Investment giant BlackRock Inc.

BLK,

is making what it calls one of its strongest strategic calls of the moment: Inflation is likely to stay closer to 3% as the world increasingly splits itself into competing blocs.

Attacks by Yemen’s Houthi militants on Red Sea vessels, followed by a U.S.-led response, are prompting a rerouting of tankers and cargo ships which is driving up shipping costs. Meanwhile, Taiwan’s Jan. 13 election of a new president whose party supports a separate identity for the island is doing little to soothe U.S.-China relations.

Read: Oil traders aren’t panicking over Middle East shipping attacks. Here’s why. and It’s less than a year until the inauguration. Here are the stock-market lessons from 134 elections in 17 countries

Geopolitical fragmentation is accelerating, in stark contrast to the era of globalization that prevailed after the Cold War, according to Wei Li, global chief investment strategist, and others at BlackRock Investment Institute. The world has jumped from one crisis to another in more recent years, starting with U.S. trade wars with China under former President Donald Trump and the COVID-19 pandemic.

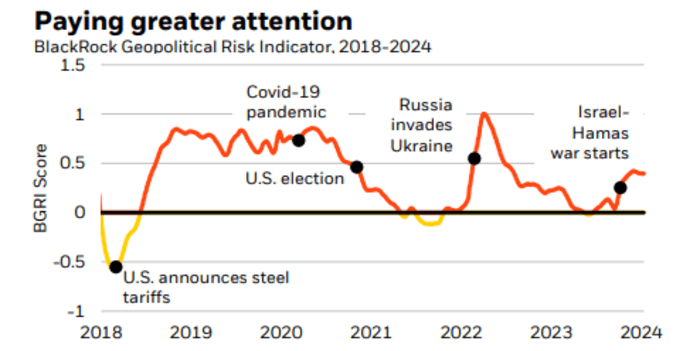

A geopolitical risk indicator from New York-based BlackRock, which managed $10 trillion at the end of the fourth quarter and is the world’s largest asset manager, is rising toward levels last seen in the run-up to Russia’s invasion of Ukraine in February 2022.

BlackRock Geopolitical Risk Indicator, 2018-2024

Source: BlackRock Investment Institute, with data from LSEG and Dow Jones.

“Geopolitical fragmentation, one of five mega forces or structural shifts we track, is playing out in recent events in Asia and the Middle East,” the team at BlackRock Investment Institute wrote in a note on Monday. “Fragmentation is a key reason we see persistent inflation pressures —keeping policy rates above pre-Covid levels.”

“Bottom line: We expect deeper fragmentation, heightened competition and less cooperation between major nations in 2024,” the team said. In addition, “we see the rewiring of globalization benefiting countries like Mexico and Vietnam,” which are acting as intermediate trading partners between different geopolitical blocs.

Investors and traders had entered 2024 with confidence that U.S. inflation would be heading toward 2%, and as many as seven quarter-point rate cuts from the Federal Reserve might be in store. Much of the reason for those rate-cut expectations had to do with falling oil prices last year.

Though oil prices settled at their highest level in about a month on Monday, they have been mostly rangebound. In particular, crude has failed to include a geopolitical risk premium since the start of the Israel-Hamas war in October, with U.S. benchmark WTI

CL00,

CL.1,

trading around $19 a barrel below its 2023 peak set in late September. The lack of a more meaningful jump in oil has masked the rise in shipping prices, which is resulting from the Red Sea conflict.

The BlackRock team said it sees “inflation staying closer to 3% in the new regime,” joining a growing list of financial-market participants who have been warning about the risks of persistent price gains.

That list includes James Solloway, chief market strategist and senior portfolio manager at Pennsylvania-based SEI, and Brent Schutte, chief investment officer of the Northwestern Mutual Wealth Management Co. Their concerns come at a time when one of the bond market’s most widely followed gauges of long-term inflation expectations has been nudging higher.

See also: No rate cuts in 2024? Why investors should think about the ‘unthinkable.’ and Traders give up on a March rate cut by Fed as bond-market inflation expectations move higher

An inflation rate of 2% is the level that the Fed defines as being consistent with its mandate of full employment and price stability, and a failure to achieve that on a sustainable basis would draw into question the central bank’s institutional credibility. Inflation, as measured by the annual headline rate of the consumer-price index, has remained stuck at or above 3% for seven straight months through December — suggesting that traders are off base with their current expectations for five to six quarter-point rate cuts in 2024.

On Monday, traders and investors were mostly focused on the ramping up of the fourth-quarter earnings season. All three major stock indexes

DJIA

COMP

finished higher in New York trading. Meanwhile, 2-

BX:TMUBMUSD02Y

and 10-year Treasury yields

BX:TMUBMUSD10Y

fell from their highest levels of the year, reached on Friday.

Q2 2024 Earnings Call Transcript")