jasonbennee

Overview

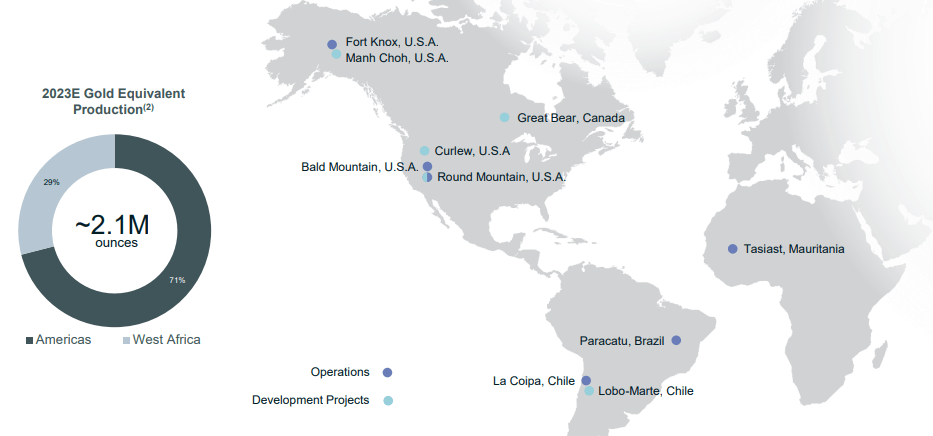

Kinross Gold (NYSE:KGC) is a relatively large gold mining company that I have covered a few times over the last few years. Those articles can be found here. The company is expected to produce about 2.1Moz of gold equivalent in both 2023 and 2024, where most of its production is in North and South America, even if a substantial percentage of production and cash flows comes from its low-cost Tasiast mine in Mauritania.

Figure 1 – Source: Kinross January 2024 Corporate Presentation

In this article, I will review the recent operating performance and compare the company with a few industry peers, where I decided to compare Kinross with Barrick Gold (GOLD), Newmont (NEM), Agnico Eagle (AEM), and Alamos Gold (AGI).

