Scott Olson

A list of defensive consumer staple names have been getting cheaper over the last 12 months. Among my favorites is The Hershey Company (NYSE:HSY), which may have the smartest combination of operating business undervaluation, future growth prospects, and high to rising dividend yield. If you believe a U.S. recession and bear market are next for Wall Street in 2024, this defensive pick could be a great idea, especially on minor weakness. Now, I don’t expect spectacular returns from this leading global chocolate and candy maker, but if you are good with +10% in projected annual total returns over the next 3-5 years, Hershey should be near the top of every safety-first research list.

For me, consumer staple and packaged food stocks in general remain too expensive on basic fundamental valuation ratio analysis vs. historical setups when Treasury interest rates are in the 4% to 5% range. Some offer better value and upfront yields, but business growth is non-existent. Really, dividend stories for the majority of consumer staples are not a clear-cut resounding buy proposition, especially if interest rates surprise and rise again this year.

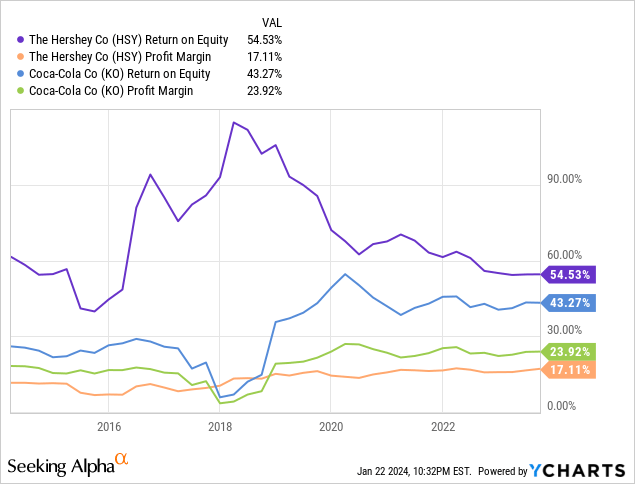

For reference, Hershey runs one of the top profit margin and return-on-equity businesses in the large-cap packaged food industry. Final profit margins on sales of 17% and ROE beyond 54% are exceptional numbers comparable to Coca-Cola (KO), displaying a high margin-of-safety for conservative investors.

YCharts – Hershey vs. Coca-Cola, Return on Equity & Final Profit Margin, 10 Years

In the end, Hershey may be sitting on the best value and growth foundation out of the consumer staple packaged-food group, with a killer dividend yield argument to buy shares. Let me explain why.

Valuation Getting Interesting

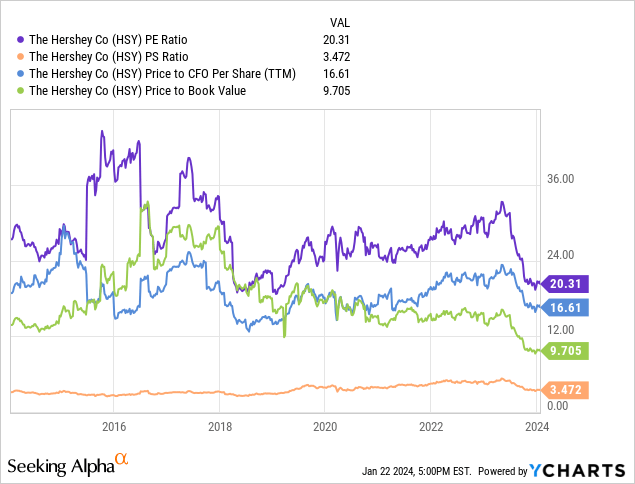

Overall, valuation stats are explaining a better-than-typical entry point for Hershey buyers. On the 10-year graph below of price to trailing earnings (20x), sales (3.5x), cash flow (16.6x), and book value (9.7x), we can see the company is materially less expensive than decade averages, except for the sales ratio around normalized readings.

