Corporate profit margins are rising — again. This means that profit margins continue to postpone a decline from their well-above-average levels. For years we’ve been told that margins were reliably mean reverting: high profit margins would soon come down, while low margins would soon rise.

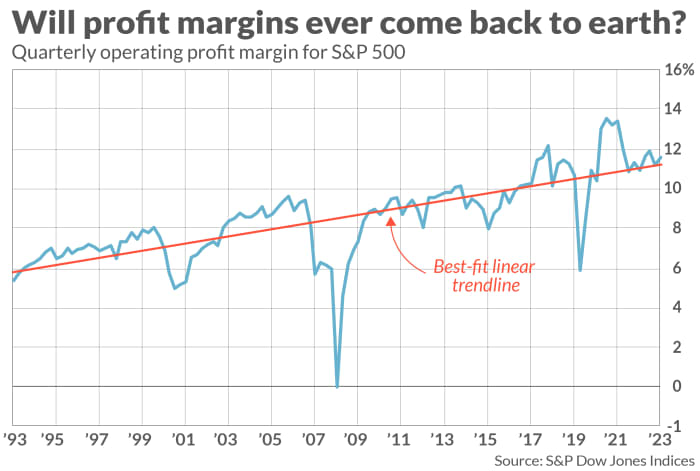

This has not been the case with S&P 500

SPX

companies over the past 30 years, however, as you can see from the accompanying chart. If there’s any reversion going on, it is reversion to a rising trendline rather than to any historical mean.

Could profit margins continue rising at this same rate for the foreseeable future? The standard theoretical answer is “no.” If the profit margin were to keep rising, publicly traded corporations eventually would attract so much capital from less-profitable pursuits that corporations’ profit-producing machine would reach the point of diminishing returns — thereby forcing margins to decline.

The bulls have a new comeback to this theoretical argument: AI changes everything. We’re on the brink of a pioneering era in which capital and labor don’t have to fight over shares of the economic pie, their argument goes. Productivity growth from AI will know no bounds, as will the return on capital.

You should be skeptical of this otherwise seductive story. Investors over the decades have been fed a steady stream of “new era” narratives, and invariably the exuberance to which those narratives led produced bubbles that burst. “This time is different” are the four most dangerous words on Wall Street.

A lot is riding on profit margins

The exuberant bulls are right about one thing: the stock market needs this “new era” narrative in order to justify its current lofty level.

To illustrate, consider what it would mean for the stock market’s future if the profit margin merely stays at its current level but rises no further. That is already a generous assumption, since the profit margin could conceivably decline significantly. But just staying constant at its current level has sobering implications.

That’s because, without margin expansion, stock market growth would hinge on just two factors: Sales growth and/or P/E expansion. Neither translates into a robust projection of future returns.

Consider first sales growth. It’s difficult to see how corporate sales can grow faster than the overall economy over the long term, and economic growth over the next decade is projected to be slower than the historical average. The non-partisan Congressional Budget Office, for example, is projecting that real (inflation-adjusted) GDP growth for the next 10 years will average just 2% annualized.

Yet even that estimate is too optimistic, since corporate sales over the long term grow at a somewhat lower rate than GDP. Historically, according to Rob Arnott, founder of Research Affiliates, sales growth has lagged GDP growth by around 0.9 of a percentage point, annualized. If the future is like the past, therefore, and the CBO estimate is accurate, sales growth over the next decade will average just over 1% annualized.

P/E expansion does not provide much hope either. The S&P 500’s current P/E ratio, based on trailing 12-month as-reported earnings per share, is 24.8, which is 55% higher than its long-term (since 1871) average of 16.0. The S&P 500’s cyclically-adjusted price/earnings ratio (CAPE) stands at 32.6, nearly double its long-term average of 17.4.

The bottom line? If the market’s P/E multiple stays at its current elevated level, expect the S&P 500 to beat inflation over the next decade by around 1% annualized. If that multiple declines significantly, watch out below.

Mark Hulbert is a regular contributor to MarketWatch. His Hulbert Ratings tracks investment newsletters that pay a flat fee to be audited. He can be reached at mark@hulbertratings.com

Also read: If this is all the downside the bears can deliver, then the bull market may still be intact

Q2 2024 Earnings Call Transcript")