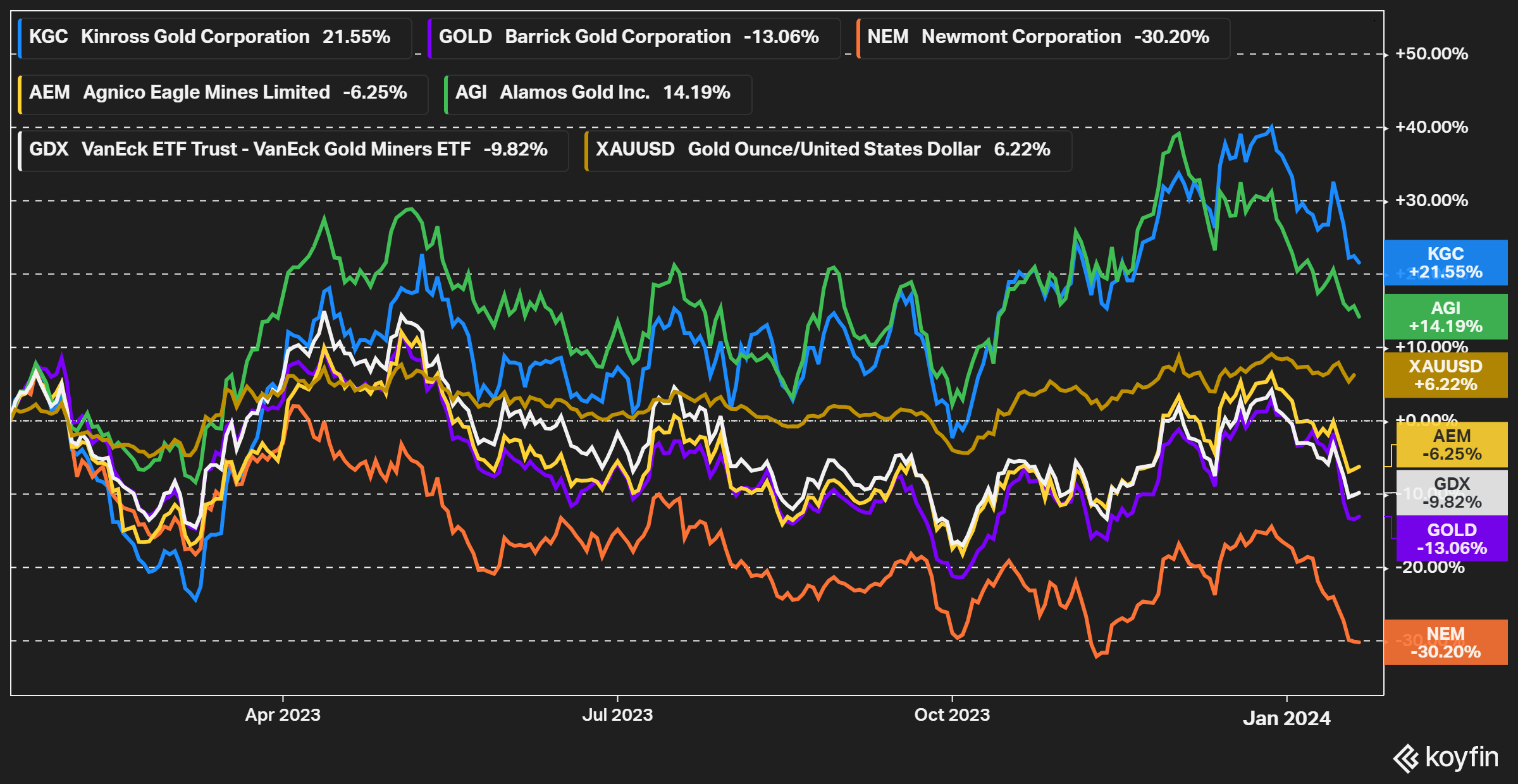

We can in the chart below see that the stock price performance for Kinross has been relatively good over the last year, at least on a relative basis. Kinross is up 22%, the stock has outperformed the peers and the VanEck Gold Miners ETF (GDX). The outperformance is likely due to a good operating performance which has led to very solid cash flows.

Figure 2 – Source: Koyfin

Operations

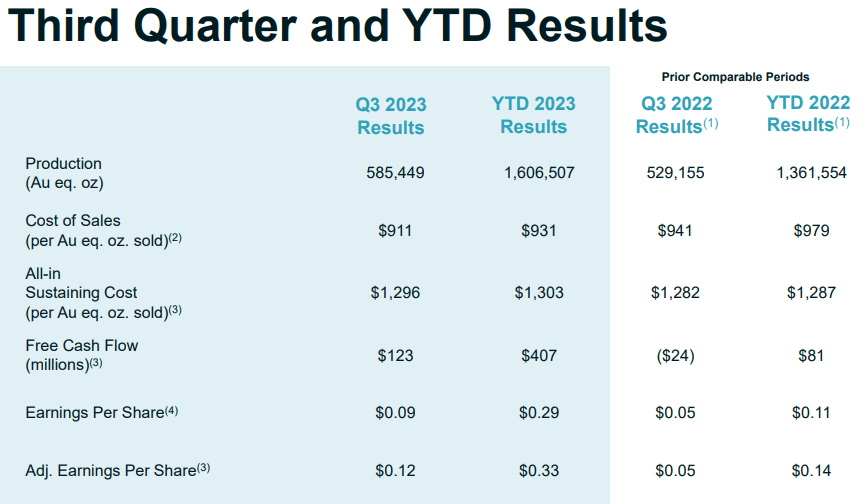

Kinross has during the first three quarters of 2023 shown substantial improvements compared to last year. The company has produced 1,607Koz of gold equivalent compared to $1,362Koz last year. Consolidated cash cost has decreased to $931/oz from $979/oz in 2022, while All-In Sustaining Cost (“AISC”) has increased slightly to $1,303/oz in 2023 from $1,287/oz in 2022.