YCharts – Hershey, Basic Fundamental Valuation Ratios, 10 Years

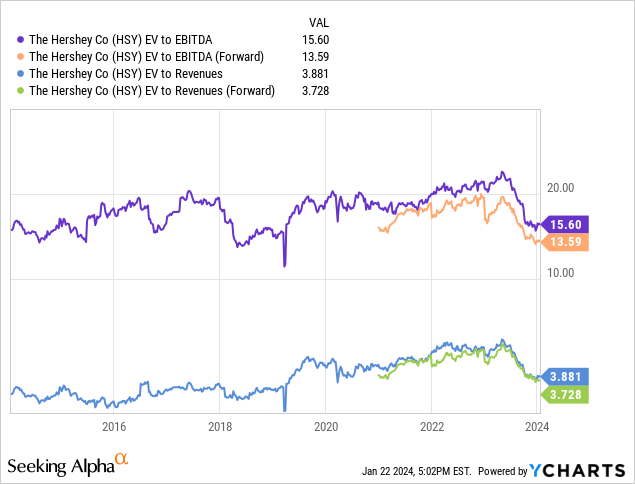

When we include debt totals and cash on hand, the enterprise valuation does appear to be nearing bargain territory. On EV to EBITDA and revenue ratios, Hershey is best situated since early 2019, especially when we look at forward Wall Street analyst forecasts.

YCharts – Hershey, Enterprise Valuations, 10 Years

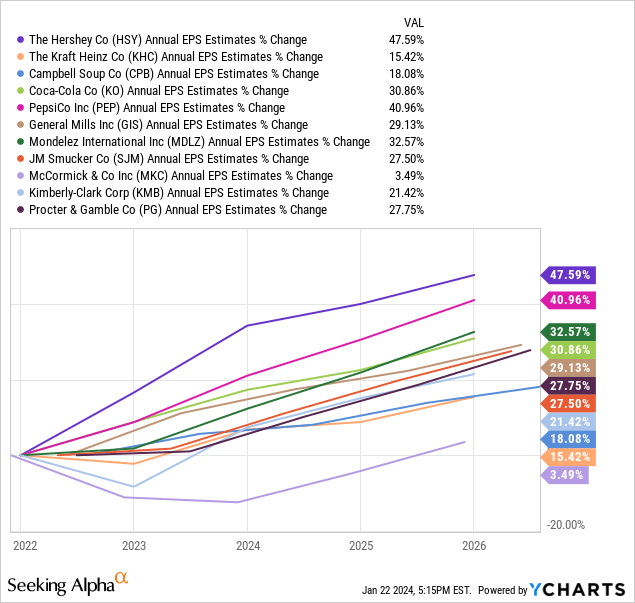

Plus, the attractive valuation is sitting on better-than-average industry growth rates. When we look at a group of the largest food and consumer staple names, company income growth measured from 2022 into 2026 has been (should be) incredibly positive vs. peers.

YCharts – Packaged Food & Consumer Staples, Estimated EPS Growth, 2022-26, Made January 21st, 2024

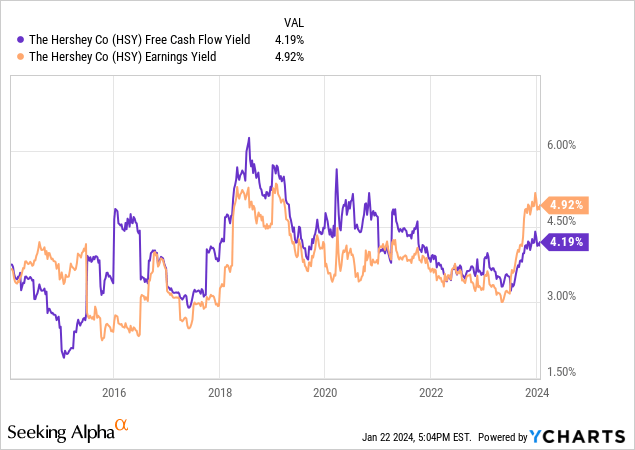

For me, another slight dip in the stock would translate into an even stronger valuation setup, especially if free cash flow and earnings yields can get above 5%. Being able to purchase Hershey with a business investment yield of 5% and cash payout closer to 3% annually would create the best valuation setup since early 2010, right after the Great Recession ended (not pictured).

