Yuichiro Chino/Moment via Getty Images

Catalyst Pharmaceuticals, Inc. (NASDAQ:CPRX) is a promising biopharmaceutical stock that treats rare neurological and epileptic diseases with Firdapse for LEMS, Fycompa for epilepsy, and Agamree for DMD. CPRX is also dealing with lawsuits to stop the entry of Teva’s (TEVA) generic version of Firdapse into the market. Currently, Firdapse is protected until 2026 or until a court rules on the infringement matter. On the other hand, CPRX has the exclusive US commercialization license of the FDA-approved drug Agamree, aiming towards a meaningful market share if it successfully manages retail price and insurance coverage. However, overall, I don’t think the stock’s risk-reward profile is compelling enough to either be bullish or bearish at this point. Hence I rate it a “hold” at these levels.

Firdapse and Fycompa: Business Overview

Catalyst Pharmaceuticals is a commercial-stage biopharmaceutical company founded in 2022, with an IPO in 2006. CPRX, headquartered in Coral Gables, Florida, specializes in commercializing and developing treatments for rare neurological and epileptic disorders. CPRX’s main products are FIRDAPSE and FYCOMPA, representing 65.6% and 34.4% of the company’s total product revenues for the first nine months of 2023, respectively. This makes CPRX essentially a bet on these two biopharmaceutical products.

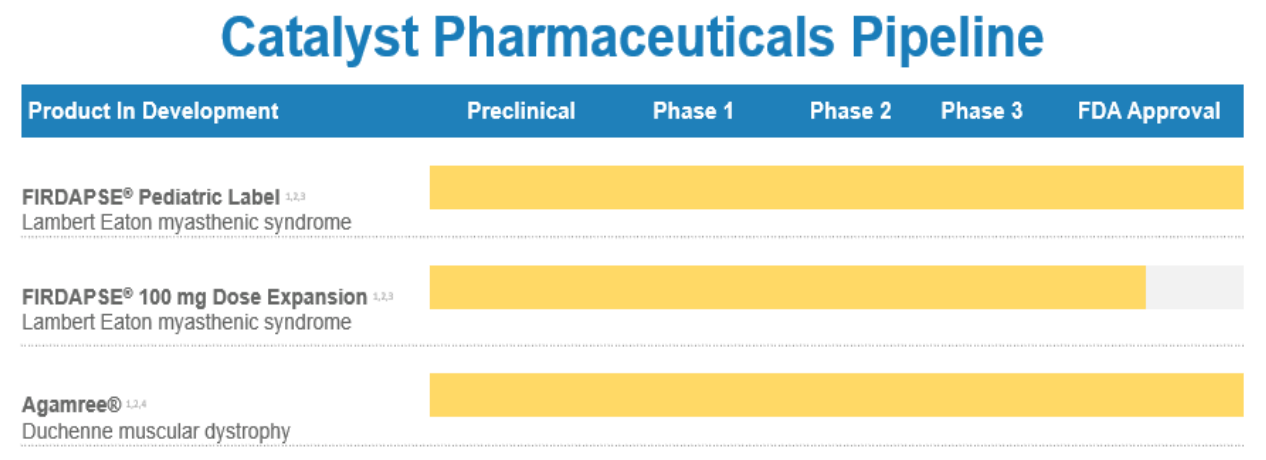

Therefore, digging into the company’s product pipeline, CPRX commercializes a proprietary portfolio that includes Firdapse for rare neuromuscular disease approved in the US for Lambert Eaton Syndrome [LEMS] and Ruzurgi for treating pediatric LEMS patients. The company is also in Phase 3 clinical trials for LEMS for patients older than six to maintain muscle strength and improve the perception of the patient’s physical well-being. For epilepsy, the company delivers Fycompa to control seizures with convulsions. More recently, CPRX completed the acquisition of Fycompa in January 2023, expanding its IP portfolio with an established epilepsy drug.

CPRX collaborates with other pharmaceutical companies with license agreements and partnerships, such as BioMarin Pharmaceutical Inc. (BMRN), Endo Ventures Limited, and Santhera (OTC:SPHDF). For instance, in October 2023, the drug Agamree was FDA-approved for Duchene muscular dystrophy [DMD] disorder for patients two years and older. Santhera Pharmaceuticals, a Swiss company, developed this medicine, and CPRX holds the exclusive license of Agamree in the US. CPRX is planning the launch of Agamree in the US in Q1 of 2024, potentially boosting CPRX’s revenues significantly, which is contingent on the market reception for this product. The agreement between the two pharmaceuticals includes a $36 million payment to Santhera and around $105 million for milestones in sales and royalties. For context, CPRX generated roughly $102.69 million in revenues, according to its latest quarterly report. Upon Agamree’s commercial launch in Q1 of 2024, the company aims to start a comprehensive patient “Assistance Program” to ensure affordable access for all DMD Patients, minimizing patient co-pays and deductibles, according to its latest investor presentation in January 2024.

