csfotoimages/iStock Editorial via Getty Images

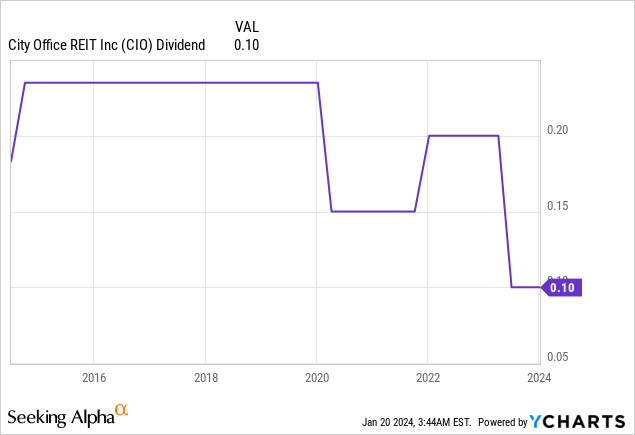

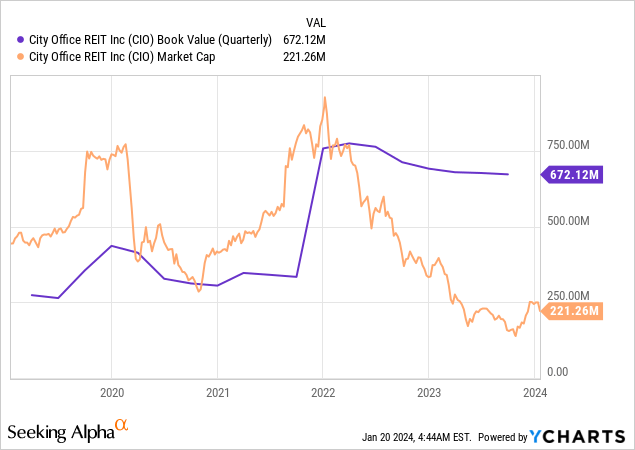

The sustained collapse of equity office REITs since 2022 has likely opened up some opportunities to acquire highly distressed assets with decent underlying fundamentals despite the bleak backdrop posed by the tripartite of high interest rates, work-from-home trends, and the specter of a recession. City Office REIT (NYSE:CIO) is down roughly 70% over this time frame, now trading hands at a 67% discount to a book value of $16.83 per share at the end of its last reported fiscal 2023 third quarter. The internally managed REIT last declared a quarterly cash dividend of $0.10 per share, left unchanged sequentially and $0.40 per share annualized, for a 7.3% forward dividend yield.

However, book value is a somewhat contentious metric for office REITs as it does not capture the deterioration in underlying property fundamentals across the US. The national office vacancy rate reached 18.1% in November 2023, up 190 basis points over its year-ago comp, with the biggest increases seen in West Coast markets, with San Francisco particularly hit hard.

