Daniel Bosma/Moment via Getty Images

Brookfield Renewable Partners (NYSE:BEP) has done well since we last recommended it in October. The company’s total return since has almost doubled the S&P 500, perhaps giving the illusion that the opportunity to invest has passed. Despite that recent strength, the company is well-positioned in a growing market, making it a valuable investment.

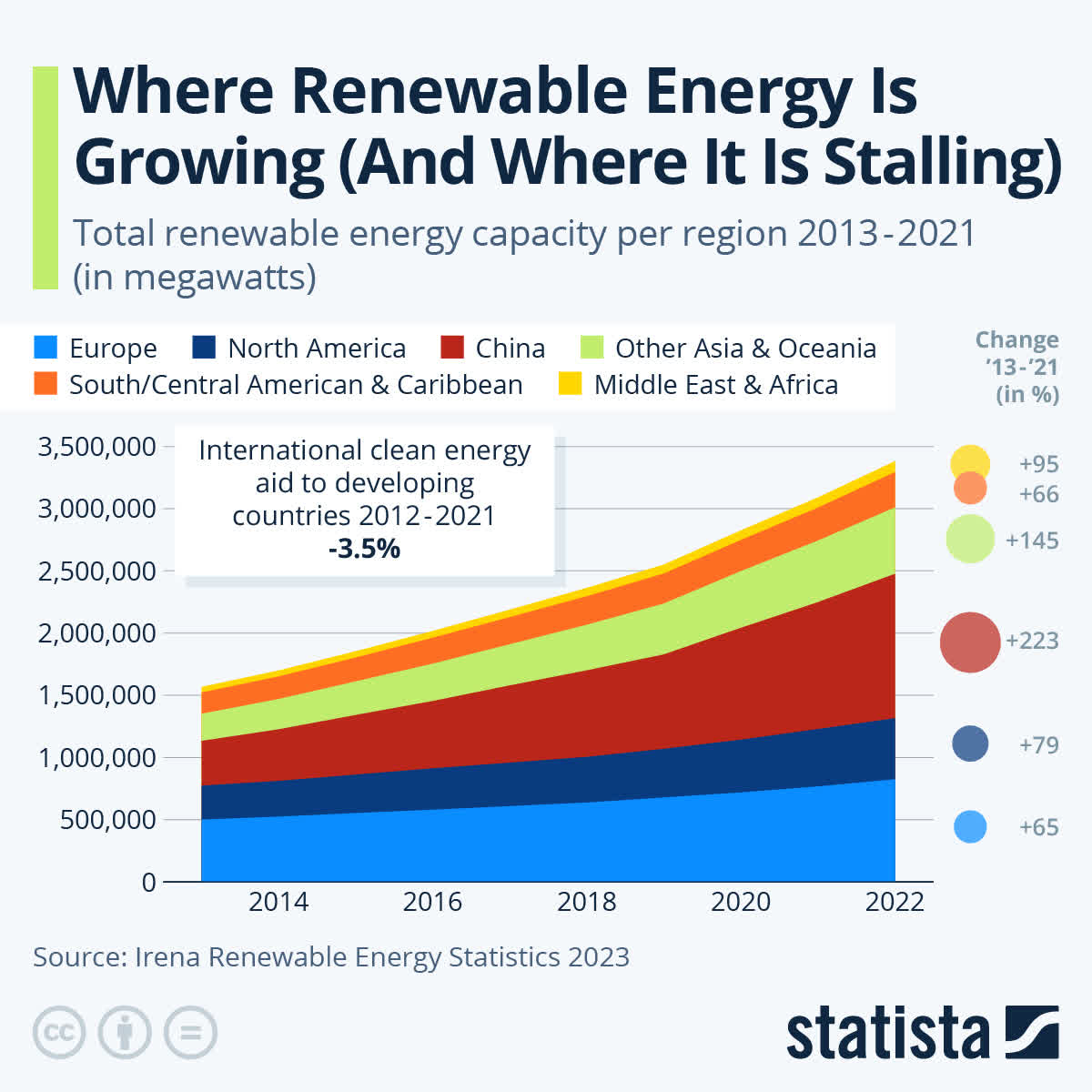

Renewable Energy Growth

Not just for environmental reasons, renewable energy has hit a point where it’s cheaper than coal and natural gas in many situations.

Statista

The above chart shows how fast renewable energy is growing especially in countries that have traditionally been major coal and natural gas consumers such as China. Total capacity across the countries has more than doubled in just a decade. The world’s installed electric capacity is 8.5 terawatts, which means that renewables are now ~40% of global capacity.

