bennymarty/iStock Editorial via Getty Images

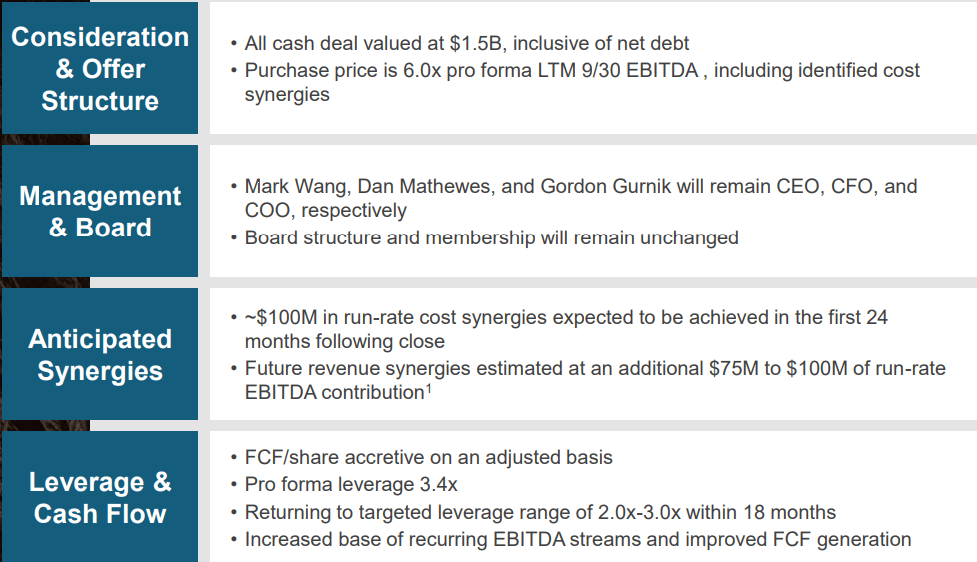

Hilton Grand Vacations (NYSE:HGV) is a timeshare company that was spun off from Hilton Worldwide Holdings (HLT) in 2017 but is allowed to use Hilton names and many of its properties with a special licensing deal. The company recently announced that it finalized the highly anticipated acquisition of Bluegreen Vacations (NYSE:BVH) for a sum of $1.5 billion including BVH’s net debt. The deal was closed using cash and HGV had to borrow money to pay this including $900 million of senior secured notes due in 2032 with an interest rate of 6.625%.

Apparently, the deal is expected to have multiple benefits for HGV. First, the combination of the two companies is expected to have $100 million in annual savings due to synergy within the first 24 months in addition to another $100 million in the longer term. Second, the new company is expected to benefit from larger economies of scale, more geographical distribution, and a bigger diversity of assets. Third, it is expected to increase HGV’s free cash flow and EBITDA figures almost immediately. Also, the combination of the two companies will immediately add 200k members to HGV’s total membership which it can use to upsell more vacation packages and services in the future.

The HGV basically says that the purchase price reflects only 6 times pro forma LTM EBITDA of Bluegreen Vacations but this figure includes cost synergies. Since the purchase price was $1.5 billion and the two companies are expected to run synergies of $100 million, that leaves us another $150 million to account for if the purchase price of $1.5 billion is in fact only 6 times its pro forma EBITDA which would come down to $250 million. This means that HGV was expecting Bluegreen Vacations to have about $150 million in pro forma EBITDA. Another interesting thing to note is that Hilton Grand Vacations admits that this acquisition will increase its leverage ratio to 3.4x in the short term because of the debt it took on but also predicts that it will be able to bring down its leverage to a more conservative 2.0 to 3.0 within 18 months due to high levels of cash generation.

Acquisition Highlights (Hilton Grand Vacations)

It is not clear where those synergies would come from though. Since both companies had their own portfolio of real estate assets that were managed separately, this is not likely to generate many synergies since you can’t combine the operations of resorts in different cities or states. Synergies will more likely come from the corporate side of things such as sales and administration which may not be very large to begin with. It will be interesting if the combination of these two companies can really squeeze that much synergy out that quickly.

This acquisition is adding about 218k members to HGV’s total membership. More importantly, it is reported that 75% of these members are Generation X or younger (born after 1965 or 1970 depending on which definition you take). It is typically said that most timeshare members tend to be on the older side and timeshare companies are having trouble getting younger people to sign up for memberships, which means Bluegreen had a unique set of members that are difficult to come by and could be valuable.