City Office REIT November 2023 Presentation

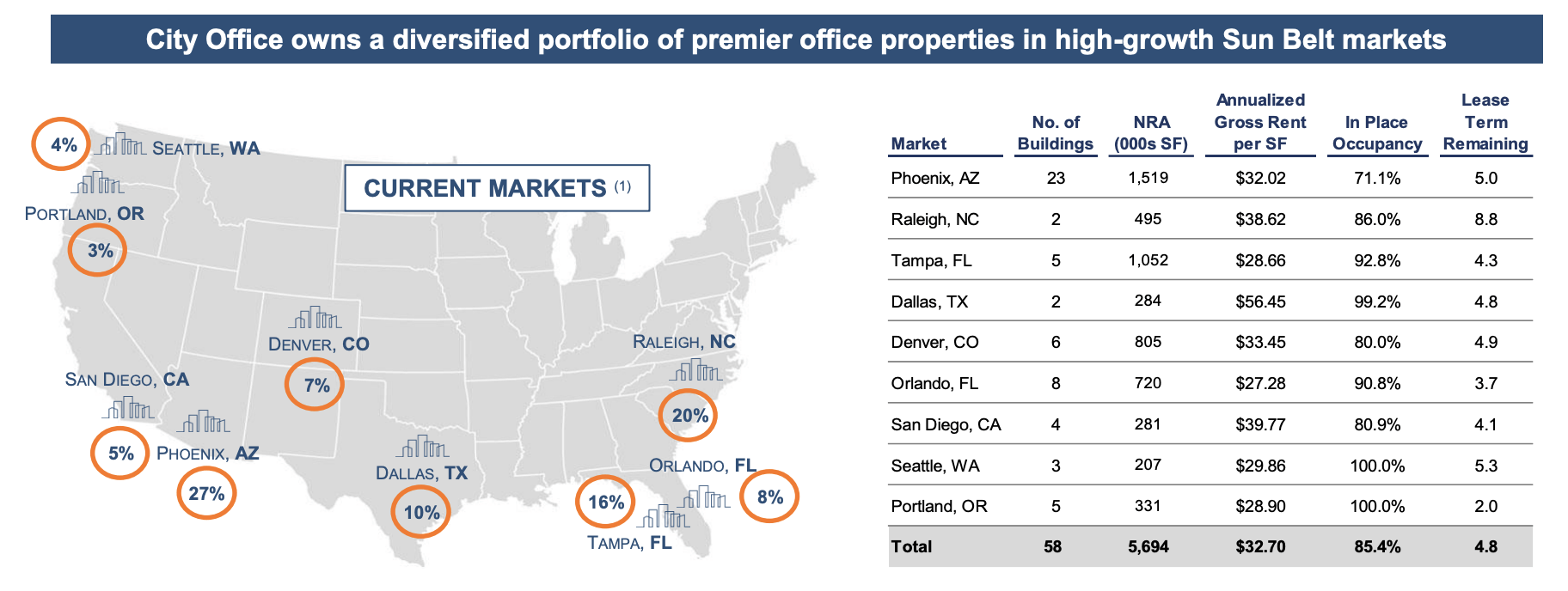

CIO is highly diversified across the US, focusing on the Sun Belt markets, with Florida and Arizona forming its largest markets. The REIT owns or has a controlling interest in 58 properties spread across 5.7 million square feet of office properties in 10 cities at the end of its third quarter. These had an aggregate 85.4% occupancy rate with 4.8 years remaining on average on their leases. The question now is just how much of a value play CIO is with book value likely not a full reflection of the actual market value of its properties.

Revenue, FFO, And Dividend Coverage

CIO generated revenue of $44.2 million during its third quarter, a 2.9% decline over its year-ago comp but a beat of $230,000 on consensus estimates. The dip in revenue was led by occupancy, which fell by 40 basis points despite same-store cash net operating income increasing by 2.2% versus its year-ago quarter. However, operating income at $8.3 million dipped from $9 million in the year-ago period, with net income attributable to common shareholders a loss of $1.9 million.

City Office REIT Fiscal 2023 Third Quarter Form 10-Q

Core FFO for the third quarter came in at $13.7 million, around $0.34 per share, and down 5 cents from core FFO of $0.39 in the year-ago period. The more relevant figure for the dividend is adjusted FFO, which came in at $6.3 million during the quarter. This was $0.15 per share, dipping by 3 cents from the year-ago period. This meant 150% coverage for the dividend or a 67% payout ratio.