Many in the climate change sector are saying that capacity needs to triple from today to 2030 to meet renewable targets. Whether that happens remains to be seen, but regardless there’s no denying that the market is seeing substantial growth.

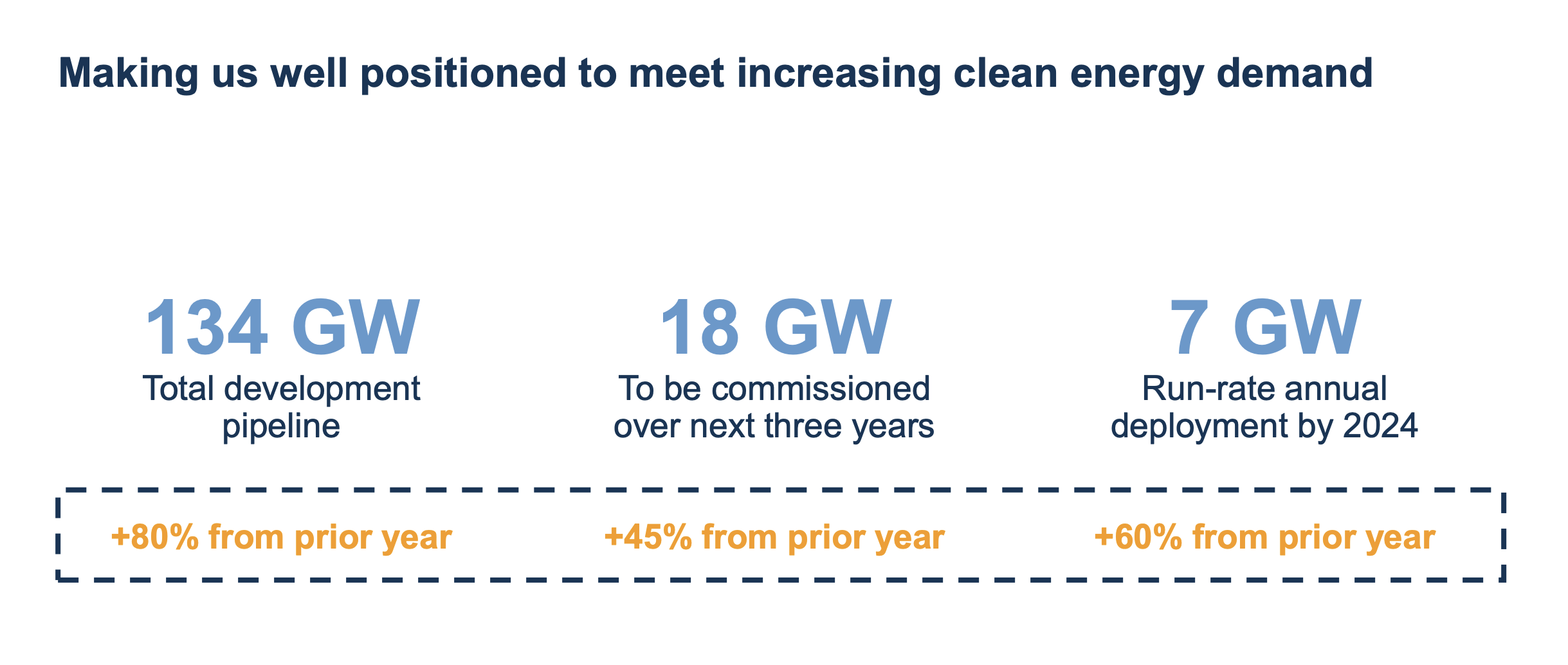

Brookfield Renewable Partners Growth

The company has a massive development pipeline that it’s using to continue its growth.

Brookfield Renewable Partners Investor Presentation

The company’s potential development pipeline is massive. The company’s total pipeline is 134 GW which has gone up 80%, but the most relevant number is the 18 GW that the company is going to deploy over the next 3 years (a 45% YoY improvement). The company’s run-rate annual deployment by 2024 is expected to be at 7 GW (a 60% YoY improvement).

We discussed above how assumptions are that we need 7 TW in new deployment by the end of the decade, and Brookfield Renewable Partners is expected to be 0.1% of this 7-year requirement on an annualized basis. Contributing <1% total, the company has the financial ability to be extremely choosy.

