SOPA Images/LightRocket via Getty Images![]()

Mortgage REITs are always a favorite of income investors, but the sector struggles under certain market conditions. Double-digit yields have always – and likely will always – attract those looking for “safe” returns, but in my view, mortgage REITs carry elevated risk at the moment. The run off of the bottom that was set in October has been great for the sector, including Annaly Capital Management (NYSE:NLY), but it is my view that the risk of holding Annaly stock now outweighs the potential reward.

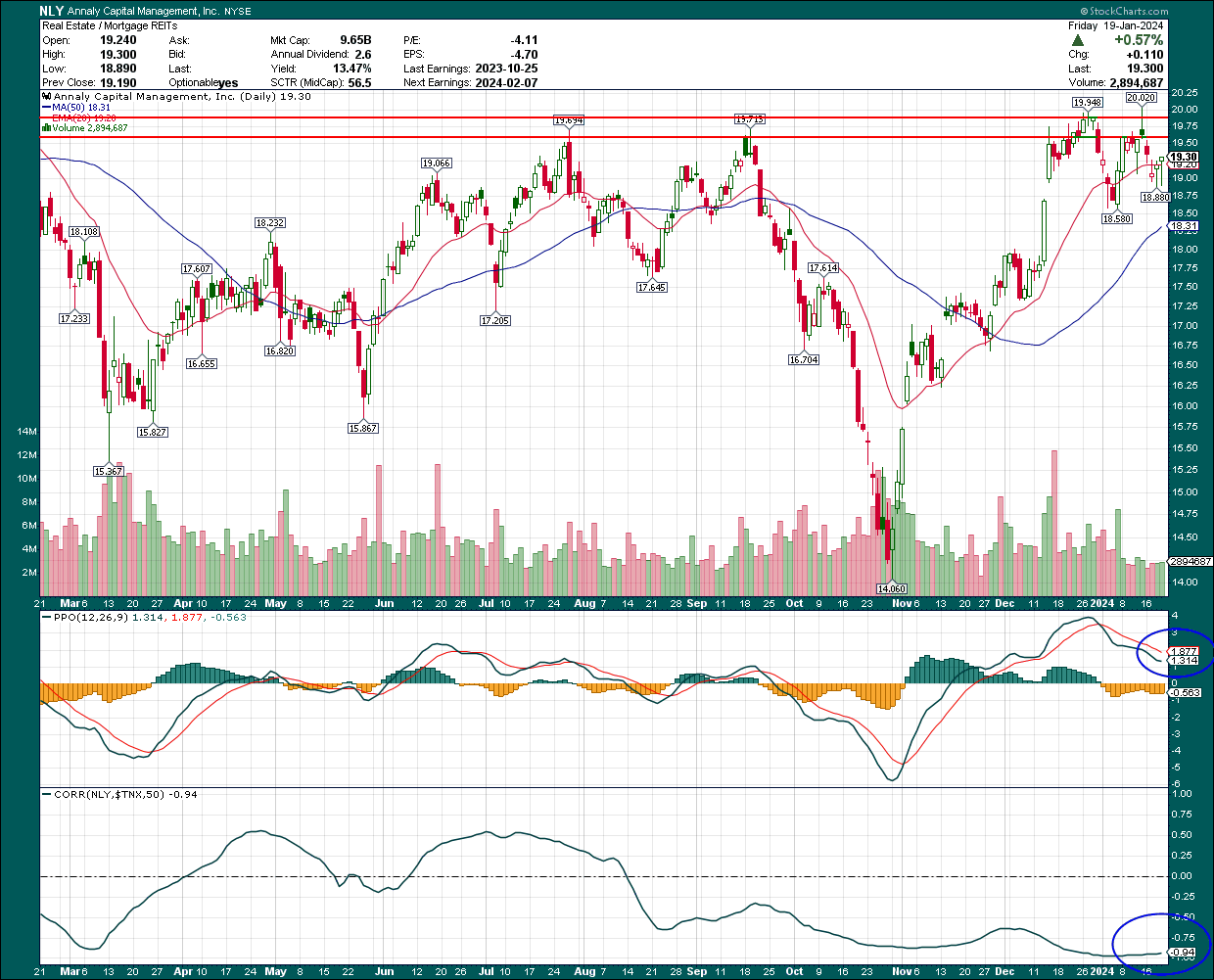

A quick look at the technical picture

Annaly set a spike low in October during what amounted to a mini panic in equities as everything was sold. As we all know, that resulted in a V-recovery and equities are now at or near their highs. We see a similar pattern with Annaly below, but the bulls have become exhausted, according to my read of the below.

