Bloomberg/Bloomberg via Getty Images

This article was co-produced with Chuck Walston.

Although I characterize myself as a largely buy-and-hold investor, I’ll admit I kicked CVS Health Corporation (NYSE:CVS) stock to the curb when the company froze its dividend. I did this even though I understood the logic behind management’s decision.

Back in 2017, CVS made a bold move to acquire Aetna, a health insurance company, for $77 billion, including debt assumption. That acquisition caused CVS’s leverage ratios to spike. Obviously, it was a prudent choice to freeze the dividend.

The merger with Aetna was but one giant step in the company’s transition away from a simple pharmacy and into a customer-centric health company.

With the acquisitions of pharmacy benefit manager Caremark in 2007, Aetna in 2018, and last year’s deal to acquire healthcare service providers Signify and Oak Street, management has now transformed the company into a leader in the healthcare services industry.

Even so, shares of CVS have not fared well of late. The stock is down 13% over the last twelve months. A decrease in COVID-19 vaccination rates, coupled with a recent revision of its full-year EPS guidance, are two of the headwinds that buffeted the stock.

Nonetheless, last quarter’s results and management’s guidance show CVS should notch reasonable growth for the foreseeable future.

Add to that revived dividend growth, hefty share buybacks, and an enticing valuation, and CVS may present a solid investment opportunity.

A Look At Recent Results

CVS reported Q3 2023 results on the first of November.

The company provided a double beat for investors, with non-GAAP EPS of $2.21, up from $2.17 in the comparable quarter, and $0.08 above consensus.

Revenue of $89.8 billion climbed 10.6% year over year to beat analysts’ estimates by $1.63 billion.

Adjusted operating income rose 10.8% to $1.88 billion, and health services revenue increased 8.4% to $46.9 million.

Although revenue in the company’s healthcare benefits business surged 16.9% to $26.3 billion, adjusted operating income for that segment fell 6.4% to $1.54 billion.

The pharmacy and consumer wellness segment recorded 6% revenue growth to $28.87, but also saw adjusted operating income decline slightly to $1.39 billion.

Management provided revised guidance for FY 2023. The forecast for GAAP earnings is in a range of $6.37 to $6.61, down from the prior range of $6.53 to $6.75.

However, the company reiterated the previous guidance for adjusted earnings per share in the range of $8.50 to $8.70, and for cash flow from operations of $12.5 billion to $13.5 billion.