Source: Corporate presentation, January 8, 2024.

Agamree has the orphan drug designation for rare pediatric conditions, a status the FDA grants for seven years of market exclusivity. This type of FDA designation is considered an incentive for rare diseases that otherwise might not be profitable to develop. Thus, Agamree is now officially FDA-approved, though, as previously noted, it’s too early to make a call on how important Agamree will be for CPRX. Nonetheless, I believe the first quarter of 2024 will be key. The next earnings call should contain information regarding Agamree’s initial performance of its commercialization phase. I am optimistic about Agamree’s prospects, as it targets a relatively large population. For context, between 11 to 13 thousand patients could benefit from this drug, and the treatment regimen is 6 mg per kg per day, implying a relatively steady revenue stream.

Why Agamree is Key: Risk Diversification

Unfortunately for CPRX, Teva Pharmaceuticals is also trying to market a generic version of Firdapse. TEVA alleges that CPRX’s patent, which expires in 2037, is not infringed by their generic drug. As you might expect, CPRX took legal measures to defend its IP, and Firdapse may end up upholding its patent with the lawsuit filed in New Jersey in March 2023. This could extend the patent’s validity until May 2026 or until a court decision regarding patent infringement. However, this remains an ongoing legal matter for the company, and the results will undoubtedly be material for CPRX’s long-term prospects. After all, Firdapse represents 65.6% of the company’s revenues, so this issue strikes at the core of the company’s business.

Source: Corporate presentation, January 8, 2024.

This is why Agamree’s commercialization is key for CPRX. It’s an opportunity to benefit from a market with limited competition due to its effectiveness and designation as an orphan drug and rare pediatric disease. But, if successfully commercialized, it could diversify CPRX’s revenues and reduce its dependence on Firdapse, mitigating its risk profile for investors.

However, to take advantage of this opportunity, CPRX has to implement an effective commercialization strategy and manage the related costs, trying to maximize profits. The success of this strategy will define the company’s financial performance in the next quarters. Indeed, this will be the main challenge for CRPX’s new CEO. Richard Daly was appointed CEO in October 2023, effective January 2024. Thus, he’ll oversee Agamree’s initial commercialization efforts and successfully defend its Firdapse IP against TEVA’s generic competitor product. He is a seasoned pharmaceutical executive with a wealth of experience in the commercial side of the industry, but time will tell if he’s up to the challenge.

Source: Corporate presentation, January 8, 2024.

Fairly Valued and Contingent on Two Catalysts: Valuation Analysis

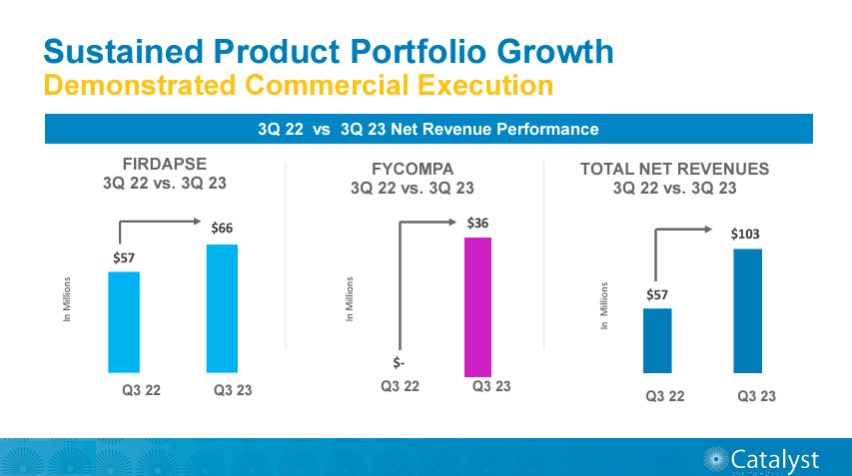

According to CRPX’s most recent earnings call, the company reported relatively promising results during Q3 2023. Their total revenue was about $102.69 million, of which 99.9% came from product revenue. In this context, product revenue is essentially the sales of its leading products, Firdapse and Fycompa. Also, the new FDA-approved Agamree promises the opportunity for a significant impact on the US market, which I anticipate will be product revenue as well. This makes CPRX’s licensing and other revenues relatively irrelevant to our valuation.

Source: TradingView.

