24K-Production

Investment Thesis

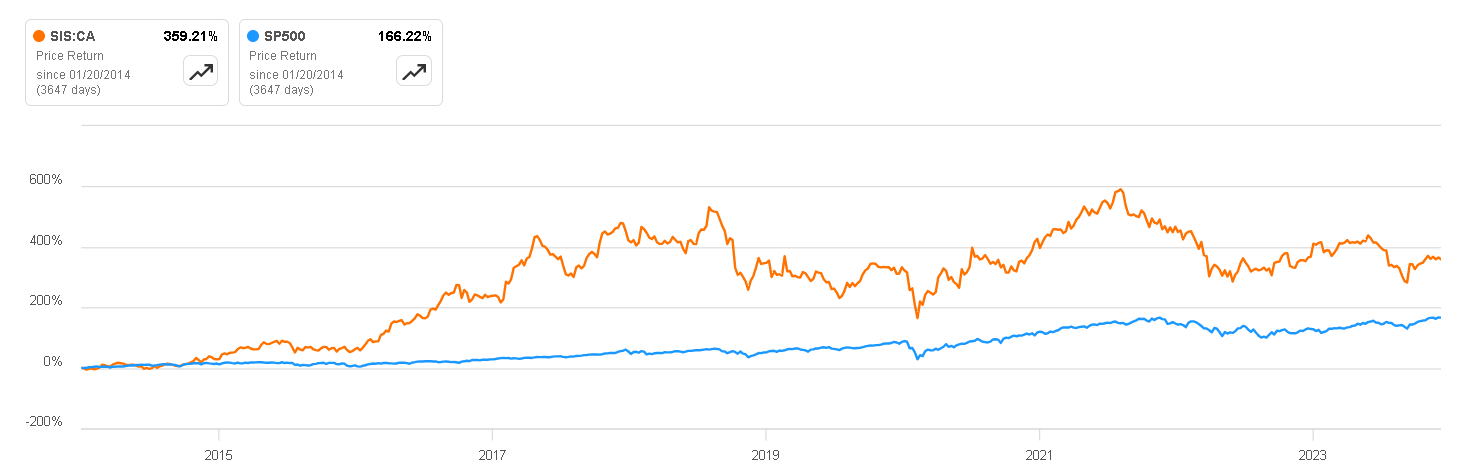

Savaria (TSX:SIS:CA) (OTCPK:SISXF) is a company operating a business with defensive characteristics and benefiting from tailwinds that ensure organic growth for decades. Coupled with various acquisitions throughout its history, this has resulted in a compound annual growth of its Free Cash Flow of 28% in the last decade. As a result, it is not surprising that the company has outperformed the S&P 500.

In this article, we will delve into the company’s business model and explore the various products it offers. We will discuss how the aging population benefits the company, address some concerns that should be monitored, and finally, conduct a valuation to justify why, at the current price, it deserves a ‘buy‘ rating.

Price Return vs S&P500 (Seeking Alpha)

Business Overview

Savaria specializes in the manufacturing and distribution of accessibility products, such as elevators, wheelchair lifts, and stairlifts. These products are designed to improve mobility and accessibility for individuals, such as the elderly or people with mobility challenges.

Savaria serves a diverse range of markets, including residential, commercial, and institutional sectors. The company has been in operation for several decades and has expanded its product offerings to address the growing demand for accessibility solutions. Currently, these products are segmented into three categories:

Accessibility

In this segment, Savaria designs and produces mobility products such as stair lifts or wheelchair lifts. These products are utilized by private clients who wish to install them in their homes, as well as corporate clients such as shopping centers or public institutions that install them to enhance the experience of users with disabilities or mobility challenges.