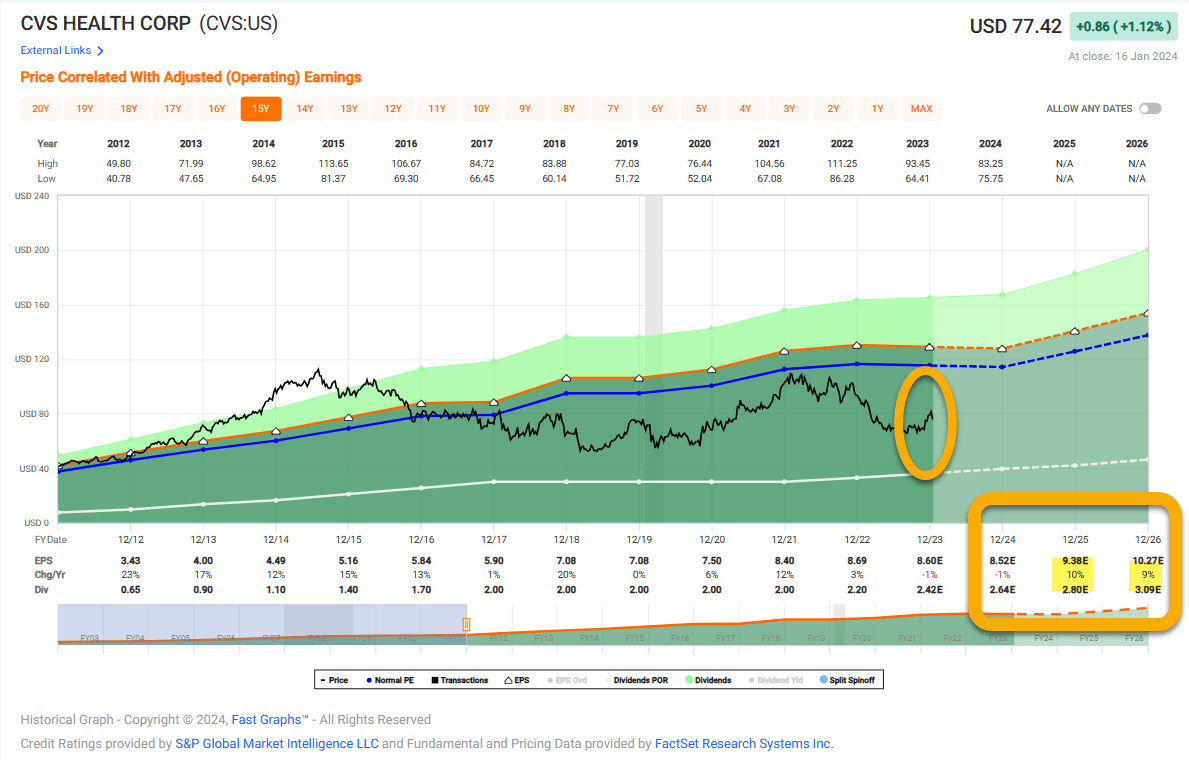

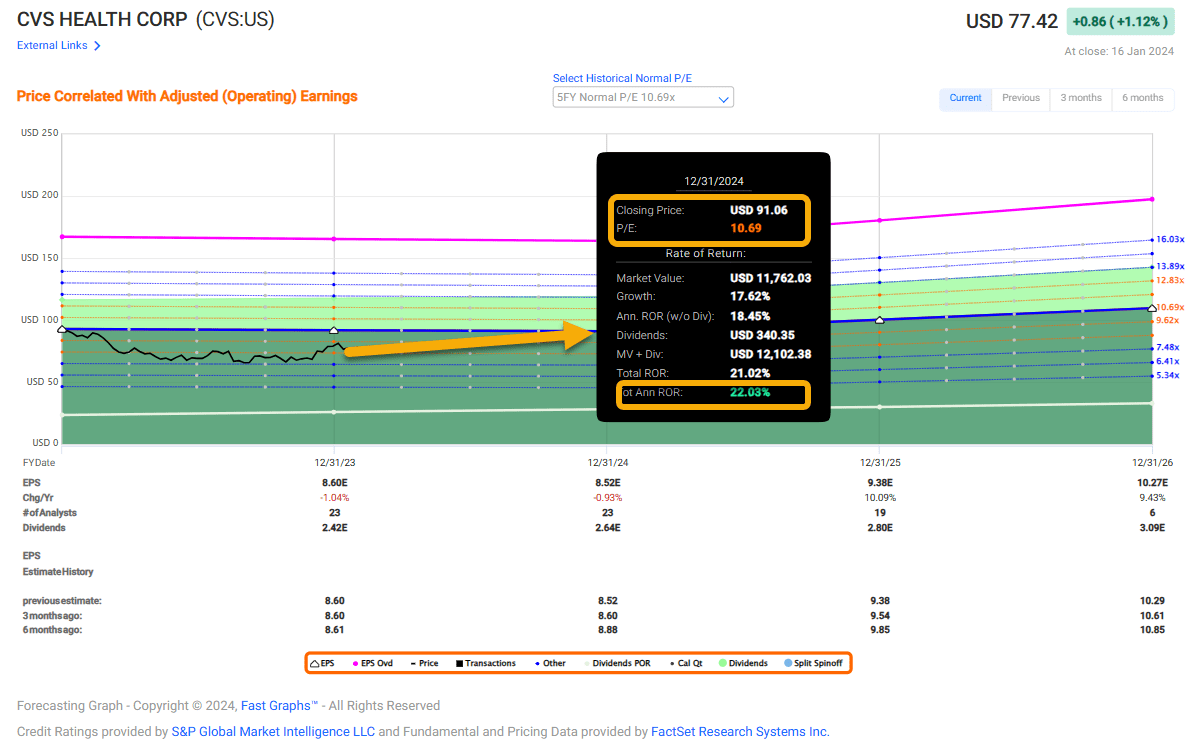

CVS

Management also expects cash flow near the upper end of that guidance range.

CVS pointed to costs related to recent acquisitions for the reduced guidance.

Recent Developments

Early last month, CVS introduced CostVantage, a simpler, cost-based drug pricing program. Expected to roll out this year, CostVantage is designed to overhaul how the company prices prescriptions. The goal is to provide greater transparency while at times lowering drug prices.

The cost of medications are largely determined by pharmacy benefit managers (PBMs). PBMs negotiate discounts between drug manufacturers and insurers. However, with the CostVantage Plan, customers will pay the drug manufacturer’s list price plus a markup and dispensing fee.

CostVantage will also provide customers with information regarding prescription drug costs and their insurer’s portion of the total cost.

In 2023, CVS closed multibillion-dollar deals to acquire home health services providers Signify and Oak Street Health, businesses that focus on primary care for seniors.

