Eugene Mymrin/Moment via Getty Images

SoFi Technologies, Inc. (NASDAQ:SOFI) is a promising, high-potential investment in the fintech market ahead of the company’s 4Q-23 earnings.

SoFi Technologies is scheduled to report quarterly earnings on Monday, January 29, 2024, and I think we could be headed for a blowout earnings release, particularly as inflation is retreating which might have spurred the fintech’s account growth in the fourth quarter.

With GAAP breakeven also expected for 4Q-23, I think the odds are in favor of a rather strong earnings presentation at the end of January.

My Rating History

SoFi Technologies has underperformed expectations in the last three months which may have something to do with uncertainty about whether or not the fintech could move towards GAAP profitability in 4Q-23.

I upgraded my stock classification to Buy before the fintech’s third quarter earnings in October as I anticipated robust growth in new accounts which SoFi Technologies did indeed deliver.

Before my upgrade, I was very bearish on SOFI for a long time due to its high valuation and deeply negative adjusted EBITDA.

With that being said, the fintech’s member growth is convincing and GAAP profits are imminent. SoFi Technologies’ stock surged in December, but in January dipped again, which might be an opportunity to buy into the fintech before it releases fourth quarter results.

Expect Record 2023 Results

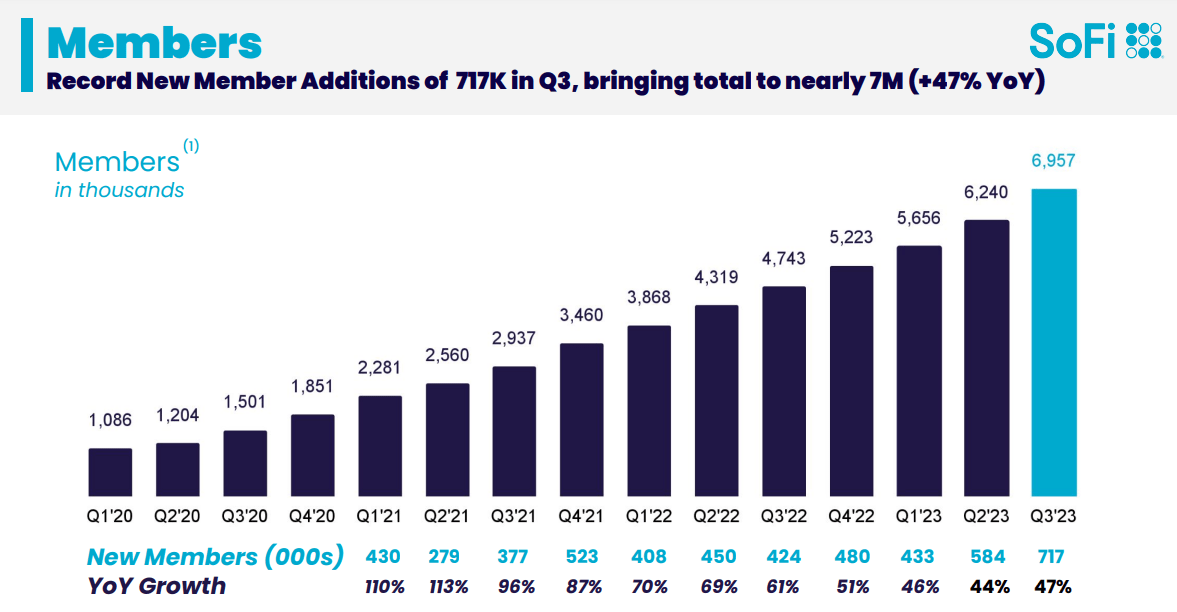

What has triggered previous stock rallies for SoFi Technologies was the accomplishment of robust growth in members. SoFi Technologies added a rather impressive 717K new members to its business in the third quarter which showed the second consecutive acceleration in terms of absolute member adds.

Taking into account the fintech’s member momentum, particularly in the last two quarters, I think it is probable that SoFi Technologies ended 2023 with a record number of members using its products.

SoFi Technologies brought its products and services to almost 7 million members as of the end of the third quarter and I would not be surprised for the fintech to report record new member adds in the fourth quarter on January 29, 2024.

Student loan payments also resumed in the fourth quarter which might be an additional catalyst for the fintech’s growth. Generally, the combination of accelerating member momentum in 2Q and 3Q (based on absolute member growth figures), the restart of student loan payments, and subsiding inflation are reasons why I expect to see a blowout earnings release next week.

Members Growth (SoFi Technologies)

Of course, I don’t have any special insight into SoFi Technologies’ finances, but I think there is a possibility that the fintech will report its highest number of member adds ever for 4Q-23.