An interesting aspect of this segment is that once the equipment is installed, at some point, it is likely that damage will occur, requiring repair by a technician. Savaria, being the manufacturer, can provide the necessary technical support with high profit margins, as it only requires sending a technician for repair. In the last annual report, they did not specify the amount of revenue generated by these services. However, in the FY2021 report, the company indicated that almost $67 million CAD (10% of revenue) was generated in these services, and it could be a growth opportunity with high margins.

This segment represented 71% of revenue during FY2022, has grown 38% annually since 2017 (both organically and especially inorganically), and according to the company, it is the segment with the highest Adjusted EBITDA margins (almost 18% during FY2022). Therefore, it seems to make sense that it would have so much relevance in sales.

Accessibility Products (Savaria)

Patient Care

The Patient Care segment is typically more focused on corporate clients such as hospitals, senior centers, among others, where individuals who require a high-care resting place are usually accommodated. These products include lifts for transferring patients from a wheelchair to bed or bathroom, hospital beds, or beds with therapeutic designs.

This segment has grown 30% since 2017, again with the help of acquisitions, and currently represents 22% of revenue. Additionally, it is the second segment with the best Adjusted EBITDA margins (14% during FY2022).

Patient Care Products (Savaria)

Adapted Vehicles

In this segment, the company designs and implements modifications to minivans so that they can be used by people with reduced mobility. This applies to clients who want to use them in their daily lives and to commercial clients, such as ambulances, firefighters, paramedics, nursing homes, among others.

This segment has experienced an annual growth rate of 15% since 2017 and currently represents only 7% of the total revenue. Moreover, it maintains an average Adjusted EBITDA margin of only 8%, solidifying its position as the weakest of the three segments. This fact likely prompted management to make the wise decision to divest a significant portion of this business segment, particularly in the Norway division.

In addition, the corporation experienced a decrease of 3.9% due to the divestiture of the vehicle division in Norway in the quarter.

CFO Stephen Reitknecht on Q2 conference call

Adapted Vehicles (Savaria)

It can be noted that each of the company’s segments addresses very critical needs related to people’s health and mobility. Therefore, while sales may be affected in a difficult macroeconomic environment where people are not willing to make such heavy spending or corporate and public clients decide to allocate their resources to other aspects, the almost indispensable nature of the products means that sooner or later, they have to be purchased regardless of economic conditions.

This can be better observed when looking at the company’s performance during the great financial crisis of 2008 and the most recent one in 2020. In both instances, the company’s revenue decreased only by 5%, while its operating margin remained solid. This shows us a business that, although not immune, does have a certain resilience in the face of unexpected crises.

Author’s Representation

Population Aging: A Tail Wind

Another particularly attractive quality of the company is that it operates in a sector that has structural tailwinds, favoring growth in the coming years, even decades. This is based on the fact that the world population continues to grow year after year, and advancements in science have significantly improved life expectancy.

In the following graph, we can see that the increase in life expectancy is gradual, and except for the ‘bump’ caused by COVID-19 in 2020/2021, the increase is quite sustained.

U.S. Life Expectancy (Health System Tracker)![]()

An increase in population, coupled with an improvement in life expectancy, results in more and more individuals reaching adulthood, leading to an increased need for equipment that helps improve mobility.

This trend is particularly noticeable in Europe, where the percentage of older adults in the population is the highest in the world, and the expectation is that this will continue. It is not surprising, therefore, that Europe and North America make up 100% of Savaria’s revenue and are the main growth drivers for the coming decades.

% of Population Over 60 Years (Research Gate)