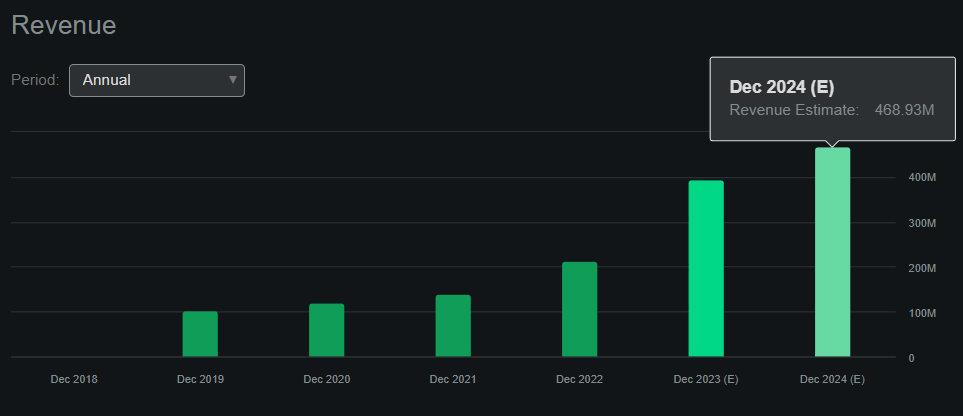

So from a valuation perspective, it’s worth noting that Seeking Alpha’s dashboard on CPRX projects $468.93 million yearly revenues for 2024. This would be a 19.1% YoY revenue increase compared to 2023. Moreover, using the expected 2024 revenue figures and CPRX’s market cap of $1.73 billion, I calculate it trades at a forward P/S ratio of roughly 3.69. If we compare this valuation multiple to the sector’s median forward P/S multiple of 3.67, CPRX would appear to be priced in line with its peers.

Nevertheless, I would argue that this valuation multiple largely depends on Agamree’s future sales performance, which remains a wildcard. Also, Firdapse’s ongoing IP legal battle with TEVA is key, as a generic competitor should significantly hurt CPRX’s long-term prospects. Both of these issues could be positive catalysts if they resolve favorably for the company. For instance, if Agamree’s revenues are surprisingly high and the company successfully defends its Firdapse patent, I’d argue that the current valuation is cheap. In fact, if Firdapse’s patent holds against TEVA, the additional upside of the dose increase is pending FDA approval. However, if Agamree disappoints and CPRX’s Firdapse patent fails against TEVA’s generic drug, it’d be a devastating blow to the company’s outlook, and I’d lean bearish.

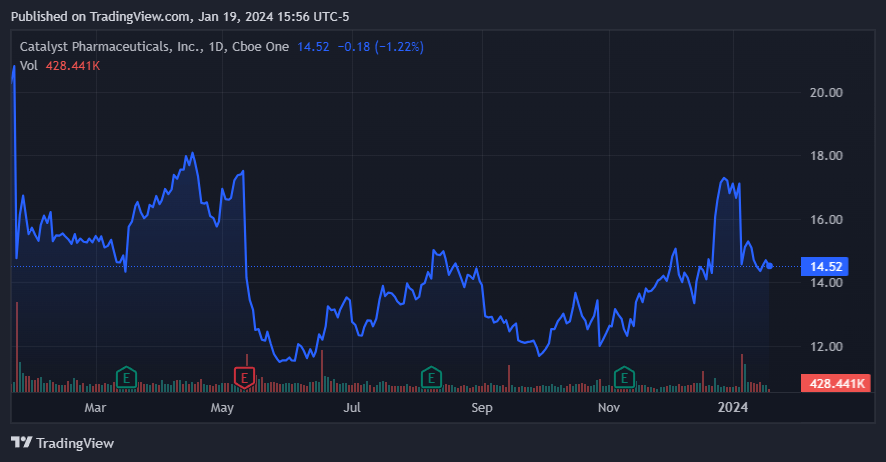

CPRX stock has treaded water during the last year. (Source: TradingView.)

Lastly, it’s also worth noting that CPRX’s latest balance sheet shows cash and equivalents of roughly $121.0 million, which has been trending lower consistently since December 2022, when it stood at about $298.4 million. Moreover, I estimate CPRX’s trailing twelve months cash burn at approximately $113.7 million. I obtained this figure by adding up the company’s cash from operations, CAPEX, and purchase of intangibles over the TTM period. Thus, at the current rate, I estimate that CPRX has close to 2.59 years left of cash runway at the current cash burn rate. Naturally, this is just an approximation, but it shows that cash concerns are relatively mild for now, in my view.

Conclusion

Overall, I’ve identified two key issues surrounding CPRX. You can think of these as bullish or bearish catalysts that could set the tone for the stock. However, for now, I find it difficult to predict either Agamree’s initial sales performance or the result of its legal battle with TEVA. Given that the stock appears to be already trading in line with the rest of its sector, I find no reason to lean bullish or bearish on CPRX. Hence, I rate the stock a “hold,” but I will reassess my stance after these catalysts play out.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")