Tim P. Whitby

The Vita Coco Company, Inc. (NASDAQ:COCO) has proven to be a rewarding investment since its 2021 IPO, providing an impressive return of 81.04%. The company’s performance has been consistent, exceeding EPS expectations for six consecutive quarters and demonstrating a steady growth in its top line. The management’s upward revision of its FY 2023 guidance indicates a strong future, with the company projected to triple its EPS. While the forward P/E ratio of 31.13 and a high short interest of 15% might raise eyebrows, it’s crucial to consider Vita Coco’s strategic focus on the coconut water market. This sector is growing faster than others due to its price resilience, and Vita Coco has successfully maintained a leading position. The company is expecting a strong FY2023 and is targeting a market that is expected to grow at a CAGR of 10.77%, reaching $4.73 billion by 2029. Therefore, for investors seeking a long-term opportunity, Vita Coco presents a compelling case for consideration.

Stock trend since IPO (Seeking Alpha)

Company overview

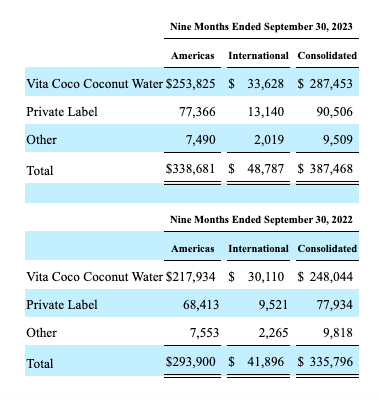

Vita Coco may be a smaller contender in the beverage industry with a market cap of $1.39 billion, but it has carved out a niche for itself. In 2004, it introduced the first line of natural coconut water to the U.S. market, ahead of beverage giants PepsiCo (PEP) and Coca-Cola (KO). The majority of its revenue is still derived from its branded coconut water products. However, it has diversified its product line through acquisitions, adding Runa, Ever & Ever, and PWR LIFT to its portfolio, which fall under the ‘Other’ category. It also offers a private label that includes coconut water and oil. While the ‘Other’ category is experiencing a YoY sales decline across its Americas and International segments, which is a secondary priority for the business at this point in time.

Q3 2023 YTD versus Q3 2022 YTD (Sec.gov)

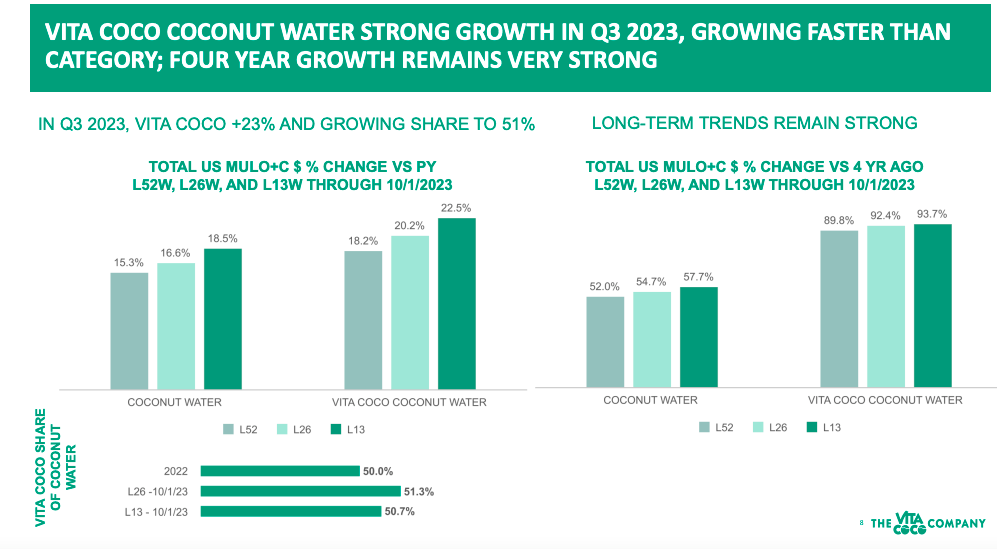

The coconut water category has demonstrated resilience, outperforming other beverage categories, and showing less sensitivity to pricing fluctuations. Within this category, Vita Coco’s water continues to grow at an above-average rate. This is also where the company is focused on growth through innovations and multipacks.

