FABRICE COFFRINI/AFP via Getty Images

Background

We last covered Philip Morris (NYSE:PM) in July of 2023–you can read the article by clicking here. At the time, we were bullish on the prospects of the long-downtrodden tobacco company as it seeks to diversify its offerings and move towards a ‘smoke-free future.’

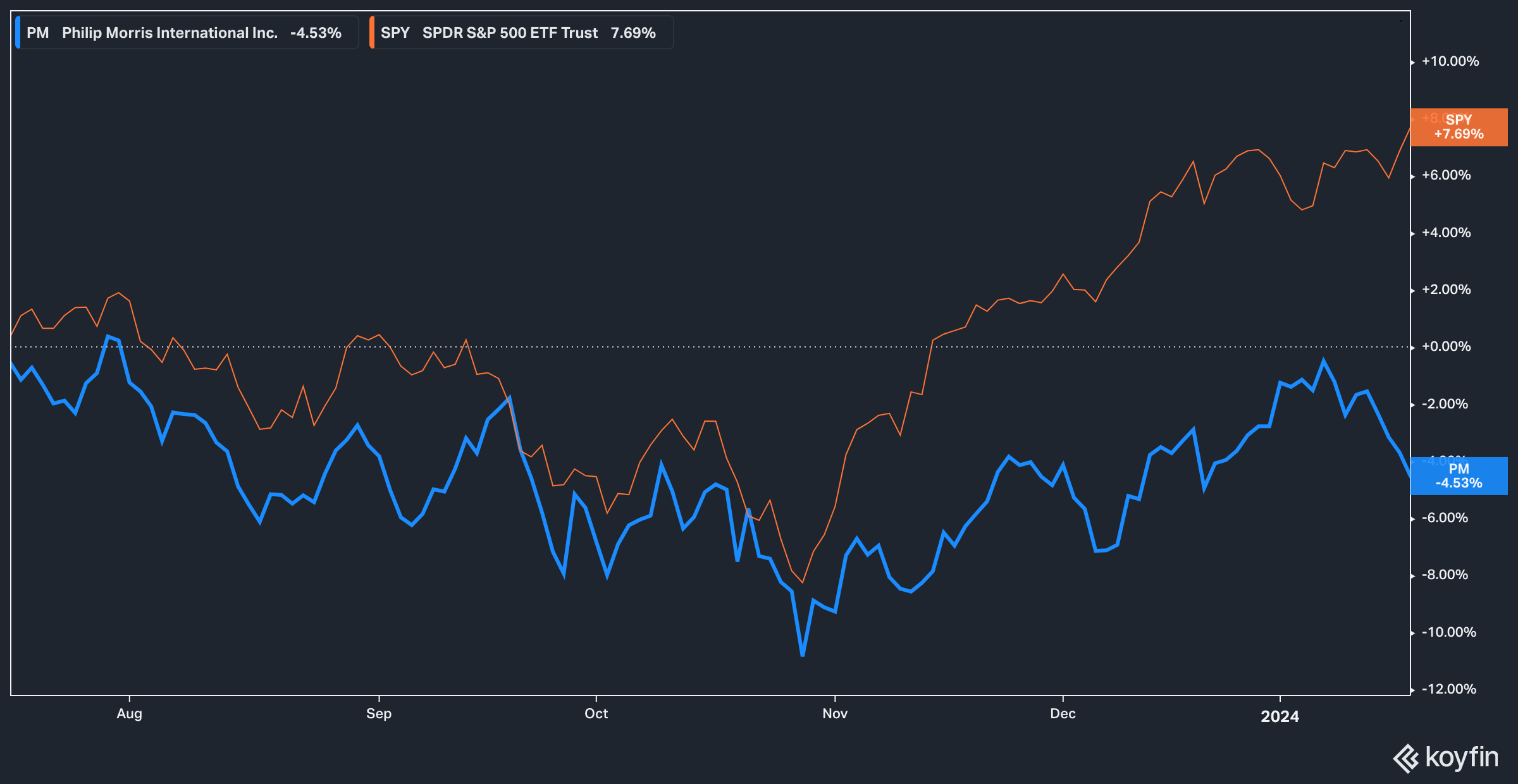

Since article, the stock has largely traded sideways, underperforming the market by a fairly wide margin.