The substantial increase in production, relatively flat costs, and a higher gold price in 2023 have led to a large increase in EPS to $0.29 in the first three quarters of 2023 compared to $0.11 in 2022. Free cash flow was a very impressive $407M compared to $81M the prior year.

Figure 3 – Source: Kinross Q3-2023 Corporate Presentation

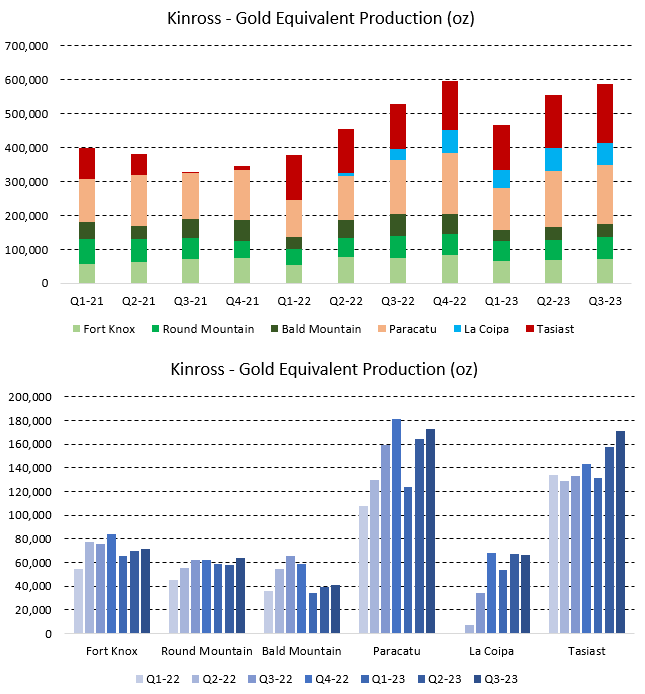

The large year-over-year production increase in 2023 has come from the company’s three lower-cost operations Paracatu in Brazil, La Coipa in Chile, and Tasiast in Mauritania. The three remaining assets in the U.S. have seen production decline slightly in 2023 compared to 2022.

The increase at La Coipa is most noticeable as the ramp-up of production has been very successful over the last two years and the mine is on track to meet the 2023 production guidance of 240Koz of gold.

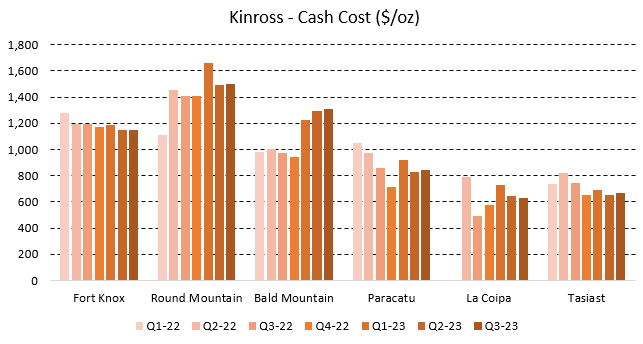

Figure 4 – Source: Kinross Quarterly Reports

Cash cost for the U.S. operations have increased slightly in 2023, cash cost has roughly been flat at La Coipa, while we have seen a very encouraging declining trend at the two largest mines of Kinross, Paracatu & Tasiast.