Strong growth within the category (Investor presentation 2023)

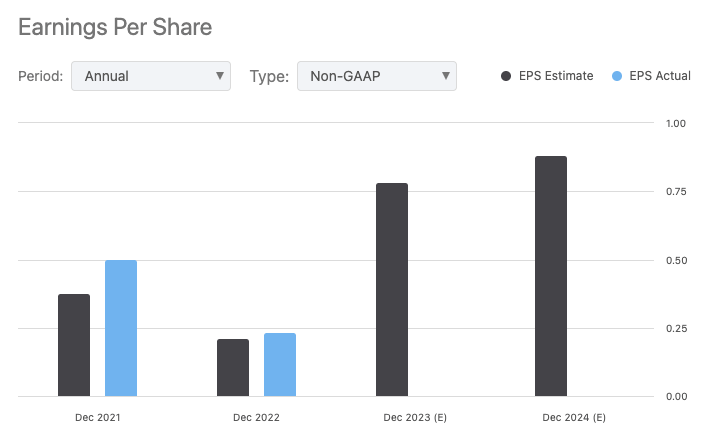

The company’s top line has been on a steady upward trajectory, growing at a 3-year CAGR of 14.64%. Despite a dip in its EPS to $0.23 in FY2022, the company’s EPS is projected to triple, potentially reaching $0.79 per share in FY 2023.

Annual EPS performance (Seeking Alpha)

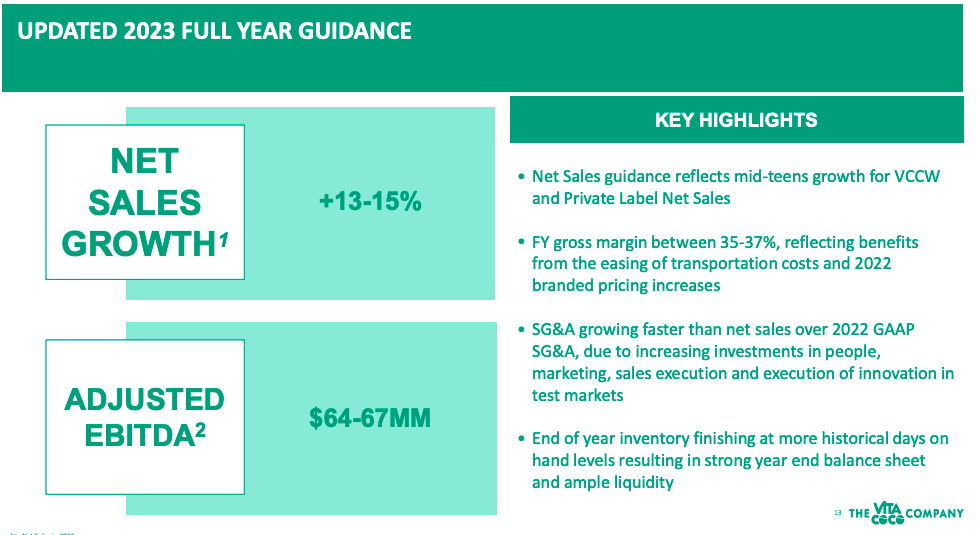

Vita Coco anticipates sustained growth in its core products and sees significant growth opportunities within its newer investments. In Q3, the company raised its FY 2023 guidance for Adjusted EBITDA from $56-$60 million to $64-67 million. It also projects a sales growth of 13%-15% YoY, up from the previous estimate of 10%-12%. This upward revision signals the company’s confidence in its growth and potential upside.