YCharts – Hershey, Free Cash Flow & Earnings Yields, 10 Years

Dividend Yield Buy Argument

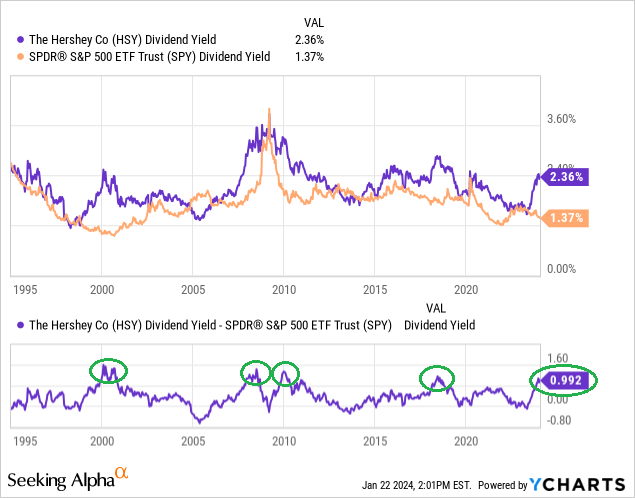

At first glance, Hershey’s 2.36% trailing dividend yield (2.5% forward rate) is not much to write home about. But, this number represents a nice premium beyond what the overall blue-chip SPDR S&P 500 ETF (SPY) is sending to owners with 1.37% in yield.

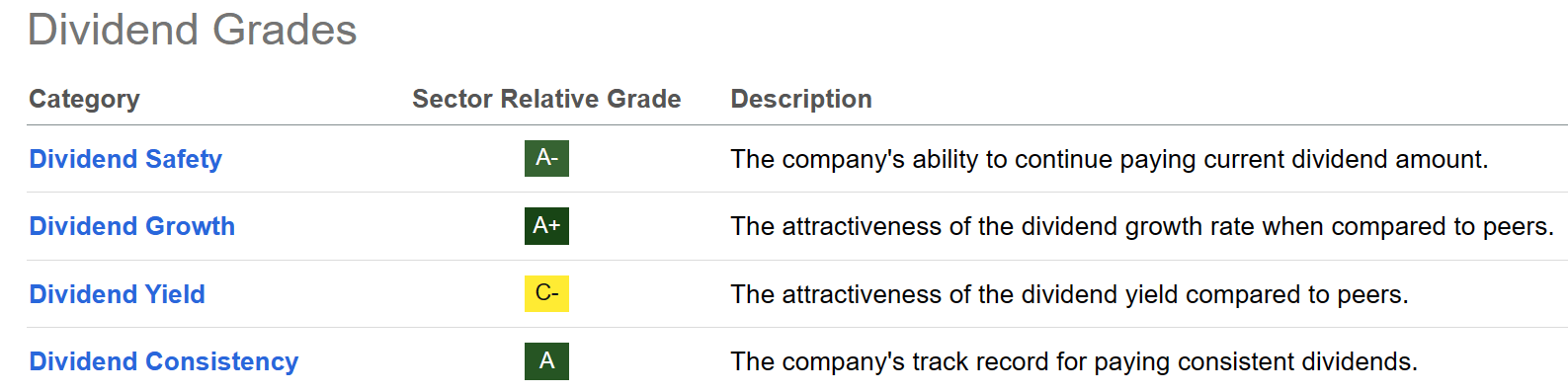

More good news is Hershey has an A+ track record of paying a regular dividend and growing the payout with climbing earnings over time (sending checks since 1990).

Seeking Alpha Table – Hershey, Quant Dividend Grades, January 21st, 2024

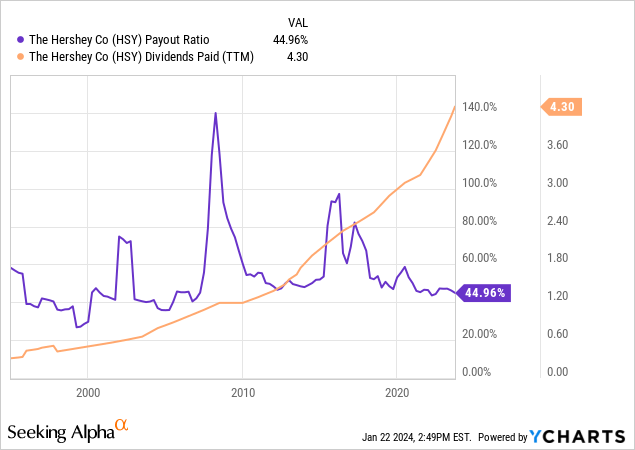

You can review the excellent dividend coverage on earnings and growth rate stats below since 1995. Over the last 29 years, the cash payout has increased at an annualized compounded rate of 9%. Using the Rule of 72 for compounding, you can project a doubling over the next 8 years, if this trend continues. A dividend double is absolutely possible with today’s coverage ratio of 45% out of earnings on the low end of historical ratios. For example, the immediate future 2.5% yield could easily be 5% annually on your investment today by 2032. A 3% rate (on another share price drawdown in Q1 2024) could morph into 6%, for forward thinkers.

