jetcityimage

Well recognized for its charming mascot, Flo, Progressive Corporation (NYSE:PGR) is one of the largest insurance companies in the world by market cap, sitting narrowly under $100 billion as I write this. Curiously, the stock is at its all-time high, with a P/E like a tech company. While many other companies’ shares slumped in value during the events of 2022, PGR kept plugging along.

It’s worth examining what exactly investors are getting with this established and friendly brand. I’ll review the financials and the outlook for the company. Ultimately, as good as the company is, I think PGR is overpriced, and that makes it a SELL.

Current Business

Progressive primarily deals in car insurance. They also offer products related to property, workman’s compensation, and various other products. Car insurance easily makes up the majority of their business. With 29.5m policies in effect as of November, 19.4m were under their personal auto line, with an additional 1.1m policies in their professional lines.

Progressive’s Nov. Results (progressive.com)

As can also be seen above, slightly more of these policies are underwritten directly through the company than by outside agents. Direct sales occur on their website, through their app, or over the phone. Where possible, the company tries to bundle different insurance products into a single offering in order to increase revenue and build stronger customer relationships.

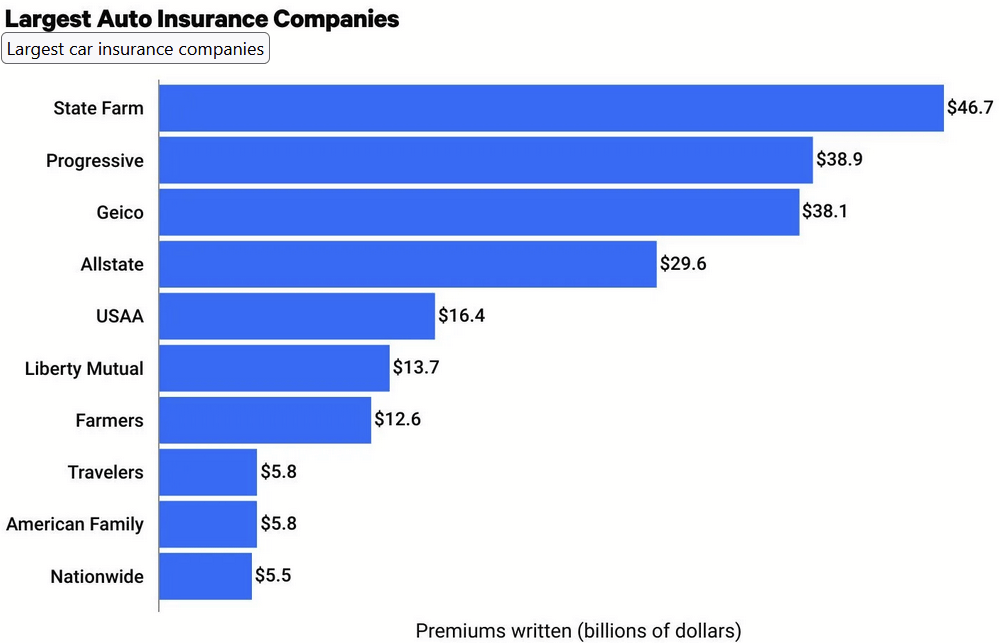

The car insurance market is very competitive, and Progressive has many rivals in that space. According to ValuePenguin, as of January 2024, Progressive had the second-largest slice of American market share for car insurance, at 14.1%.

valuepenguin.com

Based on the figures they provide, the top 10 auto insurers control about 77% of that market. It’s a tight space.

The company’s extra cash is invested, ideally to get a better return and yield than simply keeping it in the bank, which is normal in insurance.

Q3 2023 For 10Q

In Q3 2023, the company reported $61.9 billion in investments on its balance sheet. Due to regulatory constraints, most of these are in fixed-income securities, and very little is in equities.

Q3 2023 Form 10Q

Overall, the balance sheet is reasonably strong. The portfolio itself is sufficient to cover most of its liabilities, and tangible assets overall are well in excess of that.

