Sean Gallup

Shopify (NYSE:SHOP) made a significant mistake in their logistics business in the past. Currently, their management is refocusing on their e-commerce platform, margin improvement, and expense management. Shop Pay has experienced tremendous growth momentum. I understand Shopify is a quite popular name among institutional and retail investors. However, the stock price is deemed to be 25% overvalued. Consequently, I am initiating coverage with a ‘Sell’ rating and a fair value estimate of $60 per share.

Past Missteps & Current Expense Management

Shopify’s management had ambitious goals in the past, expanding their business lines into a wide range of areas, including logistics. Their rationale for entering the logistics sector was an attempt to compete with Amazon (AMZN). However, Shopify lacked the robust experience and talent needed to operate the logistics business, leading to a significant burden on costs and profit margins. In June 2023, they finalized the sale of Shopify Logistics to Flexport, resulting in a recorded impairment loss of $1.34 billion on their profit and loss statement.

There are several reasons why Amazon can succeed in the logistics business while Shopify faces challenges. Logistic operations inherently require significant capital investment for warehouses and distribution centers. In other words, a substantial amount of cash flow is needed to establish a sizable logistics network. Shopify, at the time, was barely generating any free cash flow, making it difficult to support the financial demands of the logistics business.

In contrast, Amazon leverages its cloud business to finance both its e-commerce and logistics endeavors. Amazon’s cloud business serves as a lucrative cash cow, providing crucial support for their substantial capital expenditures. Additionally, Amazon’s massive scale in e-commerce contributes to the viability of its independent logistic network, a luxury that Shopify, as a smaller player, does not enjoy.

The positive development is that Shopify is now concentrating on its core e-commerce business and actively managing operating expenses. They are focusing on three main areas: headcount, marketing, and back office. For instance, in Q3 FY23, their stock-based compensation decreased significantly from $150 million to $102 million compared to the same period last year. These cost reductions are enhancing the company’s margin and significantly improving free cash flow.

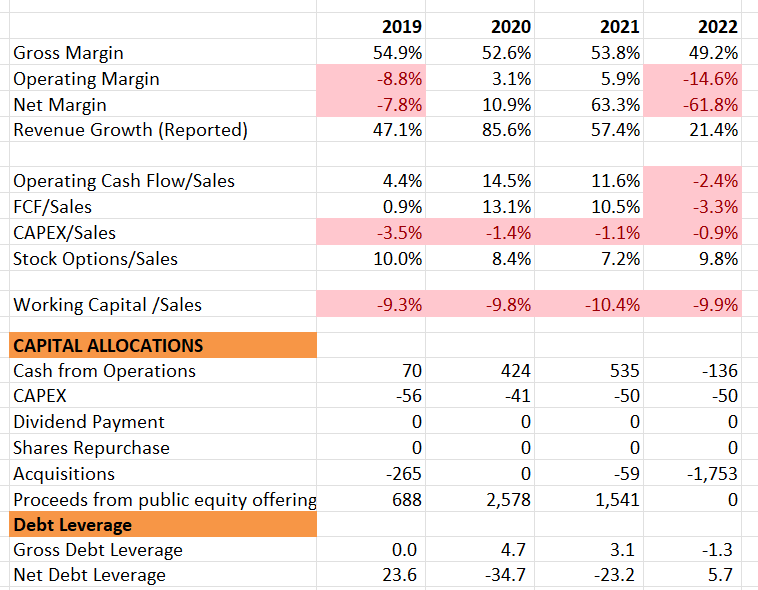

As depicted in the table below, Shopify has not generated substantial operating profits in recent years, and its free cash flow margin lags behind that of other platform companies. A pure focus on topline growth without meaningful margin expansion could face resistance from investors. Hence, it appears prudent for Shopify’s management to prioritize margin improvement and free cash flow generation.

Shopify 10Ks

Shop Pay Penetration Growth

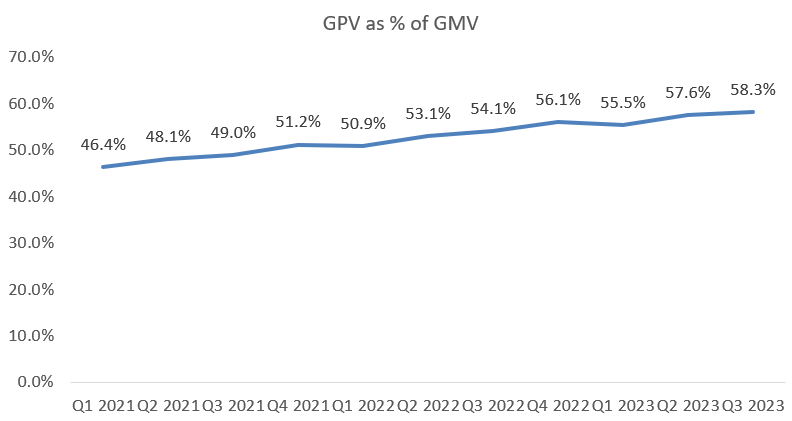

Shopify launched Shop Pay in 2017, and since its inception, it has exhibited remarkable growth. In Q3 FY23, the company disclosed that over 100 million buyers have utilized Shop Pay, facilitating $12 billion in gross merchandise volume during the quarter, marking a significant 50% year-over-year growth. The chart below illustrates the gross payment value as a percentage of gross merchandise volume, a crucial metric indicating payment penetration. This ratio has steadily increased from 46.4% in Q1 FY21 to over 58% in the most recent quarter.