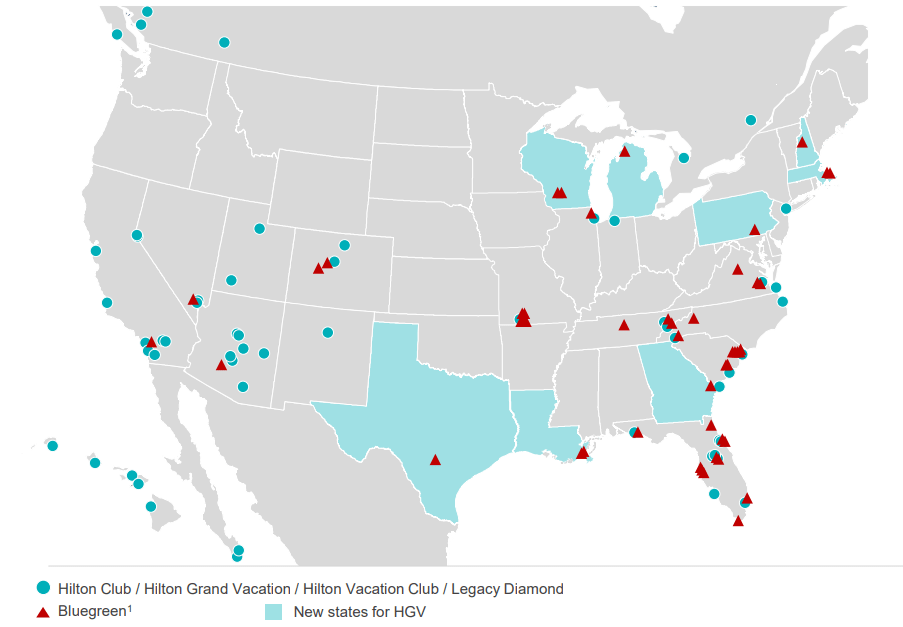

Furthermore, the combination of the two companies is adding 48 resorts to HGV’s portfolio and increasing its footprint by adding 8 new states and 14 new geographies to the company’s total exposure. As you can see below, HGV didn’t have any properties in states like Texas, Wisconsin, Michigan, Louisiana, Pennsylvania, and Georgia but now it will gain exposure to these states as well as increase its existing exposures in places like Florida and South Carolina.

Assets Map (Hilton Grand Vacations)

