Tamer Soliman/iStock Editorial via Getty Images

Africa Oil Corp. (OTCPK:AOIFF) is a $900 million USD oil corporation. The company has made a number of intelligent decisions, and it’s now part of one of the largest discoveries on the continent. As we’ll see throughout this article the company’s potential farmout transaction, along with other assets, make it a valuable investment.

Africa Oil and TotalEnergies

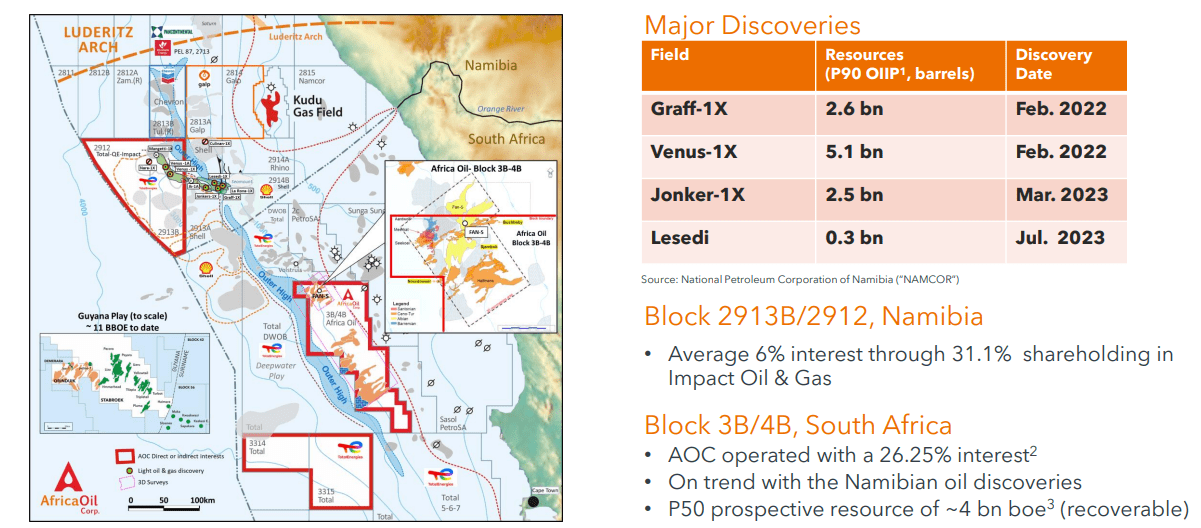

Africa Oil Corp. owns more than 31% of Impact Oil and Gas. Impact Oil and Gas has an interest of just under 10% (post farmout transaction) in the legendary blocks 2912 and 2913B.

Africa Oil Corporation

The Venus-1X well is one of the most legendary wells off the coast of Africa, in 2022, with more than 5 billion barrels of estimated resources. As a result of the farmout transaction, Africa Oil Corp.’s average interest has been cut in half. However, it accelerates the potential of the field to now be developed into something that could produce hundreds of thousands of barrels / day.

That could result in 10+ thousand barrels / day in eventual attributable production for Africa Oil Corp.