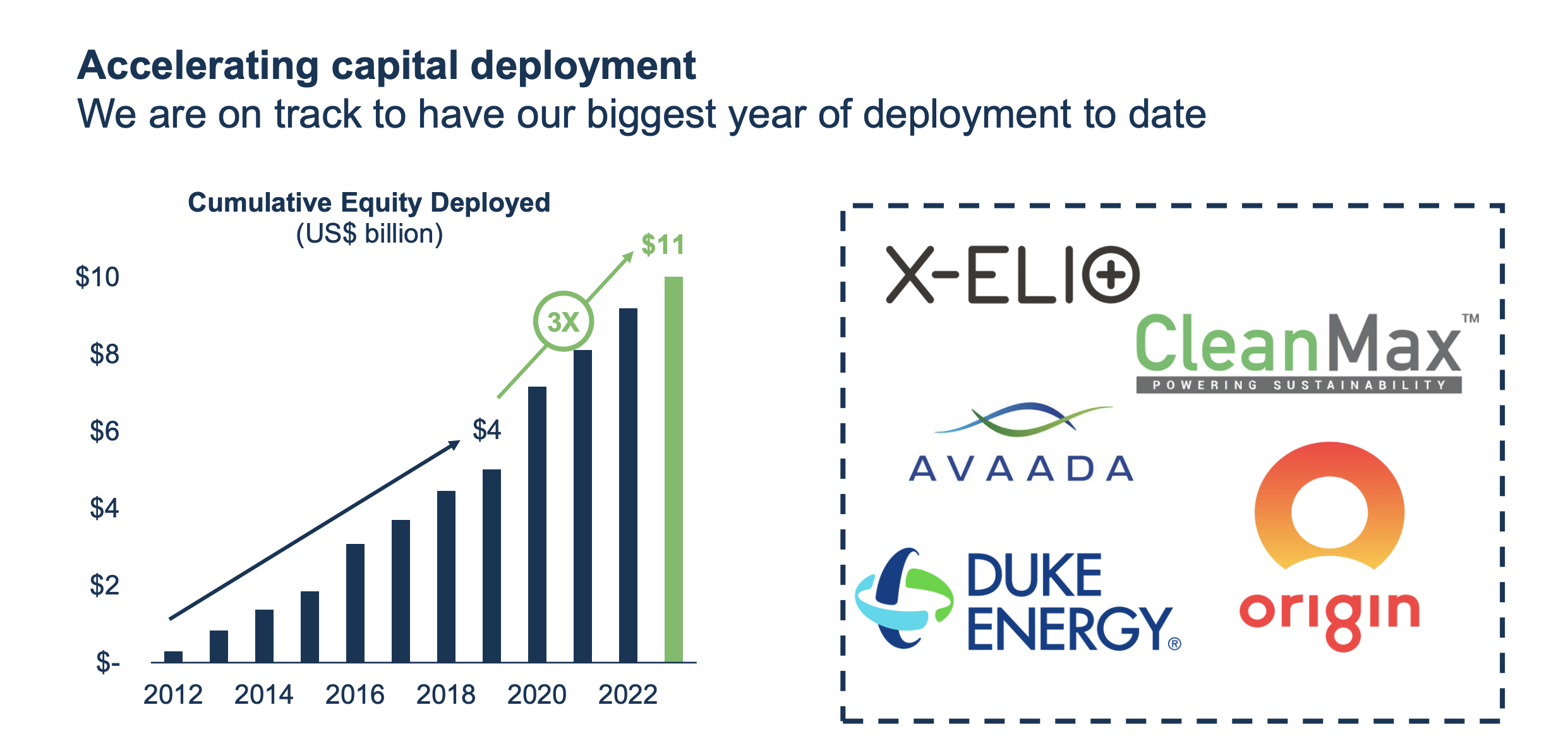

Brookfield Renewable Partners Capital

The capital that the company is deploying, especially with partners is massive.

Brookfield Renewable Partners Investor Presentation

The company is on track for its biggest year of deployment so far, despite higher interest rates. For a $7.5 billion USD company, the company’s cumulative equity deployed is expected to triple towards $11 billion. The company has been rapidly taking advantage of new equity deployments.

Using its cash to partner with other equity companies that have had a tough time in a high interest rate environment is a strong strategy.

Brookfield Renewable Partners Investor Presentation

The above shows the company’s project strategy. A substantial % of the GW of assets is under construction and almost completed, which will mean GW of power providing immediate cash flow. A substantial amount of other production is quick production that the company can quickly bring online. These assets will rapidly increase cash flow.