StockCharts

The stock briefly broke out in December but that breakout failed, resulting in a second attempt in January. That also failed, and while the bulls have been able to keep the stock from selling off hard, momentum is weakening. Given the inverted hammer from the second attempt, which is a bearish candle, it is my view that the bears are directionally in control right now.

A key factor with mortgage REITs is obviously interest rates, and I’ve plotted Annaly’s 50-day correlation with the 10-year Treasury yield in the bottom panel. It’s at -0.94 right now, meaning that essentially, Annaly’s share price and the 10-year Treasury yield are moving almost perfectly inverse of each other. That makes logical sense given the business model, but it is always best to verify assumptions, rather than just assuming they are true. Indeed, we can see Annaly is sometimes positively correlated to rates as evidenced in much of 2023. For now, however, the relationship is inverse.

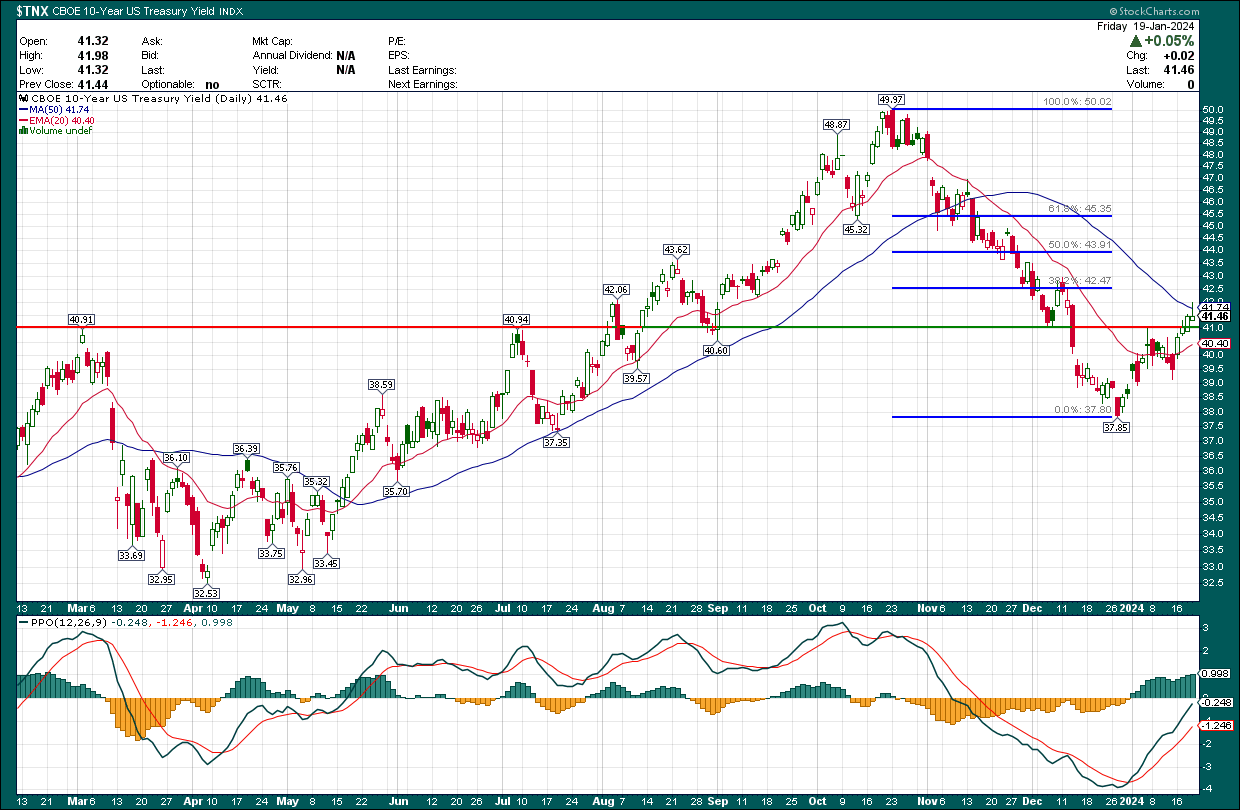

That means the path of the 10-year Treasury is of utmost interest for Annaly holders, and we’ll take a look at that now.