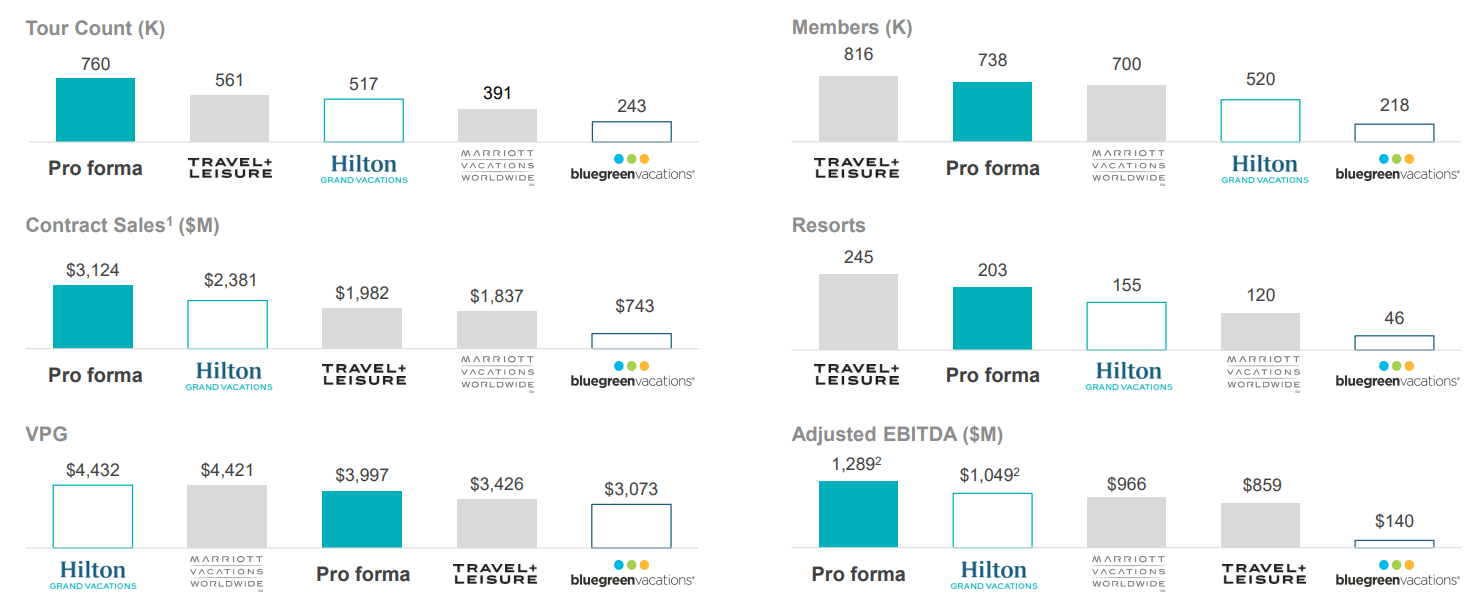

As you can see below, HGV used to be behind competition namely Travel + Leisure (TNL) in several metrics but the combined company should either close the gap or pass TNL in most of those metrics. For example, the combined tour count is now at 780k up significantly from Hilton’s 517k alone and easily passes TNL’s 561k. The number of total members rises from 520k to 738k, closing the gap with TNL’s 816k. The adjusted EBITDA will rise from $1.05 billion to $1.29 billion (including the expected synergies of $100 million), increasing the difference with TNL’s $859 million so it will put HGV in a more advantageous position from a competitive standpoint.

Combined Metrics (Hilton Grand Vacations)

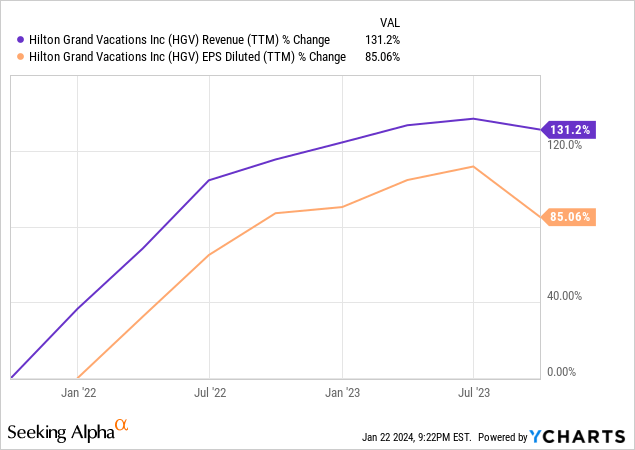

This is not the first time this company made a large acquisition either. Just a few years ago in 2021 it acquired Diamond Resorts and incorporated all of its elements into its own ecosystem which was also a similar deal. Since then, the company’s revenues rose by 131% and its profits (measured by EPS) rose by 85% but this was not only because of the acquisition alone, although the acquisition definitely helped.

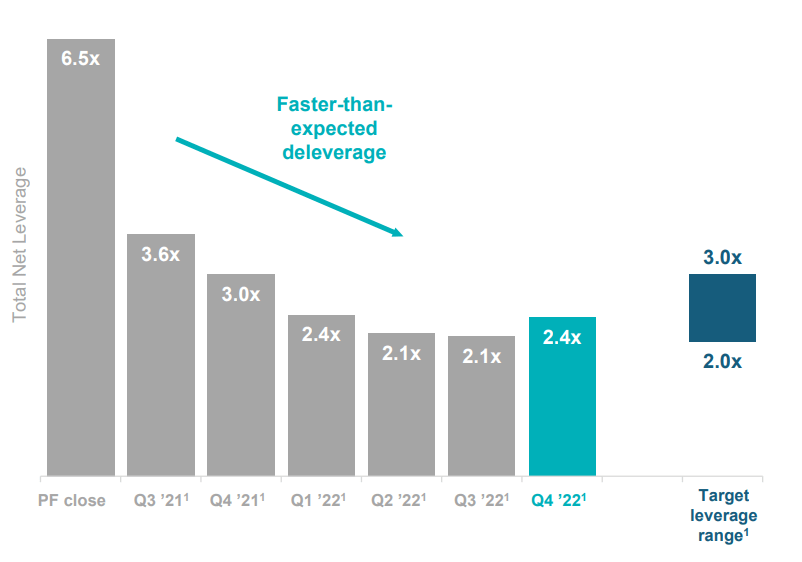

The last time the company made a major acquisition it had to take on a significant amount of additional debt and at one point its leverage ratio was as high as 6.5x. Obviously, there were worries about whether it could reduce its leverage to a more acceptable level and it was able to do it fairly quickly. We may also be able to witness something similar this time if the company starts seeing the benefits of synergies from this acquisition as quickly as it says it will.

Leverage From Last Acquisition (Hilton Grand Vacations)

Vacation industry is an interesting industry. On one side, we know that people are still going on vacations and spending a lot of money based on earnings growth of a variety of companies in this sector. Cruise companies like Royal Caribbean Cruises (RCL) and Carnival Corporation (CCL) are both reporting increasingly good results showing strong demand. Similarly, major airline companies like United Airlines (UAL) also report that there is a lot of demand for travel. We also know from companies like Airbnb (ABNB) whose results show that rising travel demand might be secular in nature.