The $8 billion deal brings Signify’s network of over 10,000 clinicians across the U.S. to CVS. On average, these clinicians spend 2.5 times more time with patients during home visits than an average visit with a primary care provider.

Signify estimated it conducted nearly 2.5 million patient contacts through in-person and virtual visits in 2022.

Management guides for over $500 million in synergies to be realized from the merger.

The deal for Oak Street Health, for about $9.5 billion-plus the assumption of Oak Street’s debt, was CVS’ third-largest acquisition in the last decade. Oak Street operates over 160 primary care centers that offer routine health screenings and diagnoses for older adults.

However, while CVS is expanding its home health services business, it is pulling back on its brick-and-mortar presence. A week ago, a company spokesperson revealed a plan to close some pharmacies that operate in Target Corporation (TGT) stores.

CVS runs pharmacies in roughly 1,800 of Target’s 1,956 stores in the US. The number of stores that will be shuttered was not disclosed, but a Wall Street Journal piece claimed the company plans to close “dozens” of locations.

Back in 2021, management disclosed a plan to close roughly 900 locations, approximately 10% of its stores, between 2022 and 2024. Since then, CVS has closed about 600 stores, with the remaining 300 expected to close this year.

The Target closures will begin in February and run through the end of April.

Last fall, CVS announced it would work with drug manufacturers to commercialize and co-produce biosimilars.

Through a wholly owned subsidiary named Cordavis, CVS aims to develop biosimilars to spur competition and lower drug prices.

Out of the gate, Cordavis is partnering with Sandoz Group AG (OTC:SDZNY) to market a private-label version of Hyrimoz.

Set to launch in the first quarter of 2024, Cordavis will list the Hyrimoz biosimilar, at a price that is 80% lower than the current list price of $6,922 for a four-week supply.

Debt, Dividend, And Valuation

The company’s credit is rated BBB. CVS ended the third quarter with $16.1 billion in cash and short-term investments.

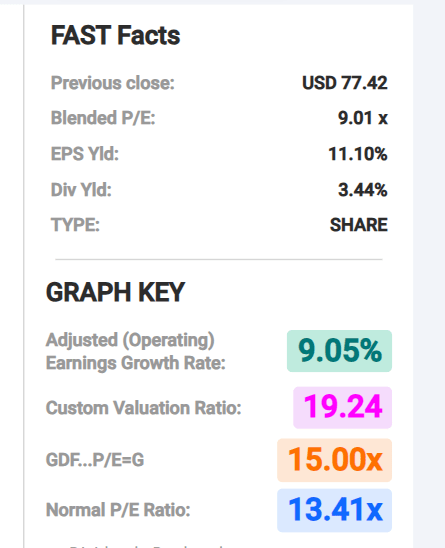

The current yield is 3.44%.

CVS raised the dividend by roughly 10% in each of the last three years. With a payout ratio of 27.47%, the dividend is safe and the company has substantial room to raise the payout at a low double-digit pace for the foreseeable future.

The current forward P/E of 9.00x is only marginally lower than the 5-year average P/E for CVS of 9.63x. Even so, that metric is well below the sector median P/E of 18.45x.

The stock has a 5-year PEG of 0.35x, indicating it may be significantly undervalued.

CVS currently trades for $77.30 per share. The average 12-month price target of the 27 analysts that follow the stock is $90.79 per share.

The company repurchased $3.5 billion of shares in 2022 and $2 billion in the first quarter of 2023. CVS has not repurchased shares over the last two quarters. The company’s market cap is just below $100 billion.

CVS only owns a mid-single digit percentage of its stores.

FAST Graphs

Is CVS A Buy, Sell, Or Hold?

CVS is a company that appears to be in an unending metamorphosis.

However, unlike the “diworsification” that so often plagues many firms, CVS’s large-scale acquisitions are evolving the company to meet the changing environment.

Furthermore, demand for medical care will be fueled for years to come by the aging demographics in the US. CVS forecasts adjusted EPS growth over the long term of 6% or greater.

CVS

The pause in dividend growth that led me to shed the shares years ago is over. CVS now pays a fairly hefty yield that is growing at a strong pace and appears to have room to run.

And last but far from least, the stock is trading for a valuation that provides a solid margin of safety.

With all of this in mind, I rate CVS as a Buy.

FAST Graphs

During my due diligence investigation, I initiated a small position in CVS. I hope to add to that investment significantly in the coming weeks, as funds become available.

FAST Graphs

Author’s note: Brad Thomas is a Wall Street writer, which means he’s not always right with his predictions or recommendations. Since that also applies to his grammar, please excuse any typos you may find. Also, this article is free: written and distributed only to assist in research while providing a forum for second-level thinking.

Q2 2024 Earnings Call Transcript")