Shopify Quarterly Earnings

I agree that Shop Pay is mission-critical for Shopify’s future success and growth. Firstly, the streamlined two-tap checkout process, requiring no additional code, significantly enhances the online payment experience for buyers. This simplicity not only expedites the checkout process but also contributes to an overall improved shopping experience. Consequently, Shop Pay is well-received by merchants, and this positive reception is reflected in the increasing penetration observed over time.

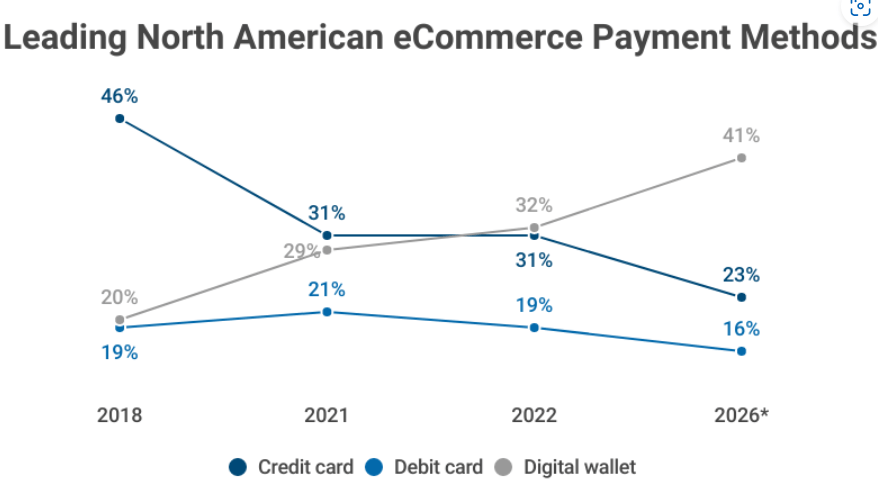

Secondly, according to CapitalOne, the expected growth of digital wallets is anticipated to increase e-commerce penetration from 32% in 2022 to 41% in 2026. This projected expansion in market penetration serves as a significant tailwind for the anticipated growth of Shop Pay in the coming years.

CapitalOne Research

Finally, Shopify has been actively investing in its Checkout platform and has introduced Checkout Extensibility, allowing merchants to customize their checkout interfaces. Notably, the checkout platform is fully compatible with Shop Pay. These product offerings are expected to enhance merchant loyalty and foster increased usage of Shop Pay.

Recent Result and FY24 Outlook

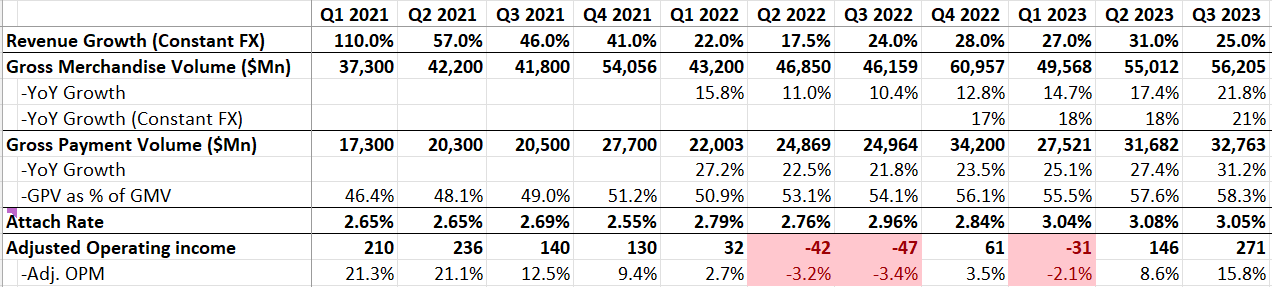

In Q3 FY23, Shopify achieved a 25% growth in revenue in constant currency, and the adjusted operating margin improved to 15.8%. Both Gross Merchandise Volume (GMV) and Gross Payment Volume (GPV) continued to experience rapid growth, as illustrated in the table below.

Shopify Quarterly Earnings

On the balance sheet, Shopify concluded with a robust net cash position of $4 billion. Thanks to the combination of top-line growth and margin improvement, the free cash flow increased to $276 million in Q3 FY23, a notable improvement from -$148 million in Q3 FY22. For the full-year guidance, the company anticipates revenue to grow at a mid-twenties percentage rate. Additionally, they project strong margin expansion in Q4 FY23, with the gross margin expected to improve by 300-400 basis points year over year.

Given their strong year-to-date results and the robust momentum in GPV and GMV, I have confidence in Shopify’s Q4 FY23 performance. Looking ahead to FY24, I anticipate that Shopify will maintain a growth rate of more than 25% in revenue, supported by ongoing margin improvement.