On the other hand, vacation industry will only outperform under strong economic conditions. This is a highly cyclical industry and it has very wild ups and downs. HGV has some cushion against this high level of cyclicality because it sells memberships so a good portion of its revenues are recurring and predictable but it is not that difficult for people to drop their memberships if needed.

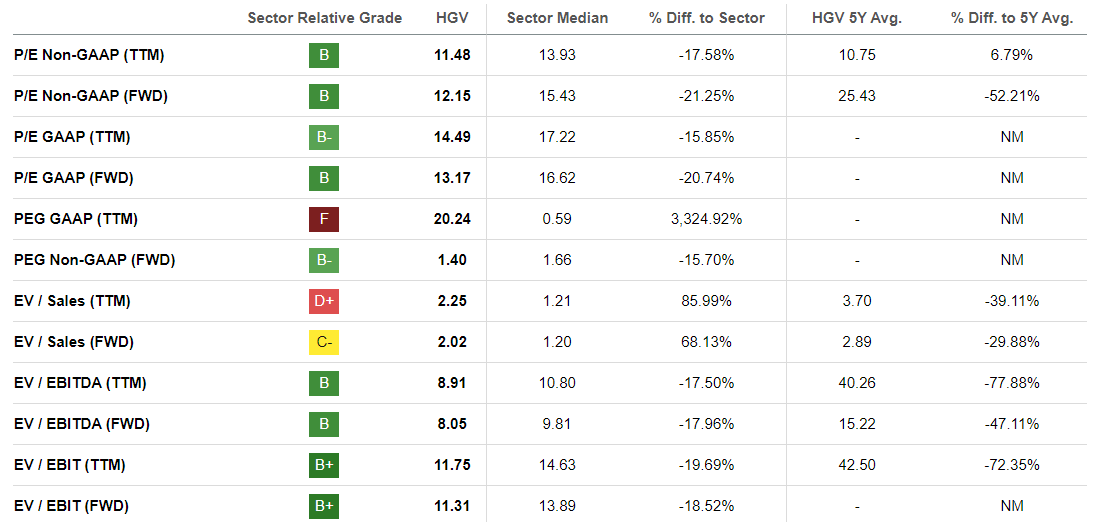

HGV’s valuation looks slightly better than its peers. The company has a trailing P/E of 11.48 and a forward P/E of 12.15 as compared to a sector median of 13.93 and 15.43 respectively, indicating a discount of 17% to 21%. The company’s GAAP-based P/E multiples are slightly higher but they also indicate a 15% to 20% discount against its peers. Furthermore, the company’s EV/EBIT and EV/EBITDA metrics are both indicating a 17%-19% discount against its peers which is very consistent with its P/E metrics. Of course, these numbers are based on HGV alone and don’t include the effects of the merger or any future synergies so the company’s actual future metrics might be even cheaper.

Valuations (Seeking Alpha)

As a matter of fact, the analysts covering the company see it growing its net EPS by 20% in 2024 and another 28% in 2025 most likely due to benefits from this acquisition. Based on these estimates, the company looks even cheaper with a forward P/E of 8 based on 2025 estimates. We will have to wait and see if the company actually hits those numbers though.

Analyst estimates (Seeking Alpha)

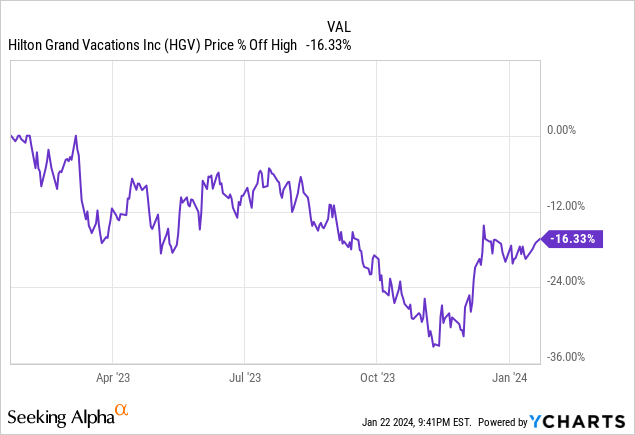

Investors have been selling the stock for a while and at one point it was down as much as -35% from its 52-week high. Much of the drop happened as a reaction to this acquisition as investors were worried about the company taking on more debt but it’s been on its way to recovery since October and now it’s only down -16% from its 52-week high.

This could be a good buy if the company achieves its synergy targets but it also all depends on the shape of the economy. If we get a recession like several people have been predicting, this stock could drop sharply due to its cyclical nature and you might be able to buy it at an even cheaper valuation but if the economy continues the way it’s been performing recently, the company and stock might actually have some significant upside ahead.

Q2 2024 Earnings Call Transcript")