City Office REIT November 2023 Presentation

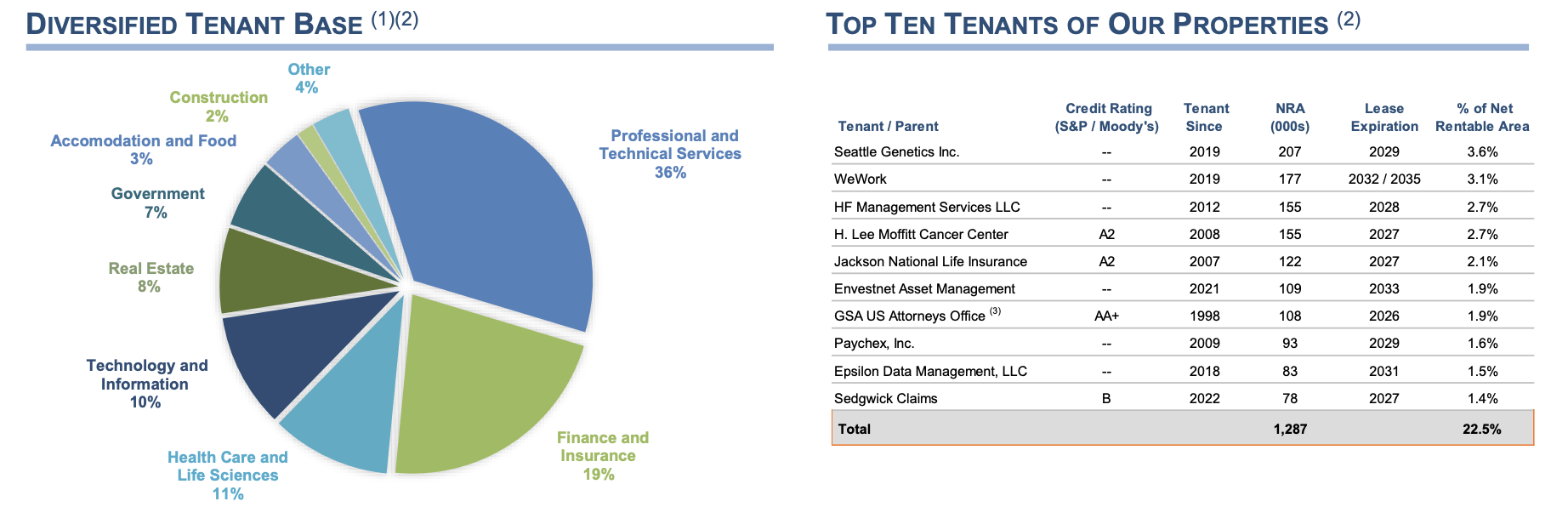

The REIT’s 3.1% exposure to bankrupt co-working space provider WeWork (OTC:WEWKQ) is a liability, with ongoing restructuring efforts likely set to deliver lower rents or a period of elevated vacancy as CIO attempts to lease the space to a new provider. CIO’s weighted average common shares outstanding was also down 5.2% year-over-year due to an ongoing $50 million share buyback program authorized in May 2023.

Leverage, Maturities, And The Fed

City Office REIT November 2023 Presentation

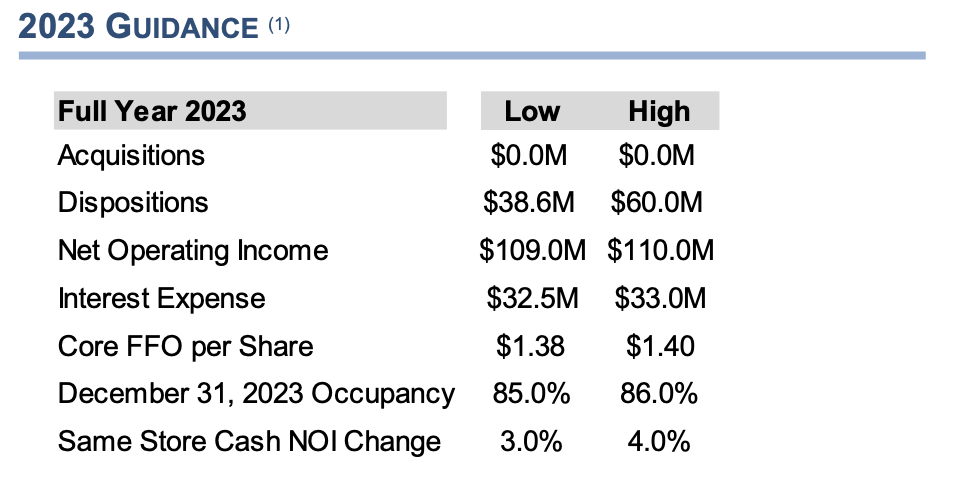

CIO is guiding for core FFO to be $1.38 per share at minimum for its full year 2023, which means it is currently swapping hands for 4x times core FFO. I’d expect AFFO to be lower at around $0.60 per share, which means a higher but still very constrained 9.2x multiple.