Koyfin

In the last half-year, Philip Morris has delivered negative 4.5% on a total return basis, quite a gap from the 7.7% returned by the broader S&P 500 (SPY). For context, the price return (which excludes dividends) for the time frame clocked in at negative 7%.

Given the time that has passed (and an upcoming February 9th annual earnings report), we want to revisit Philip Morris and see if the narrative is still intact, and if there is still a chance for this stock to outperform in the future. Let’s dive in!

The Narratives

Saying that cigarettes are becoming more unpopular is not a controversial statement. Philip Morris acknowledges as much, and the numbers bear it out. What is becoming more popular, however, are the company’s Heated Tobacco Units (HTUs, which are different from e-cigarette or vaping devices) and Nicotine Pouches (sold under the ZYN brand).

Sales Volumes (Company Filings)

As can be seen above, cigarette sales declined by 1.3% in the first nine months of the fiscal year, while HTU’s sales surged by 18% from 77 billion units in 2022 to 91 billion in the same period for 2023.

Sales Volumes (non-cigarette or HTU) (Company Filings)

The big question for investors, however, Is whether or not the adoption of oral nicotine products (particularly ZYN nicotine pouches and Snus) will continue to grow at current levels or whether a ceiling is being reached. To date, the numbers have been outstanding. In Q3 2023 the company posted smoke-free net product revenues of $3.3 billion–a 35% increase year over year.

Dampening this success story, however, is the ban on flavored HTUs that went into effect in late November 2023, and is expected to be a headwind for the company in the fourth quarter and beyond.

An additional, but short-duration, headwind for the stock in the fourth quarter is likely to be a surge in device sales which have a lower margin profile than the cartridges and tobacco units that go into them. CFO Emmanuel Babeau addressed this in the Q3 call:

[T]here are going to be some mix impact in Q4 and notably on the devices as we are rolling out ILUMA in a significant number of new markets. We are also launching some new innovation in some markets on the ILUMA device. That’s going to generate, I would say, significantly accelerated activity on our device sales, and that is having a negative impact on the margin. So that’s going to be clearly one element. Then on top of that, there will be certainly some investment during the fourth quarter, and that is having an impact on the margin.

With these headwinds, it’s perhaps not surprising that the stock has underperformed. We point out, however, that these headwinds are largely temporary, especially when one considers the fact that the company in October filed to sell its latest HTU iteration–the IQOS Iluma–in the United States.