Key Ratios

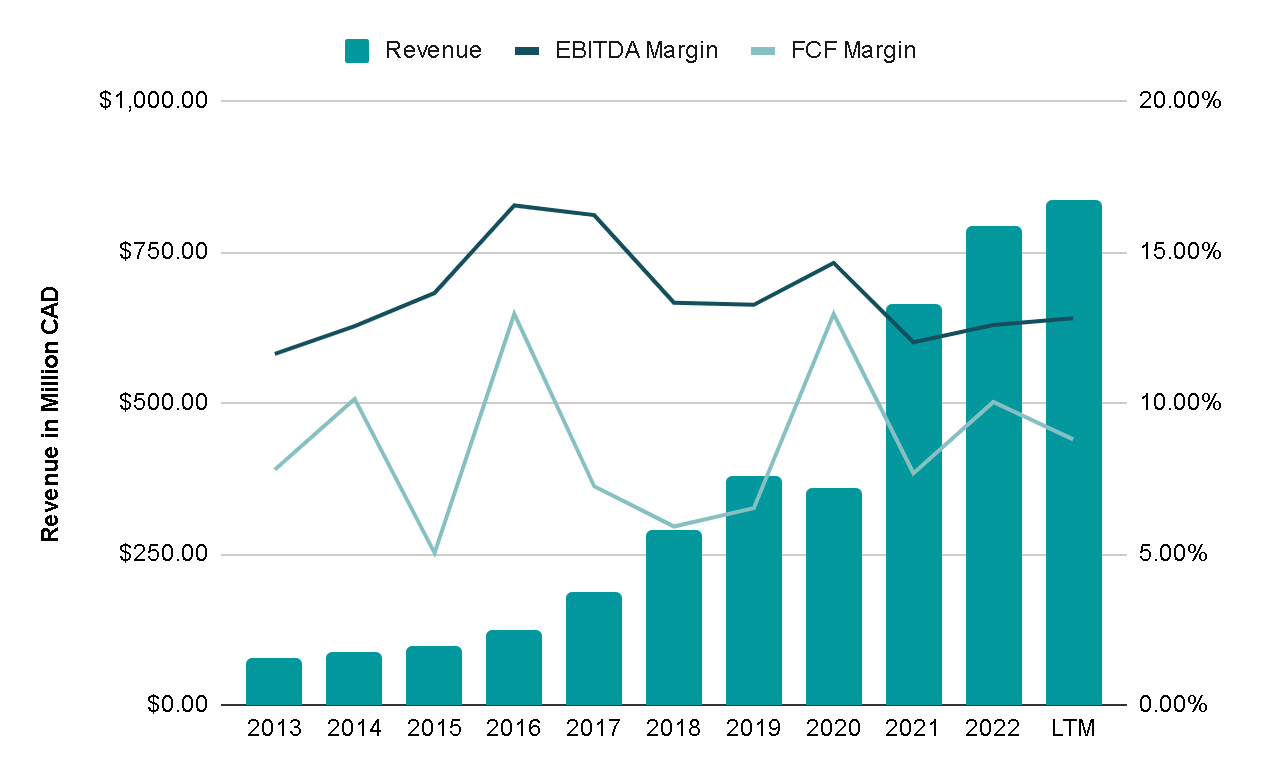

The company’s revenue has grown by 27% in the last decade, although we cannot observe any improvement in the margins, as they have remained around an average of 12-13% for EBITDA and 8-9% for Free Cash Flow.