City Office REIT November 2023 Presentation

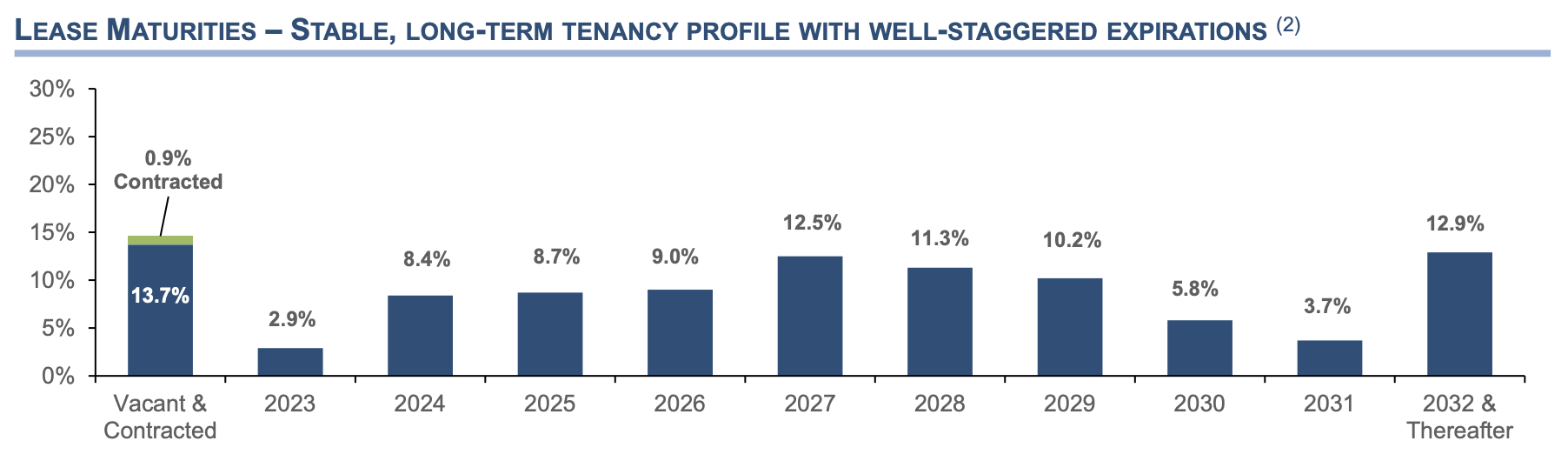

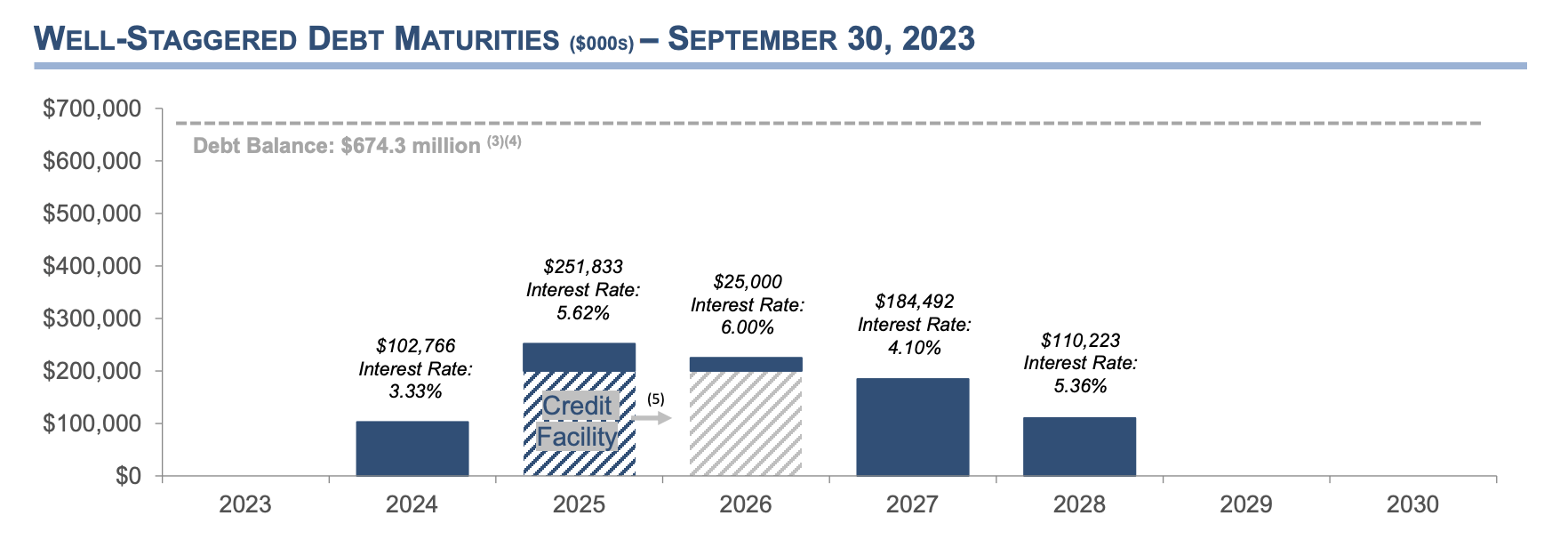

I like the REIT’s well-laddered lease expirations, with just 16.8% of leases expiring by 2025. This gives CIO more time to be able to execute new leases against office property markets that might still in recovery. CIO executed 119,000 square feet of new and renewable leases during the third quarter, with renewal cash rents that were 3.1% higher versus expiring rents. However, debt maturities are quite front-loaded, with $102.8 million coming due in 2024 and another $251.8 million coming due in 2025. This is against cash and equivalents of $36.7 million at the end of the third quarter.

City Office REIT November 2023 Presentation

Hence, further asset disposals will likely be necessary despite the $330 million of completely unencumbered properties that CIO can attach mortgage debt to. I have not been buying any common shares of purely office-focused equity REITs as the industry is still going through a reset to a new normal. However, I’ve been buying relevant distressed preferreds or bonds. CIO’s 6.625% Series A Preferreds (NYSE:CIO.PR.A) currently offer a 9% yield on cost and are trading around $6.68 below their $25 per share liquidation value. The Fed will be instrumental to value creation for both securities this year, as nearly 150 basis points worth of cuts through 2024 remains the base case according to the CME FedWatch Tool. Both of these securities are rated as a hold.

Q2 2024 Earnings Call Transcript")