Improved FY2023 guidance (Investor Presentation 2023)

Financial overview

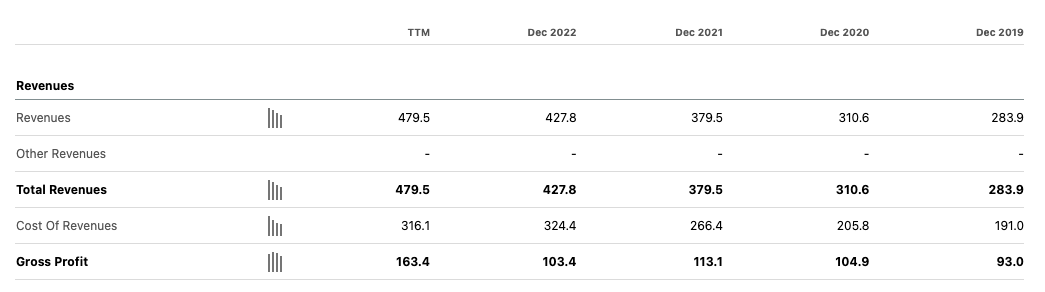

Since its initial public offering, Vita Coco has demonstrated robust performance despite its relatively short financial history. The company’s top line has shown consistent growth year after year, and it’s on track to mark its fifth consecutive year of growth in FY2023, with a projected increase of 13% to 15% YoY.

Annual revenue and gross profit (Seeking Alpha)

The company’s net income has seen a significant uptick from FY2022 to TTM, currently standing at $37 million. This upward trend in net income underscores the company’s strong financial health.

Annual net income (Seeking Alpha)

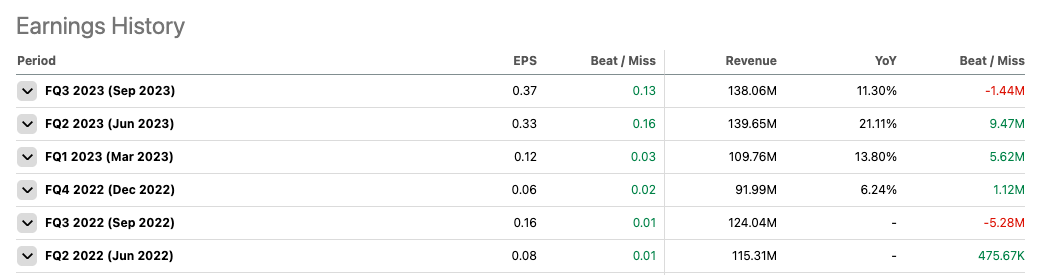

Vita Coco has consistently outperformed its quarterly EPS expectations for the past six quarters. This consistent performance instills confidence in the company’s ability to deliver strong results in the final quarter of FY2023.

Quarterly earnings history (Seeking Alpha)

A look at the company’s Levered Free Cash Flow reveals a positive TTM of $68.8 million, a substantial increase from the previous two fiscal years. This positive cash flow enables the company to reinvest in the business, pay off debts, and provide returns to investors. While the company does not currently have a dividend program, it has announced a $40 million share repurchase program, further enhancing its appeal to investors.

Levered free cash flow (Seeking Alpha)

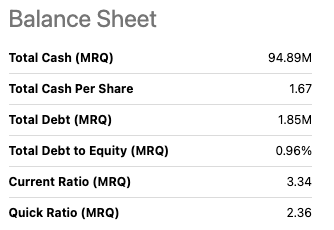

Lastly, Vita Coco maintains a healthy balance sheet, with total cash reserves amounting to $94.89 million. The company’s current ratio of 3.34 and a quick ratio of 2.36 indicate sufficient liquidity, further strengthening its financial position.