StockCharts

The 10-year yield took a nosedive off of the peak set in October, which uncoincidentally corresponded pretty much exactly to Annaly’s bottom. There’s been a swift retracement, however, as the yield has gone from about 3.75% to 4.15% in a matter of weeks. Key in this move is the fact that yield has taken out what should have been consequential resistance at ~4.10%. That level briefly held in early January but was quickly taken out thereafter, and has held on the past several trading days. Does that mean yields are going to move much higher? Maybe, but right now I’m watching the 50-day moving average at 4.17%, as well as the 38% Fibonacci retracement level of the October to December decline, which is about 4.25%. It is my view we don’t get through both of those levels, but we’ll have to wait and see. Momentum at the moment is extremely strong for this move up in yields and must be respected unless and until it turns. Keep in mind that whatever happens to yield, Annaly is inversely correlated.

Finally, before we move into some fundamental factors, let’s take a look at money flows for mortgage REIT stocks.

StockCharts

We can see here that the sector has underperformed the S&P 500 for most of the past year, meaning that Wall Street is simply choosing to put its money elsewhere. We want to follow the big money because that’s where the outperformance is, and mortgage REITs simply aren’t where to be right now.

Rising rates, funding, and the distribution

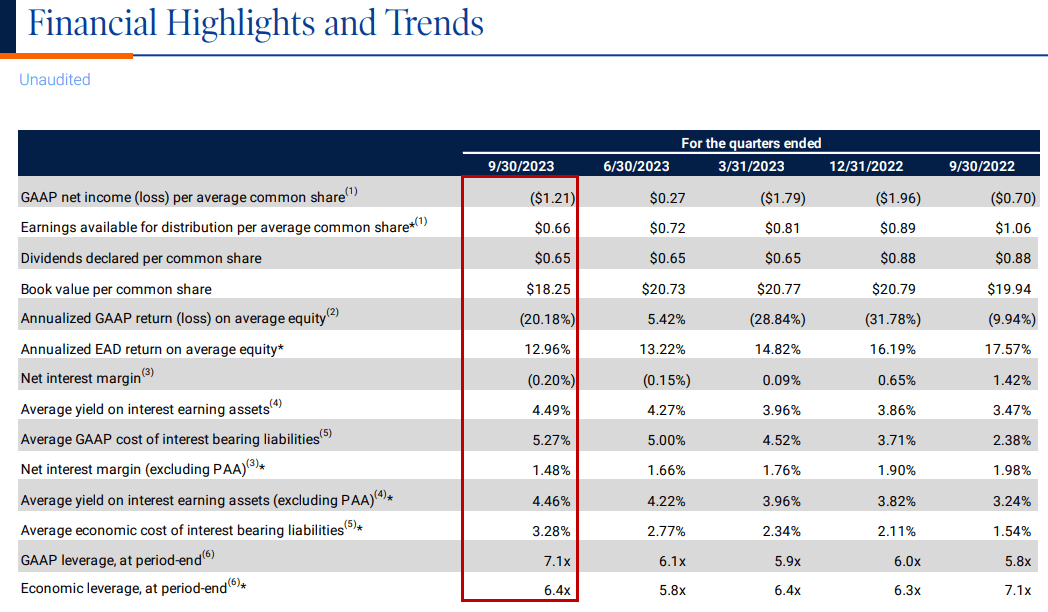

We’re all familiar with Annaly’s model so I won’t explain it here, but in short, the company borrows money and leverages it several times into income-focused securities. That means its ability to select investments at the right time relative to funding costs is really all that matters.

Investor presentation

For the past few quarters, we’ve seen deterioration in the company’s ability to generate earnings available for distribution, as well as net interest margin (adjusted or unadjusted). These things impact its ability to pay a distribution, which is why the distribution is well off of 2022 values at the moment. It’s important to caveat this data with the fact that yields have risen sharply since September 30th, 2023, so we’ll see what Annaly was able to do with that environment in a couple of weeks when it reports Q4 earnings. But to be fair, the period captured in the data above included several months of sharply rising rates, and it clearly didn’t help. I’m skeptical the Q4 report will show much improvement based upon this.