The introduction of Markets Pro, designed to facilitate international transactions for merchants, positions Shopify well for global expansion without undue burdens related to taxation and payments. After a significant success in the U.S. market in FY23, the plan to launch this service in other countries in FY24 is expected to contribute to additional revenue sources.

Furthermore, I anticipate continued growth in Shopify Pay in FY24. If the Federal Reserve begins to cut interest rates, it could potentially stimulate healthier consumer spending in FY24, benefiting Shopify. With continued control over staff hiring, reductions in marketing and back-office expenses, and the absence of burdens from the logistics business, I foresee Shopify’s margin expansion continuing in the upcoming fiscal year.

Valuation

The assumptions for FY23 align with their guidance, and I don’t anticipate any significant surprises in their Q4 FY23 results. As discussed earlier, my forecast for the company in FY24 includes a 25% organic revenue growth and 1.3% from tuck-in acquisitions. Looking further ahead, I project a gradual slowdown in their revenue growth rate to 10% by FY32, with acquisitions contributing an additional 1.3% to overall growth.

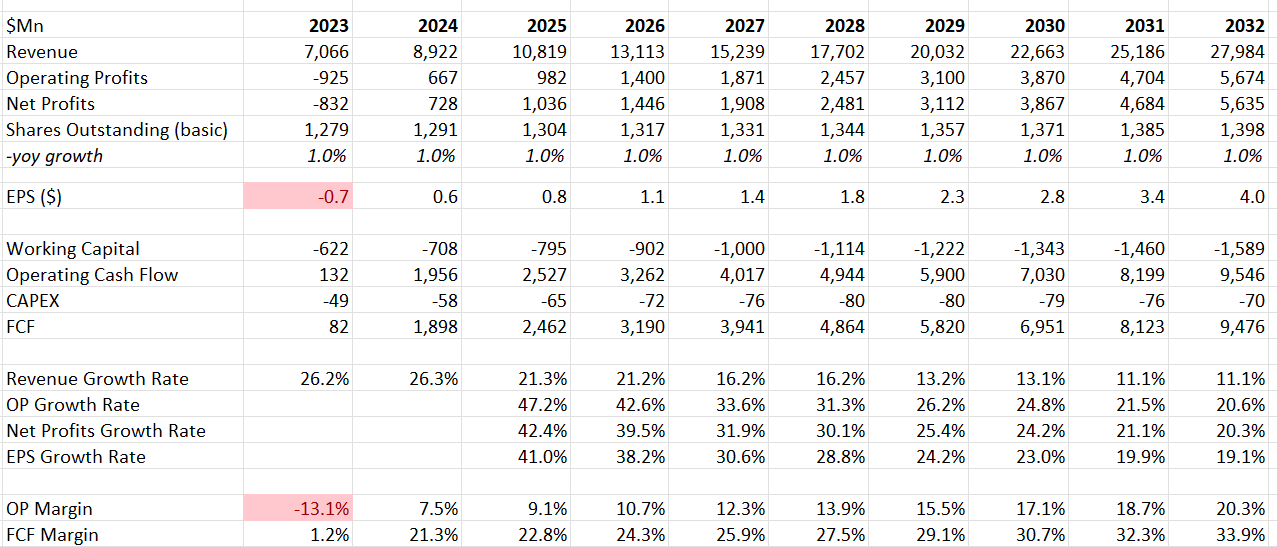

Given the company’s refocus on the e-commerce platform and proactive management of headcount and operating expenses, I expect their margin expansion to persist in the coming years. According to my calculations, I project their operating margin to improve to 20.3% by FY32, which seems to be a reasonable level for a software platform company.

Shopify DCF – Author’s Calculation

I am applying a 10% discount rate in the model, using the same assumption for all valuations. I assume a 5% terminal growth rate, believing that the company should grow faster than the overall GDP growth when it reaches business maturity. The fair value is calculated to be $60 per share, indicating that it is currently 25% overvalued at the present price. From the perspective of free cash flow multiples, the current stock price is trading at more than 40 times FY25’s free cash flow, and I believe the valuation is excessive.

Key Risks

Using the Platform to Scam Customers: As reported by the media, tens of thousands of sellers are allegedly utilizing the e-commerce platform Shopify to engage in scams and sell counterfeit goods. Unlike Amazon’s platform, which displays buyer reviews, Shopify’s e-commerce site operates with greater independence for merchants, allowing them to manage their sites individually.

Past Equity Offerings: In February 2021, the company issued 11,800,000 Class A subordinate voting shares at a price of $131.50 per share, raising $1.54 billion after fees. Generally, I am not in favor of public companies issuing new shares to raise funds, as it tends to dilute the existing shareholders’ interests.

Takeaways

I believe Shopify’s refocus on e-commerce is a smart move, and Shop Pay and their Checkout platform could drive their platform business growth in the future. However, the stock price is 25% overvalued; thus, I am initiating a ‘Sell’ rating with a fair value of $60 per share.

Q2 2024 Earnings Call Transcript")