Author’s Representation

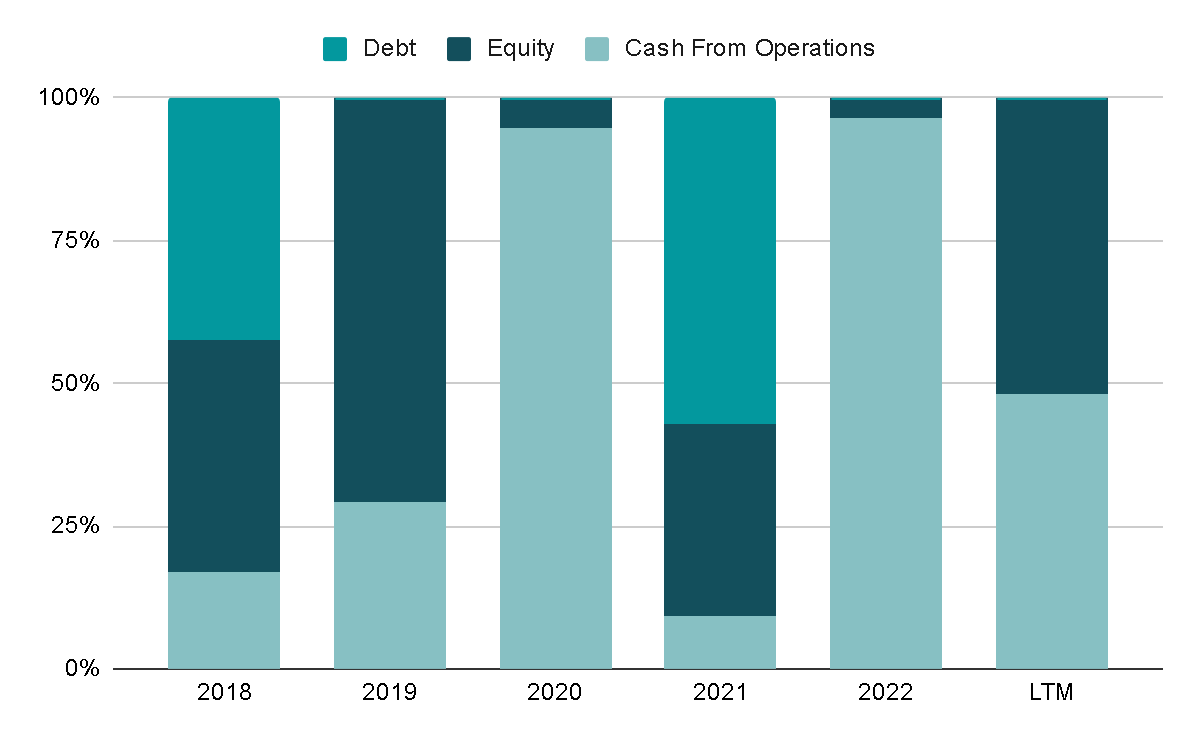

In the last five years, the company has utilized all its tools to finance its operations. Specifically, 40% of the capital has come from the issuance of debt, which has been used during times when the company makes acquisitions. Mainly, 34% has been from the issuance of shares, and the remaining 26% has been the cash generated by the operations of the business.

