Here on Seeking Alpha, we’ve made no secret of our disdain for option-enabled, ‘high income’ funds that utilize covered calls and other derivative strategies to generate a high level of “yield” for investors.

In the past, we’ve written a number of articles on the topic, which you can review here:

Of the funds that we’ve evaluated, we’ve rated one as a “Hold” (JEPI), and we’ve rated two as a “Sell” or “Strong Sell” (TSLY and QYLD).

None have a “Buy” rating – and there’s a reason for that; all of these funds sell covered calls on their underlying holdings and distribute that cash as income every month.

If you’re invested in these ETFs, you may be shaking your head right now in agreement, wondering what the problem is.

Here’s the key – these funds distribute the cash they earn whether or not their option trades realize a profit. That’s right – cash from covered calls isn’t just free money, when the fund sells options, there can be associated, realized losses if the options expire in the money. That way, over time, if a fund consistently realizes losing option trades, while they pay out the cash proceeds that could buttress against negative P/L, fund AUM can slowly bleed out over time.

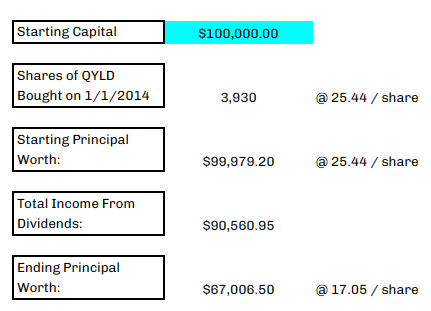

[Let’s say an] income-oriented investor invests $100,000 into QYLD in 2014:

Author

On Jan 2nd, 2014, the investor purchases 3,930 shares of QYLD, which are trading at $25.44. Then, he sits and does nothing over the ensuing decade.

In that time, the investor earns $90k in dividend income, but his dividend generating principal, after that whole time, would be worth only about $67k.

QYLD’s yield looks high at 12%, but given the depreciation of the principal, the investor’s original 100k spent now has a yield on cost of only 8%, a 33% drop in earnings power over 10 years:

Seeking Alpha

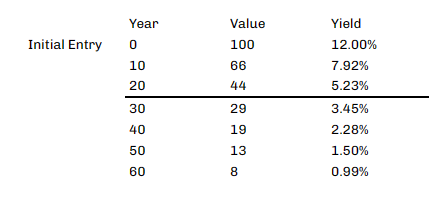

Given that QYLD’s yield and principal seem to have a steady rate of decay based on a natural occurrence of unprofitable trades, one might be able to model out this behavior:

Author

For this reason, we tend to avoid high-income ETFs in our own investing.

For its part, JEPI appears to be better than the rest, investing in a lower-volatility basket of stocks and selling calls further out of the money, which reduces the risk of long-term earnings decay considerably. As a result, it hasn’t seen any decay in earnings power over time, which is fantastic. It’s also why we consider it a ‘Hold’, as opposed to a ‘Sell’.

However, spurred on by the runaway success of JEPI, in 2022, JPMorgan (JPM) issued a new ETF with a similar composition to JEPI called NASDAQ:JEPQ.

We don’t think the fund will do as well over the long haul, and today, we’ll look at two potential problems with the fund to explain why.

JEPQ’s Methodology

To understand JEPQ, it’s a good idea to look at JEPI, other JPMorgan income ETF, as management basically copy-pasted the same strategy onto the Nasdaq 100 (QQQ).

For reference, JEPI basically functions by building a portfolio of high quality, low risk, low beta stocks that are constituents of the S&P 500 (SPY).

Then, the fund sells calls on them via equity-linked-notes, or ‘ELN’s.

This approach has worked well, as we’ve laid out.

It follows, then, that JEPQ has been built in exactly the same way:

The investment seeks current income while maintaining prospects for capital appreciation.

The fund (JEPQ) seeks to achieve this objective by (1) creating an actively managed portfolio of equity securities comprised significantly of those included in the fund’s primary benchmark, the Nasdaq-100 Index® (the Benchmark), and (2) through equity-linked notes (ELNs), selling call options with exposure to the Benchmark. It is non-diversified.

