y) in 2023, and $945 mln (-13% y/y) in 2024. Revenue is set to decline in 2024 due to expectations that spot rates will fall and the fact that contracts based on these rates make up more than 80% of the company’s total revenue.

Invest Heroes

Operating costs

The company’s operating costs include the following:

- Voyage expenses – fuel, port charges, canal tolls, cargo handling operations and brokerage commissions paid by the company under voyage charters. These expenses are subtracted from shipping revenues to calculate TCE revenues.

- Vessel and crew expenses – crew costs, vessel stores and supplies, lubricating oils, maintenance and repairs, insurance and communication costs associated with the operation of vessels

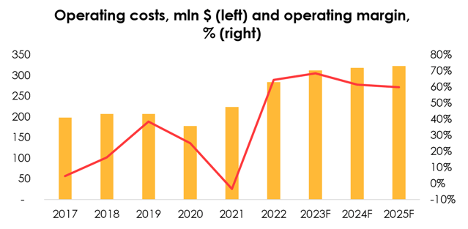

Assuming that larger/lower tonnage tankers require proportionally more/less funds, we project operating costs based on the average costs per 1,000 deadweight tons, which averaged $8,900 over the last 12 months.

Based on the projected number of ships in International Seaways’ fleet and the known deadweight for each of the tanker types, we expect expenses to operate the fleet to reach $312 mln (+10% y/y) in 2023, and $319 mln (+2% y/y) in 2024.

We currently know that deals have been signed for building two LR1s, with the delivery expected in the second half of 2025. There is also an option for two contracts to build additional LR1s, with the delivery time starting from the second half of 2025 and ending in the first quarter of 2026.

Invest Heroes

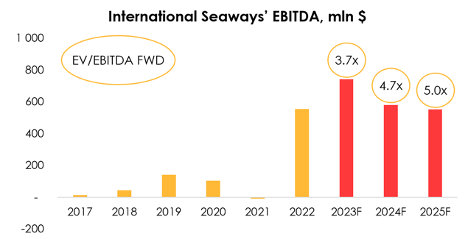

The company’s EBITDA is set to total $742 mln (+34% y/y) in 2023, and $580 mln (-22% y/y) in 2024. The decline is mostly attributable to expectations of lower revenue.

Invest Heroes

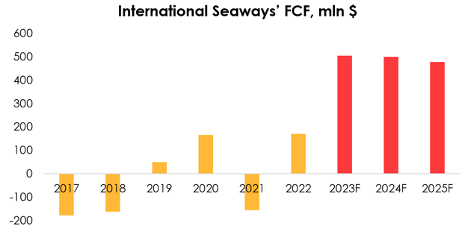

The company’s FCF is set to total $504 mln (+194% y/y) in 2023, and $499 mln (-1% y/y) in 2024.

Invest Heroes

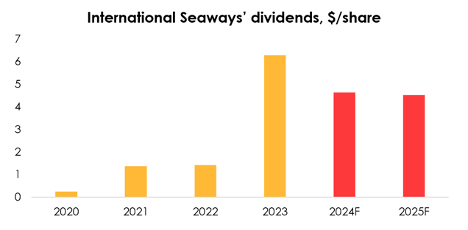

The company pays a quarterly dividend of $0.12 per share, but due to expanding revenue in 2023, along with its regular dividend it four times paid an additional dividend ranging from $1.13 to $1.88, which corresponded to a dividend yield of 13%.

Assuming the company continues to pay additional dividends on the back of strong earnings that are driven by higher-than-historical-average spot rates, we expect the dividend yield to be about 9% in 2024 and 2025.

Invest Heroes

Valuation

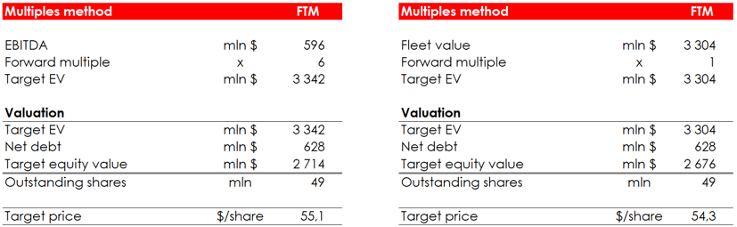

We use two methods to evaluate the company: the method of EV/EBITDA multiples and the EV/market-value-of-the-fleet ratio. The second method reflects that the enterprise value is too low relative to the market value of its fleet.

The target price is $55. The rating is HOLD.

Invest Heroes

Tanker attacks in the Red Sea

Having studied the company’s business and prospects in detail, let’s look at the burning issue for shipping companies in recent months – the Houthi attacks in the Red Sea – and understand if International Seaways’ business is exposed to the risks of current events.

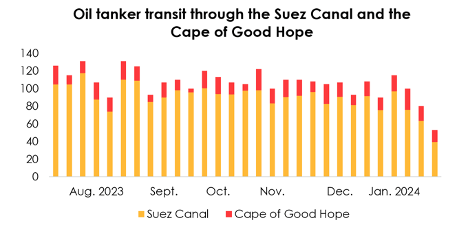

In mid-December, shipping companies responded to the increased risks associated with the Houthi attacks in the Red Sea by diverting vessels to alternative routes. Despite the increased risks, there was no significant reduction in tanker traffic through the end of December, with the exception of container ships, the number of which in the Red Sea has decreased significantly since December 16. This is due to the fact that, according to MariTrace, more than half of the vessels involved in incidents are container ships, and they are the most risky. By the end of December, half of the container ships that regularly transit the Red Sea and Suez Canal were avoiding the route due to the threat of attacks.

In December 2023, the movement of tankers carrying crude oil and petroleum products in the Red Sea was fairly stable. According to the Houthis, they attack ships bound for Israel and mainly non-oil cargo. Additional costs (vessel expenses, insurance costs) were not a major concern for most tanker companies, as the Red Sea remained much more accessible than the route around Africa, but since the beginning of the U.S.-led airstrikes, it appears that more and more tanker companies have decided to avoid the risk and transit through the Cape of Good Hope (making the route almost 1/3 longer) or even cease operations.

Reuters

The U.S. and a number of other countries continue to tighten maritime security, but increasing risks from air attacks have led a significant number of companies to refuse transit through the Suez Canal, which is likely to affect and increase spot oil tanker freight rates. Undoubtedly, the crisis in the Red Sea is creating an even more tense situation in the tanker transportation market.

Conclusion

Based on the aggregate crude oil and refined product tanker data described above, we expect oil tanker demand to exceed supply in 2024 with little potential tanker arrivals.

As the imbalance promises to be smaller than in 2023, spot rates will continue to decline from peak levels but will still be well above historical values over the past 3 years, which will help tanker companies maintain robust financial results.

After a stable December 2023 for oil tanker traffic through the Suez Canal, a significant proportion of companies have stopped transporting oil through this route in January 2024, which is likely to lead to higher spot rates for oil tankers in the near future.

Q2 2024 Earnings Call Transcript")