Author’s Representation

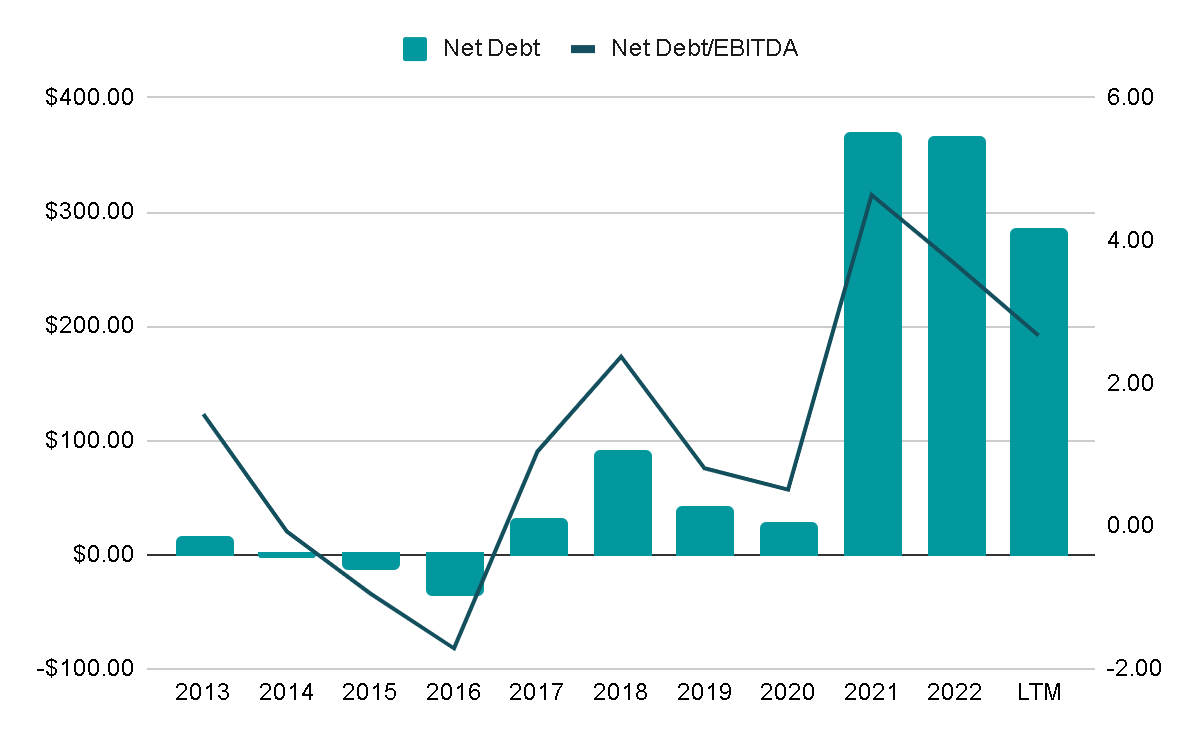

When I first encountered the company in 2021, it seemed uninvestable to me due to its high amount of debt, with a Net Debt/EBITDA ratio of almost 5x. However, the company has dedicated its efforts to reducing this level of leverage, and currently, the ratio is already around 2.7x, thanks to allocating almost $100 million annually to pay down debt.

If the company continues on this path, it could become much more attractive, as it would be a debt-free company in a stable sector, paying a good dividend.