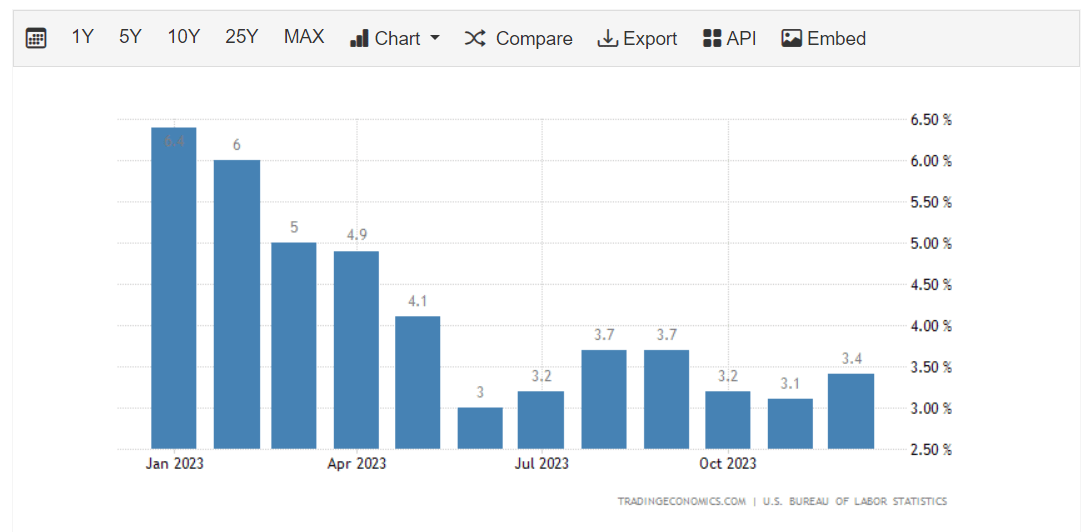

First, the U.S. economy expanded at an annual rate of 5.2% in the third quarter, meaning the economy probably provided robust tailwinds for businesses.

Second, and most importantly, inflation is retreating which is freeing up cash and allowing consumers to spend more money. A fintech like SoFi Technologies which is offering checking accounts, investment products, and personal loans might profit from these trends. With inflation on the back foot, I think SoFi Technologies could be a major beneficiary of these trends, not only in 4Q-23 but also in 2024 more generally.

Inflation did see a bit of a flare-up in December, with inflation going up to 3.4%, but the general trend is positive and inflation is nowhere near where it was in 2023. For consumers, this means more spending power, and for SoFi Technologies, it means more demand for its banking products.

Inflation (Tradingeconomics.com)

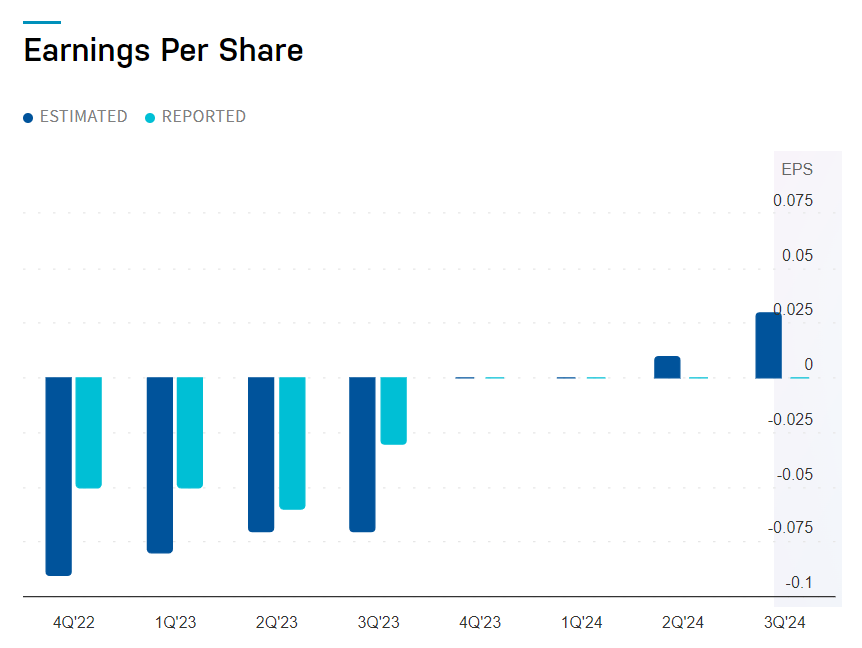

What Does The Market Expect For SoFi Technologies’ 4Q-23?

The market models a breakeven quarter for SoFi Technologies after the fintech said that it targets positive GAAP earnings in 4Q-23. Reaching this breakeven milestone could be a catalyst for investors to reevaluate SoFi Technologies as not just a growth stock but as a profitable growth stock. Thus, I think that the earnings release for 4Q-23 is one of the most important earnings releases in the fintech’s recent history.