Africa Oil Corporation

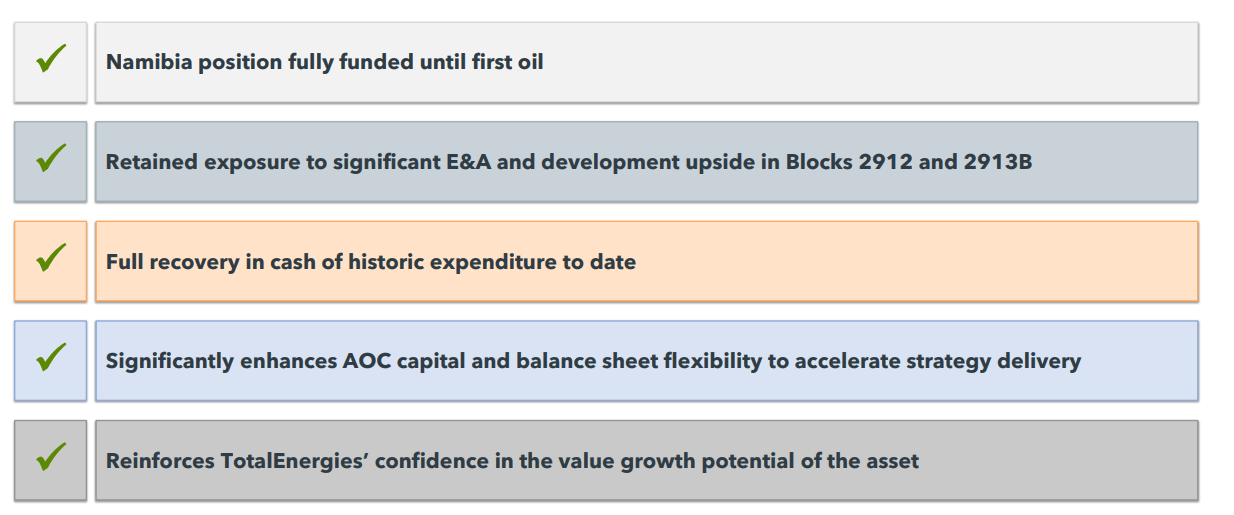

The transaction will result in all capital expenditures being carried by TotalEnergies. All past costs will also be reimbursed, providing Impact Oil and Gas with just under $100 million immediately. The Namibia position is now fully funded until first oil, although the capital obligations which could hit $1 billion, will now be funded from first oil sales.

There are a number of ongoing appraisal and exploration wells through 2024, and we’d like to see the company announce a timeline for the first FPSO deployment. We expect it to come by the end of the decade. This is essential for Africa Oil Corp.’s long-term success and it’s a major catalyst that the company has.

Africa Oil Portfolio

Africa Oil Corp. has an impressive portfolio of assets.

Africa Oil Corporation

The company is working to consolidate and de-risk its portfolio. Its core assets are the offshore drilling assets that it has off the coast of Nigeria, where it continues to have 10s of thousands of barrels / day of production attributable to the company. The company’s Venus assets, especially the follow-on Block 3B/4B assets are core.

The company views it at being at a significant discount to its underlying value and we agree with that. Smaller oil companies tend to face a larger impact from declining oil prices and Africa Oil Corp. is an example of that. We would love to see the company aggressively repurchase shares now.

Africa Oil Corp. Earnings & Repurchases

The company’s production assets along with it solving its debt mean it can now focus on shareholder returns.

Africa Oil Corporation

The company has a dividend of more than 2% and it’s continued to generate strong dividends from Prime Oil and Gas. It finished 2022 with $200 million, and received $125 million in 2023 from Prime Oil & Gas, a strong double-digit yield. The company had $14 million in corporate costs, $79 million in various equity and exploration expenses, and $30 million in shareholder returns.

Some of those investments were one time such as settling Canadian tax obligations and the equity investments in Impact Oil & Gas. As a result, we’d like to see the company spend more in share repurchases in these upcoming years. As the company does so, it can drive higher shareholder returns.

Thesis Risk

The largest risk in our thesis is crude oil prices. The company is incredibly profitable at current oil prices but prices have remained volatile with incredibly strong U.S. production. At the end of the day the company’s existing production is its only asset and earning cash flow from that is the only way for the company to justify its valuation.

The company’s second largest risk is its assets. Not only is the company’s current production from a single asset, which means it faces all the associated risks in terms of replacing it, but the company’s asset is only oil. That means both in the short-term as the company attempts to develop new assets, and in the long-term as oil is replaced as a fuel, the company faces substantial risks.

Conclusion

Africa Oil Corp. is a small cap oil company that has been punished heavily by dropping oil prices. That’s the sad reality of a small cap company. However, that low share price also presents an opportunity for a company that’s focused on repurchasing its shares. The company has the cash flow with current weakness to drive higher returns.

At the same time, the company has a number of impressive catalysts. The recent discoveries in blocks 2912 / 2913B along with the farmout agreement mean that in the coming years the company could have 10s of thousands of barrels / day in attributable production. That combined with additional exploration wells and current cash flow makes the company a long-term investment.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")