Author’s Representation

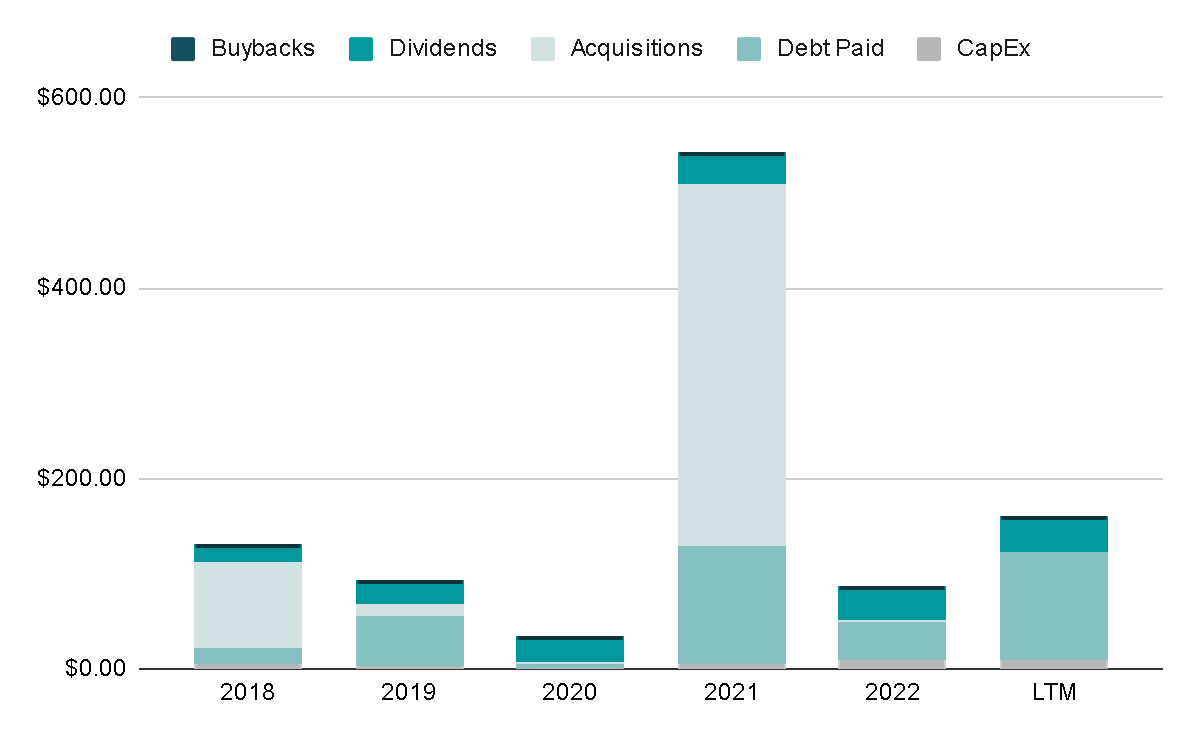

This capital has been used, as mentioned before, with 53% allocated to make acquisitions, such as that of Garaventa Lift in 2018 for $100 million CAD or the Handicare Group in 2021 for just over $360 million CAD. You can observe the correlation between making an acquisition and issuing debt and shares.

The remaining funds have been used to repay the debt issued, invest in the business through CapEx, and pay a dividend that currently has an almost 3.5% yield, representing almost 90% of the Net Income generated.