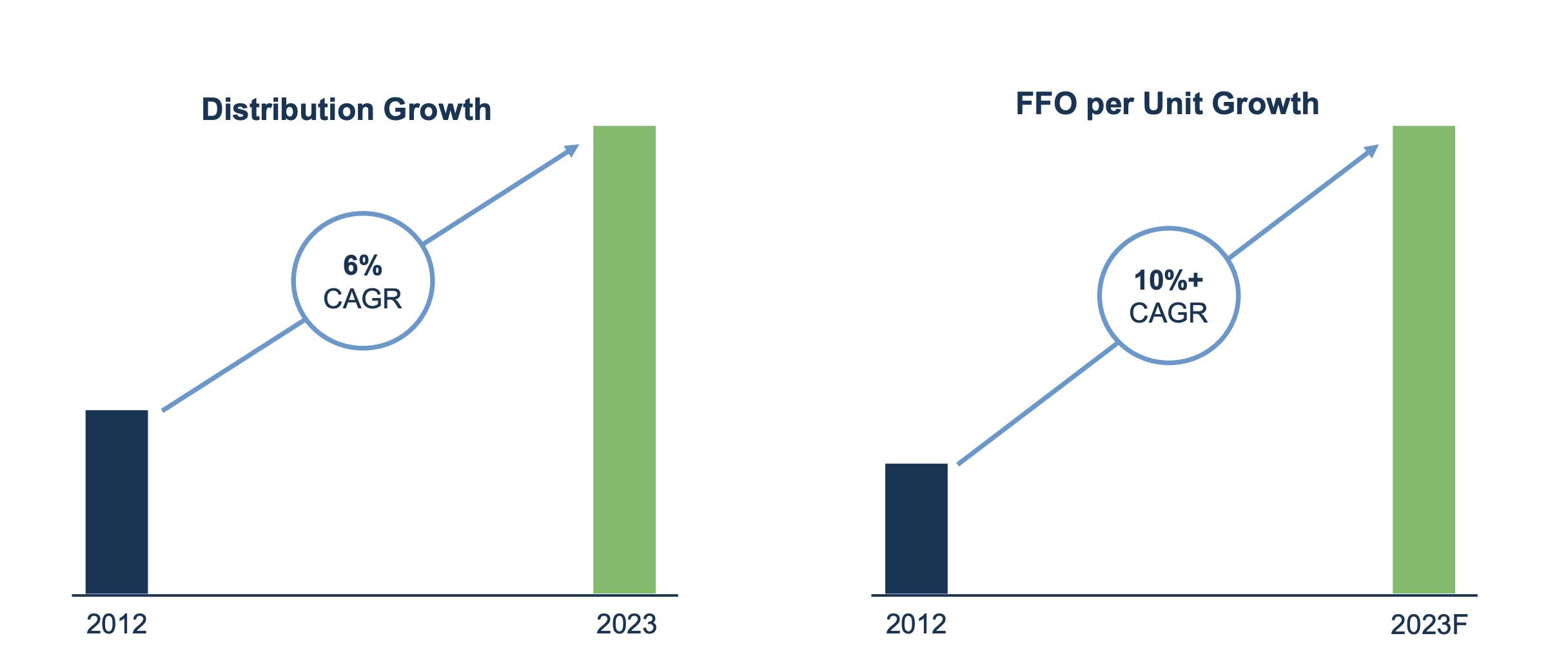

Brookfield Renewable Partners Returns

The company has a dividend of more than 5% and a history of growing it at more than 6% annualized. The company’s FFO per unit growth has been 10%.

Brookfield Renewable Partners Investor Presentation

The company’s model is simple. It can borrow money and lower rates, which combined with its existing capital, enables it to build projects. Those projects provide long-term steady cash flow, ideally, that will keep growing with dividends. All of that will lead to both FFO per unit and at the end of the day distribution growth for shareholders.

Higher interest rates do threaten that model, and that’s something worth keeping an eye out for, along with increased payments from Brookfield Renewable Partners to Brookfield Asset Management. These continued growth and returns make the company a valuable investment. The company is continuing to target 12-15% annual returns.

Thesis Risk

The largest risk to our thesis is two-fold.

The first is that climate change is a big problem and renewable energy is a potential solution. Governments are providing massive amounts of capital for renewable energy growth and that means that the return rate needed on projects is much lower. That could make it harder for Brookfield Renewable Partners to earn the returns to justify investing.

The second is that Brookfield Renewable Partners is effectively a subsidiary of Brookfield Asset Management and passes a substantial % of the earnings up with dividends. That non-alignment between incentives is supposed to be resolved by the benefits for Brookfield Asset Management if Brookfield Renewable Partners outperforms. However, it doesn’t necessarily work.

Conclusion

Brookfield Renewable Partners is an impressive company in the reliable renewable space. There is a massive amount of opportunity to grow here and the company is opportunistically deploying large amounts of capital. As other companies struggle more in an era of high interest rates, the company is also using equity stakes and acquisitions.

Going forward, we expect the company will be able to continue paying its 5-6% dividend yield. On top of that, we expect the company to continue hitting its growth targets to hit its long-term target of a 12-15% growth rate. That growth means even with its recent appreciation, the company is a valuable investment.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")