Figure 5 – Source: Kinross Quarterly Reports

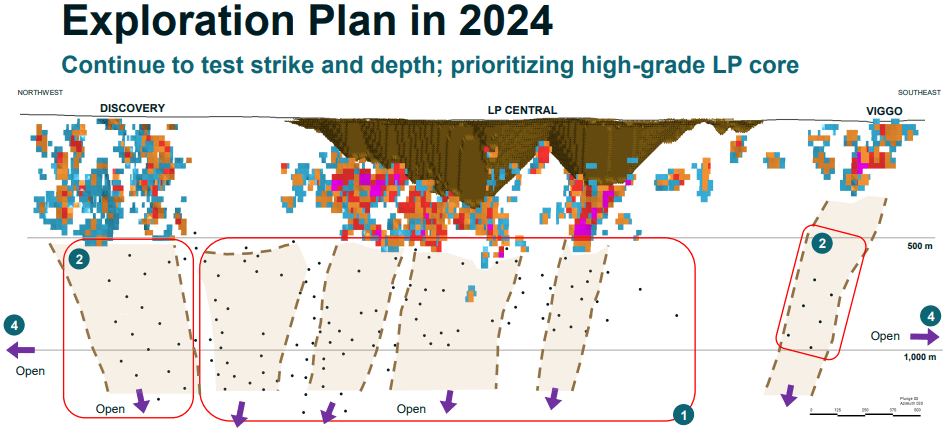

There is no doubt the development project Great Bear is an important part of Kinross as well, the most recent resource update showed 5Moz of gold resources, with slightly more than half of that in the indicated category, while the rest of the resources are in the inferred category. Most expect this asset will continue to grow over time and has the potential to be a massive contributor to production and cash flows, even if it is at least 5 years from production at this point.