Author’s Representation

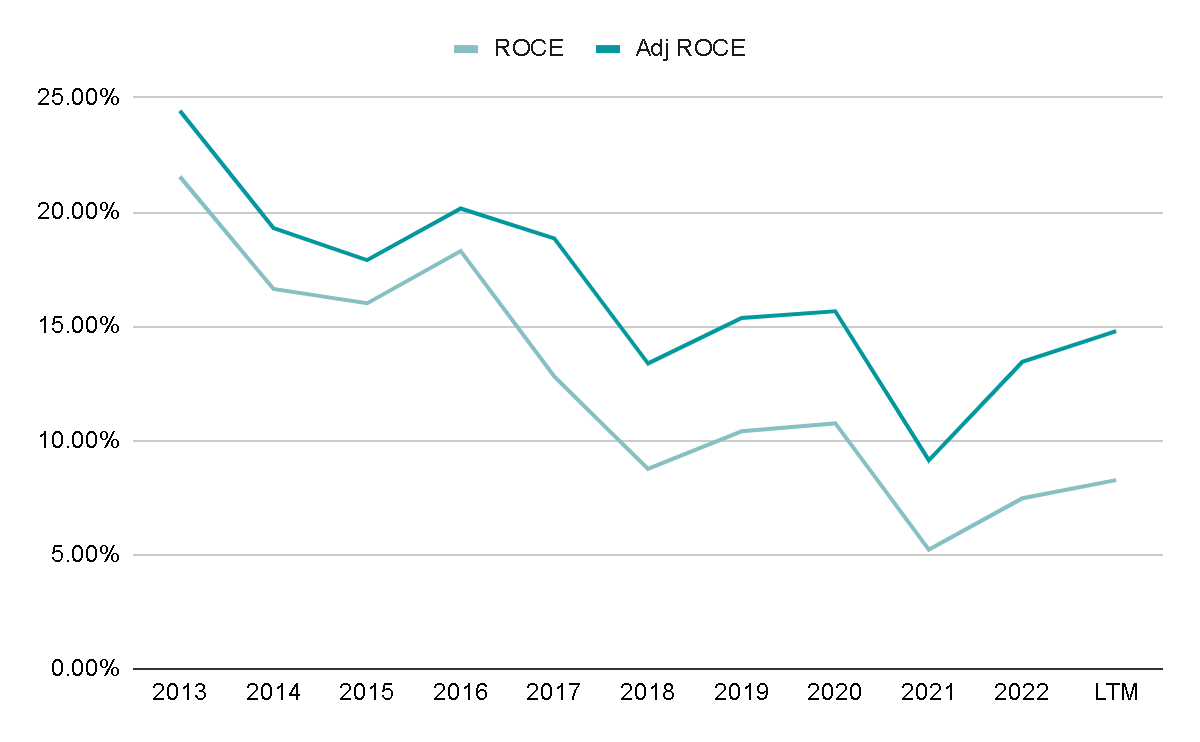

One aspect that concerns me is the constant decrease in Return on Capital Employed over the last decade. Examining the competitive landscape, it doesn’t appear that this decline is solely due to competition, as there are few companies operating in the sector. For this reason, acquisition targets tend to be relatively large in size, such as Handicare, the latest acquisition, which during FY2020 generated $295 million CAD compared to the $350 million CAD that Savaria generated at the time of announcing the acquisition.

This decrease could indicate poor capital allocation decisions over the years, both in the acquisitions made and in the new products manufactured by the company. It’s a worrisome sign, and I would like to monitor this situation closely in the coming years since when returns are not keeping pace with the capital employed, there could be an impact on the company’s overall financial health.

Author’s Representation

Valuation

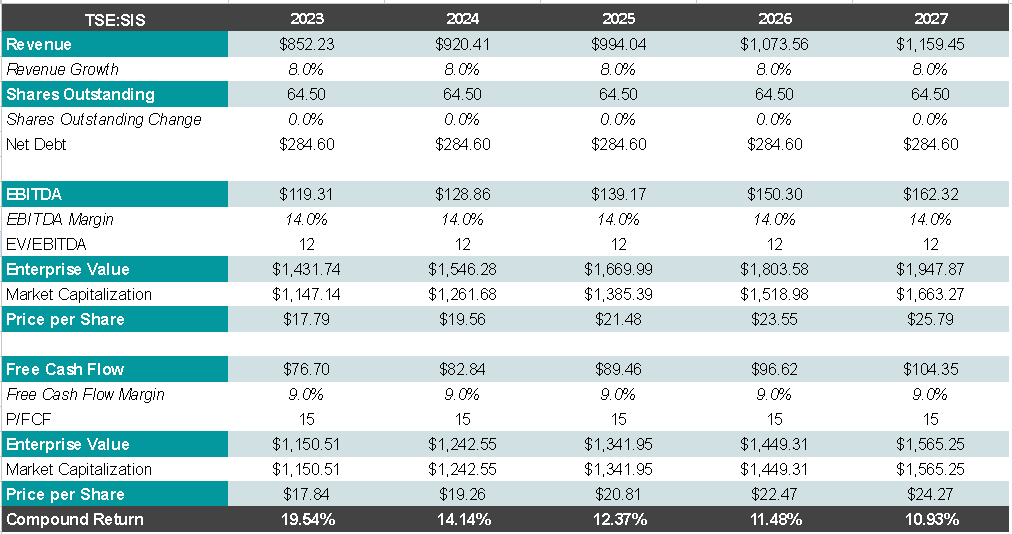

Assessing the company’s growth is somewhat complicated because acquisitions usually contribute significantly to both growth and margins, which are not always predictable, though they typically oscillate within a certain range. However, in recent quarters, the CEO has been discussing the goal of reaching $1 billion in revenue, so I’ll use this as a guide.

I see on the year 2024 and 2025 to reach our $1 billion of sales. And I mentioned on past call that we have to have objective of 20% of EBITDA. For sure, nothing is easy, but we are very confident to achieve both EBITDA and sales.

CEO Marcel Bourassa on Q3 2023 conference call.

This objective is expected to be achieved between 2024 and 2025, thanks to a mix of finishing integrating Handicare, organic growth of between 8 and 10% for the Accessibility and Patient Care segments due to cross-selling initiatives, strong demand, and price increases. However, I will be somewhat more conservative and assume that this objective will be achieved by 2026, and we will maintain average margins of 14% EBITDA.