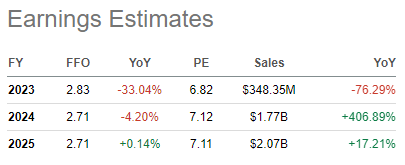

Perhaps that’s why FFO estimates for Annaly are less than stellar moving forward. FFO is not a perfect measurement by any means but it’s certainly good enough to use directionally for Annaly, and I’m not seeing a lot to like here.

Seeking Alpha

It’s clear from these estimates that Annaly is going to struggle to grow its ability to distribute cash to shareholders, and given the valuation (which we’ll get to below), this simply isn’t good enough.

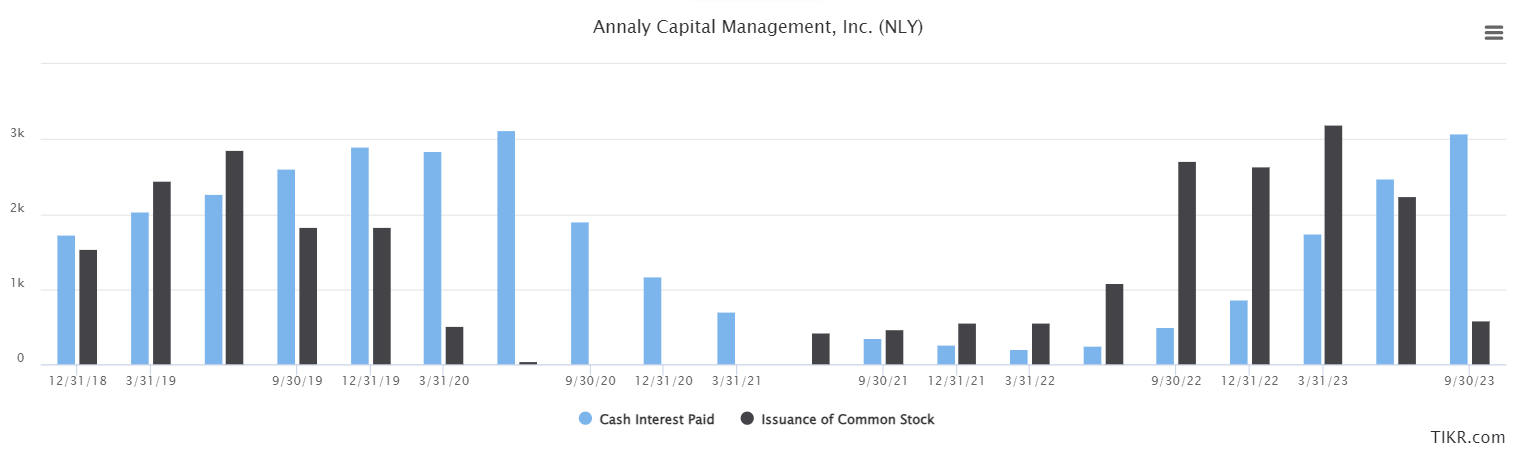

Now, rising rates mean that Annaly’s funding costs rise, and below, we’ll see that its cash interest costs and common share issuances are extremely highly correlated.

TIKR

This is trailing-twelve-months data for the past few years, and we can see that the times when Annaly is forced to pay higher funding costs, the only way it’s been able to do that is to dilute shareholders. The company is extremely highly leveraged through the normal course of business, as that’s literally the entire mortgage REIT business model. That leaves basically no room for flexing the balance sheet when needed like a normal company would, so it dilutes shareholders as really the only course of action.

I don’t know about you, but this is extremely off putting. Dilution not only reduces your stake’s relative size, but it also makes the distribution more expensive. Every time Annaly issues a share, it increases the cash cost of whatever distributions are declared, all else equal. That’s exacerbating a problem that already existed, and that kind of thing is not for me.

Is it at least cheap?