Earnings Per Share (SoFi Technologies)

Potential For A Breakout

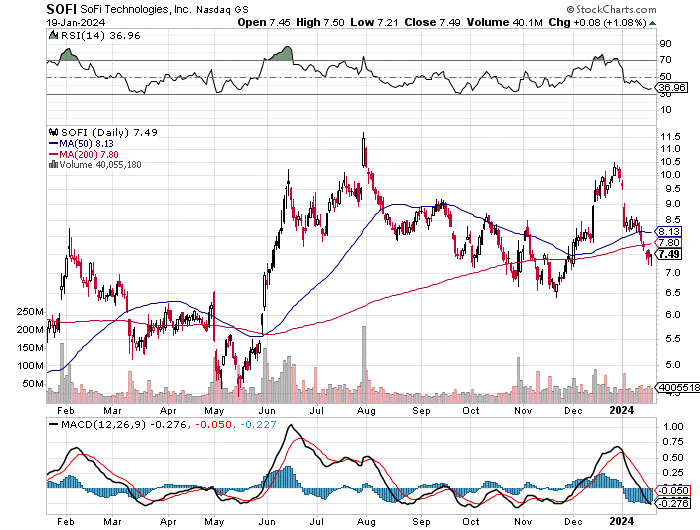

A robust earnings report for 4Q-23, particularly as far as member growth and GAAP profitability are concerned, could be a catalyst for a breakout move for SoFi Technologies.

SoFi Technologies’ stock sits at a key level, too: The stock price of $7.49 sits slightly below $7.80, which is where the 200-day moving average line presently runs. This is an important support level for SoFi Technologies and a more serious down move from here would deteriorate the chart picture substantially.

With the upcoming 4Q-23 earnings report, however, potentially acting as a catalyst, I think there is a good chance that investors are going to see a breakout move to the upside after earnings.

Moving Averages (StockCharts.com)

SoFi Technologies’ Consolidation Provides An Entry Opportunity, Low Sales Multiple

I rarely buy stocks when the market has caught on to them. I like to find highly promising stocks with short-term catalysts before the market causes their stock prices to move. Thus, the present setup for SoFi Technologies, ahead of 4Q-23, is quite compelling.

The fintech’s stock has fallen back from $10.50 to slightly below its 200-day moving average line but taking into account SoFi Technologies’ 2Q-23 and 3Q-23 upside momentum in members, I think the fintech is headed for a robust earnings release later this month.

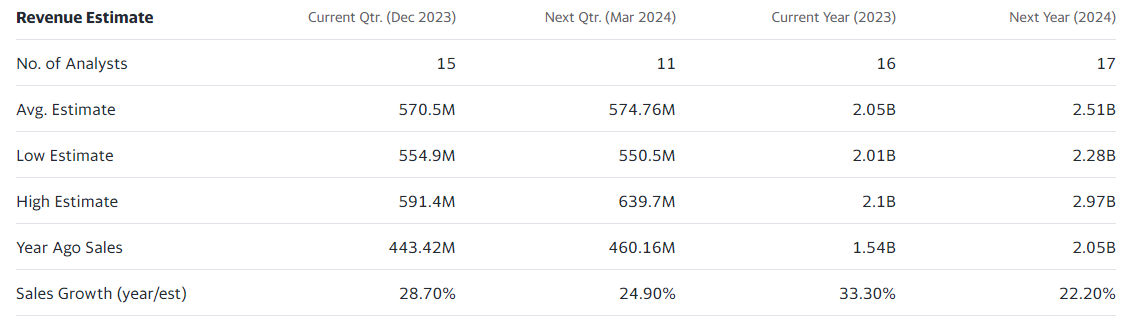

Presently, SoFi Technologies is selling for 2.9x sales estimated for 2024 which I think is not an aggressive sales multiple, particularly not with the fintech set to cross over into positive GAAP profitability in the near term.

The market presently also models a rather solid 22% sales growth for 2024. Upstart Holdings Inc. (UPST), an AI-focused lending platform, is selling for 3.9x sales despite not being profitable and not nearly as promising a business upswing as SoFi Technologies.

Revenue Estimate (Yahoo Finance)

Unique Risks With SoFi Technologies

SoFi Technologies has proven to be a highly volatile stock and the company is often making outsized moves after the fintech’s quarterly reports, to both the downside and the upside.

Based on public data aggregated by MarketBeat, SoFi Technologies has a short interest ratio of 13% which makes the fintech quite highly shorted. Thus, there is a chance of a short squeeze in the event of a robust 4Q earnings report, but also the risk of a sharp move to the downside (and an increase in short interest) if the fintech fails to beat expectations.

A failure to transition the business to GAAP profitability is the biggest potential risk factor in the short term, in my view.

My Conclusion

SoFi Technologies is scheduled to release earnings for the fourth quarter on January 29, 2024, and I think the fintech is set for a blowout report.

SoFi Technologies has guided for at least a breakeven quarter in terms of GAAP profitability and even a slight outperformance on the EPS level could set the stage for a bigger breakout in 2024.

Falling inflation and a strong U.S. economy provide a favorable backdrop for SoFi Technologies as well. Thus, I am looking to see a blowout number on new member adds as well.

With 22% anticipated sales growth for SoFi Technologies and the company selling for a low sales multiple given its growth, I am optimistic that we could see the beginning of a larger stock rally later this month.

Q2 2024 Earnings Call Transcript")