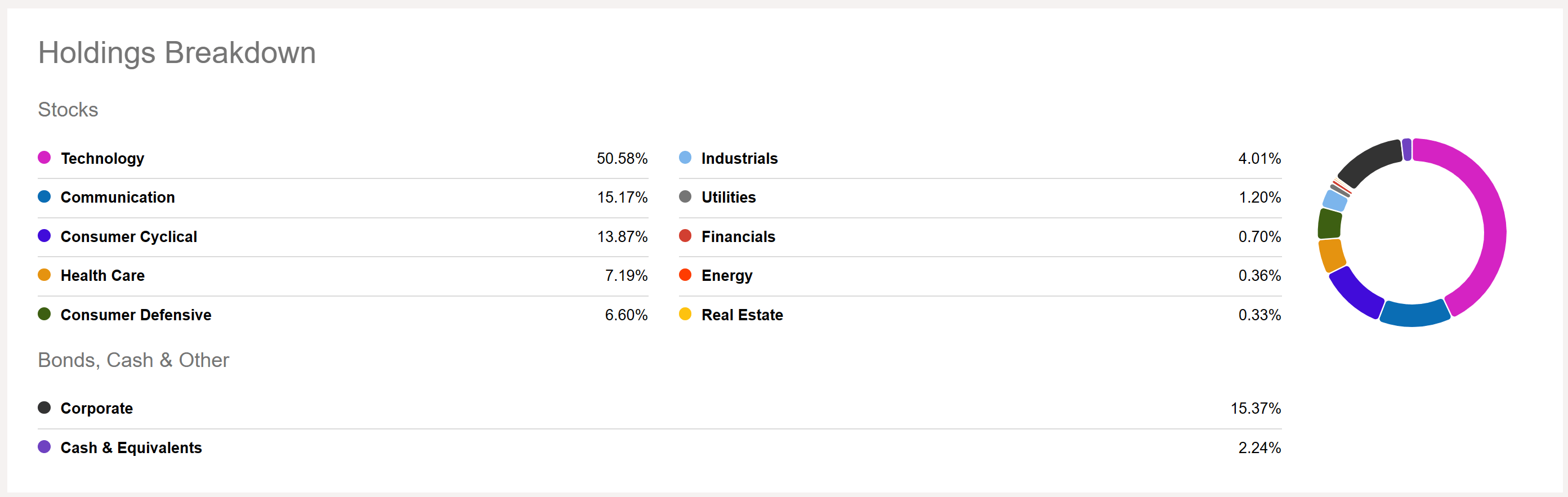

Since inception, it’s been running this strategy – by holding a group of stocks that closely resembles the Nasdaq 100, weighted in such a way as to attempt to reduce volatility and maximize Sharpe. It then generates ‘income’ via holdings in ELNs that sell calls:

Seeking Alpha

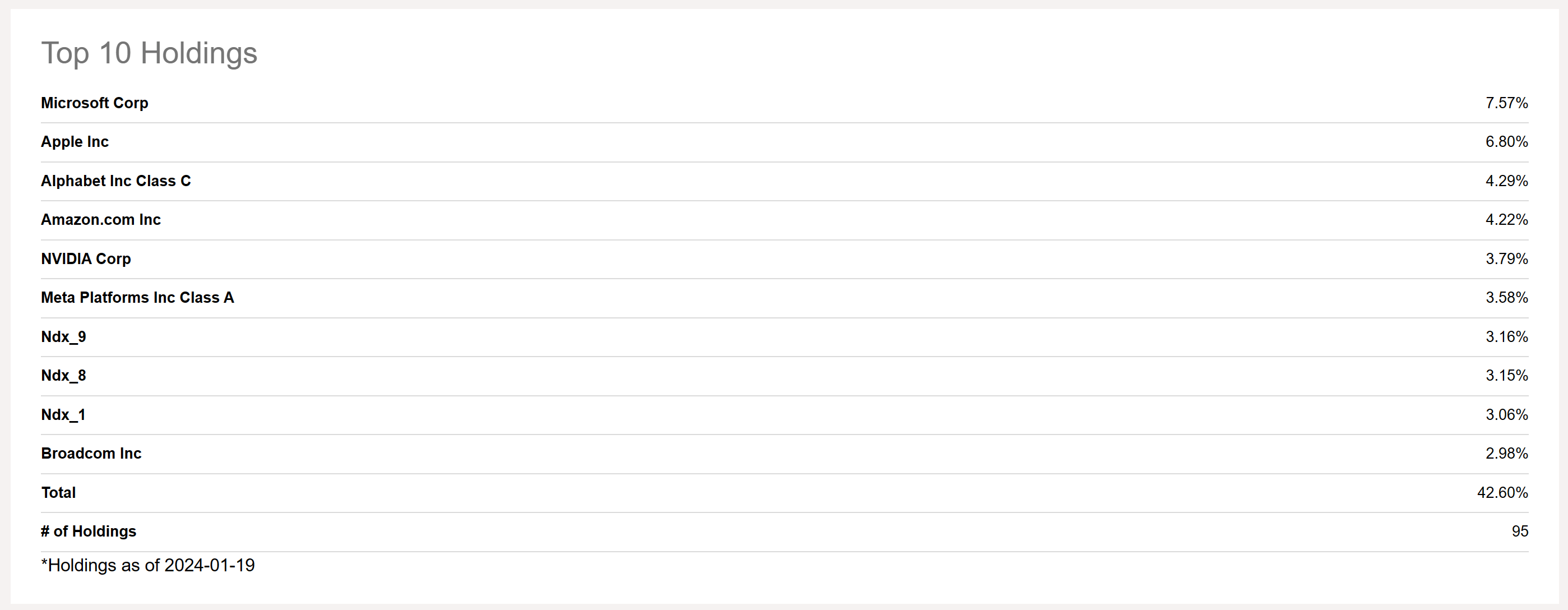

You can see the fund’s high level of exposure to Technology (XLK), Communications (XLC), and Consumer Cyclical (XLY) stocks, like Apple (AAPL), Microsoft (MSFT), Alphabet (GOOG), Meta (META) and Amazon (AMZN):

Seeking Alpha

You can also see the ELN positions, that comprise a number of the top ten holdings above, and more than 15% of the fund’s assets.

This strategy has resulted in a TTM dividend yield of 9.72%. For managing the fund, management currently charges a 0.35% annual fee on assets.

Problem Number 1: Big Picture Volatility

Here’s the issue.

As we’ve oft explained, the more volatile an instrument is, the more likely it’s going to frequently ‘violate’ its short call position.

In other words, the more something moves, in terms of realized ranges, the more it will finish a given month with a short call position in-the-money.

This behavior is best shown when taken to an extreme; in the case of TSLY, yield-on-cost has been decimated over time as Tesla has whipped around and the option premiums haven’t been able to adequately account for this risk:

Seeking Alpha

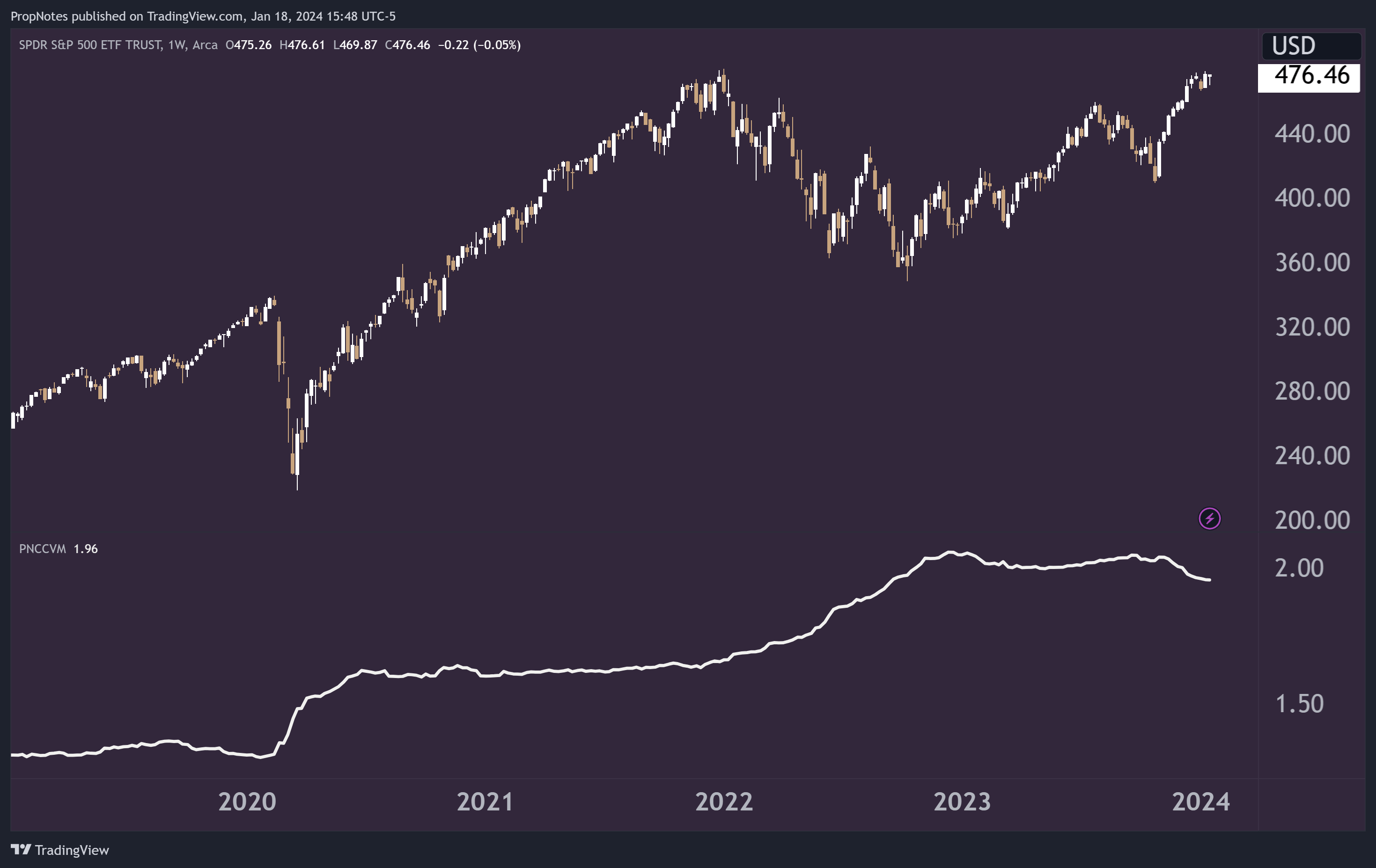

JEPI has done well in this regard, mostly avoiding losses caused by an option assignment.

This is due to SPY’s low overall level of volatility, which has averaged below 2% per day over the last 5 years:

TradingView

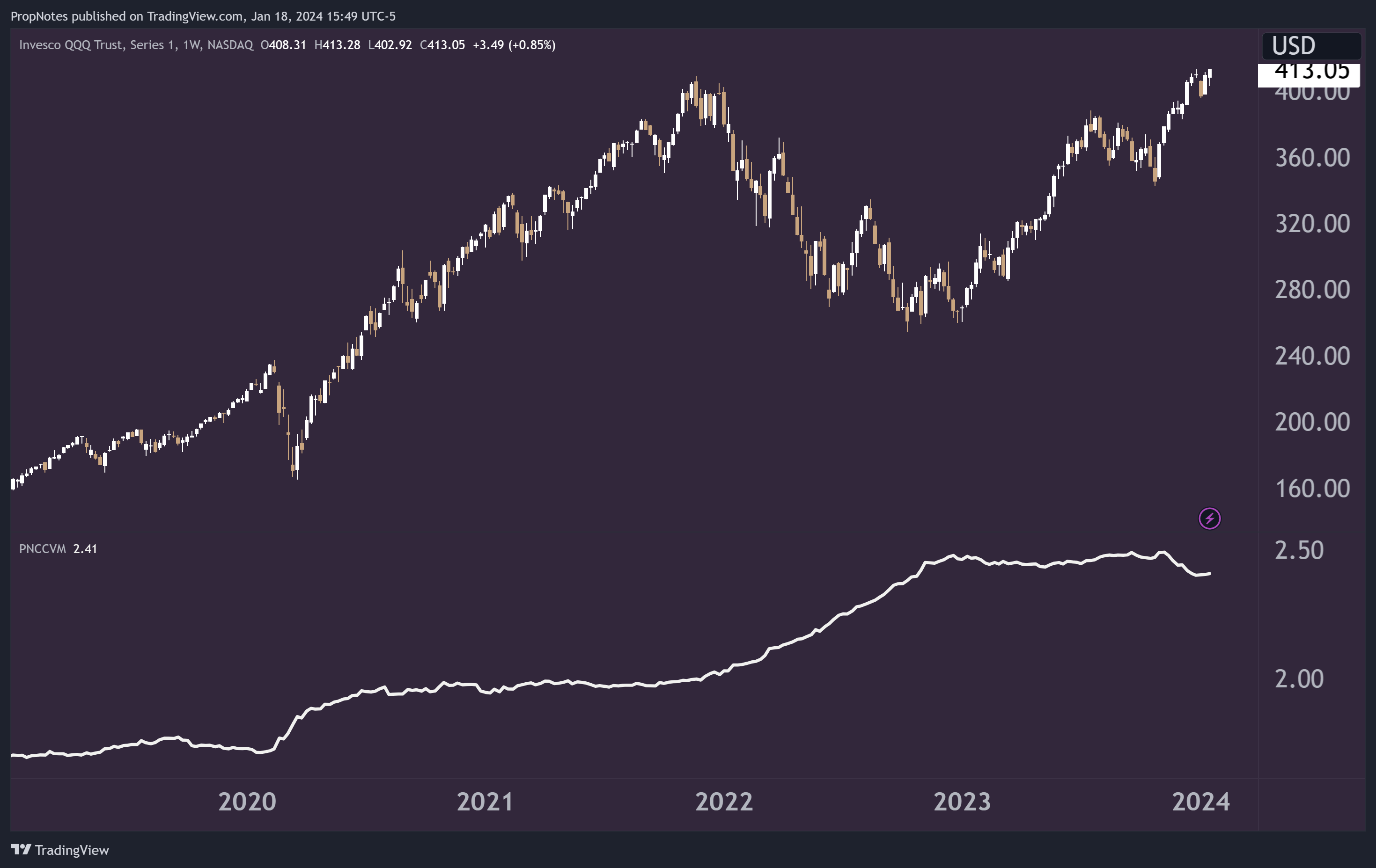

However, QQQ’s level of volatility is much higher, at 2.41% per day since the start of 2019:

TradingView

This doesn’t seem like a big difference, and nominally, it isn’t. However, when multiplied over a number of consecutive days, QQQ has the ability to deviate in a big way.