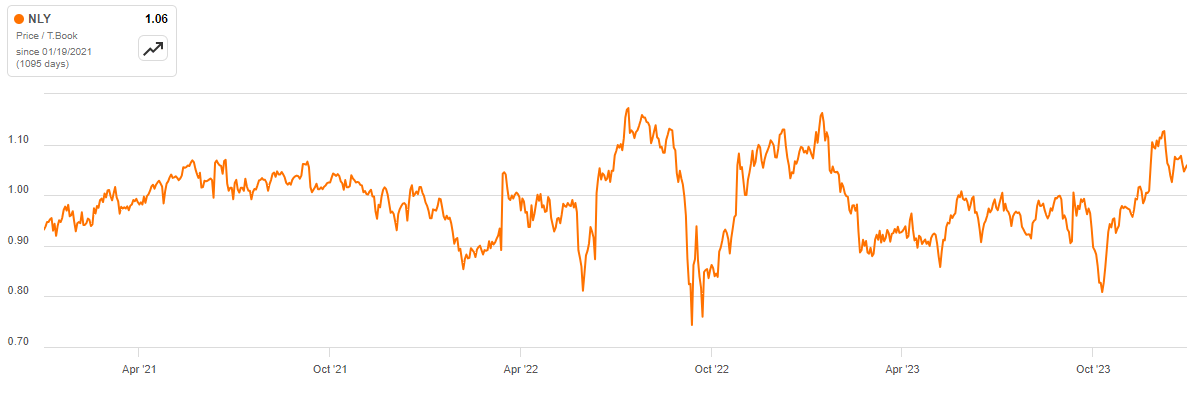

The answer to that question is a resounding ‘no’ as I’ll attempt to show below. Let’s start with price-to-tangible book value.

Seeking Alpha

Shares trade at 1.06X tangible book value today, which is quite clearly elevated by historical standards. That kind of thing would be justified if Annaly were on the cusp of some wave of new earnings growth, but it is my belief there’s plenty of evidence above to suggest that’s not happening, and won’t for the foreseeable future. The stock is just expensive.

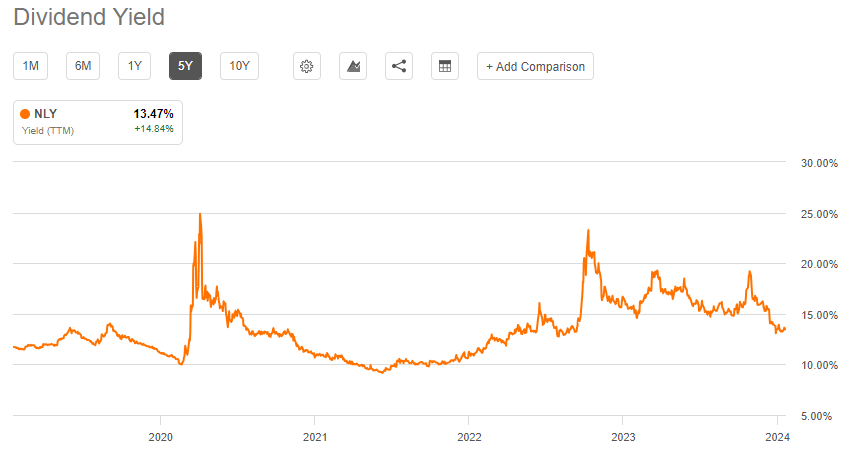

We can also use the dividend yield to value Annaly given it’s a pure income stock.

Seeking Alpha

The yield is much lower than it’s been for the past 18 months or so, but admittedly higher than most of the three years before that. Depending upon your perspective you could make the case it’s expensive (on the past 18 months), cheap (on the period of 2019 to early-2022), or fairly valued (considering all five years). My perspective is to more heavily weight recent years, and on that, the yield is less attractive than it has been since mid-2022. Again, if the company were on the cusp of a wave of new earnings, that would be fine, but it is my view that it isn’t.

If we wrap this up, I see a stock that has little to no likelihood of a path to higher earnings, a dividend that’s already been significantly cut, and valuation metrics that are downright unattractive. I don’t think the stock will breakout above the $20 level based upon the evidence I have, so I’m placing a sell on the stock. I believe the company’s ability to pay its current run rate of distributions around 65 cents quarterly is at risk, and that the stock is expensive. No thanks.

Q2 2024 Earnings Call Transcript")