Photofex/iStock Editorial via Getty Images

Investment Thesis

In September last year, we gave Norsk Hydro ASA (OTCQX:NHYDY) a Hold stance based on our concern about potentially lower aluminum prices going forward. That was a downgrade from our bullish view of the company back in January of 2023.

The share has been marginally up since September, with an increase in the share price of 4.3%.

During Norsk Hydro’s capital market day at the end of November last year, the presentation was primarily focused on ESG and the expected changes in the aluminum industry because of their customers’ race towards zero carbon emission.

The company does have strong ties to premium car manufacturers like Mercedes (OTCPK:MBGAF), Volkswagen Group (OTCPK:VWAGY), and Porsche (OTCPK:POAHY). We do assume they can command a slight premium, as these customers are willing to pay for greener products to reduce their overall CO2 reduction.

However, all this comes at a cost. In this article, we will revisit our previous stance.

Latest Financial Results

Norsk Hydro will come out with its Q4 results on the 14th of February. In the meantime, we will just focus on the third quarter of 2023.

The third quarter of 2023 was not good for the company, regardless of whether you compared it to Q3 of the previous year, or just with the Q2 of 2023.

On the top line, Q3 revenue was 17% lower than Q2 at NOK 44.7 billion. Adjusted net income from continued operation was done 90% from NOK 3.41 billion to NOK 341 million.

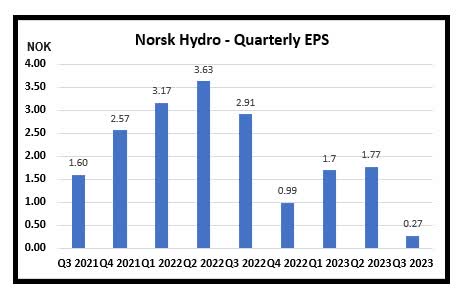

This translates to an adjusted EPS of NOK 0.27 in Q3. The most troubling with the EPS is that it is at lower levels than in earlier years.

Norsk Hydro’s EPS drop. (Data from Norsk Hydro. Graph by author)

If we look at the first nine months of the year, Norsk Hydro’s adjusted EPS is down from NOK 9.70 to NOK 3.75.

Management explained that the main reasons for this large drop in earnings in Q3 came from low economic growth due to rapid monetary tightening, pressuring household spending, and lower business investments. This has put pressure on the demand for primary aluminum.

It was noted that Chinese demand was stronger than expected on strong demand in the renewables and EV segments. This confirms reports we have seen about the recent success the Chinese have had in manufacturing and exporting both EV and renewable products. The export of EVs increased by 62% in 2023.

ROE for the first nine months was 8.5%. This is considerably lower than the 33.6% that they delivered a year ago and was one of the main reasons for our earlier bullish stance. In that article, we compared Norsk Hydro up against the large Chinese competitor Chalco.

Cash at the end of 2023 Q3 was NOK 19.1 billion. Adjusted for this cash, they had a net debt position of NOK 20.4 billion at the end of Q3.

Market development

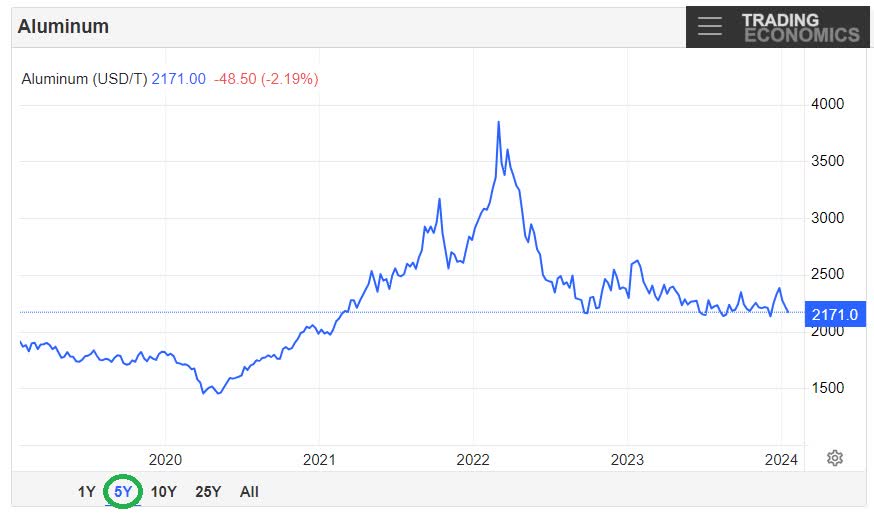

The price of aluminum seems to have found a floor around the USD 2,100 to USD 2,200 level. European smelters’ capacity utilization is still running below 50%, because of the high cost of electricity and the lower price of aluminum.

We believe this low utilization rate is expected to continue through 2024, as higher prices are required for companies, like Norsk Hydro, to restart a smelter that is now down.

Aluminum Price 5-Year Graph (Trading Economics)

Norsk Hydro always hedges the price of aluminum for some portion of its production. As of Q3 last year, they had hedged 440,000 tonnes for this year at a level of USD 2,500 and 300,000 in 2025 for USD 2,400.

Risks and Conclusion

Will there be a recession in 2024 or just a soft landing?

What happens to the economies in the EU and the U.S. matters the most to Norsk Hydro, as these are their two main markets.

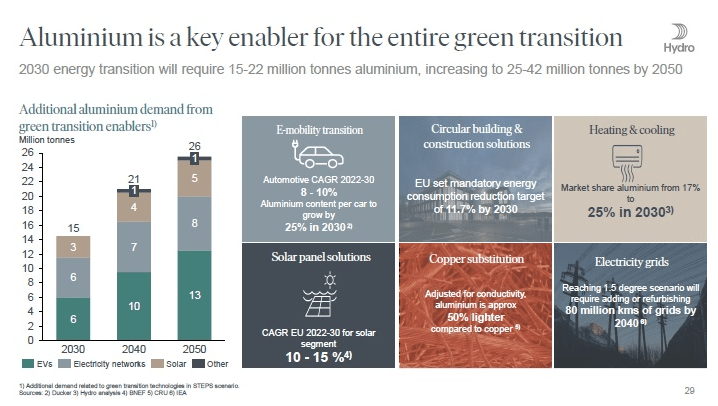

Huge investments are required globally if companies are to transform their industries to produce products like steel, aluminum, and cement. All major building materials. Estimates vary, but we have seen USD 110 trillion which is going to be required from now until 2050.

Consumers will also have to pay some of this through changes to how we move around and where our energy will come from to cool or heat our buildings.

Aluminum’s role in decarbonizing the world (Norsk Hydro – Presentation at Capital Markets Day November 2023)

All these new “green” activities that Norsk Hydro is embarking on require Capex, and this could be a concern.

At the end of November, management raised their annual Capex guidance from NOK 12.5 billion to NOK 15 billion for the period 2024 to 2026.

To do this, they have also tweaked their dividend policy plan, expecting to pay out between 50 and 60% of earnings for 2023, compared to 62% paid out in 2022.

We believe lower earnings and return of capital to shareholders will result in a lower share price throughout 2024, hence we downgrade our stance to a Sell.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")