Financial History

What kind of results has this business model gotten? The company experienced successful growth over the past decade to become one of the leading auto insurers in the country. I’ll include YTD data for 2023 (up to Q3 and based on the company’s news releases for October and November).

Author’s display of 10K/10Q/reported data

Progressive is and continues to be a steady grower and compounder. How has this been reflected in earnings and returns to shareholders?

Author’s display of 10K/10Q/reported data

Their earnings have trended toward growth. The strange rise in 2020 was due to a lack of claims amid reduced traffic (and therefore reduced accidents) during the COVID lockdowns. Dividend payouts show that these extra earnings were ultimately given out to shareholders.

Despite continually rising revenues, earnings were down in 2022. In their 2022 Form 10K (pg. App.-A-51), management explained in the Operating Results that this was a combination of a decline in the market value of their portfolio’s securities, impairment of goodwill, and (importantly) losses incurred from their Property Line, primarily policies in the Southeast, due to storms.

Author’s display of 10K/10Q/reported data

Balance sheet shows unsurprising growth of assets and liabilities, given what I’ve already mentioned.

Author’s display of 10K/10Q/reported data

Yet, asset growth has been 3.32x since 2014, while TBV has only increased 2.4x, somewhat due to the more recent challenges.

A Look to the Future

As I mentioned earlier, this company, despite being insurance, is trading at a very high multiple. That suggests there is optimism about growth in earnings, so where would the growth be?

Auto Line

To reiterate, Progressive is the #2 car insurer by market share. The big ten have 77% of this market. The opportunities are shrinking. Progressive already operates in all 50 U.S. states. There’s not much new territory to penetrate. For the Auto Line revenues to grow, they need to be able to raise prices without losing customers, acquire shares from these strong competitors, or ride the wave of a growing market. Should anything of these things occur, I believe the impact will be small. Let’s start with pricing, and I’ll quote the company in their 2022 10K again:

While a leading brand is key to our success, we operate in a very competitive industry where price is a very strong consideration for consumers when they shop or decide to renew their policies. Consequently, competitive prices are one of our four strategy pillars.

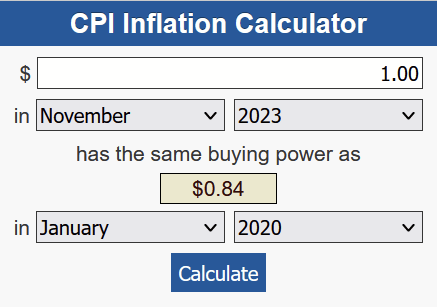

So they are aware of this, and I expect they will be hesitant to raise prices significantly over time. Now, they have been making substantial increases to keep up with recent high inflation, and that’s to be expected. Of course, that’s only nominal growth.

Inflation Calculator (Bureau of Labor Statistics)

If you look back at the chart on revenues, that $55.7b for 2023 is more like $46.8b in 2020. So yes, Progressive at least has some pricing power against inflation, but let’s not let it warp our perception of growth too much.

As far as taking market share goes, they may be able to do that with the smaller insurers, but I believe the other big nine will also be doing that. They also have potent marketing campaigns. Flo is pitted against the likes of the Gecko, Mayhem, and Jake from State Farm. It’s one of those signs where Progressive is a great business but doesn’t quite have a moat all to itself.

Lastly, I believe the number of drivers who need insurance is unlikely to rise by any major degree. There are already 240m licensed drivers in the U.S. With the millennials all grown up now and declining birth rates for years, there’s not a large, new cohort of drivers for insurers to scoop up anymore. Realistically, Auto Line’s growth will be incremental.

Property Line

Progressive’s Homeowner’s Insurance

This is really where the company wants to lock in growth and may explain the high price of PGR. As previously stated, Progressive likes to bundle its products with its Auto Line, as this is not only a larger sale, but they believe those customers are more likely to renew. This topic was a major source of discussion in the Q3 Earnings Call. I’ll quote some of the management on it:

The thing to consider there, Josh, is which segments we’re growing in would be somewhat indicative of where they’re coming from. So we are continuing to grow well in the more preferred segments of our business, the “Robinsons,” but also we call “Wrights” who are homeowners that do not bundle yet their home and auto with Progressive. And we have not been growing, actually this year, we’ve been shrinking a little bit on the standard end. So the nonstandard end of the spectrum. So that bodes really well for our future growth because, obviously, those customers stick with us longer.