Balance sheet overview (Seeking Alpha)

Valuation

Since its debut on the stock market in 2021, Vita Coco has been making its mark in the beverage industry. The company’s value has surged by an impressive 81.04% since its IPO, a testament to its robust business model and strong market presence. The CEO proudly announced that Vita Coco ranks as the 7th best-performing IPO since 2021. Despite outperforming the S&P 500 index over the past year, Vita Coco’s stock is still trading below its average price target of $30.50. This suggests a potential upside for investors looking to capitalise on the company’s growth trajectory. Wall Street analysts seem to agree, giving the stock a 4.33 Buy rating. However, it’s worth noting that the stock has a high short interest of 15%, which could indicate some negative market sentiment.

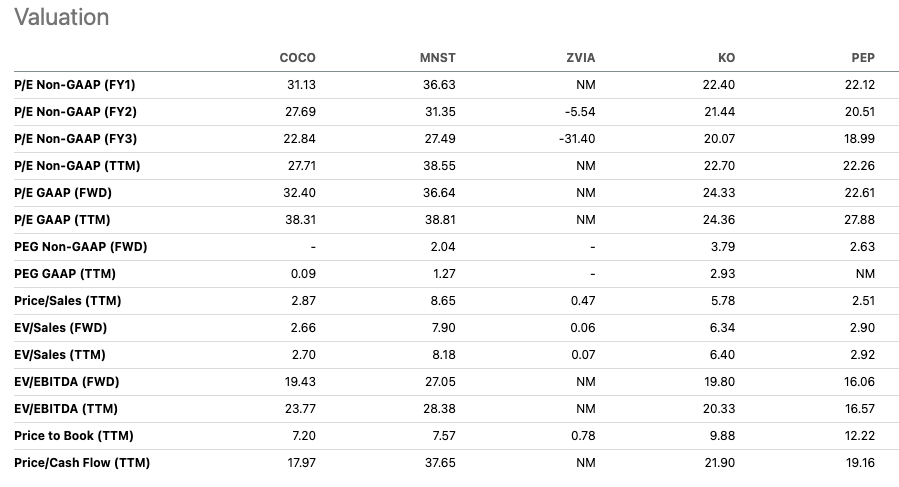

When compared to peers in the market – Monster (MNST), Zevia (ZVIA), The Coca-Cola Company, and PepsiCo – Vita Coco’s price-to-earnings ratio of 31.13 is on the higher side. This is significantly above the consumer staples median of 17.93, which might raise some eyebrows. But here’s where it gets interesting. One of the major attractions of Vita Coco’s stock is its growth rate. The company’s PEG TTM is much lower at 0.09 compared to its peers. This indicates that the stock is potentially undervalued, making it a compelling option for growth-oriented investors.

Relative peer valuation (Seeking Alpha)

Risks

Investing in Vita Coco comes with several risks that investors should consider. The company operates in the highly competitive beverage industry, which is subject to changing consumer preferences and intense competition. Any inability to anticipate or respond to such changes could impact Vita Coco’s market share. Additionally, Vita Coco’s performance is subject to operational risks, including supply chain disruptions and changes in commodity prices. The company’s international operations also expose it to risks related to currency fluctuations and differing regulatory environments. Lastly, the high short interest in Vita Coco’s stock indicates that some investors have a bearish outlook on the company, which could put downward pressure on the stock price. It’s important for potential investors to carefully evaluate these risks and conduct thorough due diligence before investing in Vita Coco.

Final thoughts

In my opinion, Vita Coco presents a compelling investment opportunity. The company’s impressive return since its IPO, consistent track record of beating EPS expectations, and upward revision of its FY 2023 guidance all point to a promising future. Despite operating in a competitive beverage industry, Vita Coco has carved out a niche for itself with its focus on coconut water. The company’s ability to grow faster than the category itself, coupled with its expansion into new product offerings, further strengthens its position. While the high short interest is a point of concern, the company’s strong financial performance and positive cash flow provide a counterbalance. Therefore, investors looking for a growth stock in the beverage industry may want to consider Vita Coco.

Q2 2024 Earnings Call Transcript")