Figure 6 – Source: Kinross January 2024 Corporate Presentation

Peer Comparison

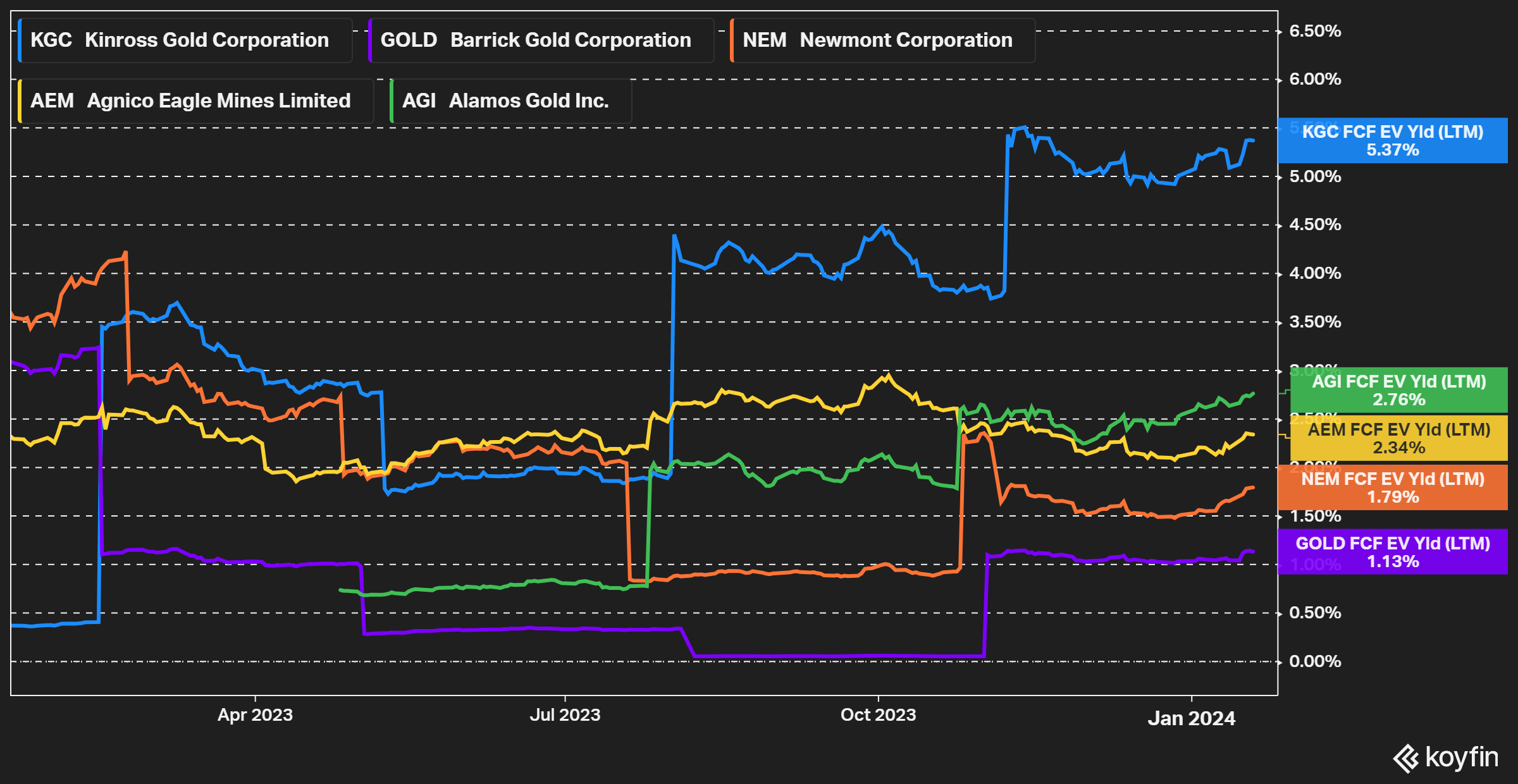

The reason Kinross has outperformed many of its peers over the last year comes down to strong cash flows, where we can see the superior free cash flow yield based on historical data in the chart below.

Figure 7 – Source: Koyfin

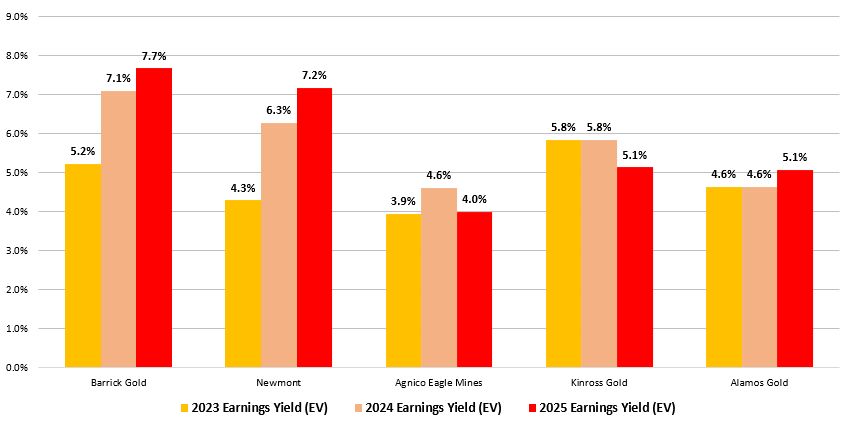

However, when it comes to estimates for 2024 & 2025, there doesn’t appear to be the same valuation discrepancy between the companies, as illustrated in the chart below. Note that I have relied on the earnings yield, where the enterprise value is used to account for the debt, but earnings are used instead of free cash flow, because fewer brokers typically provide free cash flow estimates compared to earnings estimates, making the earnings estimates more reliable.