Part of the struggle is that the Property Line has not been profitable lately, largely due to large storms in 2022 and the company’s exposure to Florida:

Q2 2023 Company Presentation

While I think there is some intelligence to the idea of leveraging their existing book of Auto customers and turning them into bundle customers as a means of growth, the execution has not started well. This was also mentioned in that earnings call:

Yes. I think we start with what we started with about a year ago, and that was to de-risk the book and have less new apps and policies in volatile states and more in nonvolatile. And you saw the data on that in the queue that we believe we’re doing a great job. We’re non-renewing about 115,000 policies in Florida, we’re just over indexed in Florida. And so we love Florida. We have a lot of Robinsons. We have a lot of autos and we continue to have a lot of homes, but we were not making money and we needed to non-renew some. So that will happen over the next year or so.

While the company is going to improve its risk models to underwrite less and with better prices, I personally think this could be a warning. Perhaps expanding into a line that could be as big as Auto is them deviating from their strong suits.

That isn’t to say that they won’t pull this off, but where car insurance is steadier and more predictable, property insurance is a different product with different risks. An investor has to ask, “If increased revenues also come with increased costs, is it really earnings growth?”

Having said that, if we assume that they learned from the problems of Florida and other Gulf States, successful execution of the strategy could grow earnings significantly.

Valuation

So let’s talk about the current valuation before I do my own. The market cap of Progressive sits just below $100b, a big company! Yet, the TBV is only $16.6b. Not many insurance or financial companies will trade that high above TBV. YTD net income for 2023 is also $3b, so where is the $100b in value?

Well, first consider that some of this is due to market behavior since the events of 2022 (war in Ukraine, inflation).

Seeking Alpha

If we look at total returns since Jan. 1, 2022 to today for the S&P 500, the S&P Insurance Select Industry Index, and PGR, we’ll notice that both of the latter beat the former. Insurance companies are often seen as defensive stocks, so the whole sector stayed up on that, regardless of earnings. Insurance companies are seen as safer, so people pay more for them.

Still, PGR’s return has been more than that of the Index, so people must expect growth. If earnings are typically around $3b, then to me that suggests the market thinks they’ll grow to about $10b reasonably soon. What are the possibilities, then? If we assume progressive only averages 3% earnings growth each year, then $10b doesn’t happen.

Author’s calculation

If we assume Progressive only averages 15% growth (which would be commendable for the company of that size), it happens in 2032, not exactly soon.

Author’s calculation

If we average 25% growth for at least the first six years, we get there by 2029.

Author’s calculation

Even if it’s not for a full decade, 25% is a lot to accomplish, especially for a big insurer like Progressive. It’s especially tough if the source of growth still needs to be made a profitable segment first. While I think Progressive is a great company, I’d like to buy it with more modest growth assumptions. If I value it for 3% growth and apply my standard discount rate of 10%, here is the value of the next decade’s earnings.

Author’s calculation

That’s $21.3 billion. Added to the tangible book value of $16.6b and divided by the number of shares, which tells me the fair value of the company is $64.50. The current price of $170 seems rich to me.

Conclusion

Progressive is an excellent company with one of the most recognizable brands in insurance. Yet, it’s trading at an all-time high, as if the #2 car insurer has a path to meteoric growth. Rather, the premium is borne out of investor preferences for “defensive” insurance stocks in the wake of 2022 and anticipation of growth from the Property Line that isn’t making money, due to misguided risk assumptions.

The strategy for growth is a smart one, but investors should watch a bit longer to confirm that they can actually start to do it, and even when that day comes, they should be careful not to overpay for a bright future, or else they won’t make money. Maybe, at best, this is a $70b business, but I don’t see a justification for $100b. In the meantime, I wouldn’t want to risk my hard-earned money buying PGR, and if I did own it, it would be an easy SELL at this price.

Q2 2024 Earnings Call Transcript")