YCharts – Hershey, Dividend Payout/Earnings Ratio and Trailing 12-Month Paid Amount, Since 1995

Hershey Performance: High Relative Dividend Yield

Believe it or not, the “relative” +1% in extra Hershey cash distribution yield vs. the prevailing S&P 500 average rate has proven quite rare historically. Below I have graphed the spread differences back to 1995, circling in green positive adjusted yields beyond +1%.

YCharts, Hershey vs. SPDR S&P 500 ETF, Dividend Yields & Spread, Since 1995, Author Reference Points

The truth is these positive relative dividend-yield periods have proven great times to buy Hershey. Let’s review what happened during the last 4 instances over three decades.

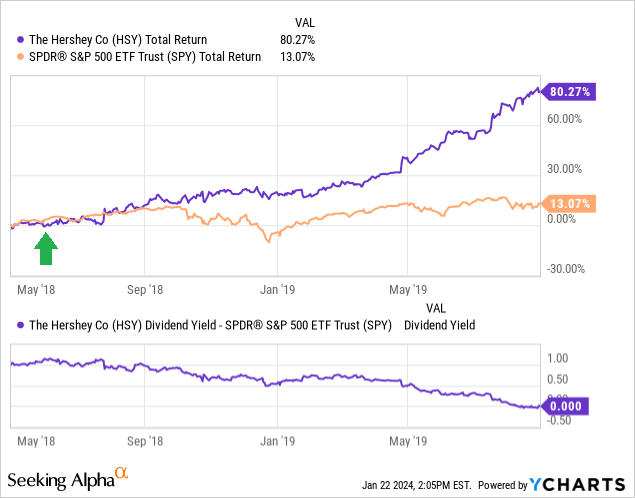

2018

The +1.2% spread in June 2018 coincided with a share price bottom. From that point, Hershey outlined a +80% total return into August 2019, about 14 months later. In comparison, the S&P 500 index gained +13% in value over the same span for investors.

YCharts, Hershey vs. SPDR S&P 500 ETF, Total Returns, Dividend Yield Spread, May 2018 to August 2019

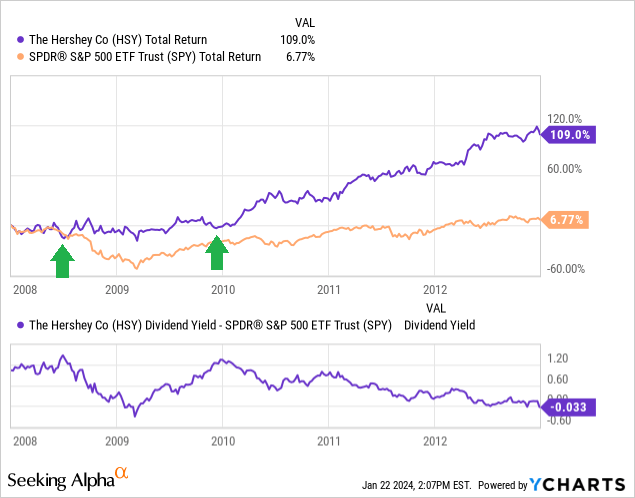

2008 & 2009

Again in July 2008 (+1.4% spread) and December 2009 (+1.3% spread), Hershey bottomed quickly and reversed in price. Shares rose and outperformed the S&P 500 after each occurrence. In total, from early 2008 to the end of 2012, Hershey’s total return was +109% (+125% from the first high dividend spread peak in July) vs. a minor S&P 500 gain of +7%!

YCharts, Hershey vs. SPDR S&P 500 ETF, Total Returns, Dividend Yield Spread, 2008 to 2012

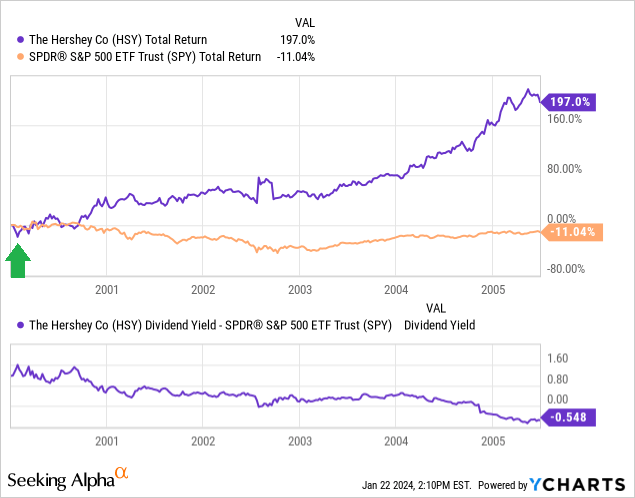

2000

My last reference point took place in January 2000, with a +1.6% positive yield spread for Hershey. Shares immediately began to increase in value. A +197% gain over the next five and a half years ran circles around the -11% LOSS generated by owning the S&P 500 index.