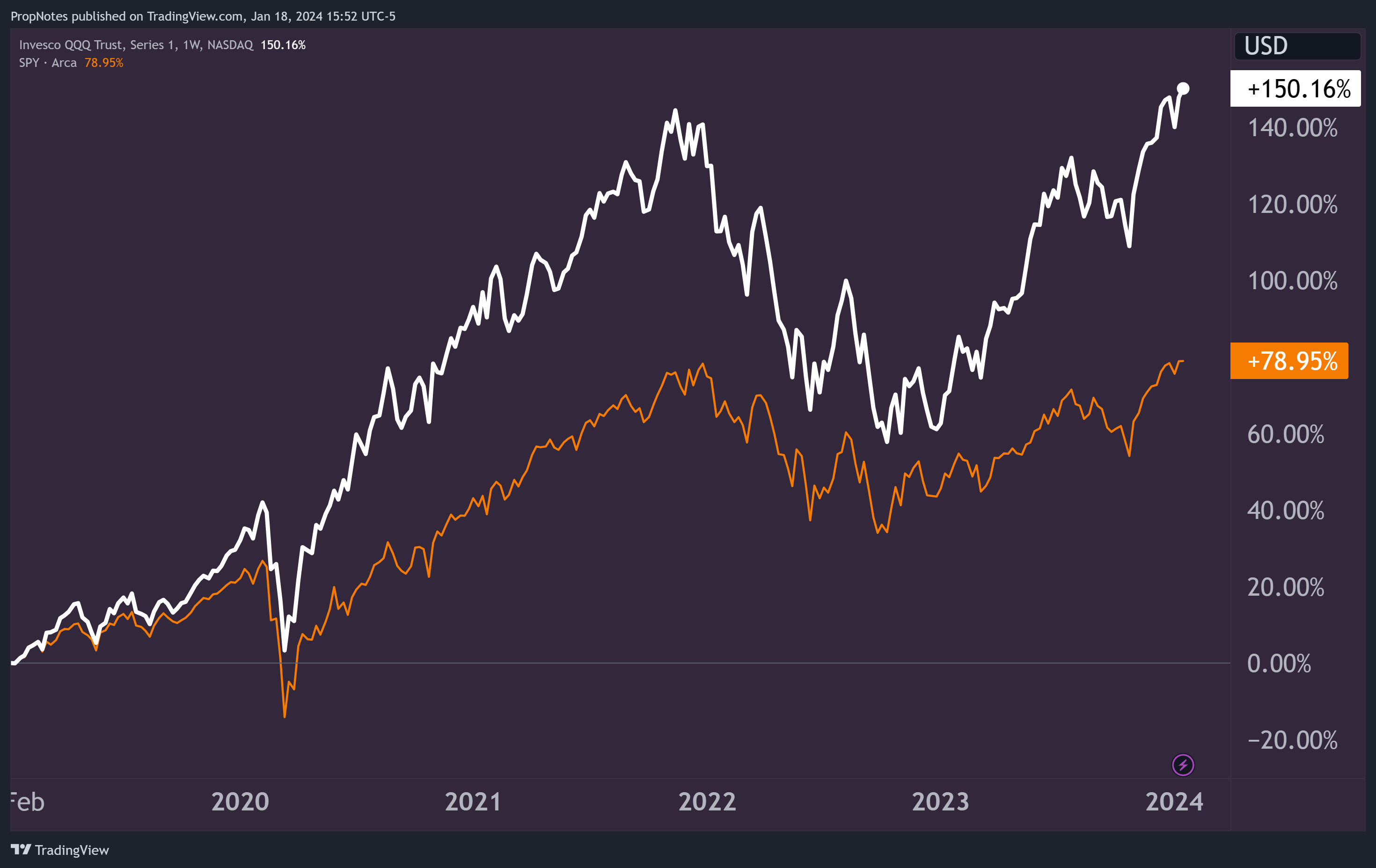

This is also how QQQ has been able to outperform SPY so convincingly over the last 5 years – a larger daily range to move within.

TradingView

In our view, JEPI has found the sweet spot of volatility, low risk, and income.

JEPQ, by contrast, has the potential to be an improved version of QYLD, which features a decaying NAV, as mentioned. It’s not clear that this will be the case, as JEPQ sells OTM options, which is a better overall practice than selling ATM.

However, the increased volatility poses a strong threat to JEPQs long term outperformance prospects.

Some may argue that this shouldn’t happen based on the fact that options are live instruments and are priced for this. However, we haven’t seen any evidence of MM’s ability to account TSLA‘s volatility situation that has caused drastic underperformance in TSLY.

Overall, in our view, it’s likely that JEPQ’s more volatile underlying index will cause trouble for the same strategy that has worked well on JEPI.

Problem Number 2: IV Depression

Even if it weren’t the case that the strategy had the potential to underperform for the long-haul, short-term pricing is also incredibly adverse for people looking to enter JEPQ at the present moment.

Implied volatility in the tech sector is at multi-year lows, as we recently wrote about in an article focused on Netflix (NFLX).

It’s important to realize that writing options is equivalent to selling insurance. Insurance is generally a good business, but there are times when there is too much capacity, and premiums go below the level appropriate for the risk involved. In the property insurance market, for example, this usually happens when there haven’t been many major disasters for a few years. I believe that’s where the stock options market is now.

Option volatilities are too damn low! Here’s a table of QQQ implied vols over the past year:

Implied Volatility

14.02%

Historical Volatility

12.02%

IV Percentile

0%

IV Rank

0.94%

IV High

28.79% on 01/03/23

IV Low

13.96% on 12/14/23

So we are basically at yearly lows for QQQ vol. In fact, the only time in history I could find where implied vol was lower was in the second quarter 2017. In most mean reverting markets, like implied vol, selling near all-time lows is not a good idea.

We couldn’t agree more. In mean reverting markets, selling vol is not a good idea. Thus, even if JEPQ management can do a good job of handling the higher intrinsic historical volatility of the Nasdaq 100 index, the timing of a buy into this fund also appears to be historically poor.

This could have an impact going forward, as meek premiums harvested may not be able to buttress against a downside scenario and may not bring in enough cash to justify their existence in an upside scenario.

Summary

All in all, as long as the market goes mostly sideways, you’re in a good position with JEPQ.

But, with heightened vol a trademark of QQQ’s risk/reward profile, and a historically poor entry point for this vol pricing in today’s current market, we rate JEPQ a ‘Sell’ – at least until management can prove they’re able to navigate the opportunity with a high level of accuracy.

Q2 2024 Earnings Call Transcript")