Figure 8 – Source: Data from Koyfin

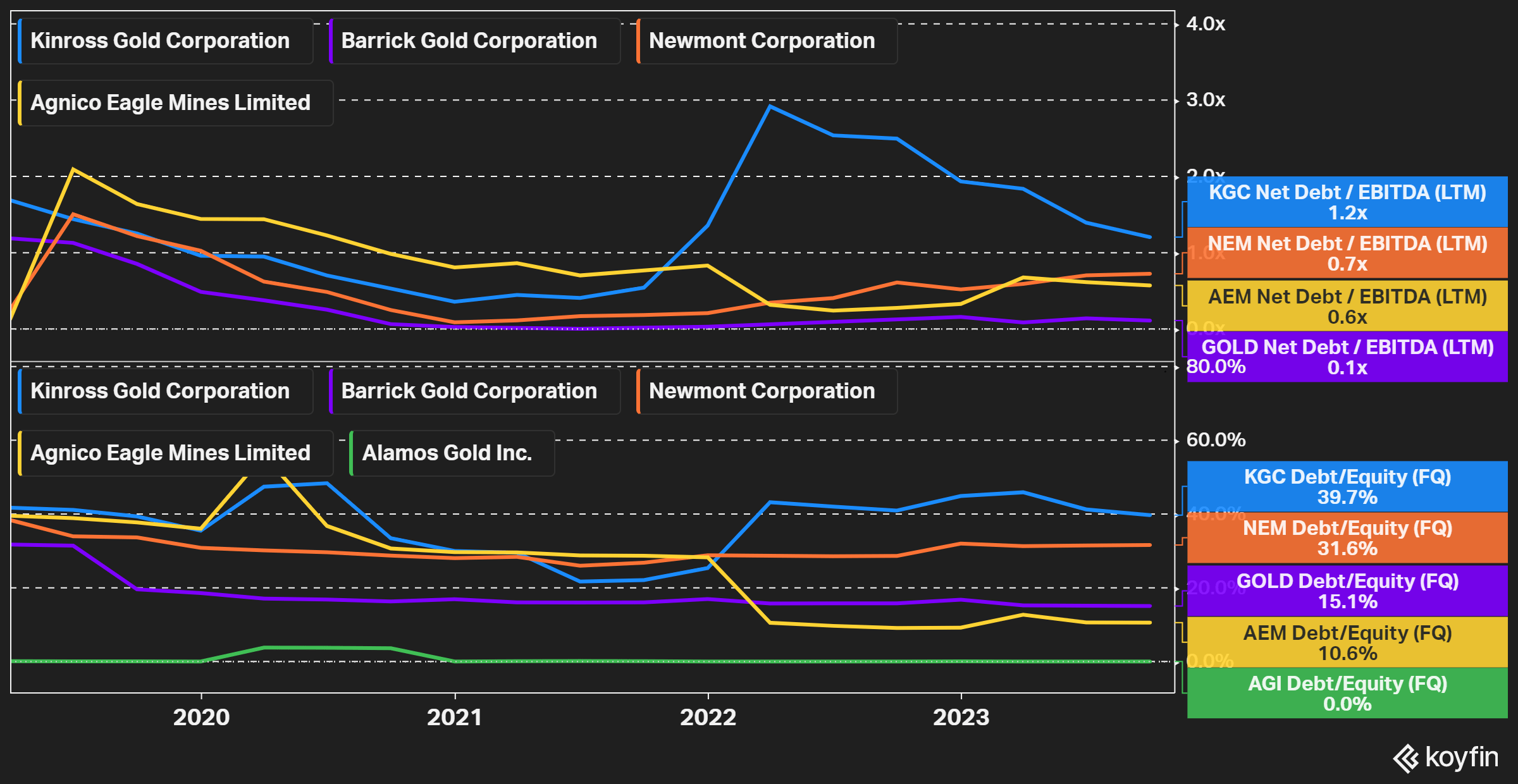

We can also see that Kinross still has a decent amount of debt on the books, while most of the peers have chosen to deleverage more over the last few years. Based on recent performance, which looks to have been a good choice by Kinross, but the higher debt level does increase the risk as well.

Figure 9 – Source: Koyfin

Conclusion

Kinross has delivered strong operating performance over the last year, which has translated to a very good cash flow yield. The successful ramp-up of La Coipa has offered a nice tailwind for the stock.

In the second half of 2024, we can expect a preliminary economic assessment on Great Bear, first production from Manh Choh in Alaska, and some exploration drilling. So, the company has some interesting catalysts in the coming year as well.

The stock is relatively cheap compared to its history, even if that is true for most precious metals miners today. However, I am more neutral on Kinross because the valuation for 2024 & 2025 is more in line with peers, the company has a higher financial leverage than many of its peers, and because Great Bear is many years from production, which makes it doubtful the market will start to price in positive developments from that project.

Q2 2024 Earnings Call Transcript")