YCharts, Hershey vs. SPDR S&P 500 ETF, Total Returns, Dividend Yield Spread, 2000 to June 2015

Final Thoughts

Hershey may have entered the sweet spot of the dividend spread cycle, indicating sizable odds of a bottom in share pricing soon (if it hasn’t been reached already). Going into a possible 2024 recession, Hershey’s defensive outperformance should be worth following closely in the coming weeks and months.

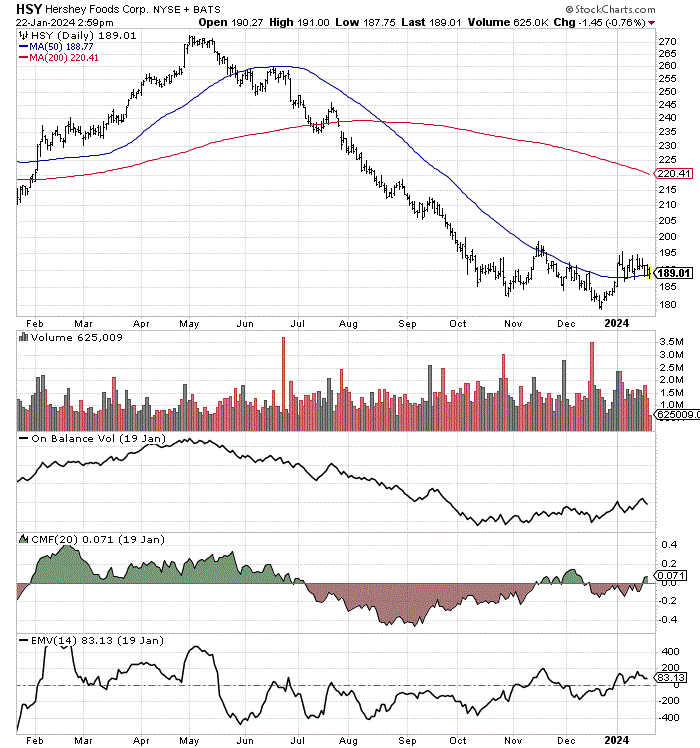

With a December low of $179 in December, trading chart momentum has turned more positive. On the 12-month chart of daily price and volume changes below, you can review the improved On Balance Volume, 20-day Chaikin Money Flow, and 14-day Ease of Movement calculations since October.

StockCharts.com – Hershey, 12 Months of Daily Price & Volume Changes

The whole investment equation is looking more bullish by the day, including a decent underlying fundamental valuation, bullish dividend yield story, and bottoming technical pattern.

I have a total return estimate of +10% annualized over the coming 3-5 years, under the assumptions a mild recession hits in 2024, with inflation rates staying around 3% and risk-free Treasury yields settling around 4%. I am using a normalized 25x P/E multiple (10-year average) and 2% nominal dividend yield in the future, with 10% growth rates for both EPS and the cash distribution as my baseline formula.

Nothing spectacular, but a +10% yearly return may nicely outperform the U.S. equity and bond markets in general. If you are searching for a blue-chip consumer staple, with a list of reasons lining up in its favor, Hershey may be a wonderful risk-adjusted choice to contemplate for your portfolio.

In my view, the biggest downside risk to shareholders is interest rates will continue to rise. Such would undercut Hershey’s valuation ratios and keep pressure on the stock quote, even if sales and earnings hold up. Something of a chocolate and candy shortage in the U.S. was a thing in 2023 on cocoa commodity production issues. Better balance in the chocolate marketplace could hurt EPS growth rates in 2024-25, although nothing is guaranteed. The company does have an enviable history of stable and steady income expansion, with a flexible business model able to pass along cost increases to consumers.

I rate Hershey a Buy under $195, with Strong Buy territory under $175 for long-term investors. At this stage, I firmly believe another price dip lower would turn into a terrific buying opportunity (if it happens).

Thanks for reading. Please consider this article a first step in your due diligence process. Consulting with a registered and experienced investment advisor is recommended before making any trade.

Q2 2024 Earnings Call Transcript")