With these assumptions, if we were to buy at the current price and expect an exit multiple of 12x EV/EBITDA and 15x Free Cash Flow, the compound annual return would be between 10% and 12%, plus the dividend yield of 3.5%

Author’s Representation

Personally, I find this to be an attractive return, considering I’m being very conservative on sales growth, margins, and valuation multiples. Therefore, the likelihood of this return being better than projected is high.

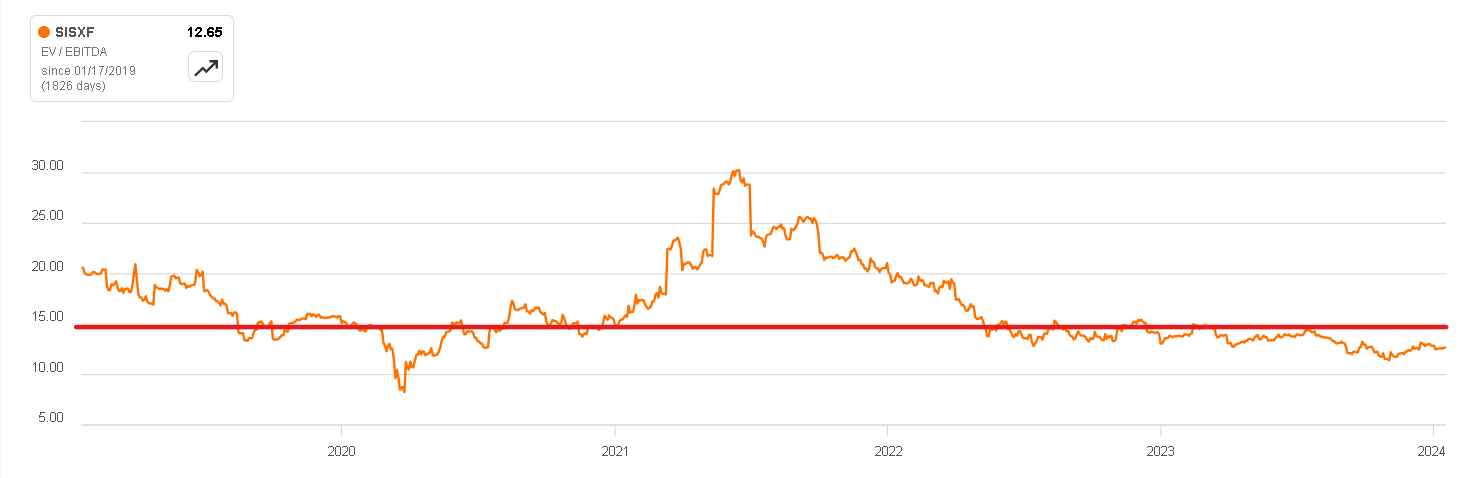

The average EV/EBITDA multiple since 2019 has been 15x, which is quite reasonable given the stable nature of the business. Again, the return looks good, considering my conservative estimates, and the chances of performance being better than my estimate are elevated.

EV/EBITDA Ratio (Seeking Alpha)

Final Thoughts

The company operates in a market where future growth is expected to be limited. However, it has a product that is practically indispensable to its customers, providing a degree of solidity in the face of crises, as we already saw in 2008.

On the other hand, it seems relevant to mention that the greatest risks and concerns are continuing to reduce debt in the coming years, seeing an improvement or at least stability in margins, reversing the trend of a decrease in the return on invested capital. It’s important to remember that Savaria is not entirely immune, so during economic contractions, individuals and businesses may cut back on spending, leading to a temporary decrease in demand for Savaria’s products.

Despite these considerations, I find the current valuation to be very attractive, and the risk/reward ratio more than offset. Therefore, I have decided to assign a ‘buy‘ rating.

Editor’s Note: This article discusses one or more securities that do not trade on a major U.S. exchange. Please be aware of the risks associated with these stocks.

Q2 2024 Earnings Call Transcript")