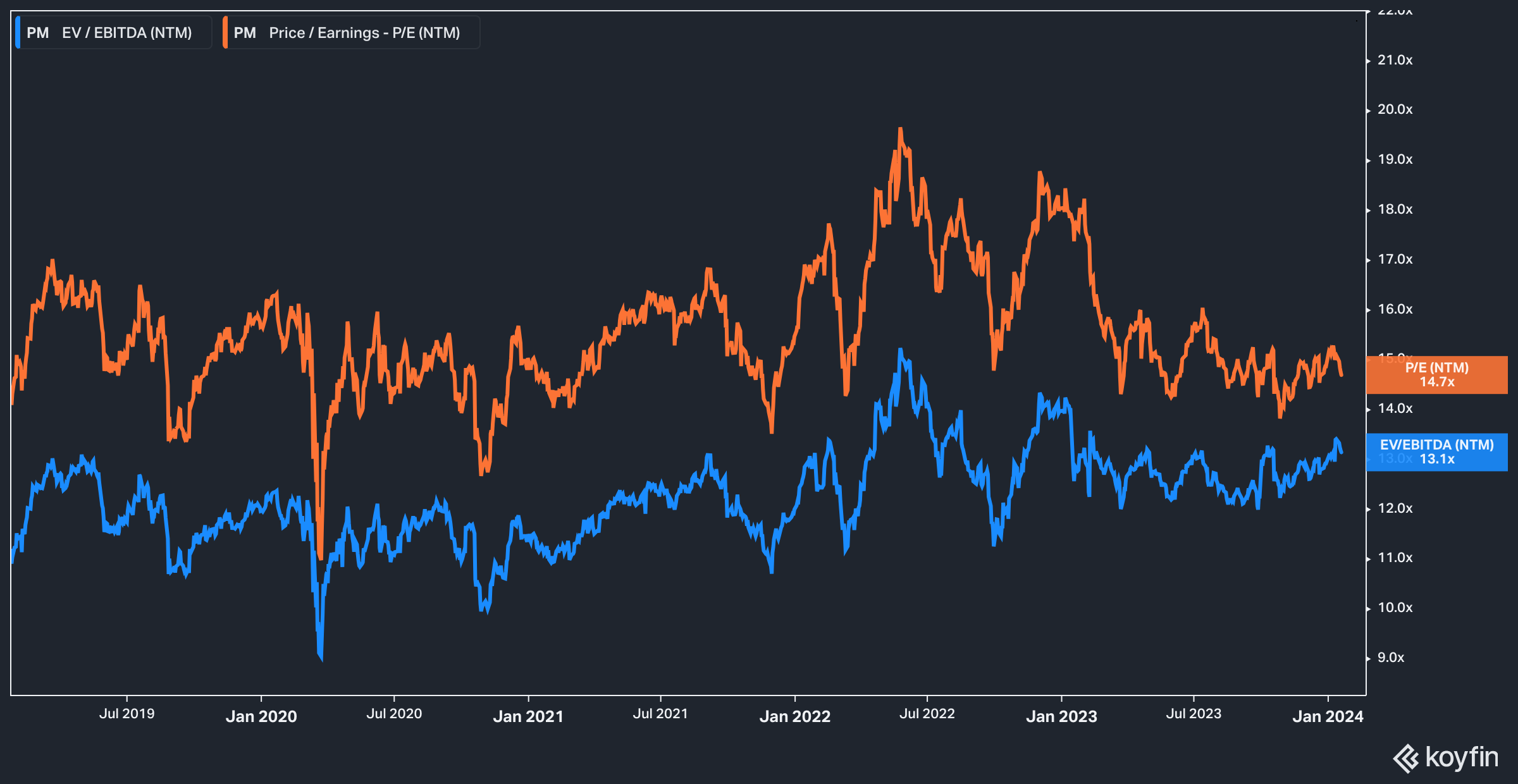

Valuation & Expectations

At the time of our last writing on Philip Morris, the stock traded at almost 16x forward earnings estimates. Today, the stock trades hands for 14.7x forward earnings.

PM Forward Valuations (Koyfin)

We think that the current levels–the lower quartile of the five-year range for forward P/E–present an interesting opportunity for investors not currently in Philip Morris.

For their part, analysts are also positive on the outlook of the stock from here on out. As of this writing, 5 of the 18 analysts who cover Philip Morris rate it a Strong Buy while 10 rate it a Buy. The average price target for the stock is currently $109; 18% above the today’s price.

