Unlock the Editor’s Digest for free

Roula Khalaf, Editor of the FT, selects her favourite stories in this weekly newsletter.

The decline of London’s equity market — from one of the world’s leading aspirational listing venues to somewhere US investment managers rest on their way to Paris or Delhi — has been thoroughly discussed.

That’s natural. A couple of decades ago, the UK accounted for roughly 8 per cent of the MSCI All-Country World Index; today it’s about 3.5 per cent. Throw in a few high-profile jiltings and the result is anguish.

However, the self-flagellation is a little overdone. Stock markets, like currencies, seem to occupy a special place in a country’s national psyche, where every blow is painfully personal even if it is just part of a much broader beating.

That is particularly true of London, where the health of the equity market is often wrongly conflated with its grander, more meaningful status as a global financial centre. But “de-equitisation” is a trend everywhere.

There are fewer and fewer public companies. Going public has become more onerous and staying private more feasible. As Craig Coben has written, the reality everywhere outside the US capital markets is struggling. (and even there, the number of listed companies has shrunk below that of Communist China).

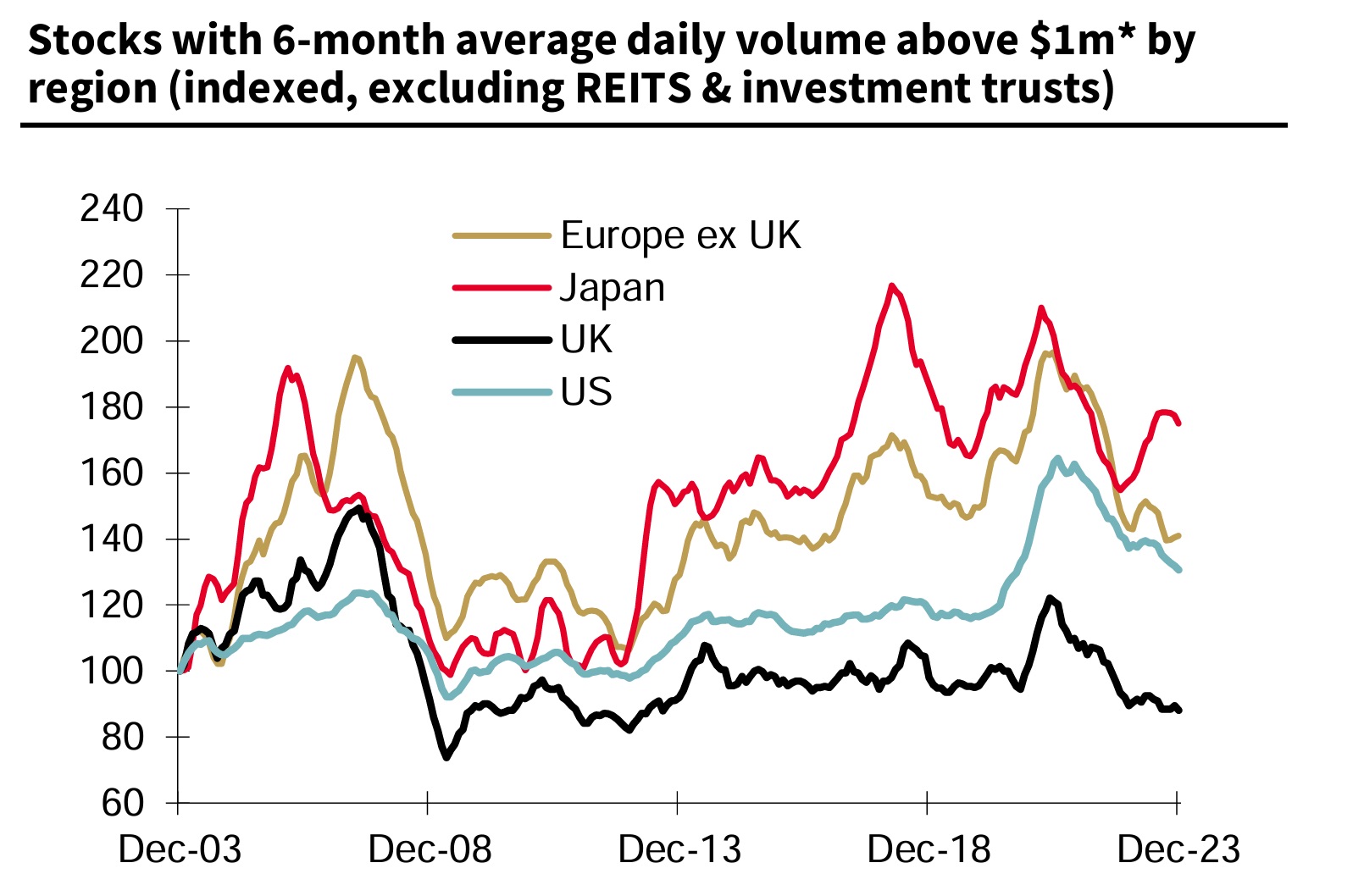

Nonetheless, this chart in the latest note from SocGen’s Andrew Lapthorne caught FT Alphaville’s eye (zoomable version):

The UK is the only major developed market where the number of reasonably liquid stocks has actually shrunk over the past two decades. Today, there are just 319 UK stocks where the six-month average daily trading volume is $1mn or more, according to Lapthorne.

In the rest of Europe there are 869, in Japan 1,411 and in the US there are over 3,000 somewhat liquid stocks. You can see the decline in trading volumes since the 2020-21 retail frenzy everywhere, but the UK is the only place to have seen an absolute decline in the number of $1mn ADV stocks since 2003.

This matters a lot more than the nominal number of listed companies. If you don’t have a liquid secondary market, it deters people from buying in the first place. For bigger fund managers the equity market becomes a Hotel California where you can’t check out (at least not without burning the joint to the ground on the way out).

We’re not sure why UK trading volumes have atrophied so much more than elsewhere. Even with stagnant listings you’d expect average daily volumes to rise over time simply because of inflation – FTSE 100’s market cap has roughly doubled to £2tn over the past two decades. “The trends are not encouraging,” Lapthorne writes. Quite.

Q2 2024 Earnings Call Transcript")

{kind=link}