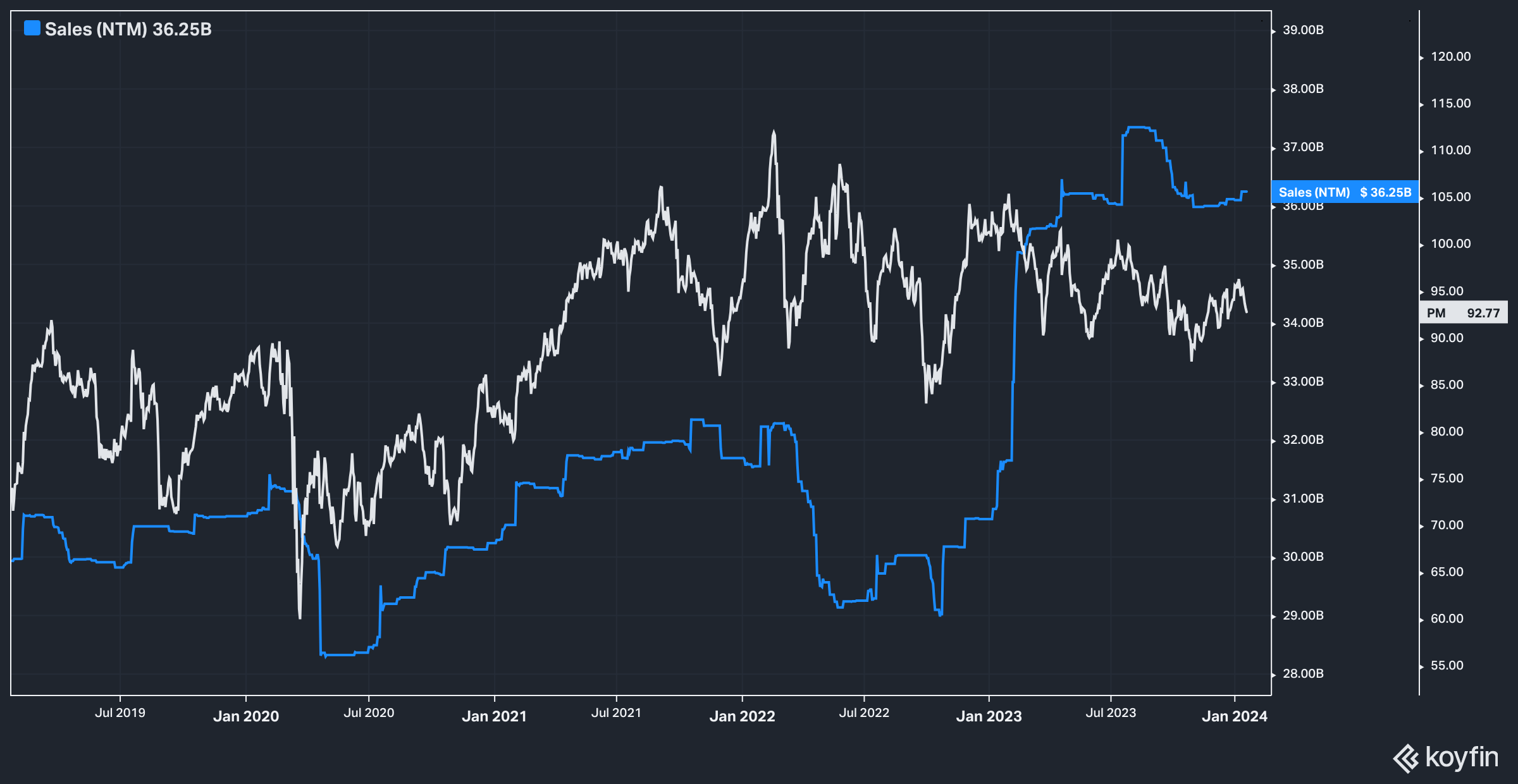

Supporting the idea that the stock is cheap at the moment is a break in the historic relationship between the stock’s price and forward sales estimates.

Koyfin

In the last five years, Philip Morris stock has largely traded above its forward sales estimates, with the stock roughly moving in synch with those expectations. As sales estimates slumped in 2022, the stock entered its current doldrum state.

2023, however, saw a spike in estimates sales estimates as the company’s acquisition of Swedish Match was completed and smokeless nicotine products were expected to make a major dent in the top and bottom lines.

The market seems to not have fully bought into this optimism, however, as evidenced by the relationship between the stock price and forward sales estimates–but we think this is likely to change over the next few quarters.

Looking ahead to fourth quarter and annual earnings, analysts estimate that the fourth quarter will bring in $8.9 billion in sales ($35 billion for the year), $3.25 billion in EBIT ($13.5 billion for the year), and $1.39 per share on a GAAP basis ($5.02 for the year).

We think that the company is unlikely to beat these estimates based on management guidance (discussed above) and the expected margin impact posed by higher device sales.

Longer term investors, however, may find reasons to be excited. Assuming approval for the IQOS Iluma in the U.S. market and continued adoption of oral products, EPS for FY2024 is expected to surge to $6.51, and $7.15 for FY2025, meaning that today the stock trades at only ~13x FY2025’s expected earnings.

The Bottom Line

We do not expect that Philip Morris will post a surprise to the upside in the coming quarter. As such, we do not view it as likely that the stock will re-rate higher in the very near term (meaning the next quarter). What we do expect, however, is continued adoption of oral products going in to FY2024 and further into FY2025, which we think could lead to a restoration of the stock’s historic relationship to sales. For these reasons, we think that the back half of 2024 will present a better opportunity for Philip Morris stock than the first half. Risks to our product are primarily regulatory, including the possible disapproval of the IQOS Iluma product in the U.S. market.

Q2 2024 Earnings Call Transcript")